Europe

Communications

CEO Johan Svanstrom is the wrong leader for RMV’s critical transformation. Despite bringing a background as a “digital native” who scaled Expedia’s Hotels.com to over $3bn in revenue, more recent roles at BIMobject and RMV reveal a polarising leader who is disinterested in operational details and relies on a closed circle of advisors. Svanstrom will continue to champion an AI strategy with high-level, buzzword-driven directives while delegating core business oversight, creating significant execution risk and key-person dependency on a team he has already begun to alienate. His chaotic leadership and lack of operational discipline are a direct mismatch for the rigorous execution and financial control the company desperately needs. Paragon’s research includes interviews with former senior executives who worked with Svanstrom for more than 32 years combined.

Roche - SERD: Is lidERA being over-extrapolated?

Healthcare

Foveal published on adjuvant SERDS and sees a mispricing emerging between Roche and AstraZeneca, with the market potentially extrapolating lidERA into a broader commercial opportunity than is warranted, while underappreciating a more practice-aligned pathway elsewhere. The core debate is whether investors should be underwriting a broad SERD backbone in early breast cancer today, or positioning for a narrower outcome with a different catalyst path into 2027 that could shift relative value across the group.

Industrials

Investors remain far too apathetic towards European construction stocks, overlooking a multi-year infrastructure and housing investment cycle that could materially benefit BAM. The shares have hardly moved so far in 2026, despite the group reporting FY25 revenues up 9% Y/Y to €7.0bn, adjusted EBITDA up 20% to €400m and net profit almost tripling to €211m, while ending the year with €792m net cash, a €13bn order book and a new €40m buyback. BAM will issue new mid-term targets next year, but Europe’s 2026-2030 infrastructure strategy will release ~€600bn of funds further boosting the group’s order book, while civil infrastructure in UK currently faces a "herculean to-do list" that requires a 30-50% increase in investment over the next decade. TP €15 (55% upside).

Materials

APAM is evolving from a cyclical European stainless-steel producer into a more diversified materials platform, supported by its integrated recycling activities and higher-value product mix, which VRS believes should improve long-term margin resilience and sustainability alignment. Recent performance reflects a challenging market backdrop rather than a deterioration in core fundamentals, with VRS highlighting operational efficiency improvements, the strategic importance of ELG recycling and the acquisition of Universal Stainless, which expands APAM’s aerospace footprint in the US. Europe’s increasingly protective stance on steel imports could also add ~€200m to EBITDA from 2027 onwards while improving utilisation rates. Their analysis incorporates a valuation framework combining six different methodologies spanning intrinsic, peer-based and probabilistic approaches.

Technology

Following publication of its FY25 universal registration document, Iron Blue increase their CAP score +3pts to 30/60 (newly top decile and fertile grounds for shorting). This higher score reflects: 1) Increased stripped out costs (both restructuring and share payments). 2) Higher cost capitalisations. 3) Iron Blue’s conclusion that CAP may have fair value adjusted downwards the software on WNS’s balance sheet. 4) The dropping of organic growth as an alternative performance measure in a year of material acquisition revenue contribution. They also note that in FY26 Grant Thornton will replace PwC as one of CAP’s auditors - PwC had been in place for nearly three decades.

North America

How should you think about AI revenue exposure?

Trivariate argues investors need a more systematic way to think about AI revenue exposure, with the S&P 500 increasingly behaving like a giant AI ETF. Using an LLM-based process, they identified 262 US companies with meaningful AI-linked revenue across 13 business categories. They then analysed the daily beta-adjusted returns of those categories and found that many were highly correlated. Principal Component Analysis helped quantify this common factor structure, while correlation-based clustering consolidated the 13 categories into 6 broader AI-revenue groups that better capture both business exposure and how the stocks have actually traded. These 6 categories are: 1) Utilities / Datacentre REITs, 2) Datacentre Buildout, 3) AI Platform, 4) Vertical & Edge, 5) Services & Integration, 6) Memory and Semiconductor Capital Equipment. To access the full report and investment conclusions including long and short ideas contact us below.

Special Sits Idea Forum

MYST’s buyside events continue to deliver impressive performance (~19% avg. alpha on highlighted ideas at their previous Special Sits Forum). Their latest event featured a high number of potential takeouts / M&A plays, business separations, several Media stocks and various AI-related companies. The most compelling ideas included:

Chemours (CC US) - Refrigerant share gains + “free kicker” from steepening China TiO2 cost curve. TP $46 (110% upside).

ITT (ITT US) - High-quality pumps pure-play experiencing positive mix shift. TP $284 (45% upside).

Valmont Industries (VMI US) - “Non-obvious” AI infrastructure play benefitting from utility pole pricing inflection. TP $709 (35% upside).

Fundrise Innovation Fund (VCX US) - AI / Anthropic proxy trading at ~10x NAV with upcoming lock-up expiry catalyst. TP $50 (75% downside).

Communications

The latest reporting suggests SPCX is targeting a ~$1.75trn valuation, which would make it the largest IPO in history, but New Constructs argues the implied expectations are “out of this world”, with investors materially underestimating execution risk, competitive intensity and capital requirements. Their report highlights rapidly falling Starlink ARPU, misleading non-GAAP reporting and weak internal accounting controls, alongside governance concerns including minimal voting rights for IPO investors, extensive related-party transactions and potentially significant future dilution. They also note that ~80% of IPO proceeds are already earmarked for debt repayment and other obligations, while customer concentration risk remains elevated. New Constructs' reverse DCF analysis suggests the proposed valuation implies SPCX will ultimately generate both the highest revenue and highest NOPAT of any public company; sees >70% downside if revenue growth merely tracks historical rates.

