Gold’s next move

In his latest video, Jeffrey Christian of CPM Group reviews the latest developments in gold, silver, platinum, and palladium markets, explaining why prices are rising again and what may come next. He discusses the recent price movements in gold and silver, including the sharp rally earlier in the year, the pullback following Federal Reserve policy signals, and the renewed strength tied to political tensions and broader concerns about global economic stability. Jeff also addresses recent commentary around Russian gold sales, clarifying how the Russian central bank has been managing its reserves since the start of the Ukraine conflict and why recent sales are not unusual in that context. He then turns to the growing interest in hedging, particularly among mining companies, and explains how producers and investors can protect profits while maintaining upside exposure.

Click here to watch.

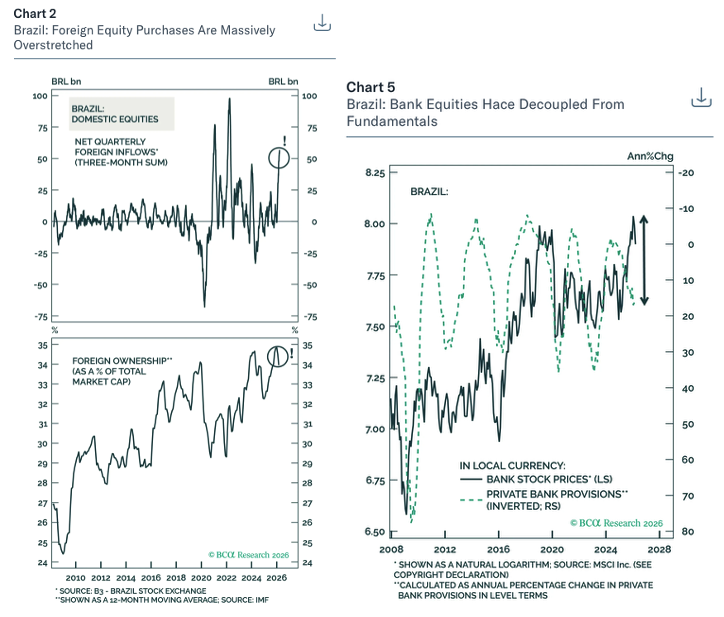

Brazil: Overhyped

Report by

BCA Research

BC

Should investors buy the dip? The BCA team think not. The recent bull market has been fuelled by unsustainable foreign inflows and is massively overstretched (see left chart). The divergence between rising stock prices and worsening macro fundamentals has become untenable (right chart) – investors are too sanguine. Domestic demand will worsen, with odds of a recession rising for the next 6-12 months. The only factor that can prevent such a drastic economic slowdown is major fiscal easing, yet this would cause markets to sell off. Some investors argue that high commodity prices will bail out Brazil, which is theoretically correct, yet in the past this has brought down equities due to the global growth recession it causes. Commodities also matter far less to Brazil’s stock market today. Stay underweight Brazil in equity and fixed-income portfolios. The team also recommend a new short-term trade (three-month horizon): Pay 10-year Brazilian swap rates.

US: The Private Credit Crunch

US money and credit growth has slowed over recent weeks, and Andrew Hunt believes the Private Credit Crunch may be intensifying. If private finance had indeed become the principal source of external funding over recent years for the now significantly cash flow negative US corporate sector, then the ongoing problems in the private channels will now be causing a binding credit crunch that will likely further suppress economic growth, even before the impact of higher energy prices. This will impact the AI sector. The impact of the Big Bill may offer some near-term support to growth, but Andrew suspects that by Q2 the economy may be soft – a recession may be due to arrive in H2. Investors can expect the FRB to remain active in the debt markets and to press ahead with rate cuts next quarter. If global capital flows continue to stall then the USD will weaken. Under this scenario, UST yields could continue to rise until the FOMC is forced into YCC.

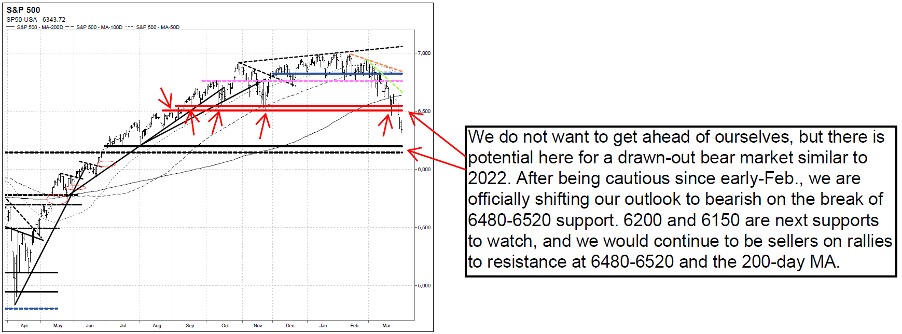

US: Down to bearish

The Vermilion team are officially downgrading their outlook to bearish with the S&P500 (SPX) violating major support at 6480-6520, Nasdaq futures (NQ) violating 24,000 support, and the Russell 2000 (IWM) breaking down below crucial $245 support. This comes the team downgraded their outlook to neutral early in March. Concerns that they discussed since early-February stemmed from deteriorating market dynamics, and ever since then they been concerned about a deeper pullback, likely to 6720-6776, 6690, or 6480-6520 on SPX, while also discussing since mid-March how downside capitulation is likely needed before finding a reliable bottom. With continued deterioration in market dynamics, their report last week discussed how they were closely watching for a breakdown below 6480 and that the SPX likes to test the 200-day MA as resistance (from below) before continuing lower, and this is likely what happened on 3/23/26. 6200 and 6150 are the next supports to watch, and they would continue to be sellers on any rallies to 6480-6520 and 200-day MA resistances.

Turning cautious ahead of the obvious

Konstantin Fominykh’s tools turned cautious before the markets saw the obvious, having initiated sell signals on the S&P500 and US industrials on Feb 9th (before the 9% and 8% drops), US healthcare since Feb 3rd (7% drop), US tech (11% drop) and Bitcoin (38% drop). The Middle East situation is worsening. Private credit signals a prolonged contraction; default rates appear low on the surface, but adjusted measures suggest significantly higher stress, with effective defaults closer to ~6.4%. Konstantin is selling US financials. He also remarks that the AI/tech trade is not working because everyone already owns a lot of it, and has a fresh sell on AI and Next Gen Software ETF (March 23rd). There is a likely recession ahead catalysed by a reversal in AI capex and the energy supply shock; expect earnings to peak Q1-Q2. Investors were spoiled by the 16-year bull market, so it’s no surprise that people still believe in "strong earnings" and "buy the dip".

