Europe

Consumer Staples

Following publication of its FY25 annual report Iron Blue lifts their RKT score +2pts to 28/60 (top quartile / fertile grounds for shorting). This reflects 1) 7-year high stripped out restructuring charge; 2) another spike lower in balance sheet trade spend accruals; 3) reduced inventory and bad debtor impairment provisions; 4) various additional risks related to NEC litigation, HS compensation changes and UK Suboxone civil proceedings within RKT’s contingent liabilities disclosures; 5) another increase in KPMG’s non-audit fees; and 6) the 14% discretionary upward adjustment to the CEO’s annual bonus to reflect strong share price performance (which compares with shares -14% FY26 YTD).

Industrials

The stock was pitched as a long idea at MYST’s latest Industrials Idea Forum, with prior events generating +11.4%, +10.4% and +9.5% average alpha. The presenter argued ENR’s recent underperformance vs. GE Vernova reflects macro-related fears among European investors, not fundamentals, leaving a valuation gap set to close. Multiple catalysts were highlighted, including “super cycles” in Gas Services and Grid Technologies and a profitability inflection in Siemens Gamesa expected in 3Q26. Street estimates are too low, with additional upside from potential changes to the Siemens AG trademark licensing fee and an end to the war in Ukraine. With strong backlog visibility and a clean balance sheet, the presenter has a TP of €225, offering 35% upside.

Materials

GMR upgraded KGH to Buy, following the recent pullback, arguing the stock offers a cheaper, lower-risk way to gain silver exposure. KGH is a much larger silver producer than often appreciated, with silver contributing ~26% of 2026 revenues (rising to ~32% at higher prices), supported by stable production and assets in low-risk jurisdictions. GMR forecasts earnings to rise ~70% Y/Y, with a base case of $79/oz silver in 2026, falling to $52 and $47 thereafter. The stock trades on ~7.7x 2026 P/E and ~4.4x EV/EBITDA (vs. ~7-8x for peers), with ~6.3% FCF yield. Valuation becomes increasingly compelling above $60-70/oz silver. Additional support comes from net debt trending to zero by 2028 and declining royalty charges.

Technology

GR20 views NEM's acquisition of HCSS as a strategically and financially well-structured transaction that strengthens its exposure to faster-growing, under-digitised infrastructure markets. The deal expands the group’s Build & Construct segment, increasing its addressable market and rebalancing revenue away from the more mature Design business. Crucially, the use of a 28% minority stake held by Thoma Bravo limits upfront cash outlay and preserves balance sheet flexibility, while reflecting ongoing challenges in private equity exits. The combination offers meaningful upside through cross-selling, cost synergies and AI-driven product enhancements, although EPS accretion is only expected from 2028. With valuation multiples now compressed following share price weakness, GR20 sees an attractive entry point.

North America

Communications

The competitive landscape is intensifying and the existential risk for IRDM is getting bigger, according to Hamed Khorsand. The direct-to-device market is attracting well-capitalised entrants, with Amazon’s acquisition of Globalstar and Starlink’s expansion significantly increasing capacity and bandwidth relative to IRDM’s legacy network. At the same time, a proposed FCC rule could erode the exclusivity of IRDM’s spectrum, undermining a key pillar of its valuation. Customer behaviour is also shifting, with evidence of dual-sourcing and pricing pressure. While positive FCF has supported the equity story, Hamed expects rising investment needs to weigh on future generation. The recent advance in IRDM's stock makes it a good place to short/sell shares.

Pair trade off the same catalyst: Long PVH; Short GIII

Consumer Discretionary

Brian McGough sees a compelling long/short opportunity, driven by a structural transfer of economics as PVH reclaims key licenses. PVH represents ~40% of GIII revenue but closer to ~60% of cash flow, implying a sharp earnings reset as contracts roll off through 2027. Brian expects GIII EBITDA to fall from ~$325m to sub-$150m, with equity risk skewed towards mid-single digits. Conversely, PVH could see EPS power inflect from ~$11 to $15+ as higher-margin revenue is internalised, supporting a rerating from ~5x to ~10x EBITDA and a potential $200 stock. With near-term earnings distorted by transition dynamics (GIII cutting costs to mask deterioration while PVH absorbs upfront investment), the setup offers alpha on both sides of the trade.

Consumer Discretionary

Scott Mushkin upgrades the stock to Buy, arguing the market underestimates the potential to turn around Foot Locker. Proprietary channel checks, including recent visits to “Fast Break” remodelled stores, point to materially improved traffic, ticket and margins, with early comps potentially reaching double digits. Crucially, the rollout appears extremely capital-light, supporting rapid scaling, with c.250 remodels planned by summer. Management confidence is rising, with fewer store closures than previously expected. Further upside could come from scaling clearance via the Going, Going, Gone! format, rolling out of sports trading cards within House of Sport and margin improvement through expanding private label apparel brands as well as DICK’S Media Network to the FL chain.

