Financials

86Research recommends investors aggressively buy Futu following its 14% post-1Q26 preview selloff, arguing the decline significantly overstates temporary market-driven weakness with a US$231 price target, implying 59% upside from current levels. Analysts believe downward earnings revisions and geopolitical tensions triggered excessive selling despite strong rebounds in global equity markets since early April. According to channel checks, Futu’s user acquisition and net asset inflows have already recovered to pre-March levels, positioning the company to achieve its 2026 target of 800,000 net new funded accounts. 86Research also highlights FUTU’s dominant Hong Kong brokerage position, Southeast Asia expansion plans, strong management team, and industry-leading margins. Trading at only 11x 2026 earnings, the stock remains deeply discounted relative to historical averages and peers.

Industrials

Alstom shares fell 27% on 17 April and 36% since being added to Alumbra’s high conviction Active List in January, after the company issued a profit warning and disappointing FY27 free cash flow and EBIT margin guidance. In its 16 January initiation report, Alumbra had flagged that a significant year-on-year increase in unbilled receivables across H1 2026 and H2 2025 could indicate project cost overruns, weighing on future margins and cash generation. This was supported by its review of local subsidiary filings. Alumbra had also questioned consensus expectations for €700m of FY27 FCF, given recent cash flow benefited from €639m of unsustainable items.

Industrials

Epiroc remains a strong BUY despite lagging sector peer Sandvik’s recent surge. Since its 2018 spin-off from Atlas Copco, Epiroc has delivered consistently high returns, averaging 24% ROCE, well above its cost of capital. Its strength lies in a service-led business model: recurring services generate most revenue, while mining contributes 80% of sales. Global operations and extensive service networks create barriers to entry against rivals such as XCMG and Sany. Demand is supported by strong copper and gold markets, electrification trends, and growth in underground mining. With strong Q1 2026 orders, low debt, and expanding high-margin aftermarket services, AlphaValue sees around 30% upside and continued long-term growth potential.

Industrials

Another very successful Short idea from the Alumbra team as Primoris declined 50% on earnings last week after reporting disappointing Q1’26 results and significantly reducing FY’26 guidance due to cost overruns on renewables projects and lower-than-expected renewables revenue. Alumbra still have high conviction that the stock will decline further due to continued cost overruns on renewables projects and difficult revenue comps.

Consumer Discretionary

Stellantis’ latest results reinforce concerns that its finance arm is masking weakness in the core car business. While the market is focused on the potential for a recovery in earnings, the report argues that rapid growth in leased vehicles and heavy use of off-balance-sheet JVs is helping support sales and industrial free cash flow. With credit ratings now close to junk, higher funding costs could undermine this support and create further pressure.

Materials

Guangzhou Tinci Materials Technology plans to raise over US$1bn through a Hong Kong H-share listing in 2026. The company leads globally in lithium-ion battery electrolytes, LiPF6 and LiFSI, benefiting from EV and AI energy storage demand. Profitability appears to have bottomed in FY24, with FY25 recovery supported by volume growth, vertical integration and overseas expansion into Morocco, the US and Southeast Asia.