Financials

The market is missing a key earnings driver as ~20% of AUM is currently fee-free but will convert to fee-paying over the next 6 years. This creates a LDD CAGR on the top line without requiring market growth. With a largely fixed cost base, STJ can deliver ~10 points of margin expansion through 2030. Additional bull points flagged include STJ’s success in capturing the next generation of wealth (one third of clients are under the age of 40); while AI-driven efficiencies could unlock ~30% productivity gains and further consolidation within the advisor ranks. The stock trades on ~15x depressed earnings but ~5x 2030 earnings, with ~70% of cash returned via dividends and buybacks. TP £22.00 (80% upside).

Technology

A broken IPO trading ~60% below its $25 listing price, with potential to double over the next year and deliver a 3x return over 4 years. Recent share price weakness is due to a market that has indiscriminately punished the entire software sector, as well as the company's usage yield compressing, which bearish analysts have misinterpreted as an erosion in pricing power. NAVN is the technological leader in a $185bn corporate travel and expense market, disrupting legacy incumbents with a unified platform and a differentiated model. The stock trades at ~2.9x EV/FY26 sales based on guided revenue of ~$685m - a clear dislocation for a platform growing ~29% with 74% gross margins and 13% operating margins. A path to 30%+ margins exists at scale. The setup is likened to Booking.com in 2009 when it was trading under $100/share.

Silver futures (SIK26) forecasts

With the attainment of the new low under 78.06, the Technical Analysis Group have closed half of their NT Strategic Short position, established into strength at 95/96, and are placing a trailing stop at 87.70 on the remainder of the trade. Price action from 97.30 has yet to reveal any urgency or impulsiveness to the downside. The team are expecting near term relative outperformance in gold vs silver, and are bullish the 'RATIO' whilst above 57.59, seeking upside in the near term to 67 +/-, and 72.66+. Since raising risk, they have seen a +12% rise to 64.47. The team continues to remain long term bullish and regardless of whether or not they’re in the higher degree 4th wave, they do not expect downside under their proposed 60 +/- 10 LT Long Term Range Base, before ultimately eclipsing this year’s 121.78+ high in the resumption of the underlying bull trend, exposing their next major upside attraction levels of 138 and 165 (see chart).

Iran: The War in English

The “War in English”, as jokingly referred to by Israeli officials, has settled into an intense but steady pace. Niall Ferguson believes that US and Israeli objectives remain on track despite a geopolitical expansion of the war. Should Iran prove unable to muster larger missile or drone salvos by the end of the week, it would seem likely that it has no remaining capacity to do so. This should give shipping firms and insurers more confidence to begin transiting the Strait of Hormuz next week. If disruptions to the Strait continue into next week, Niall expects a major and coordinated SPR release from net importers to take place to reduce the stress in global crude markets. However, the potential costs of a protracted conflict and closure of the Strait is being underestimated by markets. It is imperative not only for the Trump administration’s political self-interest but also for global economic stability that the duration of this war be measured in weeks, not months.

Consumer Discretionary

Hedgeye provides updates on 3 of their top Retail shorts. For GIII, they expect the next guide for the year to be an absolute disaster; forecasting a 20%+ cash flow hit from the the loss of major Calvin Klein and Tommy Hilfiger licenses back to PVH, while prior channel stuffing and tougher retail conditions could force the company to increase markdown support to key partners. Meanwhile, VFC is caught between a heavy debt burden and weakening brand momentum; Hedgeye believes a massively dilutive equity raise will ultimately be required. And finally, DDS remains a mispriced security, trading at ~12x EBITDA despite a sharply decelerating model and the company overearning by 800-1,000bp. That suggests that the real earnings power is between $10-20 per share. 5x earnings, is an appropriate department store multiple, suggesting 80-90% downside.

Healthcare

Sidoti reiterates their constructive stance on LMAT, arguing the company’s increasingly dominant niche positioning supports durable pricing power, margin expansion and visible multi-year growth. With price increases contributing meaningfully to organic growth and ~8% additional pricing expected in 2026, Sidoti sees LMAT as insulated from reimbursement and tariff pressures given its focus on critical, non-deferrable vascular procedures and predominantly single-use devices. The company will continue to benefit from the continued sales force expansion and additional European product approvals over the next several years. Backed by a strong balance sheet and capacity for accretive M&A, Sidoti increases their 2026 revenue estimate to $275.5m (from $264m) and EPS estimate to $2.86 (from $2.39). For 2027, they raise their revenue estimate to $291m (from $278m) and EPS estimate to $3.09 (from $2.67).

Technology

US expansion is the key swing factor for TEMN over the next 12 months. With a well-resourced US sales team, a localised product suite and a pipeline growing faster than any other region, GR20 sees favourable conditions for deal conversion in 2026. They also believe the recent “Claude Cowork effect” that weighed on software valuations is fading, with sector multiples appearing to have bottomed. In GR20’s view, current valuations imply limited terminal value in DCF models - an anomaly given TEMN’s positioning and growth prospects. The stock trades at an undemanding 4.2x/3.9x 2026/27 EV/sales and 11.9x/10.9x EV/adjusted EBIT.

Materials

Lucror broadly agrees with Moody’s downgrade, consistent with their “Negative” Credit Bias since Aug 24. Weak metrics are set to deteriorate further amid higher-than-budgeted capex at the Awak Mas gold project and subdued thermal coal prices. Leverage is projected to rise to c.7.0x Debt/EBITDA in FY26 (from c.6.0x in FY25) before easing toward c.4.0x in FY27 as gold operations stabilise. Liquidity is viewed as adequate over the next 12-18 months, but covenant headroom will tighten, particularly around the 3.75x Net Debt/EBITDA test. That said, the Newcastle coal benchmark has stabilised for almost a year now, so, Indika’s credit metrics may not worsen much more going forward and Lucror agrees with Moody’s outlook revision to stable. They maintain a "Buy" recommendation on the INDYIJ 8.75 '29s at 99.6/8.9%/2.7Y, as the high yield more than compensates for the weak and deteriorating credit profile.