Consumer Discretionary

Tapestry has been on a roll, driven by Coach’s use of technology, customer insight and strong design team, but momentum now appears past its peak “buzz”. While Kate Spade is beginning to show signs of life, The Retail Tracker would avoid the name at current levels - with the stock up ~135% over the past year and +16% YTD, it looks fully valued at ~22x earnings. Investors could instead own LVMH or Moncler at similar valuations, or Capri Holdings as a turnaround. For aspirational exposure, The RealReal and Lululemon are seen as more compelling.

Energy stocks structurally mispriced

Energy

Energy stocks sit at the intersection of extreme under ownership, sector-leading FCF generation, a decade of starved capital investment and a valuation spread that has historically been a precursor to massive outperformance. Since KCR's first bullish publication in Mar 20, energy has returned ~500%, trouncing tech's ~300% and crushing the S&P 500's ~210% - and that outperformance has repeated across multiple entry points spanning wildly different market regimes. The bull case doesn't need a crisis as every data point in KCR’s analysis uses realised company financials when WTI averaged <$65. Contact us to see how energy companies are currently weighted across KCR’s various model portfolios as well as their highest ranked stocks.

US LNG: Qatar changes everything

Energy

Global LNG markets had been bracing for a wave of new supply led by Qatar, but that assumption is now in question. Qatar isn’t adding 32 MTPA - it’s effectively losing 12, tightening supply from a key swing supplier. More importantly, the disruption shifts the market from a cost-driven framework to one increasingly defined by security of supply. Reliability, not price, is becoming the dominant variable in long-term contracting. This reinforces the case for energy diversification and challenges expectations of a rapid decline in coal demand. The real beneficiaries are US LNG exporters, which gain pricing power, contract optionality and greater exposure to spot markets, with US capacity effectively de-risked. While market attention remains focused on oil, the more durable opportunity lies in a structural bull case for US LNG infrastructure. Highlighted names include Cheniere, Venture Global and NextDecade.

Industrials

2Xideas latest deep-dive focuses on APG - a high-quality compounder, supported by market leadership and durable advantages in a regulation‑driven, non‑discretionary end market. Demand for fire protection inspection and maintenance is underpinned by stringent compliance requirements, while low customer cost supports pricing resilience. The group differentiates through national scale, premium service and investment in skilled labour. With significant consolidation runway and a proven M&A playbook, APG is well‑positioned for sustained DD earnings growth. 2Xideas forecasts revenue growth of 7.4% p.a. (2025-2032E), adjusted EBITDA margins rising from 13.2% to 17.9% and cumulative FCF of $7.8bn (~45% of m/cap). Applying a 20x exit NTM P/E 2032E, they estimate total shareholder returns of 12.9% p.a. over this period.

Industrials

Grid constraints threaten to slow data centre construction growth, potentially disrupting STRL’s key revenue growth and margin expansion engine. Early signs are already visible, with decelerating construction data, softer backlog and margin pressure in its core E-Infrastructure segment. The CEC acquisition is a desperate move by management to mask a plateau in its site prep business and expand into Texas ahead of increasing competition. With cash flow moderating (and diverging meaningfully from adjusted earnings), insider selling rising and valuation elevated (~22x EV/EBITDA), OWS is targeting more than 30% downside.

Airline mega-merger? More signal than reality

Industrials

Reno Bianchi provides his take on reports that United Airlines' CEO Scott Kirby has floated a potential merger with American Airlines, though any transaction remains highly speculative. The logic is clear given American’s very precarious financial situation, but regulatory hurdles appear prohibitive, with the combined entity controlling ~40% of domestic capacity and likely requiring extensive asset divestitures. The more relevant takeaway is strategic: such signalling may reflect the DOT's recent openness to further airline consolidation, or serve as a tactic to frame smaller, more achievable transactions as less contentious by comparison.

AI: Compute scarcity & rise of infrastructure pricing power

Technology

Sean Maher argues the AI narrative is entering a critical second phase: compute scarcity is driving a structural repricing of tokens, with profound implications across the value chain. While semiconductors have captured ~80% of AI profits to date, tightening constraints in power, memory and optical networking are shifting pricing power towards infrastructure providers. Hyperscalers such as Amazon may be underappreciated beneficiaries as token demand from agentic AI explodes and supply struggles to keep pace. Meanwhile, Sean highlights early-cycle opportunities in analog and power semiconductors, where cyclical recovery is aligning with structural AI tailwinds. With proprietary Taiwan supply chain tracking and a strong record in identifying inflection points, Sean continues to uncover differentiated signals ahead of consensus.