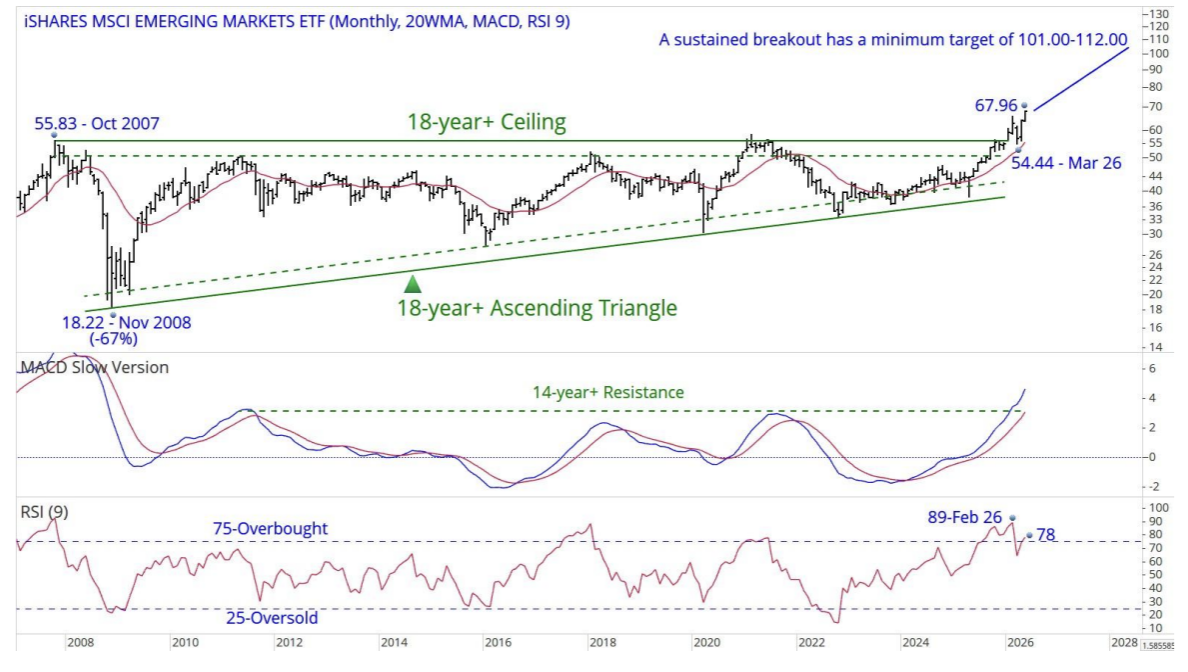

MSCI EM: The return of the Dodo

The iShares MSCI EM ETF (EEM US, last USD67.94) has successfully broken out from an eighteen-year-plus ascending triangle and is currently attempting to move beyond an eighteen-year-plus ceiling. While Chris Roberts points out that a sustained breakout above this resistance level suggests a minimum price target between USD101.00 and USD112.00, and the MACD indicates a significant improvement in momentum by clearing a fourteen-year resistance level, the nine-month RSI of 78 is approaching the very overbought threshold of 80. Consequently, it is prudent not to chase the current price; instead, the strategy is to wait for a setback toward the key support level at USD54.44 before considering a buy. Chris thinks he has found a dodo.

US S&P: Feeling good

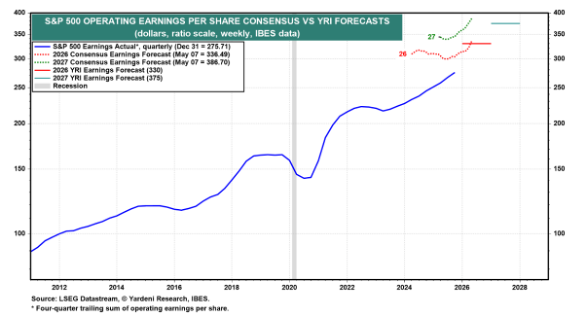

Ed Yardeni is raising his year-end S&P 500 target from 7700 to 8250. He has never seen consensus earnings expectations rise so quickly for the current and coming years as they have in recent months. The result has been an earnings-led meltup in the stock market. Ed is raising his EPS estimates to $330 this year and $375 next year, while sticking with his forward P/E range of 18.0-22.0, resulting in a year-end range for the S&P 500 of 6750-8250. His key assumption is that the economy will remain resilient, and so will earnings. Ed is also raising his probability of a continuation of the Roaring 2020s to 80% from 60% simply by merging it with his meltup scenario (previously at 20%), since he believes that any meltdown will be a buying opportunity and won't trigger a recession or bear market similar to the 1999-2000 Tech Bubble and Tech Wreck.

Consumer Discretionary

Lululemon shares are trading at both 52-week and five-year lows after a difficult period marked by product challenges and pressure on the brand’s core offering. The source notes that the company had strayed too far from its brand DNA, with limited colour in parts of the range and the departure of its senior merchant. However, early signs of improvement are emerging, including a tighter product offering, more colour and the appointment of a former Nike executive as CEO. While a full turnaround is likely to take time, The Retail Tracker sees potential for the stock to reach $175 over the next 12 months.

Technology

SK Hynix benefits from better demand visibility and reduced investment risk whilst demand for mid- to long-term agreements is increasing as customers seek volume security and price stability. Arete expects these agreements to materially reduce industry volatility and improve earnings stability, supporting its structural AI-driven thesis. They see two key catalysts for sector re-rating: substantial free cash flow generation driving higher capital returns, with details expected by year-end, and the market underestimating earnings durability over the next several years. With SK Hynix trading on 5.5x FY27 earnings and 2.5x book value, there is significant upside ahead.

Technology

Capgemini’s investment in the OpenAI Deployment Company reflects growing demand for enterprise AI deployment services, as organisations look to scale adoption through consulting, engineering and transformation support. Rather than posing a threat to firms such as Capgemini, Accenture and Infosys, the initiative highlights OpenAI’s reliance on consulting partners for sector expertise and large-scale implementation. This should create further opportunities for AI-enabled transformation services as enterprises move from experimentation to deployment.