Gold & Silver: Where prices move from here

In this presentation, Jeffrey Christian of CPM Group discusses what comes next for gold, silver, platinum, and palladium following last week’s sharp selloff, and explains why the pullback was not surprising after the rapid surge in prices. Jeff begins by looking at the US dollar, showing why claims of a “collapsing dollar” do not hold up. He emphasizes the importance of time horizons in market analysis, explaining how prices can be unsustainably high or low in the long run while remaining volatile for months or even years in the short run. Jeff then looks at the role of COMEX contract rolls and positioning, including how large open interest can affect price moves without implying any shortage of metal. He also reviews ETF activity across gold, silver, platinum, and palladium, explaining how gold ETF investors were net buyers through January, while silver ETF investors were net sellers, even as prices spiked.

Click here to watch.

Communications

Josh D’Amaro’s mix of leadership and operational qualities make him a strong choice to succeed Bob Iger as CEO. A 27-year Disney veteran, D’Amaro is viewed as a high-EQ leader who balances creative ambition with financial discipline. He is currently tasked with overseeing a $60bn capital plan over the next 10 years to turbocharge growth in parks, cruise lines and resorts, generating the FCF required to support the company’s riskier media transformation. While he lacks direct media experience, he has a proven track record of turning around underperforming assets and successfully navigating crises, including rebuilding the Experiences’ division profitability post-Covid. Paragon’s report includes interviews with former senior executives who worked with D'Amaro for more than 75 years combined.

Materials

Asymmetric highlights Daido Steel as an under-followed stock that is increasingly coming into its own. The stock has surged ~85% since they turned bullish in Jun 25, helped by a strong H1, driven by rare earth free magnet demand amid tighter Chinese export controls and robust marine valve orders. Even after the rally, Daido only trades at 0.86x PBR and ~13x FY3/27E earnings (+20% Y/Y), with relatively low foreign ownership. Looking ahead, Asymmetric flags multiple profit catalysts: potential synergies from acquiring Kobe Steel’s Koshuha specialty furnace, an improving semiconductor cycle, rising demand for rare earth-free magnets for HEVs, and expanding exposure to engine shafts and components across aerospace, energy, shipping and gas turbines - supporting margin and earnings upside over the next 1-2 years.

US Healthcare + Merger / Arb Catalysts: What’s next from DC

Healthcare

2026 is shaping up to be an active year for US healthcare policy, with President Trump's focus on affordability impacting Congressional and Administration priorities. Near term, Congress is considering spending legislation impacting clinical labs (Quest Diagnostics, Labcorp), diagnostics (Natera) and life science tools (Danaher, Thermo Fisher). Investors are also awaiting clarity on MFN deals and their impact on companies that have not yet signed agreements with the Administration. Beyond HC, Aldis also leverages their connectivity to provide timely insights and updates around M&A with regulatory catalysts, including Nexstar-Tegna and Union Pacific-Norfolk Southern. Contact us below for further information on events hosted by Aldis and access to their content library.

Earnings season screens

Mill Street has developed an "Earnings Screen Score" ranking methodology that draws on selected inputs from their MAER (Monitor of Analysts’ Earnings Revisions) stock database to identify companies which have strong near-term fundamental momentum going into an earnings report. Mill Street’s research indicates that companies scoring highly in their ranking have a much higher chance of near-term improvements in analyst expectations than those that score poorly. Stocks most likely to produce positive near-term analyst estimate activity in the next couple of weeks include Lam Research, Regeneron Pharmaceuticals and Teradyne. Bottom ranked stocks include LyondellBasell, Eaton and Marathon Petroleum. Click here to access the full report.

Materials

GMR is sceptical on a potential tie-up between RIO and GLEN, citing material integration and execution risks. They highlight stark contrasts in management culture and business models, alongside challenges around thermal coal exposure, sovereign risk tolerance and regulatory scrutiny given combined copper output. Assuming US$1.5bn of annual synergies, GMR estimates RIO could bid up to £5.40 per GLEN share for the merger to be, on average, neutral on Earnings/share and NCFO/share out to 2028. Following GLEN’s recent rally, GMR downgrades the stock to Hold and moves RIO to Sell on deal risk. Their proprietary Acquisition Rationale score reinforces caution: GlenRio scores just 9/18, a level that historically underperforms peers over the next 24 months.

Precious metals: What happens next?

In this presentation, Jeffrey Christian of CPM Group provides a market update on gold, silver, platinum, and palladium prices as metals continue to reach record levels. He explains why political developments, both in the United States and internationally, have become one of the dominant drivers of investment demand for precious metals, moving away from traditional economic fundamentals. Jeff discusses how rising political uncertainty and strained international relationships contribute to elevated investor anxiety and renewed buying interest in gold and silver. Jeff also addresses persistent misinformation in the silver market, including claims about shrinking inventories, paper versus physical silver, and alleged shortages.

Click here here to watch

Venezuela: The knock-on effects of kicking out Maduro

According to Jose Ignacio Hernandez, Maduro’s sudden removal marks a political shock that forces Washington to rethink their oil-sanctions enforcement, OFAC licensing, recognition, and Venezuela’s long-frozen public-debt problem. Delcy Rodríguez enters office structurally weak and politically exposed, constrained by internal Chavista power balances and demands from Washington. The next 4–6 weeks will be decisive. If Rodríguez stabilizes her position, a second phase opens—bringing selective movement across oil policy, creditor engagement, asset strategy, and recognition. Aurora’s latest report lays out what is most likely to change, when, and under what constraints, including the outlook for OFAC licensing, the pending Citgo sale, creditor engagement, and US recognition policy. Jose says that contingent on Rodríguez remaining in power, gradual liberalization of sanctions—particularly in the oil sector—could become conceivable. This might include expanding Chevron’s license and granting new, limited individual licenses to select international oil companies.