Consumer Discretionary

ROST exceeded very high expectations delivering an impressive 17.0% comp with the majority driven by traffic and EPS of $2.02 - ahead of Chuck Grom’s Street high $1.95 estimate and guidance of $1.60-$1.67. Even more impressive, most of the uptick in transactions is coming from new customers thanks to improved branded merchandise, better in-store experience and refreshed marketing initiatives. This should improve confidence in ROST’s ability to “comp-the-comp” later this year despite difficult comparisons. Near term, Chuck raises his 2Q26 SSS estimate to 7.0% with EPS of $1.90, while FY26 and FY27 EPS increase to $7.80 and $8.75, respectively.

Consumer Staples

Recent fieldwork and earnings results reinforce R5's upgrade from Sell to Buy earlier this year. Their thesis centres on improving merchandising and better store execution driving traffic, sales and gross margin recovery - trends which now appear to be emerging in both store checks and reported numbers, with comp sales (+5.6%) and operating margins (4.5%) beating forecasts. R5’s latest visits across multiple US markets suggest stores are “better, but nowhere near” where they ultimately need to be, supporting the view that the turnaround remains in its early stages. They also highlight a notable re-engagement from store employees, which they see as an underappreciated signal that traffic trends and customer experience could continue improving through 2026. In contrast to Walmart, where continued upside increasingly requires Amazon-like growth and margin characteristics, TGT “doesn’t have to be a superhero” for the equity to work. TP $197 (50% upside).

Industrials

Hamed Khorsand’s bearish call on KRMN is already playing out with the shares down ~40% since his Sell initiation earlier this year, yet he continues to see material downside with a 12-month target price of $37. Acquisitions masked underlying weakness in the company’s core business during Q1. Excluding newly acquired maritime defence assets, revenue would have declined sequentially, despite a strong defence spending environment. Hamed also flags KRMN’s rising contract assets (unbilled receivables), which now exceed 32% of the company’s 12-month trailing revenue, alongside weak FCF generation. Valuation remains elevated at ~42x EV/EBITDA, while comps begin to look tougher as the year progresses.

Materials

ESI is benefiting from an “acceleration in its growth algorithm”, driven by a structural shift away from consumer electronics to be more data centre / B2B driven. The market continues to underappreciate how materially the portfolio has improved, with enterprise customers now representing ~80% of sales (vs. ~60% in 2022) and gross margins expanding by >600bps (avg. ~50% gross margins and ~26% EBITDA margins over past 5 years when stripping out the effects of metals pricing). Growth drivers include Kuprion’s nano-copper technology, which could exceed a targeted $100m sales run-rate by 2028, alongside strong momentum from Micromax and EFC Gases, which are benefiting from growing demand in advanced electronics, semiconductor manufacturing, electrical infrastructure and aerospace application. Fermium forecasts revenue reaching ~$3.6bn by 2027 alongside mid-teens EPS growth.

Technology

CORZ moves sharply higher in Arete’s AI infrastructure rankings following a major expansion in its long-term power roadmap, with them now modelling 3.6GW of IT load and $6.3bn of NOI by 2032 - up from prior estimates of 1.9GW and $3.7bn, respectively. Arete argues demand for AI compute remains “off-the-charts”, while CORZ is becoming increasingly attractive to hyperscalers through the expansion of its Pecos and Muskogee campuses into gigawatt-scale AI data centre sites. Importantly, the company has leveraged its existing CoreWeave contract into $3.3bn of financing, giving it sufficient capital to begin pre-building new facilities before signing additional leases, which Arete views as a key competitive advantage. With leasable power expected to nearly triple over the next few years, Arete raises their TP to $55 (100% upside) and now ranks CORZ alongside Applied Digital as a top pick in colocation infrastructure.

Technology

DSG combines one of the logistics software industry’s strongest network-effect moats with a highly disciplined acquisition strategy. The key differentiator is the company's proprietary Global Logistics Network, which processes >24bn transactions annually and embeds DSG deeply into mission-critical compliance and supply-chain workflows, supporting gross retention in the mid-to-high 90% range and NRR above 100%. Management’s acquisition track record is also underappreciated, with 34 deals completed since 2016 generating >15% RoAIC while maintaining a conservatively financed balance sheet. Based on 12% annual revenue growth, stable‑to‑expanding margins, and an exit NTM non‑GAAP P/E of 22x, 2Xideas forecasts mid‑teens annualised total shareholder returns through FY33E.

800 VDC data centre plays

Technology

The shift towards 800 VDC data centre architectures creates a major new opportunity for SolarEdge and Enphase, whose distributed solar engineering expertise positions them well to handle the hyper-fast, chaotic load swings created by AI infrastructure. Both companies are repurposing existing R&D and already have products in testing, with Abacus arguing their architectures could compete effectively against traditional industrial incumbents such as Eaton and Vertiv. Abacus estimates the emerging market opportunity could reach ~$5-6bn by 2031 and believes successful adoption of 800 VDC systems could ultimately double earnings for both companies. Navitas is also highlighted since it provides the chips needed to make solid-state transformers work for companies such as VRT, ETN and ENPH; no matter whose product wins, NVTS benefits.

Rest of World

Consumer Discretionary

New car price deflation continued to pressure WBC in H1, as legacy brands cut prices to compete with lower-cost Asian competitors, forcing inventory repricing and depressing margins. Rowan Goeller argues this is cyclical rather than structural, expecting margins to normalise through 2026, while the increased new car sales are growing the car parc – a positive for WBC in the medium- to long-term. He also highlights the group’s cash-generative model, data-driven pricing advantages and operational initiatives such as Inspectify, its in-house vehicle inspection platform. Rowan continues to view WBC as a growth business and maintains a R52 target price (45% upside).