Industrials

Strabag is a leading infrastructure player in Germany and Austria, where urgent reconstruction needs across bridges, railways and waterways support long-term demand. Renewables is another key growth driver, now representing 18% of sales after doubling over the past two years. European data centre activity is also being supported by the EU Chips Act and Horizon Europe, while the EU Green Deal should drive longer-term decarbonisation and building energy upgrades. With momentum across infrastructure, renewables, water, energy, mining and mobility in markets including Germany, Poland, Czech Republic, the UK, Canada and Australia, the source sees Strabag’s 5.5% 2026 EBIT margin guidance as beatable.

Real Estate

Ben Jones remains bullish on M/I Homrs as volumes remain solid despite higher mortgage rates, signalling ongoing demand. Despite the US housing market showing some weaknes, increased incentives, higher LTVs, lower interest rates ahead should continue to provide support. Current operating margins of 9.3% are below recent highs but only slightly under historical averages, with long-run margins around 11%. The company’s strong balance sheet position allows them to withstand downturns and capitalise on land opportunities. Ben favours their disciplined capital allocation, balancing cash reserves and share buybacks. A persistent US housing shortage should continue supporting home prices over the long term.

Technology

When presenting FY25 results, TKH Group warned of a weak start to the year, making its 9.6% turnover growth in Q1 notable. The order book declined nearly 10% year-on-year but remained broadly stable versus year-end 2025, mainly due to weaker Tire Building orders within Automated Machinery. This was partly offset by 7.4% organic growth in Vision Technologies, supported by a stronger order book. Electrification and Digitalisation also performed well, benefiting from strong offshore and onshore cable demand. TKH continues progressing with its automation-focused strategy. The Idea maintain a positive long-term investment view based on growth, margins and cash flow generation.

Consumer Discretionary

Zach Shannon initiates a Short recommendation on Shoe Carnival which experienced a rapid deterioration in same store sales in Q4 FY25, with declines across all three of its store banners. This caused the company to walk away from its plan to rebanner more than 100 Shoe Carnival locations as Shoe Station (its higher-priced storefront) as converted stores significantly underperformed expectations. As a result, the company's CEO left abruptly (resigned or terminated) in February, with the company pulling its prior CEO out of retirement to serve on an interim basis. With inventory at a 10+ year high (inventory was up 14% last year on a 6% sales decline), the company faces pressure to rightsize the business and turn its stores around. However, guidance for FY26 is backend weighted, while FY27 consensus estimates appear aggressive. As a result, Corto believes SCVL shares have material downside risk (-20% to -50%).

Technology

Infineon Technologies AG was presented by a PM at a Revelare event as a long idea with ~50% upside to a €75 price target. The stock trades at ~16x 2027 EPS and ~12x 2028 EPS, below its 10-year median multiple of ~19x. The thesis rests on two tailwinds: analog recovery and AI datacenter demand. Infineon’s industrial and automotive businesses are rebounding, while €800–900M of annual underutilization charges should normalize, driving ~600bps gross margin expansion. Simultaneously, denser AI server racks require advanced power semiconductors, where Infineon leads across silicon, GaN, and silicon carbide. AI revenue is expected to grow from €700M last year to €1.5B this year, with additional upside potential. Gross margins could rise from ~17% to ~25% over 2–3 years, supported by higher-margin AI products and cyclical recovery.

Consumer Discretionary

Despite near-term margin pressure, DFH trades at only 7.5x 2026 earnings and 1.1x book value, well below peer averages. Analysts maintain a fair value estimate of $25 per share, implying significant upside potential. They have the second highest ROE in the sector out of the 17 builders Housing Research Center follows. The stock is trading at $13.02 and peaked at $43 two years ago. They have grown nearly 5x in the past 6 years more than any other builder and recently made a bid to acquire Beazer homes (BZH) at 0.5x book value. That would allow them to grow another 50% in 2027. They should make EPS of $2.00 in 2026 and $3.00 in 2027.

Consumer Staples

Sprouts Farmers Market reported encouraging 1Q26 results, reinforcing QuoVadis Research’s bullish stance. Revenue, same-store sales, margins, and EPS all modestly exceeded company guidance and Street expectations, suggesting management has regained control after the sharp slowdown experienced in 2H25. The company also deployed all 1Q26 free cash flow toward share repurchases, buying back 1.9M shares at an average price of $73.68, with QuoVadis modeling $500M in buybacks for full-year 2026. While guidance was largely maintained, the EPS outlook was slightly raised, signaling improved visibility. At just 13x P/E and 8x EV/EBITDA on consensus 2026 estimates, the stock undervalues Sprouts’ strong ROIC-driven growth and favorable risk-reward profile.