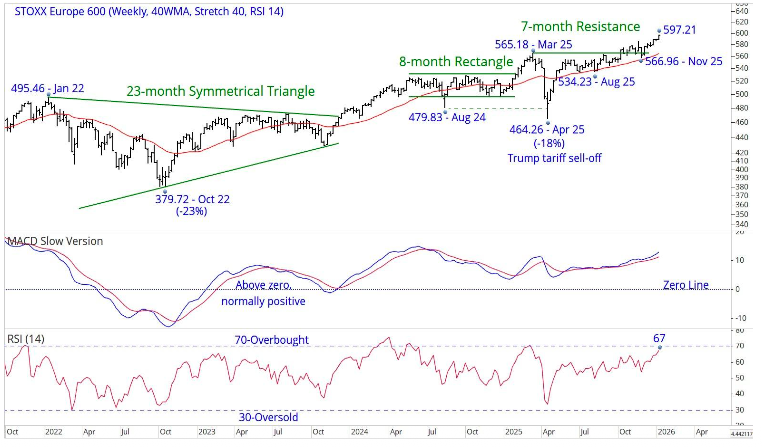

A taste of Europe

The STOXX 600 (596.14) has started 2026 with a new ATH, trading as high as 597. Next resistance is at 600, but this is not expected to be a significant obstacle. Chris Roberts’ minimum long-term target stays at 800+. That level is derived from the breakout above the 21-year ceiling around 400. The minimum expectation for a sustained breakout above a multi-year ceiling is a doubling of that ceiling. The 14-week RSI is currently at 67, just below the 70+ overbought zone. MACD has been above zero since Jan 2023. Chris remains 50% long from 576.29. The recommended stop stays at a daily close below 527.00.

Industrials

Under its new CEO, CHRW has implemented a lean, AI-enabled operating model that has enabled the company to grow earnings despite struggling topline growth. Abacus expects EPS to average ~19% CAGR over the next 3 years, even without any help from a cyclical recovery, highlighting exceptional operating leverage and incremental margins of ~100%. Importantly, the demand environment is unlikely to worsen without a severe recession, hence any cyclical upside is mostly a free option. If investors gain confidence that high incremental margins are sustainable and CHRW is once again a structural share gainer, Abacus believes the stock can continue to re-rate higher.

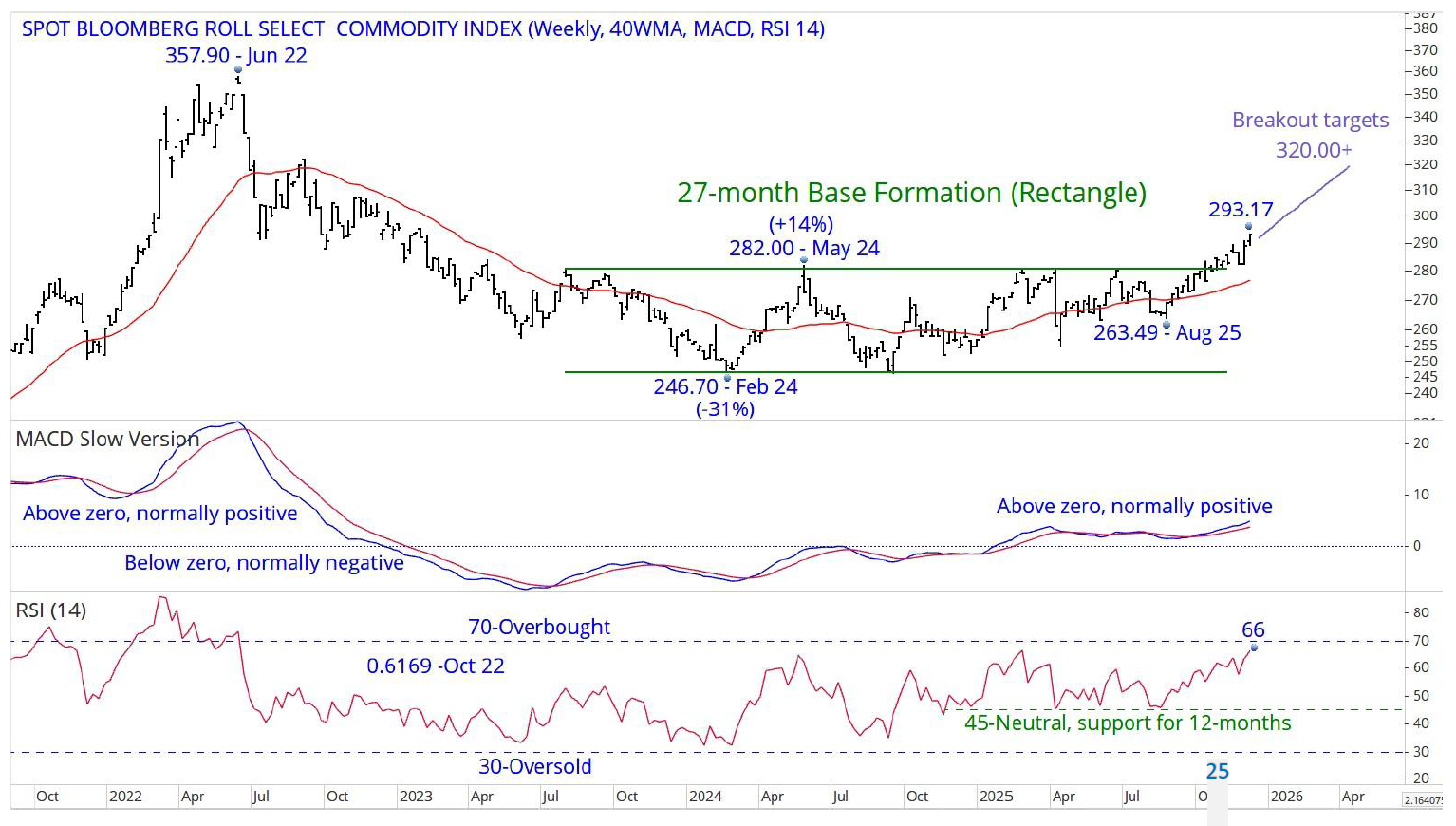

Don’t fall asleep at the wheel, this is a secular bull market

The Spot Bloomberg Roll Select Commodity Index (293.17) is the instrument that Chris Roberts’ newest data provider has, that is just about identical in shape to the Bloomberg Commodity Index that he used to feature. The breakout from the 27-month base formation targets a move to 320.00+, but Chris’s target is a new high above 2022’s 357.90. A secular bear market ended in April 2020 (see next page). The 1st leg of a secular bull market ended in 2022, and following a 30%+ decline and a distracting, time consuming sideways movement, the 2nd leg up is now underway. Indicators have room for further gains.