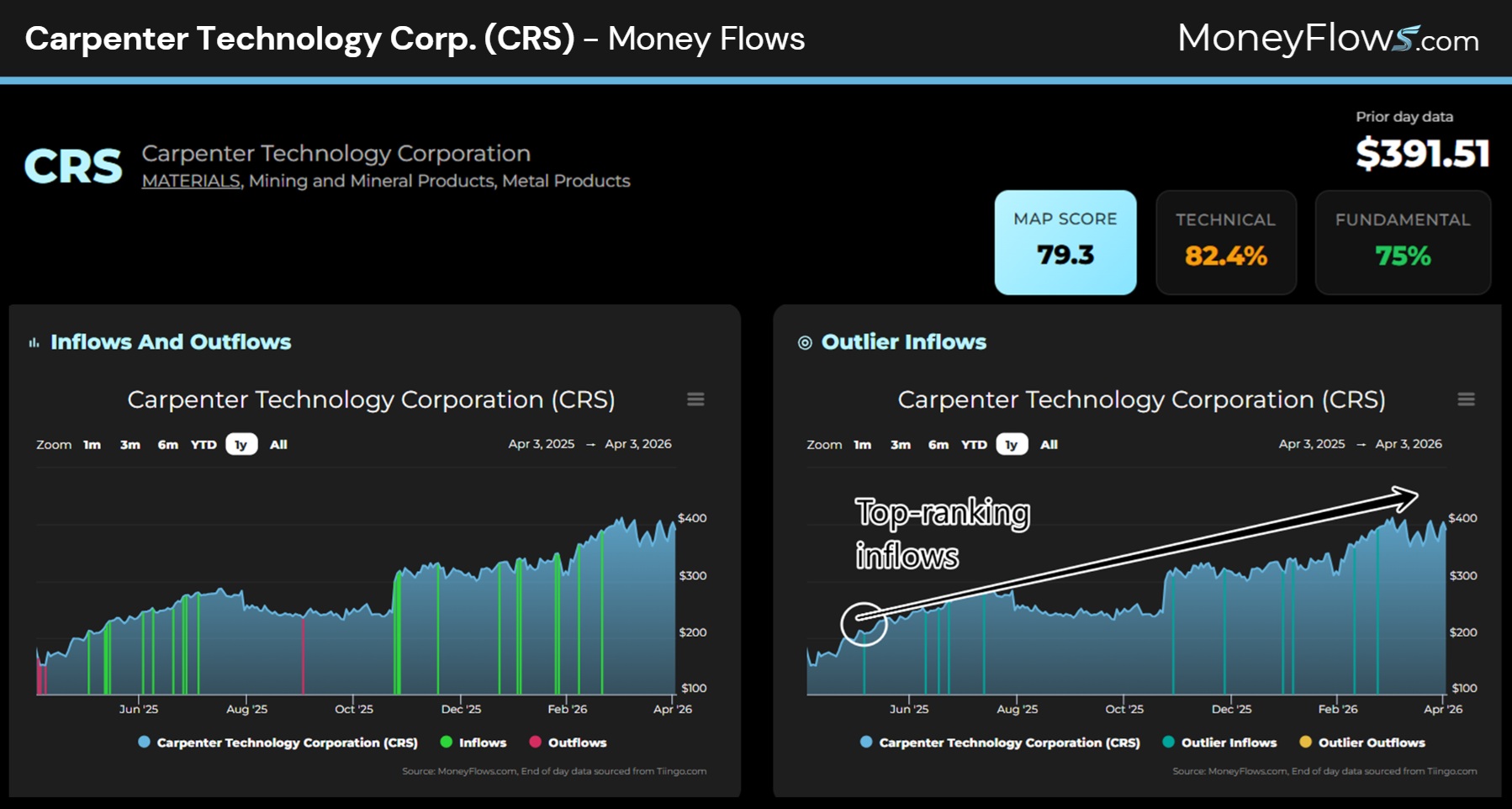

The best 3 space exploration stocks to buy in 2026

Technology

The space economy is a major structural growth theme, expected to expand from ~$614bn in 2024 to >$1.8tn over the next decade, with opportunities extending beyond rockets into the broader infrastructure stack. MAPsignals’ edge lies in identifying institutional inflows before the narrative becomes consensus, using its “Big Money” framework to find winners early. For example, Teradyne was flagged at ~$90 last June and has since surged to ~$342 on sustained inflows, with further upside anticipated. Applying the same process, they also highlight Carpenter Technology and Palantir as beneficiaries of the space buildout, supported by persistent institutional buying - including “non-stop” inflows into Carpenter. Tomorrow’s leaders are found by following the flows, not the headlines.

Asia

Healthcare

The market is overly focused on a perceived peak in TIDES-driven growth. While the 100,000-litre ramp in 2026 supports ~RMB 20bn of visible revenue, a multi-year growth stack extends beyond this, with ASO, cyclic peptides and RNAi contributing through 2029. The underappreciated angle lies in small molecule D&M, where management guides to 15%+ growth but scepticism persists following weaker 2025 delivery. Horizon Insights sees upside from commercialisation orders, overseas formulation expansion and TIDES precursor demand. If this segment outperforms, valuation upside is substantial (2H26 order disclosures will be a key catalyst). With CDMO utilisation improving and sector demand recovering, the company is well positioned for a rerating as growth re-accelerates beyond TIDES.