Healthcare

MDC Financial Research’s Event-Driven Legal℠ Investment Research service is closely monitoring Sotera Health Company's (SHC) ongoing EtO litigation in California, Georgia, and New Mexico. A key Summary Judgment Hearing related to the first group of eight Bellwether Cases in California is currently scheduled to be held May 27 - 28, 2026. A favorable Ruling could relieve Sotera from this initial set of Cases and strengthen its position against the 114 total plaintiffs (as of April 1, 2026) alleging harm from Sotera's L.A. area EtO facilities. MDC will attend this Hearing and provide timely insights.

Technology

Rosenblatt raises its price target on PENG to $54 from $32, a nearly 70% increase, following investor meetings with CEO Kash Shaikh and CFO Nate Olmstead that increased confidence in the company’s long-term direction. The firm highlights Penguin’s plan to leverage its 40+ years of memory-subsystems expertise and combine this with AI system/factory software and services to deliver a broader full-platform solution. Rosenblatt sees the strategy as increasingly cohesive, supported by the AI market’s rising need for optimised memory subsystems and the acceleration of corporate adoption of internal AI systems driven by agentic AI. The company also intends to use partner relationships to broaden its customer base.

Technology

JNK Research showed ROHM and VSH entered earnings with supply tightness already visible across power and passives. Its April-May Analog Tracker flagged pricing increases across close to 95% of products, while book-to-bill improved from 1.06 to 1.10. ROHM print showed that with FY26 still under-allocated and FY27 Q1 likely to snap back double-digit QoQ on SiC mix and capacity additions. Commentary on discrete SiC mix and FY27 capacity reads across to ON Semi and WOLF. VSH print provided the cleanest US-listed read on the VICR shortage, with Q4 backlog close to 5.1 months and book-to-bill near 1.2.

Consumer Staples

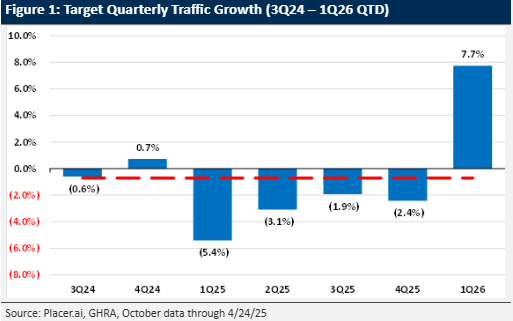

GHRA’s Proprietary Quarterly Store Manager Survey reinforces improving operational momentum, aligning with their traffic data and field checks that point to tangible progress in restoring merchandising authority through a refreshed assortment. This supports GHRA's optimistic outlook for TGT first outlined in their Jan 26 upgrade. Survey results show a notable sequential improvement: 29% of managers report sales tracking above plan (vs. 11% in 4Q25), while 31% cite stronger traffic (vs. 9%). Seasonal performance was particularly robust, with 46% indicating better-than-expected trends (vs. 9%), alongside a meaningful pickup in discretionary demand, suggesting recent brand partnerships are resonating. However, promotional intensity has increased, with 60% flagging higher markdown activity. While inflation concerns among customers edged up, sentiment appears to be stabilising.

Europe: Uncontrollable hiccups

Niall Ferguson expects euro area headline inflation, measured by the harmonised index of consumer prices, to peak near 3.5% in late 2026 or early 2027 and to return to 2% in 2H2027. This is a higher peak than consensus and a longer return to target than in the European Central Bank’s adverse scenario. The return to 2% inflation was never sustainable. Imported disinflation from Chinese manufactured goods had been masking broad but shallow inflation in domestic services, and the current shock now arrives with no disinflationary buffer. Accordingly, Niall expects the ECB to hike rates by 50 bps by year-end. His views on US and EU rates and inflation translate to a minimally stronger euro than the market is pricing; Niall sees the EURUSD spot price at 1.178 and the one-year forward at 1.193. Europe’s second inflation shock in four years will prove less acute than the first but harder to shake.

Gold and silver entering a new phase

In his latest presentation, Jeffrey Christian of CPM Group discusses the recent movements in gold, silver, platinum, and palladium prices, focusing on the sharp decline in gold and silver and the consolidation pattern developing across precious metals markets. He explains why, despite the recent drop, prices remain within the range that CPM Group has been outlining, and why the current environment continues to point toward a period of sideways, volatile trading rather than a sustained breakout. Jeff discusses how seasonal trends, macroeconomic conditions, and investment demand are interacting to shape price behaviour over the coming months. He discusses the growing likelihood of a consolidation phase through the summer, while noting how economic and political developments could still cause short-term price fluctuations.