Telfer vs. KCGM: The revival of Aussie icons

Materials

While the market remains cautious on Northern Star Resources given ongoing KCGM execution risks, potential cost overruns and weak near-term news flow, the company is nearing completion of a transformational ~A$1.8bn mill expansion to 27Mt/yr, part of ~A$5bn total investment into KCGM across FY22-FY28, which could ultimately restore production towards ~0.9Moz/yr by FY30. However, with management still needing to rebuild investor trust, GMR retains a Hold rating on NST. In contrast, they are more constructive on Greatland Resources, which is still in the early stages of reinvesting in Telfer / Havieron, with ~A$2.8bn of potential capex through FY32 supporting a pathway back towards ~0.4-0.5Moz/yr production by the end of the decade, alongside exploration upside at SLC and West Dome. Given the scarcity of >300koz/yr gold assets, GMR believes Telfer could become a strategic bolt-on acquisition for peers seeking scale in Australia.

CSN: Bridge loan supports a show me credit

Materials

EM Spreads maintains an Opportunistic Overweight on CSN bonds, arguing the market is pricing the credit closer to a distressed recovery trade than a conventional single B credit, despite no near-term liquidity event emerging from 1Q26 results. While leverage and FCF remain weak, a new US$1.2bn bridge loan materially improves funding visibility and reduces refinancing pressure, buying management more time to execute on deleveraging. The key catalyst remains tangible progress on asset monetisations, while EM Spreads sees the best risk reward in the CSN 4.625% 2031s and CSN 5.875% 2032s. The argument for the 2031s is more defensive, based on shorter duration and slightly better downside control, while the 2032s are the higher upside expression for investors willing to accept modestly more duration in exchange for incremental spread and carry.

Developed Markets

AI and Say's Law

Without a doubt, AI is a transformative tech with a strong future. However, Andrew Hunt says that some of the markets’ assumptions appear wayward to him. To “believe” in the AI Boom and in current market valuations, one must assume that the risk-free rate in the economy is at an equilibrium level currently; that there is minimal misallocation of capital occurring; that this is not simply just another credit boom; that forecast rates of likely AI take-up are accurate; and that Say’s Law will prevail (i.e. supply will create demand). Andrew finds evidence that many of these preconditions have likely already been invalidated. In previous manias, the “bell-was-rung-at-the-top” by often esoteric events within the plumbing of the credit system. It remains to be seen whether Mr Warsh will begin a quantitative tightening in the face of rising inflation, or bow to the political realities.

AI and its discontents

The AI buildout is transforming the US economy almost uniformly for the better. Output is increasing both as a result of higher investment and higher productivity. If AI works, the US will have an unassailable dominant position in the global provision of services. It appears not everyone agrees. At a commencement speech at the University of Central Florida, the fairly innocuous comment that the rise of AI is the next industrial revolution was met with booing from students. There is clear political backlash against AI, including in America, the country that stands to benefit the most from its development. Yet, technological change has a habit of steamrolling political concerns over its deployment, and technology tends to determine the political economy rather than the other way around. Dimitris Valatsas is not worried (yet) about political opposition derailing US dominance in AI, but it’s worth watching closely.

Why is quantum beautiful?

Investors tend to focus on AI because they can see the outcome directly: chatbots, images, agents. Quantum is different, points out Konstantin Fominykh. The tech attacks trillion-dollar bottlenecks, with potential use cases in drug discovery, materials science, cryptography and weather simulations. Near-term commercialisation is already appearing, such as Quantum-secure communication, Post-quantum cybersecurity, Defence applications, AI acceleration, Quantum sensing technologies. Nvidia became the dominant AI infrastructure story because every AI workload required GPU compute. However, in the future compute may become a multi-layer ecosystem with traditional CPUs and GPUs working alongside quantum processors that handle optimisation and highly complex situations. Don’t miss out.