China sulfuric acid export curbs: A tightening noose on TiO₂ supply

Materials

Sulfuric acid is becoming a binding constraint for TiO₂, with potential Chinese export curbs reinforcing an already tightening market. Acid prices have doubled y/y to ~$280/t, with recent moves of ~$140/t in 2026 alone, driving a ~$400/t increase in cash costs for sulfate-route producers - pushing marginal Chinese capacity into loss-making territory. With ~80-85% of China’s TiO₂ output reliant on sulfate processing, the system is highly exposed, meaning acid shortages translate directly into lost production rather than margin compression from the market’s key swing supplier. As acid is increasingly diverted towards fertilisers and battery materials, TiO₂ is pushed into a residual demand bucket - implying lower operating rates, periodic shutdowns and reduced export availability. With demand relatively inelastic in the near term, the setup is a classic supply shock, supporting sustained pricing upside and favouring chloride producers such as Chemours and Tronox.

Memory earnings power has shifted structurally. Valuations haven’t

Technology

The memory cycle is being misread as cyclical rather than structural, with no near-term earnings peak as AI drives sustained demand. Capacity cannibalisation from HBM and SOCAMM is expected to constrain DRAM supply into 2028, with NAND also remaining tight, while LTAs could see future output effectively prepaid - reducing downside risk and reinforcing earnings durability. Yet valuations remain anchored to legacy frameworks, underestimating pricing power and cash generation, with net cash potentially >50% of m/cap by FY27 for players like SK Hynix and Kioxia. Within memory, Arete sees NAND fundamentals as more compelling than DRAM in the near term. They also upgrade Samsung to Buy, with a continued beat-and-raise cycle expected in coming quarters.

Aegea: From accounting shock to credit opportunity

Utilities

Lucror upgrades Aegea to Buy, arguing the recent accounting restatement marks a turning point rather than a deterioration in fundamentals. While revisions increased net leverage by 0.5x, they were non-cash in nature, with no impact on liquidity, covenant compliance or cash generation. Crucially, the outcome removes uncertainty around the scale of the adjustment, with the company retaining strong funding visibility and no near-term refinancing risk. Lucror sees value across the AEGEBZ curve, preferring the ’29s (87.7 / 11.6% / 2.6Y) and ’31s (90.3 / 11.7% / 3.6Y). A potential IPO in 2027 reinforces incentives to delever and restore credibility, supporting bondholders despite ongoing governance scrutiny.

Developed Markets

The world of maximising efficiency is dead

In a point that James Aitken has made many times, he discusses how readers are beneficiaries of globalisation. The essence of globalisation was optimising the system to the limit, wringing efficiency out of it until it almost broke (twice), eliminating any kind of slack and thereby for the owners of capital maximising profits and maximising expected wealth. It was a good run; Covid was the wake-up call, Ukraine another, and Iran a third. The world of maximising efficiency is dead and the world of maximising resilience is upon us. In basic terms, the world lacked the political will to complete the post-Covid inflation fight, alongside which economies haven’t invested nearly enough to complete the shift from efficiency to resilience, rendering the world more prone to exogenous shocks. It also means investors will prefer predictable free cash flow now as opposed to nebulous free cash flow in the future. The phase shift has barely begun. Bet on it.

Global liquidity will not bottom before 2027

Michael Howell points out that the global liquidity cycle peaked in Q3/2025 and is not slated to bottom before 2027. He has pared back risk exposure as the underlying currents driving liquidity lower will ultimately dominate geopolitical twists and turns. Economic activity is still slated to recover through 2026, even if the Iran conflict extends. Global liquidity looks more vulnerable than the broader economy. It was already falling pre-conflict, and higher oil prices, bond volatility (MOVE), and a stronger USD have further dented it, with the Global Liquidity Index (GLI™) falling to 44.1 in March from a December peak of 56.1. Bond market moves confirm this deterioration in global liquidity. Yield curves are inflecting lower and falling term premia highlight a demand for safety. Gold, meanwhile, is underpinned by China’s ongoing ‘monetisation’. Higher gold must translate into higher oil and other commodity prices.

Hungary: Orban’s fall

Katharina Klotz observes that even a heavily engineered electoral system could not save Hungarian Prime Minister Viktor Orbán. As a record share of voters turned out in yesterday’s parliamentary election, the conservative, anti-corruption, and moderately pro-European Tisza party achieved a landslide victory, securing more seats than Orbán ever achieved. Katharina expects Tisza leader Péter Magyar to take office within the next month. For the EU and Ukraine, this is very good news. She expects Magyar to lift Hungary’s veto on Brussels’ €90BN loan to Ukraine (90% probability) rapidly and play a more constructive role in EU policy from defence to China. With a supermajority in parliament, he will also be able to pass rule-of-law reforms required to unlock at least a high share of the €18BN of frozen EU funds (90% probability)—a crucial lifeline for Hungary’s struggling economy.