Click here to watch.

Copper: Lack of supply growth vs rising inventories

David Radclyffe's copper coverage totals ~63% of global mine production. Copper supply continues to wrestle with many legacy headaches from 2025, mixed with the Iran conflict and its implications for diesel and sulphuric acid supply. There is therefore downside supply risk. However, the current oil disruption has implications for global growth and copper demand. Worryingly, David points out that copper inventories are rising rapidly. His coverage universe implies 0.9% annual contraction in refined copper supply in 2026, following a strong 2025. Weak supply growth for 2026, even with moderate demand growth, is at odds with strongly rising terminal market inventories, now at 1,267kt, adding to price risk. Copper is a crowded long trade, with caution warranted. The sector is not particularly cheap at spot 1.6x P/NPV10 and 9x EV/EBITDA. Antofagasta PLC is cut to HOLD. Preferred stocks include Lundin Mining Corp, KGHM Polska Miedz SA, Ivanhoe Mines Ltd, Grupo Mexico SAB de CV, Hudbay Minerals Inc and Teck Resources Ltd.

US: Going overweight on tech

The Vermilion team remain bullish on the S&P 500 (SPX), Nasdaq 100 (QQQ), and Russell 2000 (IWM). Market dynamics continue to improve ever since the major bullish false breakdowns at 6480-6520 on the SPX, 24,000 on Nasdaq futures (NQ), and $245 on the IWM, with all of them now breaking out to all-time highs and holding above bullish gaps from April 17. Everything that the team sees suggests bulls remain firmly in control, so the team want to be buying any pullbacks for the foreseeable future to the 20-day MA or 21-day EMA. The team discussed adding exposure to growth, and primarily technology, as growth has taken over as leadership relative to value. RS on the cap-weighted XLK is now breaking above its 2025 highs and they are upgrading Technology to overweight. The team have remained overweight semiconductors (SMH, NVIDIA Corp, Taiwan Semiconductor Manufacturing Co Ltd, Ciena Corp, etc.) and memory (SanDisk Corp, Western Digital Corp, Seagate Technology Holdings PLC, Micron Technology Inc) ever since last June, and these remain their favourite areas within Tech.

US: Warsh ready for prime time at the Fed

Based in part on his previous interactions with Kevin Warsh, the prospective next Fed Chairman, John Ryding discusses what he is likely to do when he takes over on 15th May. John says that Kevin understands complex economic arguments but is not wedded to conventional academic wisdom. Kevin hates inflation and firmly believes that it is a monetary phenomenon and that the Fed must take responsibility for it. Although Kevin feared at one point that the Fed might raise its inflation target to 3%, he seemed adamantly opposed to the idea. Kevin brings a great depth of institutional market knowledge to the Fed, which it desperately needs, and is willing to think outside the box. In his prepared statement to the Senate Banking Committee, Kevin made it clear that he believes “monetary policy independence is essential. Monetary policymakers must act in the nation’s interest . . . their decisions the product of analytic rigour, meaningful deliberation, and unclouded decision-making.”

Financials

Anas Abuzaakouk (CEO since Aug 2017, joined 2012) bought 30,000 shares at €149, spending €4.5m. He has a great track record based on his 21 prior purchases. This is his single largest purchase and the highest price he has paid. He last bought in Oct 2025 at €108. Smart Insider has ranked the stock several times based on his prior activity, with the majority of those signals proving to be very timely. They are ranking the stock +1 (highest rating).

Materials

The closure of the Strait of Hormuz is driving dislocation in ammonia and sulphur markets. AECI is well positioned, sourcing ~85% of ammonia from Sasol’s Secunda plant and avoiding import exposure, while ~50% of global sulphur trade typically transits the Strait. Resulting shortages have triggered sharp price spikes, with AECI monetising existing inventory. Its sulphuric acid business (~R600m revenue, HSD margins) should see a near-term earnings boost (for approx. a quarter based on current conditions). Operations have also improved following stabilisation at Modderfontein. With peer Omnia sourcing ~50% of its ammonia requirements from imports, AECI is better positioned. Chronux expects EBITDA to reach ~R4.5bn by FY27 and increases their HEPS by 10.7% (FY26) and 3.8% (FY27). TP increased to R132 (from R125).

Technology

QCOM’s guidance came in weak, but visibility into the end of the handset correction is improving, with orders expected to normalise from Q4. More importantly, confirmation of a hyperscaler data centre win provides tangible evidence that diversification is gaining traction, alongside strong automotive momentum. If the market is finally prepared to look beyond Apple-related risk, then the shares have a lot further to go. QCOM remains one of the few semiconductor names with credible AI exposure that has yet to see a meaningful re-rating, while consensus expectations - currently implying no EPS growth in 2027 - is clearly too low.