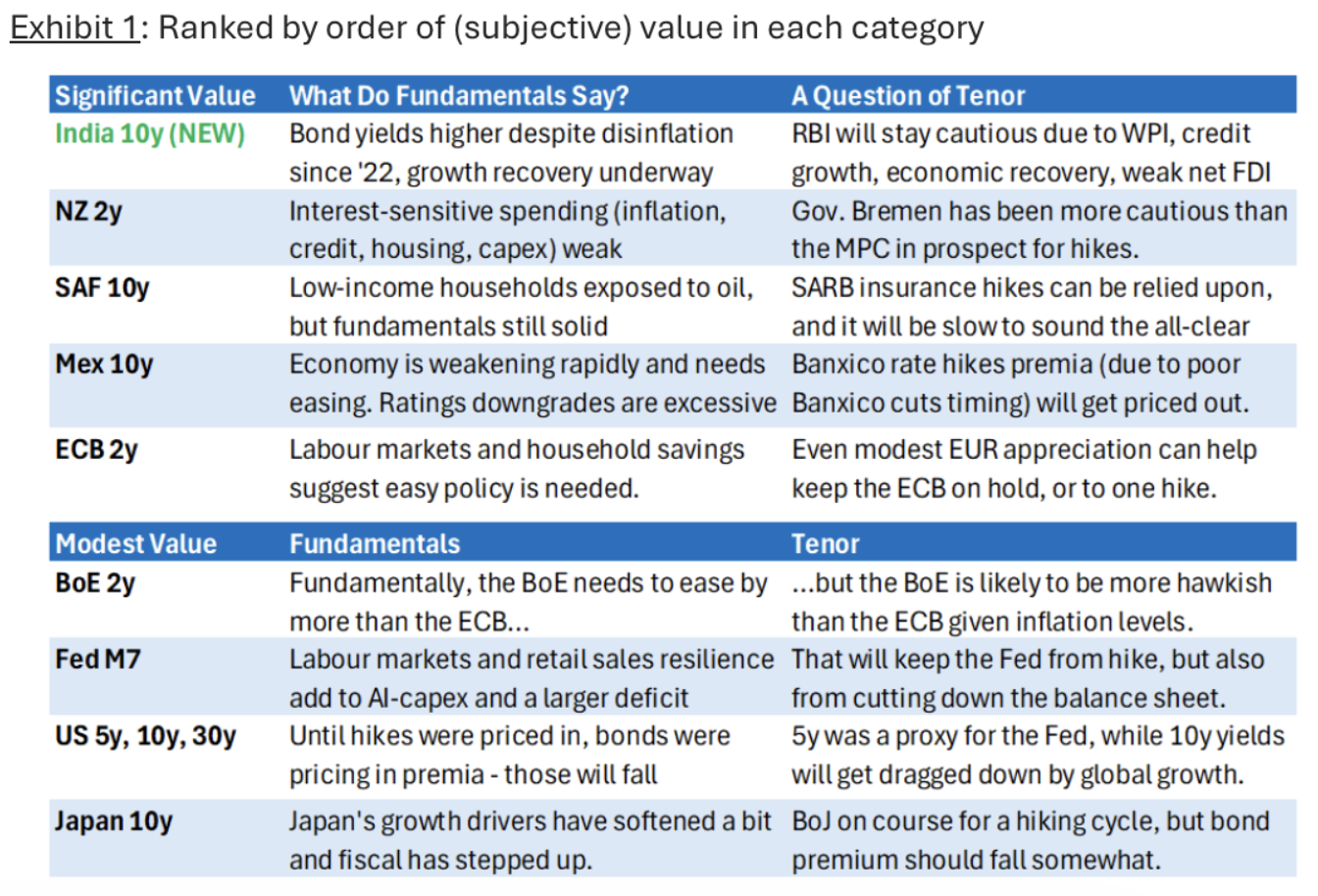

Bonds: Where to receive… and why

If the Strait of Hormuz is close to opening up, keeping in mind that normalisation of flows and data will take months, Manoj Pradhan points out that there are economies which lack either economic resilience or a contractionary policy mix that offer fundamental value either in the front or back end, or both. All front ends will rally, but how far they can go depends on how much was priced in relative to the economic resilience of the economy. In his latest message, he provides a list of where to receive, by economy and tenor, and why. He sees significant value in India 10y, with bond yields higher despite disinflation since ’22 and growth recovery underway; the RBI will stay cautious due to WPI, credit growth and economic recovery. He also sees significant value in NZ 2y, SAF 10y, Mex 10y and ECB 2y.

The ECB’s coming hike

According to Mark Bathgate, the ECB is likely to hike at their next policy meeting on June 11th. Mark points out that President Lagarde has clearly stated, “memories of 2022 are very fresh” – hence he says that the ECB is going to prioritise its inflation stability mandate and tighten policy to deliver on that. He thinks they will hike 25bps, then suggest that more hikes are possible. The most likely scenario for further hikes after the initial one is an “end of war” outcome – where business/confidence rises, but inflation continues to rise due to the 12-18 months disruptions/inflation in energy-intensive products. The market has moved between pricing 2 and 3 rate hikes over recent weeks – this seems reasonable pricing. A cash rate around 2-2.5% and 100bps curve to the 10-year part of the curve is seen by the ECB as “back to normal”, and a sustainable place for monetary policy to be (also good for the health of the EU banking sector).

Europe and China: An upcoming full-blown trade war?

The European Union has laid the groundwork for a more robust industrial policy amid anxiety over the bloc’s growing trade imbalance with China. On May 18th the FT reported that the EU is developing new rules that would require European companies to buy critical components, including chemicals and industrial machinery, from at least three separate suppliers, not all from the same country. Additionally, a growing chorus of EU voices is backing tougher action on China, such as French President Emmanuel Macron calling for the EU to adopt anti-dumping and anti-monopoly measures akin to Section 301 of the US Trade Act of 1974 to counter dependence on China. There are also signs that China’s strategic patience with Europe is running out. Dinny McMahon says MNCs exposed to both Europe and China need to urgently conduct supply chain audits and develop contingency plans for a sharp downturn in ties between Beijing and Brussels.

US: …and the answer is margins

If you want to understand equity markets today, Paul Krake advises to start and end with margins. The blended Q1 2026 net profit margin for the S&P 500 came in at 14.7%, the highest figure since FactSet began tracking the metric in 2009, eclipsing the 13.2% record set just one quarter ago. The direction of travel is unambiguous. What is changing now, and what makes this margin story qualitatively different from the cycle-on-cycle expansions that preceded it, is who participates. The hyperscalers are not building this infrastructure for their own consumption. They are building the road, and the rest of the economy pays a toll to drive on it. The productivity gain accrues to the customer. The S&P at all-time highs is not a puzzle. The cleanest expression of this view in a single trade is long the equal-weight S&P 500 against the cap-weighted index. The next phase of this story is breadth. Equal-weight is how you own it.