Aluminium in transition: The neglected materials play?

Fossil fuel demand may be falling in the future, but aluminium certainly won’t, driven by demand for EV and solar adoption, the great grid buildout and more aggressive lightweighting. There are no physical constraints to aluminium supply, with bauxite a plentiful resource that can be found near the earth’s surface, yet supply is expected to tighten relative to demand beyond the next three years. China is the main reason, having imposed a national ceiling of 45m tons per year on primary aluminium production. The next big reason lies in electricity constraints; given the amount of electricity required to produce aluminium, the economics of the metal are essentially the economics of power. Competitive advantages are available for producers with sizeable recycling operations, which the team expects to outperform over the next few years. Expect the likes of

Constellium,

UACJ Corp

and

Norsk Hydro ASA

to be the biggest relative winners.

South Africa: One notch down, guard up

The SARB delivered the unanimous 25bp cut that Peter Montalto expected, but this was no dovish pivot: the CPI path was only nudged slightly lower and the language stayed cautious. The MPC is now comfortable moving into “less restrictive territory”. It means that the country now sits a little above the new neutral range around 6.50%. Looking ahead, Peter remains more conservative than the QPM on both inflation and the policy path. He still sees a stickier non-core wedge and slower expectations pass-through than the model assumes, given the fixed public-sector wage agreement, Nersa’s tariff pipeline and unusual food CPI seasonality, even though the de jure shift to a 3% target pulls the expectations profile down. That keeps Peter above the SARB’s inflation and repo projections: his baseline is no further change for roughly six months, and a clearer next leg down only in H2 2026 to 6.00% end 2026.

2026 risks being overstimulated

Developed economies enter 2026 with inflation above target, labour markets tight, wage growth solid and governments running gargantuan budget deficits. Yet Gerard Minack points out how markets expect most central banks to ease or keep policy rates steady, Japan (and Canada & Australia) excepted. There are many hard-to-calibrate risks – such as the war in Europe, US trade policy, Fed independence – but the base-case macro-outlook is for at-or-above trend growth that threatens higher inflation and undermines the case for easier monetary policy. Gerard will discuss the implications of this for markets next week. Spoiler alert: two of the biggest issues for investors – the AI equity trade and risks around developed economy sovereign bonds – don’t hinge on the near-term cycle forecast.

The next financial crisis

That we live in a hyper-financialised world is not in dispute, but James Aitken cannot see the net benefits to society from changes like Kalshi, which monetise differences in opinion. He argues that over the long run, monetising any difference in opinion will create negative utility due to the externalities of normalising the idea of betting on everything. And one would think that these betting markets are enormously susceptible to manipulation by state actors; yet such is the path we are on. So what? James says he isn’t tilting against the windmill of the ongoing, hyper-financialisation of everything. Instead, he suggests that the path to the next financial crisis won’t run through (e.g.) private credit, geopolitics or whatever, but instead it will run directly through market structure, period. What happens when, for any period of time from minutes to hours to days, all the machines that intermediate 1x, 2x, or 3x levered ETFs, prediction markets, 0DTE, bonds, stocks etc. decide ‘computer says no’?

Industrials

Results will not live up to the enormous expectations surrounding this story, as the company shows almost no customer traction beyond Walmart. While SYM is rolling out systems across 42 WMT distribution centres through 2029, new wins have been minimal, leaving a massive revenue gap ahead. In contrast, competitors Knapp and Witron have announced dozens of new customers since 2022 including new business with WMT. Half of the company’s touted $22bn backlog sits in a stalled SoftBank JV (GreenBox), with little evidence of progress. With heavy insider selling, a recent revenue restatement, TAM overstated and the stock trading at ~10x 2027 sales, the bear case sees estimates beginning to be revised down next year and SYM’s valuation potentially halving.

Technology

2Xideas argues OS is tapping into a large, visible market opportunity as enterprises replace outdated software applications and tools. The company continues to gain market share, strengthening its position relative to peers and is on a "winner‑take‑most" path. Furthermore, OS is well‑positioned to integrate emerging AI technologies, benefitting from its role as a trusted governance and compliance layer, which largely insulates it from disruption. 2Xideas forecasts 19% revenue CAGR, driven by new customer wins, strong cross-/up-sell opportunities and international expansion. Over the next 5 years, they expect a total shareholder return of 20.8% p.a., based on an exit NTM EV/Sales multiple of 8.0x.

Materials

A 2026 copper turnaround story - IVN is now producing from all 3 of its core and globally significant mining assets. However, this has not been reflected in the share price following the seismicity event at Kakula in May 25. The market is focused on short term risks, but Kakula’s recovery is being managed and 3Q25 volumes (annualised at 285kt/yr) likely marks the bottom. With the 3 operating assets contributing in 2026 and a new smelter set to lower costs, GMR sees next year as the inflection point. IVN also offers major exploration upside - its 100%-owned Makoko district alone has 9.2Mt of copper identified, with additional drilling across Angola, Zambia and Kazakhstan providing further optionality not priced in. Trading at 1.4x P/NPV10, IVN’s growth, scalability and asset quality make the risk/reward compelling.

Fears of lower oil prices may be too pessimistic

While market participants await to see what, if any, peace accord emerges from the current Russia-Ukraine talks, William Brown notes that Wall Street analysts appear to be leapfrogging over one another in terms of how bad the global oil “surplus’ will be next year and beyond, and in turn how low oil prices could go. Once again, as William has discussed over the years, analysts always qualify their either extreme bullish or bearish price forecasts with “could” and not “will”. Be that as it may, he notes that one bank he has now heard from is JP Morgan, who suggests that Brent, again “could”, plummet into the $30s due to an “overwhelming” market oversupply. Meanwhile Goldman Sachs are reiterating their bearish view, estimating an average 2.0 MMB/D surplus in 2026, leading to a Brent average of $53.00 per barrel. In contrast, William’s view is the opposite, given what he estimates to be the substantial net short position investors and funds have already amassed.