Industrials

Report by

Insight Investment Research

Robert Crimes highlights GET as a unique long-duration infrastructure asset with a potential takeout emerging. Eiffage and Mundys will likely soon own ~59.8% of the company, having recently added to their positions. Insight’s buyout scenario IRR is 14.7% (at 25% share price premium of €24/share), +410bps above their deal Ke of 10.6%. While shuttle traffic remains pressured by excess ferry capacity, this has been offset by higher pricing, supporting continued revenue growth. The underlying appeal is the asset’s durable cash generation, with ~€710m recurring FCF (~6.9% yield) and long-term growth driven by pricing, traffic recovery and new high-speed rail routes.

Innolight: AI optics leader targets H-Share listing

Technology

Aequitas offers an early look at Innolight as it aims to raise ~$5bn in an H-share listing (up from ~$3bn in late 2025), potentially making it one of Hong Kong’s largest deals this year. The company is the global leader in optical transceivers and is benefiting from strong demand driven by AI-related data centre capex. Growth has been exceptional, with revenue up 122% in 2024, 61% in 2025 and a further 192% YoY in 1Q26, alongside margin expansion. With revenue heavily concentrated among hyperscalers and shares already trading at elevated multiples (~37x FY26 P/E), the key question for investors is how much of this growth is already priced in.

Technology

The group’s year-end update more than confirmed the optimism management showed at the interims. Revenues will be ahead of consensus, with double digit growth and record backlogs. Confidence is also evident in a 21% increase in headcount, albeit with some margin pressure from contractor usage. Consensus revenue forecasts have been upgraded, though EBIT has edged slightly lower. The balance sheet remains a clear strength with £160m of net cash and potential for ~£70m of Y2 FCF. While analysts appear to be recognising the revenue inflection, the implied to Y3 EBITM ratio here is now 40. That is very low for the growth on offer, with Willis Welby arguing the shares could easily rise 50% from current levels.

Industrials

Hamed Khorsand highlights Azul as a post-restructuring opportunity following its emergence from Chapter 11 bankruptcy, which materially reset its capital structure and reduced net leverage to ~2.3x EBITDA. The company eliminated ~$2.5bn of debt and lease obligations, cut interest costs by >50% and is now positioned to generate sustainable FCF. Despite this, the stock trades at ~3.9x 2026 EV/EBITDA, a significant discount to regional peers. The key catalyst is a planned NYSE listing, which should broaden investor awareness and drive a rerating. With a differentiated domestic network and improving profitability, Hamed sees ~70% upside to his (12-month) TP of R$50.

Industrials

Misumi appears to be at the early stages of a meaningful re-rating, as it begins to demonstrate the success of its transition from a domestic parts catalogue company to a global digital manufacturing platform provider. Over recent years, this previously highly regarded “growth” name has derated from trading at 25-40x to 15-20x, but has quietly transformed itself and now boasts a unique combination of software, hardware and logistics, which should support a re-acceleration in earnings. At the same time, there is increasing scope for enhanced shareholder returns as management optimises its cash-rich balance sheet.

Technology

The market is misdiagnosing structural share loss as a temporary slowdown. OWS’s industry checks suggest enterprise weakness is driven by competition from Microsoft Teams and Zoom, while a lack of innovation is reflected in Gartner’s Magic Quadrant rankings. Management’s expectations for high growth from AI and RingCX products appear optimistic, with feedback indicating these offerings are largely undifferentiated. At the same time, aggressive cost cuts in R&D and sales are cited as contributing to customer dissatisfaction and weaker retention. With RPOs (backlog) flat for nearly two years and FCF overstated (adjusting for buybacks reduces 2025 FCF to $196m from $530m and the FCF yield was 5.6% rather than the 15% bulls use to argue that RNG is a cheap stock), OWS sees continued pressure on growth and valuation.

Technology

JNK’s analysis suggests LSCC is tracking ahead of guidance, with Q1 supported by strong bookings extending into 1H27 and a book-to-bill above 1.2. However, this strength is partly driven by Greater China customers pulling forward demand ahead of a ~15% price increase implemented in March 2026, with regional shipments running ~25% above Q4 levels. Lead times remain elevated at over 26 weeks, constrained by substrate and packaging rather than wafer capacity. With servers accounting for ~60% of revenue and exposure to Intel and AMD platforms, the company also benefits indirectly from AI-related demand. JNK's analysis suggests pricing can support growth even if volumes soften.