US: Warsh’s natural bias

In the last week markets have moved to peg the Fed for about 28bps of hikes in the next year, a substantial shift from the 1-2 cuts priced in late February. Warsh assumes the Chair with a challenge to his natural bias – higher productivity via AI implying stronger GDP growth potential (but less inflation and hence need to hike), weak jobs markets but immigration arguably keeping the U/E rate down (which should point to rate cuts), a tighter and smaller Fed balance sheet (that implies rate cuts to offset) and different measures of inflation (trimmed mean over core PCE which conveniently is lower and implies rate cuts). This set of biases imples that Warsh is more of a cutter than a hiker. While the markets peg the first Fed hike in March 2027, Craig Ferguson thinks that the Fed will get an inflation shock in the next 3-4 months that leads to them hiking in Q3.

US Treasury yields head into a new higher range

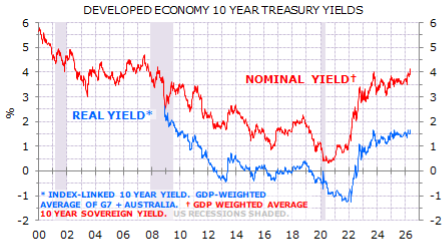

Gerard Minack points out that the post-GFC era of low rates is over: long-end rates are now back in the pre-GFC range (Exhibit 1). Gerard says they will remain high as colossal budget deficits collide with rising investment spending and sticky inflation. Structurally high real rates increase the risk of a fiscal blow-up. AI will add to upward pressure on real yields if it lifts trend growth rates. The increase in yields pre-dated the Gulf conflict, but the conflict accelerated the rise in both expected inflation and real rates. Higher rates will be a big problem for western world public finances. Political populists have little appetite for pre-emptive budget repair, so it seems only a matter of time before a developed economy faces a public sector debt crisis.

USDJPY: Stable but unsustainable

USDJPY seems stable for now, caught between the upward lift from the negative real interest rates in Japan, and the gravity of valuation and the MoF’s threats of interventions. Stephen Jen believes that the next big move in USDJPY is down. But elevated oil prices may delay the timing of this prospective correction. USDJPY remains elevated near 160. There are several powerful forces pushing USDJPY higher, even though the JPY is already grossly undervalued. Japan’s real interest rates remain very negative. The BOJ’s policy rate is minus-65 bps in real terms, and minus-300 bps relative to the Fed Funds Rate. Further, the negative terms-of-trade shock from higher oil prices is the second driver of USDJPY. In essence, the JPY is the mirror image of the USD, which has been propped up by capital inflows over the years, attracted by the higher carry and capital gains in US equities, pushing the USD deep into overvalued territory.