Gold and silver to remain volatile with underlying strength

Jeffrey Christian of CPM Group discusses the increasingly unstable economic and political environment and what it means for gold, silver, and broader precious metals markets. He compares today’s conditions with the late 1970s, noting both the similarities and critical differences to that period, and what those differences may mean for gold and silver prices. Jeff looks at the volatility across gold, silver, platinum, and palladium, explaining the factors influencing investor anxieties. He also discusses economic shifts, including weakening U.S. influence on the global stage. The video concludes with a look at inflation data, consumer behavior, policy risks, and why CPM Group expects a recession within the next 12–24 months.

Click here here to watch

UK Budget is negative for economic growth

Mark Bathgate's initial thoughts on the overall shape of the UK Budget is welfare spending and taxes up a lot, borrowing up in the first two years of the budget period, with most tax hikes coming years 4 and 5. He points out that the Budget looks to be negative for growth – primarily via the further decline in household real after tax income, and likely impacts on confidence from the messy process of recent weeks and prospects of many years of rising taxes. Moreover, three key expenditure areas have not been addressed which questions the sustainability of the current budget:

* defence spending (no funding for NATO commitments entered into at June summit);

* Ukraine 2026 & 2027 budget which UK is publicly committing to contribute significantly to;

* local government financing crisis.

Overall, Mark says this looks to maintain the trend we’ve seen over the last 15 months: higher borrowing; lower economic growth; steeper gilt yield curve/higher long gilt yields; and more speculation about next round of tax hikes. However, Mark also says that one positive is that there are less inflationary risks relative to the previous budget.

Financials

Abacus revisits BN after a 70%+ rise since their Jan 24 write-up, arguing the fundamentals remain as compelling as ever. They still see a 22% IRR over the next 2 years - even assuming a persistent ~30% SOTP discount. BN’s thesis is simple despite its perceived complexity: a longstanding focus on infrastructure positions it as a major beneficiary of US on-shoring and increased infrastructure spending, while structural growth tailwinds support its insurance and wealth platforms (Brookfield Wealth Solutions is highly attractive at ~1x book, given 15% ROE). Although BN is improving its communication, Abacus argues few investors appreciate the value, leaving ~35% upside to their TP of $63.

Materials

Ben Jones reiterates his bullish view with the stock up ~200% since initiation in July 23. AAZ is set to enjoy a dramatic increase in net income as well as FCF which is expected to swing from -$2m (2024) to c.$126m (2026) - a 45% FCF yield on today’s m/cap. He expects AAZ to develop 3 new mines (without raising equity) over the next 5 years which will boost copper production from 2.1kt in 2023 to around 40kt per year from 2028. Ben increases his base case price target from £3.70 to £5.59 (150% upside), assuming long-term copper prices at $4.50/lb, but with optionality to £8.00+ if long-run copper averages $5.50/lb, as forecast by Citi and BAML. Since publication of Ben’s report, AAZ has disclosed it is in preliminary takeover talks - unsurprising given his view that the market continues to undervalue the company’s asset base and growth profile.

Why investors keep buying silver

In his latest video, Jeffrey Christian of CPM Group discusses recent developments in gold, silver, platinum, and palladium prices, and their consolidation following October’s sharp rise. He also looks at the factors that could determine the next breakout for the metals, and whether the next price move might be higher or lower. Jeff takes an in-depth look at the physical silver market and addresses several misconceptions about physical supply, fabrication demand, investment demand, and inventories. He looks at mine production, secondary recovery, fabrication demand, inventory levels, and investor activity, explaining how the market remains well supplied even as investment demand has risen sharply in recent months. Jeff also discusses ETF flows, coin sales, premiums for 1,000-ounce bars, and why talk of a “silver shortage” is misleading.

Click here to watch.

Gold and silver update

Andrew Egan Baptiste notes that both gold and silver have rallied up to his listed attraction zones. With the attainment of the new rebound highs, he has closed his tactical long positions into strength as recently discussed. Moving forward, given the overall shallow depth of the correction off the 3901.30 selloff low, Andrew expects a corrective pullback in a wave ‘x’ position, that can then lead higher towards the 50% retracement at 4142.00, and potentially up the highs of the prior triangle wave ‘b’ consolidation at 4156.00, 4171.50, and 4175.00. Above that is 61.8% Fibo. retracement at 4201, although he doesn’t believe we can get there without a pullback. If we see evidence of a corrective pullback, Andrew will consider another tactical long. He is now looking for the next opportunity, which he says will likely be on the short side in silver.

Russia: Close to recession

Christopher Weafer notes that the Russian economy is close to recession. Economic growth has accelerated on the back of big fiscal stimulus and an upswing in the domestic demand – but GDP growth could fall into a negative territory in 4Q25. Industrial output is expected to be near zero, while other segments, such as retail sales and agriculture, could help the economy escape a contraction. However, the growth dynamic will become far less certain in early 2026 with the introduction of higher VAT and inflationary pressures. In 9M25, GDP increased by just 1% YoY (0.9% YoY in September), which puts Christopher’s 2025 growth forecast of 1.2% more on the optimistic side. Over the next 2-3 quarters, the economy will balance at close to zero. Christopher expects that it will be no earlier than mid-2026 when credit conditions could start to improve, thus offering support to a gradual rise in consumer demand and corporate investments.

The rise of China’s intelligent economy

Konstantin Fominykh comments on the breathtaking structural rise of China’s intelligent economy, powered by technology and automation, which is advanced at a scale and speed that far surpasses global peers. It is overtaking the US in key next-gen industries, and over the next few years its main strengths will be EVs, green tech, 5G, high-speed rail, and defence. Currently, we might be witnessing a cyclical recovery, with manufacturing production up 7.3% YoY, service activity expanding again, exports up 3.3% YoY, and consumer confidence finally stabilising. Konstantin’s predictive tools predict further inflows into Chinese stocks, and he recommends a buy on Chinese sector equities, financials, tech, industrials and healthcare.