Materials

GMR cuts FCX to Sell following further production downgrades at Grasberg, with the ongoing impact of the 2025 “Mud Rush” now expected to persist through 2027. They estimate cumulative production losses of 952kt of copper, 1.5Moz of gold and 6.6Moz silver over 2025-2029, equating to $19.2bn of lost revenue at spot prices (or $15.4bn on GMR’s base case price forecasts). GMR has cut 2026/27 EBITDA forecasts by 15-21% and reduced its valuation by 27%, arguing the recent share price reaction underestimates the severity and duration of the impact. With risks of further downgrades and rising capex, downside remains.

Industrials

Investors should own the stock ahead of what Craig Huber believes will be a robust US residential market recovery leading to an estimated 25% pick-up in mortgage inquires in 2027 and a further 20% jump in 2028. He also continues to argue that investor AI fears related to EFX and the information services stocks, in general, that he covers are completely irrational. With ~90% of revenue derived from proprietary data and significant regulatory barriers, AI is a net positive. Craig’s new 2026/27 adjusted EPS estimates are a Street-high of $8.79/$11.35 vs. consensus of $8.59/$10.28, with a 12-month TP of $224 (30% upside).

Drone related investment ideas

Red Cat (RCAT US) - expected to disappoint on its recent and highly speculative marine drone division; management has credibility issues from previously missing on guidance; and the company has yet to be included in the Department of War’s Drone Dominance Program.

Motorola Solutions (MSI US) - has been a dominant name in critical communications equipment for fire, police and government for decades. The long thesis now is based on the company's “transformational” acquisition of Silvus Technologies, a tactical drone networking business.

Fujikura (5803 JP) - tremendous scaling opportunity for selling co-packaged optical connectors for AI data centres, alongside expanding demand for fibre optics in drones - which is poised to become one of the fastest-growing segments within fibre optics - from military kamikaze and loitering munitions to commercial inspection drones, delivery systems and advanced surveying platforms.

Canadian Lifecos: Private credit risk under scrutiny

Financials

Roshan Paunikar’s analysis highlights rising scrutiny around private credit exposure within Canadian lifecos, with risks centred on below-investment-grade assets, valuation opacity and broader fixed-income sensitivity. While portfolios remain skewed towards higher-quality credit, companies are not insulated from a weaker environment, with potential impacts including higher credit losses, fair value marks and pressure on regulatory capital. Manulife Financial appears most exposed driven by a higher proportion of below-investment-grade private credit and a relatively riskier fixed-income portfolio, while Sun Life Financial appears most negatively exposed to wider credit spreads. Great-West Lifeco appears to have the most conservative investment portfolio among peers.

Financials

MRX is a beneficiary of geopolitical instability, particularly in commodity markets, where it is a leading player. The shares have pulled back from recent highs but are only ~12% above the 2025 peak, despite 1Q26 profits likely to rise c.50% Y/Y - implying meaningful multiple compression. Fighting Financials sees scope for this to reverse as volatility persists. Consensus Q1 PBT forecasts sit c.13-14% below management’s end of March guidance, while FY26 consensus implies flat Y/Y performance for the remaining quarters, which is clearly inconsistent with the current earnings trajectory. With the potential to return >60% of its m/cap via dividends and buybacks over the next 5 years, MRX stands out as one of the cheapest, high-quality financials in their investment universe and is one of the few compelling long ideas in a market, where opportunities are largely on the short side.

Consumer Discretionary

Paragon’s executive diligence memo was originally published when Heidi O’Neill was being discussed as a potential CEO successor at Nike and they viewed her as a poor fit for that role. At LULU, she is somewhat better matched to the brief, but their core reservations remain. She has tended to look stronger as an operator and internal brand steward than as a true strategic architect. That matters at LULU, where the challenge requires a sharper product vision, stronger innovation instincts and a willingness to make harder calls on strategy and talent. So, while the fit is better than it would have been at NKE, Paragon still views her as more of a stabiliser than an obvious answer to LULU’s deeper issues.

Healthcare

Following publication of the company's FY25 annual report, Iron Blue increases their CTEC score to 29/60 (newly top decile). They see upside risk to the group’s future D&A expense given FY25 PPE/RoU capex exceeded depreciation by a 10-year high 33% of PBT adj and balance sheet intangible assets under construction (historically mainly software) almost trebled Y/Y. Risks in CTEC’s debtor book may be emerging with year-end debtors overdue by >90 days but not impaired increasing to $31m from $8m despite FY25’s rise in provisioning expense. Inventory impairment provisioning remained compressed and CTEC continued its trend of stripping out restructuring and other costs. FY25’s trade payables spiked higher, bringing risk of mean reversion. They also note that both the CEO and CFO were internal appointments.