Emerging Markets

EM strategy

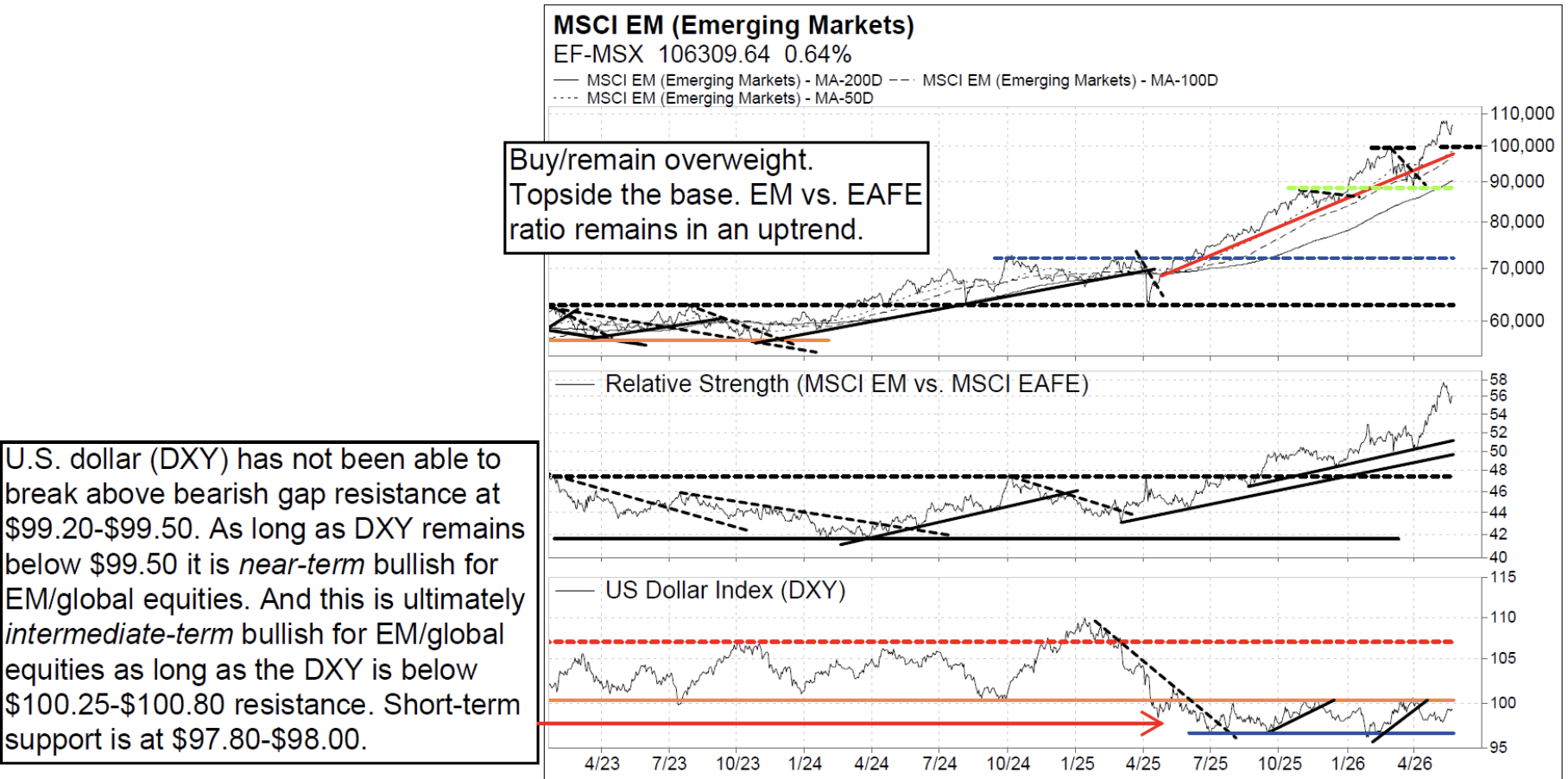

The Vermilion team remain overweight MSCI EM vs MSCI ACWI since Jan and continue to be overweight EM vs EAFE since August 2026. The team also remain intermediate-term bullish from a price perspective as long as EEM-US is above $57 (up from $55), and near-term bullish as long as $61.50-$62.00 and $59.50 supports hold. EEM-US supports to buy are at $63.50, $61.50-$62.00 and $59.50. A new uptrend has begun. When it comes to specific countries, the team especially like Taiwan and South Korea, with no other countries coming close. For sectors, the team’s overweights include EM tech and EM Industrials. EM Technology has been so strong, and has such a large weighting in EM, that it has become increasingly difficult for any other sectors to outperform relative to MSCI EM. Many leading Technology stocks that we have recommended in recent months are quite extended, and we would be buying on any pullbacks.

Argentina: A battle of wills

Marcos Buscaglia focuses on the discrepancies between the IMF and the Argentine government that transpired in the recent IMF report. While the IMF sees GDP growth converging to 3%, the government hopes that reforms could lift growth up to 4.5%. The IMF projects inflation reaching single-digits by 2028, yet the government thinks the decline could be earlier and faster. The target set for FX reserve accumulation for the year is $8bn, but the IMF scenario is at least $10bn. The authorities promised to limit FX selling intervention and made no promise on the removal of lingering FX controls. Marcos says the government has implemented a more expansionary monetary policy, without compromising its FX and price stability targets, so far. The economy will continue improving somewhat in the coming month. Inflation will be closer to 2% in May. Marcos expects the central bank will likely keep rates around current 20% levels.

Where’s China’s fiscal crisis?

Things continue to look absolutely awful on the Chinese public sector front. Not only is China already one of the most heavily indebted economies in the EM universe, it also runs ever-widening public deficits. Then there’s the looming pension crisis. In short, claims Jonathan Anderson, this appears to be a disaster in the making. So, why haven’t things exploded? On the one hand, there are already growing austerity pressures in the economy, as local governments hike levies and fees on businesses and push for higher pension contributions. I.e., the fiscal mess is already becoming a drag on activity and growth. At the same time, however, there is no sign of budgetary funding stress. Why? Because the government completely controls both funding costs and flows via its state-owned monopoly in the commercial banking system, which in turn holds virtually all fiscal and "quasi-fiscal" debt. The real question is about the health of banks, not budgets.