ECB is stuck

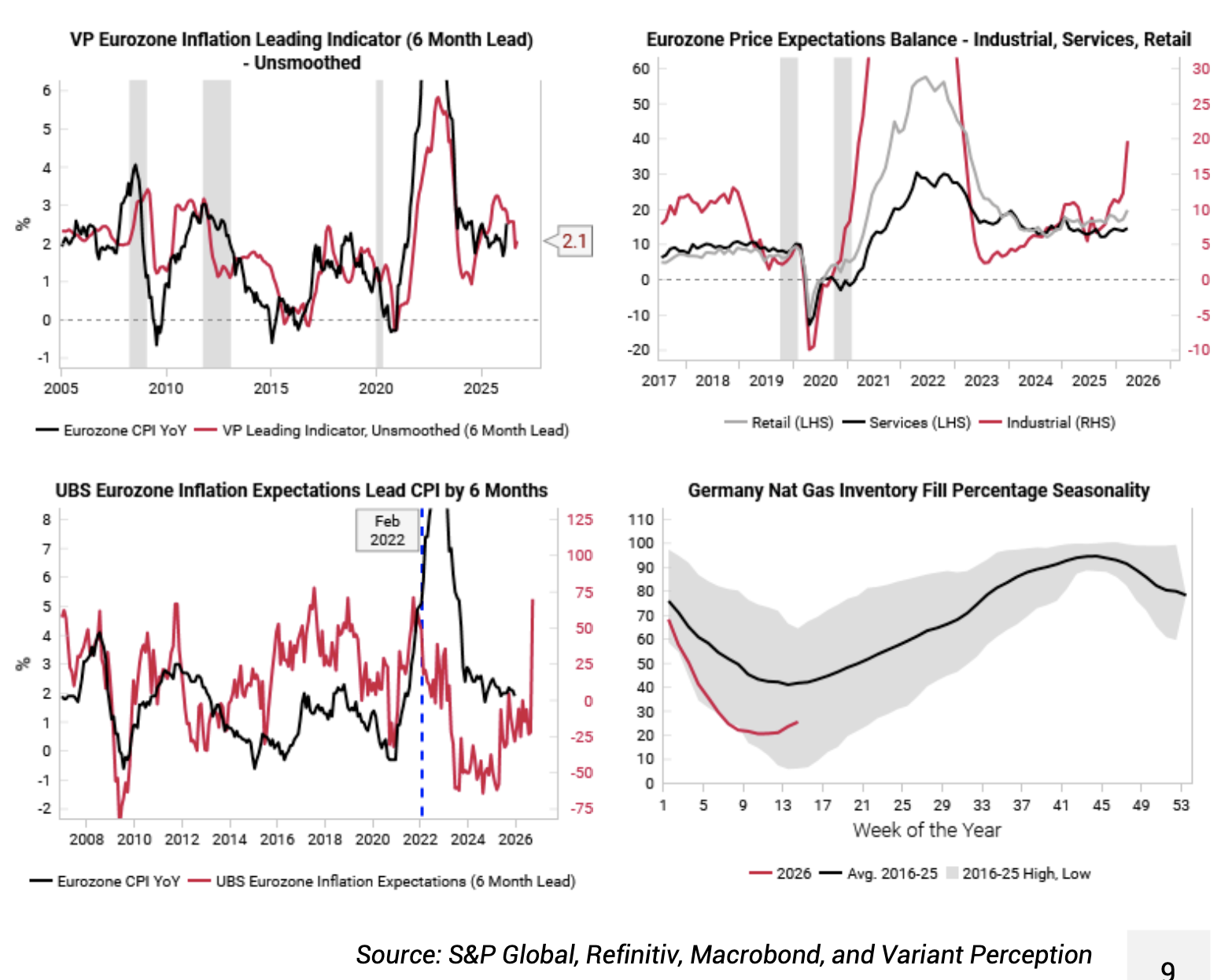

Variant Perception’s inflation leading indicator (top left chart) ticked higher this month, but there has been a much more pronounced move higher in eurozone price expectation surveys (top right and bottom left). As the team previously noted, the energy shock could not be coming at a worse time for the eurozone after a harsh 2025 winter already depleted natural gas inventories (bottom right chart). The ECB is risking a 2011-style policy error, hiking policy rates into a genuine growth slowdown. The ECB pivoted more hawkish at the March meeting, keen to avoid making the mistakes of 2022 when they were too slow to hike. There is a real danger that today's ECB is fighting the last war on stagflation, with the eurozone economy now more vulnerable to a growth slowdown. Receiving EUR 1y1y is a clean way to express this view, with the ECB likely to be forced into more rate cuts later.