Healthcare

The market is overly focused on a perceived peak in TIDES-driven growth. While the 100,000-litre ramp in 2026 supports ~RMB 20bn of visible revenue, a multi-year growth stack extends beyond this, with ASO, cyclic peptides and RNAi contributing through 2029. The underappreciated angle lies in small molecule D&M, where management guides to 15%+ growth but scepticism persists following weaker 2025 delivery. Horizon Insights sees upside from commercialisation orders, overseas formulation expansion and TIDES precursor demand. If this segment outperforms, valuation upside is substantial (2H26 order disclosures will be a key catalyst). With CDMO utilisation improving and sector demand recovering, the company is well positioned for a rerating as growth re-accelerates beyond TIDES.

Pair trade off the same catalyst: Long PVH; Short GIII

Consumer Discretionary

Brian McGough sees a compelling long/short opportunity, driven by a structural transfer of economics as PVH reclaims key licenses. PVH represents ~40% of GIII revenue but closer to ~60% of cash flow, implying a sharp earnings reset as contracts roll off through 2027. Brian expects GIII EBITDA to fall from ~$325m to sub-$150m, with equity risk skewed towards mid-single digits. Conversely, PVH could see EPS power inflect from ~$11 to $15+ as higher-margin revenue is internalised, supporting a rerating from ~5x to ~10x EBITDA and a potential $200 stock. With near-term earnings distorted by transition dynamics (GIII cutting costs to mask deterioration while PVH absorbs upfront investment), the setup offers alpha on both sides of the trade.

Communications

The competitive landscape is intensifying and the existential risk for IRDM is getting bigger, according to Hamed Khorsand. The direct-to-device market is attracting well-capitalised entrants, with Amazon’s acquisition of Globalstar and Starlink’s expansion significantly increasing capacity and bandwidth relative to IRDM’s legacy network. At the same time, a proposed FCC rule could erode the exclusivity of IRDM’s spectrum, undermining a key pillar of its valuation. Customer behaviour is also shifting, with evidence of dual-sourcing and pricing pressure. While positive FCF has supported the equity story, Hamed expects rising investment needs to weigh on future generation. The recent advance in IRDM's stock makes it a good place to short/sell shares.

Copper: Moving away from a 19-year ceiling

Spot Copper (USD5.87) is finally moving away from a 19-year Ceiling that extends from USS4.00-5.00. The minimum long-term target is USD8.00-10.00. A multi-year ceiling is rarely broken easily but copper has been fighting for 4.5 years, and Chris Roberts comments that after a number of attempts it looks to have succeeded. The encouraging development since the 2022 low has been the series of higher lows. If Chris’s view is correct, going forward investors should expect a cleaner trending market with less volatility. The weekly chart features a 4-year Ascending Triangle, which is viewed as the launching pattern for the move away from the 19-year Ceiling at USD4.00-5.00 to USD8.00-10.00+. Go 20% long at market. Add 10% at USD5.8220, 10% at 5.7720 and 10% at 5.7220. The recommended stop is a daily close below USD5.2170.

US: Underlying inflation trends are cooling

Report by

Ironsides Macroeconomics

Barry Knapp argues that recent geopolitical shocks—particularly the Iran conflict—have not meaningfully altered the medium term economic or inflation outlook. By focusing on stated policy objectives rather than speculative geopolitical outcomes, Barry concludes that escalation risk remains limited and that markets largely share this view. Inflation expectations normalised quickly, equity markets avoided a sustained dislocation and the anticipated “fat pitch” equity market overreaction never materialised. Inflation remains the central macro issue, but underlying trends are cooling. March CPI was elevated due to an energy price spike, yet the key components - core goods, rent of shelter, and non housing services - continue to moderate. Barry stresses that post pandemic seasonal adjustment distortions are overstating inflation pressure and risk repeating policy mistakes made after the Global Financial Crisis. He views the Fed’s rigid 2% inflation target as poorly conceived and expects trend inflation to settle nearer 2.5% over time.

Consumer Discretionary

Scott Mushkin upgrades the stock to Buy, arguing the market underestimates the potential to turn around Foot Locker. Proprietary channel checks, including recent visits to “Fast Break” remodelled stores, point to materially improved traffic, ticket and margins, with early comps potentially reaching double digits. Crucially, the rollout appears extremely capital-light, supporting rapid scaling, with c.250 remodels planned by summer. Management confidence is rising, with fewer store closures than previously expected. Further upside could come from scaling clearance via the Going, Going, Gone! format, rolling out of sports trading cards within House of Sport and margin improvement through expanding private label apparel brands as well as DICK’S Media Network to the FL chain.