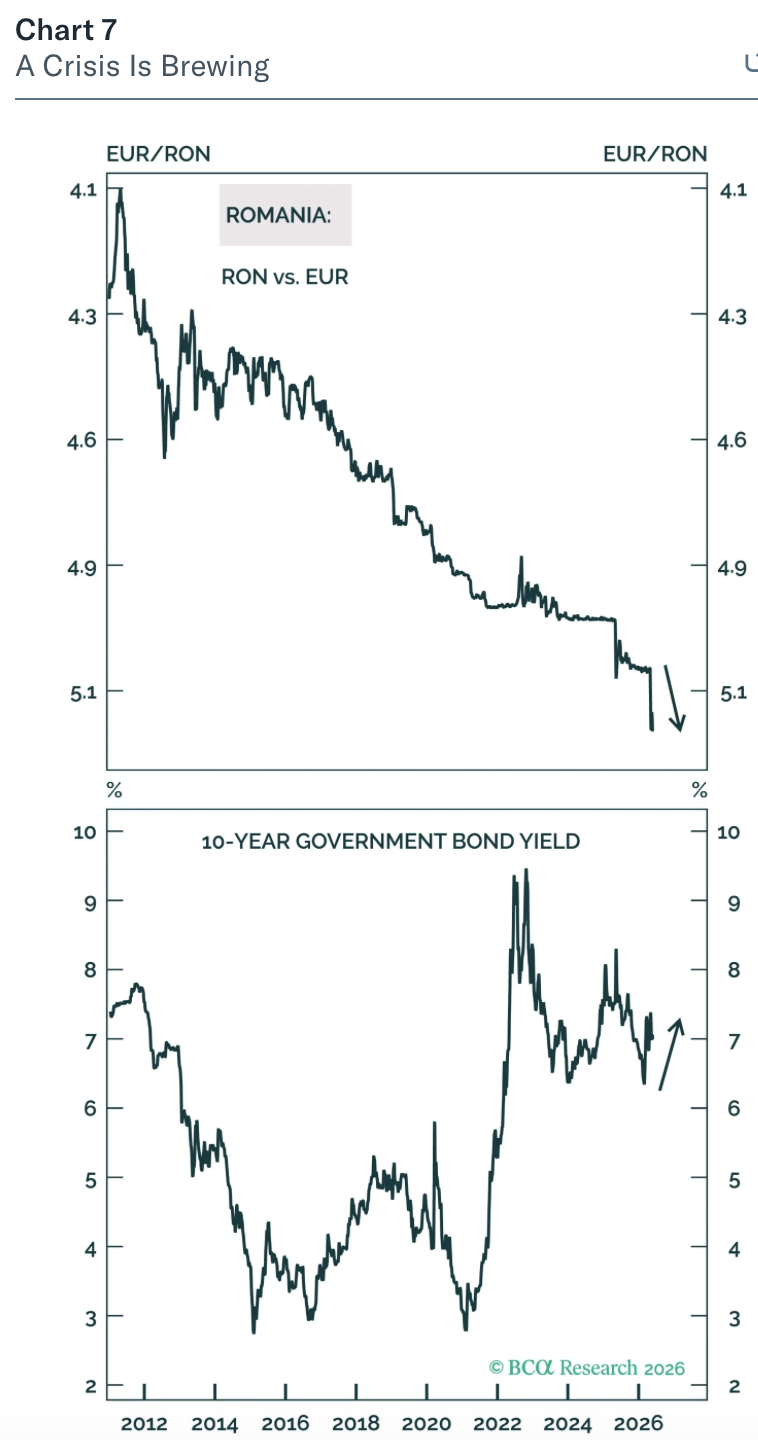

Romania: A budding currency crisis

Report by

BCA Research

BC

Romania’s macro backdrop has deteriorated to the point where exchange-rate stability is becoming increasingly difficult to sustain. The country’s imbalances have been allowed to build because policymakers kept policy too loose while foreign funding was readily available. The government's collapse makes fiscal tightening less likely. Instead, Romania will enter a vicious circle of reduced foreign financing, currency depreciation, higher inflation, substantial monetary tightening, recession, and deterioration in the fiscal position. The adjustment will likely come through markets: weaker foreign inflows, currency depreciation, tighter policy, falling domestic demand, and renewed fiscal pressure. The team recommend shorting the Romanian leu versus the euro, getting out of domestic bonds (the team prefer Hungarian, Polish and Czech domestic bonds), underweighting Romanian sovereign credit in EM credit portfolios, and underweighting stocks in frontier market portfolios.

Korea: Everything but a hike

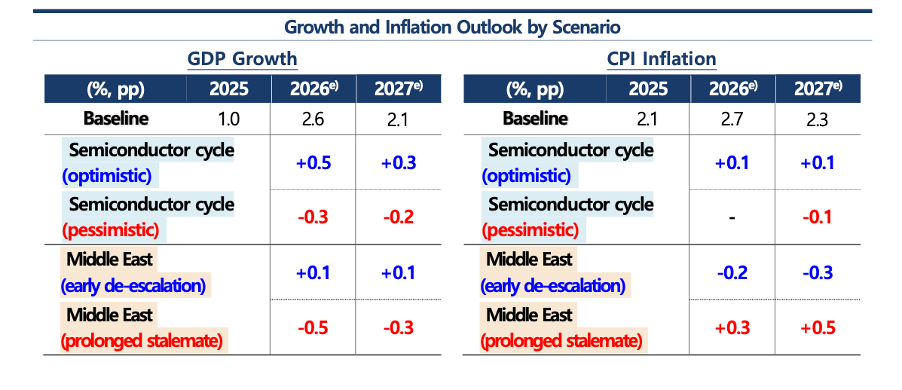

The BOK didn't hike today, but reading through the materials, Paul Cavey comments that it was a surprise that it stayed on hold. The governor made it clear that rate hikes were coming. Three aspects of the forecast stand out for markets. The BOK now thinks the current account surplus will be $250bn in 2026, up from a $72bn forecast just months ago. The bank also thinks core inflation will be 2.4% in 2026. That feels low, given core was at 2% before either of the shocks from Iran and semiconductors, and with the BOK itself flagging that big tech profits will lift nominal wages. If the semiconductor cycle and the Middle East situation were to evolve simultaneously in the pessimistic direction (see chart), adverse feedback loops between financial conditions and the real economy would emerge, further amplifying the growth slowdown.

South Africa: Yield curve repricing

South Africa’s yield curve has partially recovered from the March oil shock, which lifted yields across maturities, with the 10-year moving from around 8.1% at the late-February low to 9.4% at end-March, before easing back to around 8.65%. The curve remains materially below the old stress regime, but it is now higher and flatter because the short end has repriced more aggressively than the long end, as markets moved from pricing around 50bp of SARB cuts to roughly 75bp of hikes for the rest of 2026. The March shock did not undo the fiscal-credibility gains that drove the earlier rally, but it has made the route to further long-end compression narrower and more stretched out. The fiscal-credibility narrative remains supported by the stronger 2025/26 fiscal outturn, resilient revenue, lower-than-budgeted debt-service costs and Moody’s positive outlook. Looking ahead, Peter Montalto now sees the 10-year SAGB ending 2026 around 8.5%, from 8.0% before the US-Iran conflict.

Commodities

Copper’s record prices: What happens next?

In this presentation, Jeffrey Christian of CPM Group gives an update on gold, silver, platinum, and palladium prices before turning to copper. He explains why precious metals appear to be settling into a summer consolidation period, with gold trading near $4,500, silver holding within its recent range, and platinum and palladium also moving within broader trading bands. Jeff then turns the focus to copper, where CPM Group remains constructive on the long-term outlook but less aggressive than many other market forecasts. He discusses why copper demand tied to construction, electrification, vehicles, power grids, AI, and data centres needs to be analyzed with more nuance and less uncritical enthusiasm. While CPM expects the copper market to remain tight, with refined supply falling short of fabrication demand. Jeff also explains why some long-term copper price expectations may be too optimistic.