A high conviction defensive portfolio

As David Woo expected, no deal between the US and Iran was achieved in Islamabad and he expects things to get uglier before the war ends. He viewed the ceasefire as a tactical move by both sides to prepare for the real escalation. Trump sent Vance, the last sceptic in his cabinet, to convince him to fall behind Trump’s plan to escalate the war. David’s central scenario remains a massive bombing campaign followed by a limited ground operation to take control of the Strait of Hormuz. VIX has flipped from backwardation to contango. David views short-dated vol as very cheap, especially relative to the longer-dated vol. He struggles to see the equity rally continuing and continues to hold his long Jun and short Dec Brent spread trade and his short Nasdaq position. He is holding his defensive portfolio with his conviction level as high as ever.

Iran conflict: A buying opportunity?

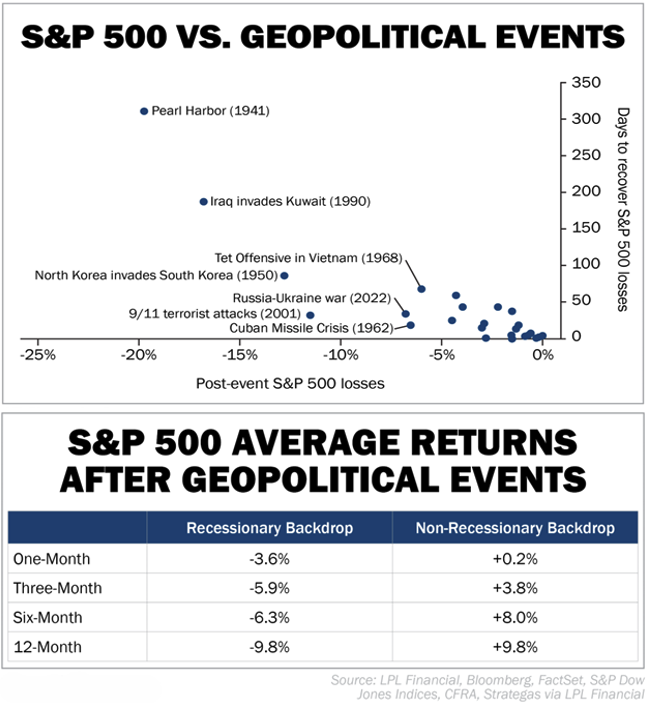

With no clear end to the Iran conflict in sight, investors are preparing for the worst. A look into history reveals that’s probably not necessary, according to Joel Litman and Rob Spivey. While markets typically wobble on geopolitical shocks, they rarely break. The chart shows how stocks have reacted to more than two dozen major geopolitical events since WW2. The S&P 500 Index's average decline during these events is about 4.5%. Markets typically bottom in roughly 18 days and recover fully in less than 39 days. Put simply, these events tend to create more fear than lasting fundamental damage. The recovery tends to arrive faster than investors expect. That's especially true when looking at geopolitical events that occurred nowhere near a recession. After events that happen near a recession, the S&P has averaged negative returns within one, three, six, and 12 months. In non-recessionary backdrops, returns have been positive for all of those time spans.

US: The AI boom continues

Graham Turner comments that there is plenty of inflation stuck in the pipeline despite some respite for energy prices. The headline CPI was up 0.87% m/m in March but the core CPI was well behaved. The key will be broader, second-round effects from the higher headline numbers. That will depend on consumer resistance: slower wage growth and uncertainty over job prospects due to AI could limit the ability of companies to push prices up more generally. The oil price shock has not yet had much impact on services demand, if the non-manufacturing ISM is any guide. The new orders index rose in March to its highest level since February 2023. There could be a delayed reaction to the Iran conflict, but Graham sees this as a potential sign that the US economy is indeed quite resilient. Low core inflation and no clear evidence that the energy shock or AI are damaging the economy would represent a big buying opportunity for equity investors.

US: Underlying inflation trends are cooling

Report by

Ironsides Macroeconomics

Barry Knapp argues that recent geopolitical shocks—particularly the Iran conflict—have not meaningfully altered the medium term economic or inflation outlook. By focusing on stated policy objectives rather than speculative geopolitical outcomes, Barry concludes that escalation risk remains limited and that markets largely share this view. Inflation expectations normalised quickly, equity markets avoided a sustained dislocation and the anticipated “fat pitch” equity market overreaction never materialised. Inflation remains the central macro issue, but underlying trends are cooling. March CPI was elevated due to an energy price spike, yet the key components - core goods, rent of shelter, and non housing services - continue to moderate. Barry stresses that post pandemic seasonal adjustment distortions are overstating inflation pressure and risk repeating policy mistakes made after the Global Financial Crisis. He views the Fed’s rigid 2% inflation target as poorly conceived and expects trend inflation to settle nearer 2.5% over time.