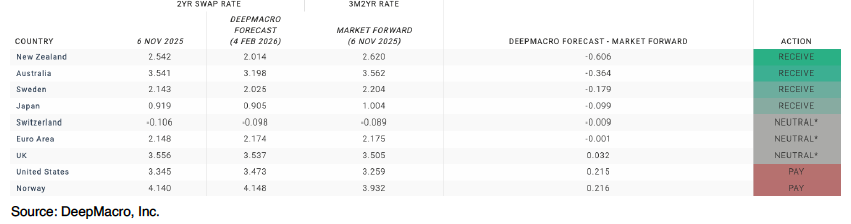

Short-Term Rates-1 Model

DeepMacro’s STR-1 is a short-term rates model, providing forecasts of 2yr swap rates for the G10 countries over the next three months. The team choose 2yr swap rates because they are an estimate of the market's expectation for monetary policy over the medium term, which they recognise as a function of economic growth and inflation. STR-1 generates receive/pay recommendations based on the difference between model forecasts, and market forward interest rates. The inputs to the model are the DeepMacro growth and inflation factors, including "Big Data", and DeepMacro's automated, machine-driven analysis of central banks. Currently, the model expects rates to rise in the US, but the market forwards expect rates to decline. In Europe the model forecasts rates to rise but by less than market forwards, and in UK it expects rates to decline but by less than market forwards, but both gaps are not large enough to recommend a trade. Please get in touch to find out more.

Communications

New Street turns more positive on Bharti, arguing that focus is likely to shift back to the company itself after Airtel Africa and Singtel materially outperformed over the past year. Bharti has historically rallied ahead of tariff hikes and with price increases expected in H1 next year, momentum should build. Growth is accelerating across Home and Enterprise, AAF continues to perform strongly and capital intensity is now falling, supporting margin expansion and rising ROIC. With fixed wireless access (FWA) adoption gaining traction and scope for meaningful EBITDA beats through FY26-27, New Street raises their TP to INR 2,750 and sees a strong case for re-rating as earnings expectations climb.

Varonis: Impact of growing competition

Technology

The company’s latest stumble stems from a weakening Federal pipeline and sluggish on-prem renewals, but channel feedback points to deeper challenges from nimble DSPM rivals like Cyera and Concentric.ai to mounting pushback on costly cloud migrations that offer less functionality. With competitive share shifts and customer dissatisfaction surfacing in SPR’s 10/12 panel, it’s clear the DSPM market is heating up fast, fuelled by AI-driven data priorities and VRNS may be losing its footing. SPR’s full note unpacks which vendors are gaining ground, why end users are rethinking their data protection stack and where this market is headed next.

Ready for the contrarian gold trade?

Cam Hui has been bullish on gold, but point-and-figure charts of gold and gold miners now show that they are either very near or have outrun their measured price objectives. Tactically, the contrarian trade would be to sell gold and buy bonds. However, a cycle analysis leads Cam to conclude that the market is undergoing a shift to a hard asset price leadership cycle. Cam’s base case calls for a multi-month correction and consolidation in the manner of the 2004–2006 experience, followed by a second rally to an ultimate top at much higher gold prices. It is within this context that a long-term point and figure objective of 9,800 is achievable in the next 3–5 years.

US equities: The case for value

Tian Yang is changing his long-held bias against value stocks and recommending a shift to overweight value vs growth. He points out that he is finally seeing alignment across A) market behaviour, B) the macro-outlook, and C) bottom-up fundamentals. On his indicators, today's set up is as good as it has been since the GFC for value to outperform. US earnings estimate revisions have broadened since Liberation Day, which has historically been indicative of value vs growth outperformance over the next 12 months (first chart below). At the same time, he notes a sharp fall in the correlation of the Russell 1000 market cap weighted index vs the equal weighted index. As the second chart shows, this correlation collapse has often marked a low in the value-to-growth ratio historically. Tian is also seeing evidence of a rotation into value stocks over the past couple of months.

Healthcare

Leveraging purchase order data from 450 US facilities, MedMine is closely tracking the rollout of Pulse Field Ablation (PFA), the key driver of BSX’s Electrophysiology growth. The US ablation catheter market for AFib is estimated to be growing about 12% Y/Y. BSX has been growing faster in part due to mix shifting from lower-priced Cryo and RF products to its premium FARAPULSE PFA system. However, BSX is facing increasing competition with its PFA market share now at 80%, 10 percentage points lower than its peak. This raises a key question: will BSX’s next growth phase come from converting the larger RF market or expanding the total patient base estimated at 60m globally? MedMine’s near real-time data helps investors track these shifts in market share, pricing and technology adoption as they unfold.

Financials

Abacus sees FIGR as a highly disruptive leader in real-world asset tokenisation - a theme they expect to define the next decade. The company has found a real-world use for blockchain, proving it can reduce the cost and time in HELOC origination by 90% (current 3% market share), with an average production cost per loan of just $730 vs. an industry average of $11,000. Beyond its low-cost origination engine, FIGR operates a marketplace for pooled credit, creating liquidity and transparency in traditionally illiquid markets. Abacus expects this model to scale into other asset classes, underpinned by ~30% operating margins and 80%+ incremental margins, with potential upside of 150% to $115.

Consumer Discretionary

PLNT is well positioned in the growing high‑value‑low‑price gym segment with scale and ample runway for growth. New CEO Colleen Keating brings relevant hospitality franchise experience to drive the next phase of growth in the US and internationally. Gen Z is the fastest‑growing membership cohort for the company, supported by initiatives like the “High School Summer Pass”. PLNT continues to refine club formats and contractual terms to improve efficiency and unit economics. 2Xideas expects 2024-31E system‑wide sales CAGR of 11.7%, driven by 6.6% annual net unit growth and 5.0% same‑club sales growth. They forecast an 11.1% EBITDA CAGR and a 44.6% margin in 2031E. European expansion remains an upside not reflected in their forecasts. They see 17.2% annualised total returns based on an exit NTM P/E of 28.0x (17.7x EV/EBITDA).