Click here to watch.

Crypto: Looking beyond the obvious

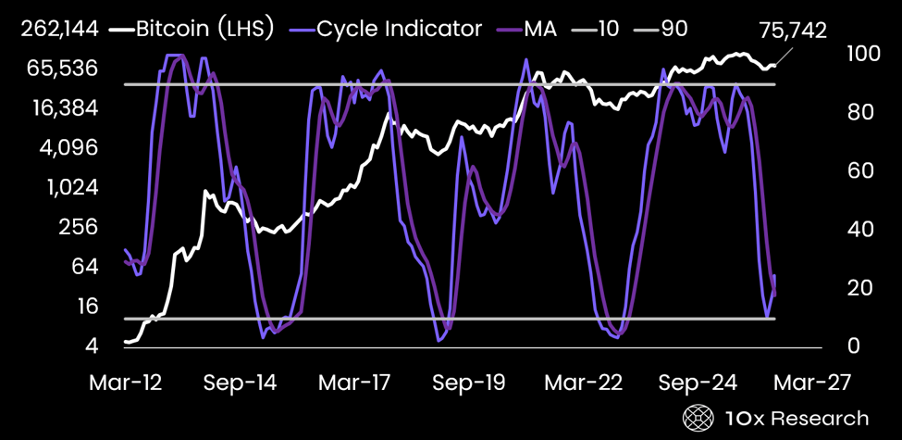

10x Research’s altcoin model portfolio is up 24% over the past seven weeks; their crypto equity picks have returned an average of +28% over the same period. Markus Thielen says that opportunity has not disappeared, but finding it requires a willingness to look beyond the obvious. His indicators continue to assign a 70% probability that Bitcoin has already bottomed out for this bear market. But the path from here is a grind, not a parabola. His short-term bearish view remains intact, even as he holds his medium- to longer-term bullish conviction. But the opportunity set is shifting, increasingly away from Ethereum, and potentially away from Bitcoin as well. This is visible in his Trading Signals model portfolio, which holds 10 equal-weight high-conviction crypto assets. Bitcoin and Ethereum are included by mandate, yet since the portfolio's launch in April, the +23.8% return has been driven almost entirely by the rest of the book, notably HYPE, ZEC, and NEAR, but also BNB, TRX, and XMR.

A critical materials reset

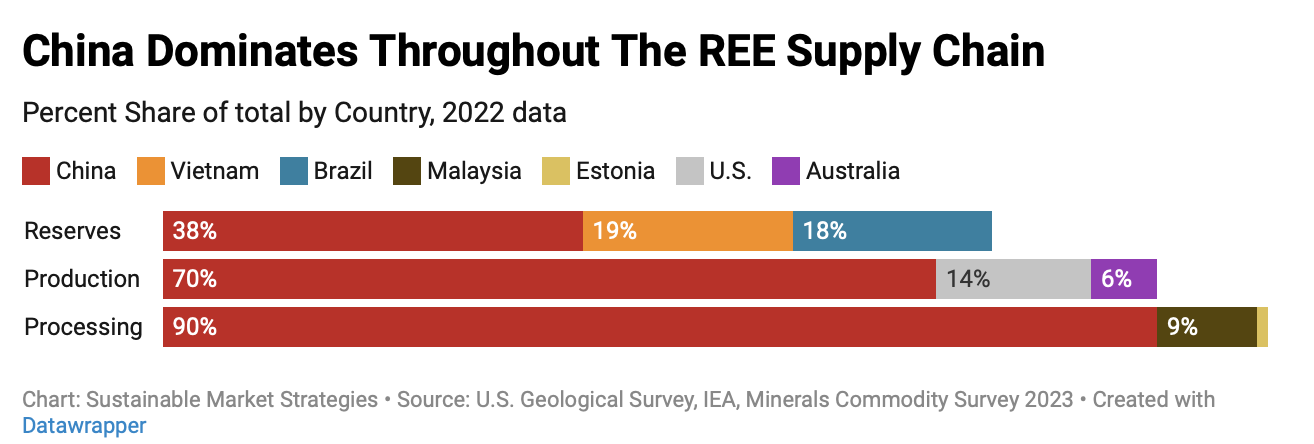

The demand story for transition materials has bifurcated: copper's case has strengthened, bolstered by a new AI infrastructure layer on top of persistent electrification demand, while nickel and cobalt face structural headwinds from the shift to new battery chemistry. Today, the bullish transition material thesis is just as much about major supply constraints as it is about structural demand. China's export control regime is a permanent feature rather than a trade negotiating tactic, and the processing bottleneck it exploits cannot be resolved through capital alone on any realistic investment timeline. The country processes 80-90% of the world's rare earth elements (see chart). Within the Sustainable Market Strategies universe, pure-play copper miners and recyclers remain their highest-conviction position. Among rare earth elements (REE) producers, the team add three new promising names to their coverage: Perpetua Resources Corp, 5N Plus Inc and Energy Fuels Inc.

Uranium: Feeling hot

The Global X Uranium ETF (URA US, USD48.96) has been ranging net sideways since peaking at USD60.51 last Oct. The ETF fell as much as 34% from the high. A new classic chart pattern appears to be forming, a 7-month Ascending Triangle. A breakout would target USD90.00 – Chris Roberts will add to his initial long if such a breakout occurs. He remains bullish on Uranium and has established an initial position this week. Go 30% long at market. The initial stop loss is a daily close below USD39.15.