The US economy was losing momentum before the Iran war

According to Dave Rosenberg, the dominant macro theme this week is the growing chasm between headline optimism and what the underlying data are actually saying. The latest personal income and spending data confirmed it: the US economy was losing, not gaining, momentum well before the Iran war introduced a fresh layer of uncertainty. The big shock was the weakness in personal incomes and cyclical spending — not in inflation. Meanwhile, the FOMC minutes showed a Fed still in neutral mode, tilted towards cutting but hedging its bets. And then there's the labour market. Friday's strong payroll headline belied many signs of softness beneath the hood — the ISM jobs components are consistent with negative payrolls, and labour market dynamism has hit an eleven-year low. Dave's advice: fade the headline.

Emerging Markets

China debt deflation

Andrew Hunt believes that China’s balance sheet recession is continuing and may even be accelerating. A financial crisis is becoming a possibility as debt deflation intensifies. Nevertheless, corporate sector liquidity improved in March, presumably as a result of a strong positive influence from the external accounts. This is consistent with the strong CNY. However, China’s central bank reported a decline in its FOREX reserves that has not been corroborated by external sources. Andrew strongly believes that the PBoC is obscuring the true amount of FX intervention / influence on bond markets that it is obtaining by routing its flows through notionally private sector entities. The CNY will remain under pressure to appreciate until the PBoC finally eases its domestic stance. Longer-term yields have further to decline, but PRC equities should struggle until the PBoC U-turns on domestic liquidity.

China: Beijing meets with Taiwan’s opposition party

Mainland China’s government has pledged a package of policy deliverables aimed at improving cross-strait relations, following a visit to Beijing by the leader of the KMT, Taiwan’s main opposition party. After the visit, the mainland’s Taiwan Affairs Office announced a ten-point list of measures to promote cross-strait engagement. The measures include loosening restrictions on mainland residents travelling to Taiwan; restoring passenger flights from five large mainland cities; improved infrastructure links between Fujian province and the Taiwan-controlled Kinmen islands; and easier access for exports of Taiwanese agriculture and fishery products to the mainland. The PRC’s 10-point pledge lacks any timeline for implementation. Gabriel Wildau notes that Beijing may delay some or all of the measures pending KMT gains in local elections, or even until after a potential KMT presidential victory in 2028, thereby reinforcing the message that benefits to Taiwan are linked to the KMT’s electoral success.

Mexico’s domestic economy starts to pick up

Mexican exports continued to hold up well despite all the uncertainties around tariff policies and the USMCA, as well as the volatility in US auto import spending. So far so good. And now the economy is picking up at home, with better consumption and earnings numbers in the most recent data. It's still early days, and private borrowing and lending activity remains weak, but Jonathan Anderson will be watching closely for a broader-based recovery ahead. He doesn’t worry about balance sheet risks in Mexico; the external balance is solid, debt levels are moderate and inflation continues to fall. The main two variables to watch are (i) the worsening budget position and (ii) what still appears to be a somewhat expensive peso. If Mexico hits further volatility ahead, it's likely to come from one of these two sources.

Mexico: Caught between SLAMLO and a productivity problem

Caught between macro inefficiencies caused by the dominance of oligopolies (typified by the sprawling empire of Carlos Slim) and the poor allocation of fiscal policies of the AMLO administration, Mexico’s growth suffered in that 'SLAMLO' regime. Sheinbaum’s austerity promised a new future of 2% growth and 2% primary surpluses. The Sheinbaum administration is now caught between a return to the SLAMLO regime if its policy intervention doesn’t work and the need to address the productivity downturn. Manoj Pradhan asks: can the new policy easing restore the promise of a fundamental alpha, or will it put both the growth and fiscal legs at risk? Partly due to weakness and in part due to risk premia, MBonos provide value given the fundamental backdrop, which Manoj explores in his latest report.

South Africa: Absorbing an external shock

According to Peter Attard Montalto, what started the year as a macro “big bang” has shifted decisively into an external oil-shock management, with Q2 centred on resilience rather than momentum. Q2 will be dominated by the implications of the Middle East conflict. South Africa is moving from a position of relative macro strength into a live test of its ability to absorb an external shock. Peter notes that considerable resilience is still being shown, especially in the currency, and the impacts are likely to be less severe than in historical counterfactuals. Nonetheless, Peter does not want to gloss over what remains a serious shift. Growth has been trimmed, inflation raised, and rates are now expected to rise in May before easing only next year. Peter assumes there will only be a temporary oil shock through May, but a prolonged conflict remains a key risk that would start to lead to domestic security and supply concerns.