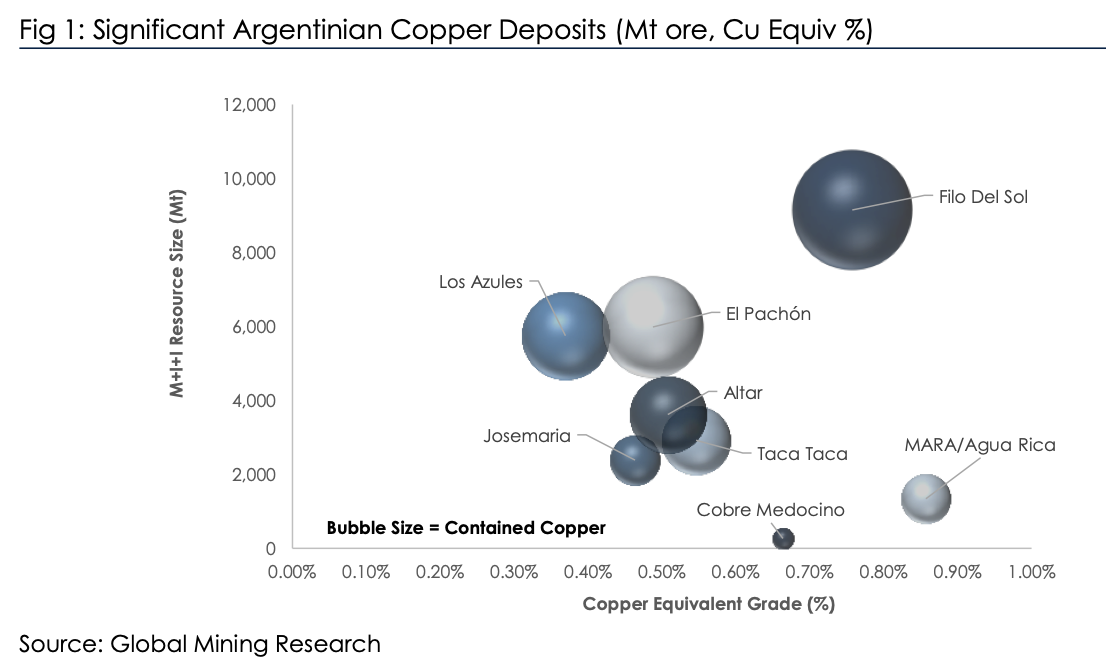

Is Argentina the next big thing?

Argentina has significant copper reserves yet produces no material copper (see chart). The new investment climate (RIGI) in Argentina, spearheaded by libertarian President Milei, is hoping to reverse this. Other volatile countries including DRC have achieved significant growth, so it’s possible. In his latest report, David Radclyffe examines the potential of Argentina copper. He sees potential for the nation to become a 1.0–1.5 Mt per year copper producer (top 10 globally), but comments on the aspirational timelines, with first copper unlikely on this side of 2029. Issues also cannot be discounted, with ESG concerns bubbling alongside a lack of infrastructure and skilled workers. David estimates the total capex at USD $40–50 billion.

Lundin Mining has the most leveraged exposure to Argentina in partnership with BHP and is the preferred exposure. There are a few exploration plays, of which NGEx Minerals (non-rated) and its Lunahuasi discovery is the largest.

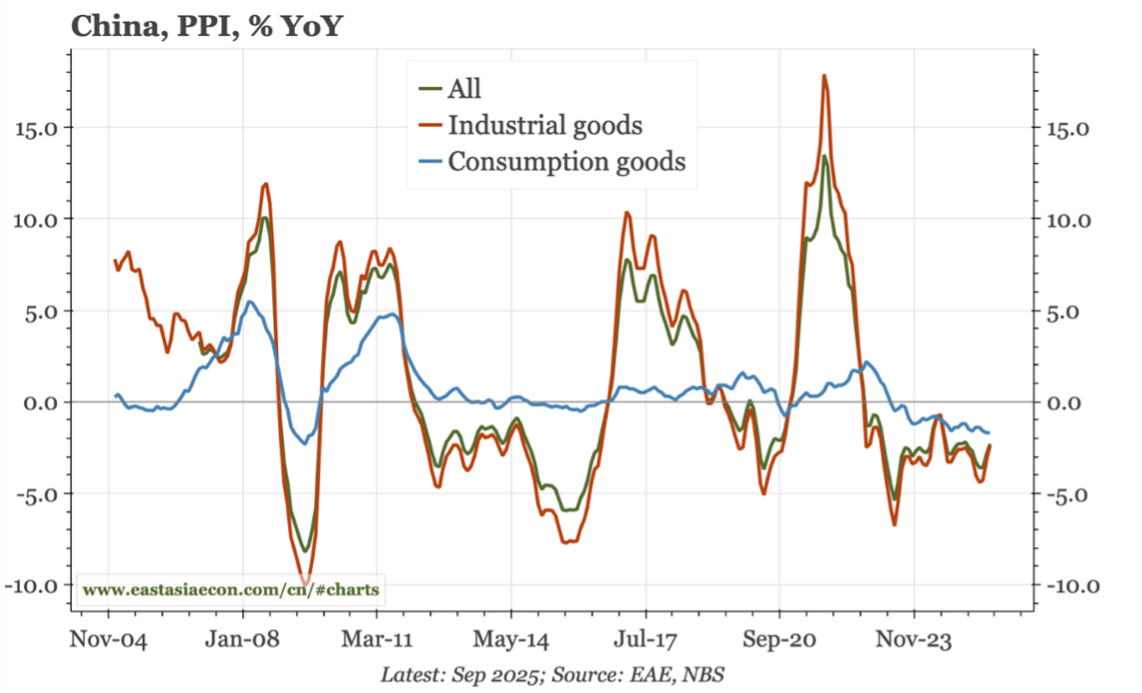

China: A fragile improvement in PPI

For the first time in more than a year, in level terms, the producer price index (PPI) has stopped falling; however, in year-on-year terms it was down 2.3%y-o-y (versus -2.9% y-o-y in August). That is an improvement, but one that looks fragile. Prices in auto manufacturing – one of the sectors targeted by the anti-involution drive – are falling more quickly than ever, and the "consumption" sector of the PPI in general shows no turnaround. Building material prices continue to be dragged down by the problems in the property market. The stabilisation in PPI is being driven by prices for "industrial" products, namely mining and energy. The short-term leads don't suggest much change in PPI in the next couple of months. But there is some upside risk coming from the YoY rise in global commodity prices (in CNY terms). Paul Cavey remarks that this would be more powerful for China if the construction cycle really finds a floor, allowing building materials prices to do the same.