Venezuela: Improvements beneath the surface

In early March, Donald Trump publicly recognised Delcy Rodríguez as Venezuela’s sole head of state. On March 11th, the State Department followed suit. As Jose Ignacio Hernandez anticipated, that recognition did not produce immediate practical effects. The more important unresolved question was not whether she could act in that capacity, but how far that status would extend in practice across litigation, corporate control, and external asset management. One month later, little has changed on the surface. Beneath that surface continuity, however, Delcy’s recognition is beginning to reshape key incentives, exacerbate domestic frictions, and push the transition in new directions. In this report, Jose Ignacio maps the concrete developments he expects across four key areas: Citgo, the Central Bank, the IMF, and the billions in unpaid claims.

Commodities

Copper: Moving away from a 19-year ceiling

Spot Copper (USD5.87) is finally moving away from a 19-year Ceiling that extends from USS4.00-5.00. The minimum long-term target is USD8.00-10.00. A multi-year ceiling is rarely broken easily but copper has been fighting for 4.5 years, and Chris Roberts comments that after a number of attempts it looks to have succeeded. The encouraging development since the 2022 low has been the series of higher lows. If Chris’s view is correct, going forward investors should expect a cleaner trending market with less volatility. The weekly chart features a 4-year Ascending Triangle, which is viewed as the launching pattern for the move away from the 19-year Ceiling at USD4.00-5.00 to USD8.00-10.00+. Go 20% long at market. Add 10% at USD5.8220, 10% at 5.7720 and 10% at 5.7220. The recommended stop is a daily close below USD5.2170.

Oil: A new $80/bbl floor?

Report by

BCA Research

BC

According to Felix Vezina-Poirier, peak escalation in the US-Iran conflict is likely in the past, with both sides now signalling a preference for a deal rather than renewed escalation. The latest headlines confirm the de-escalation rumours that circulated late Monday, with signs that neither Iran nor the US is trying to escalate in Hormuz. Iran has also signalled it would not test the US blockade in order to facilitate talks. The lack of dramatic late-day headlines on Tuesday is likely another indicator of normalisation. The focus has shifted from re-escalation to the terms of a possible deal. Sustained de-escalation would be bearish for the front end of the oil curve, but would not warrant a return to pre-Iran price levels. BCA’s Commodity strategists see an $80/bbl floor, as inventories have been depleted and countries are likely to hoard more after this episode. Given that energy flows have picked up and peak tensions appear to be over, the team are now considering a modest tactical overweight on equities.

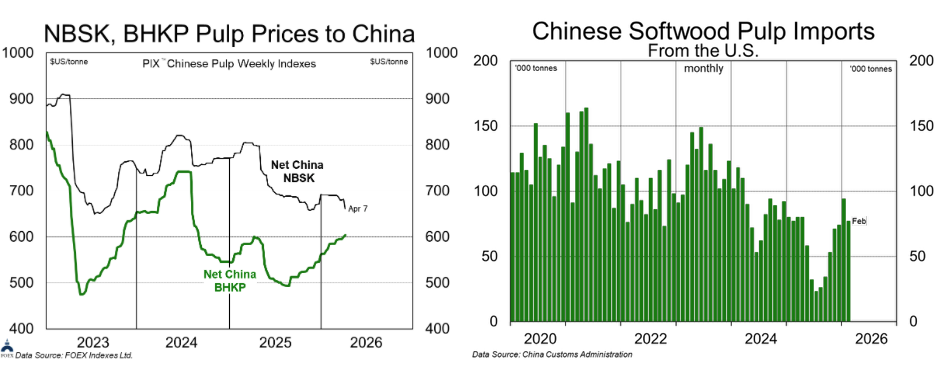

Pulp market gainers and losers

NBSK prices have been lingering at unprofitable levels for over a year now, far longer than thought possible. Current price levels are unsustainable for many mills: Back in December, Suzano indicated they believed ~35% of global BSK production was “loss-making” at $670 in China. Now, with rising fibre, energy and freight costs, that proportion is likely even higher. NBSK producers are under the greatest pressure, with more capacity closures likely and needed. With the January sale of IP’s fluff assets to GFC, there are no large, publicly traded fluff producers. Domtar and GFC cash flows should benefit from fluff price increases (as will smaller producer RYAM). If fluff/SBSK prices rise in line with announcements, it would also be supportive for NBSK producers, including MERC. Despite rising hardwood and fluff pulp markets, the team remain cautious on all pulp names. Without larger global NBSK industry supply reductions, prices will have little near-term upside and will lag any fluff pulp pricing gains.

Why Wall Street gets gold and silver wrong

In the final segment of the Silver Facts and Fantasies series, Jeffrey Christian of CPM Group discusses how investors should interpret gold and silver price forecasts, and why large shifts in bank price targets are often misunderstood. He explains how many institutions adjust their projections based on changes in current price levels rather than shifts in market conditions, which can lead to seemingly dramatic revisions. The presentation concludes with a discussion on portfolio construction, including how investors can think about allocating between physical metal and mining equities. Jeff explains how mining stocks behave differently from physical metals, sometimes lagging and at other times outperforming, depending on market conditions.

Click here to watch.