What if copper reaches $7/lb?

Report by Global Mining Research

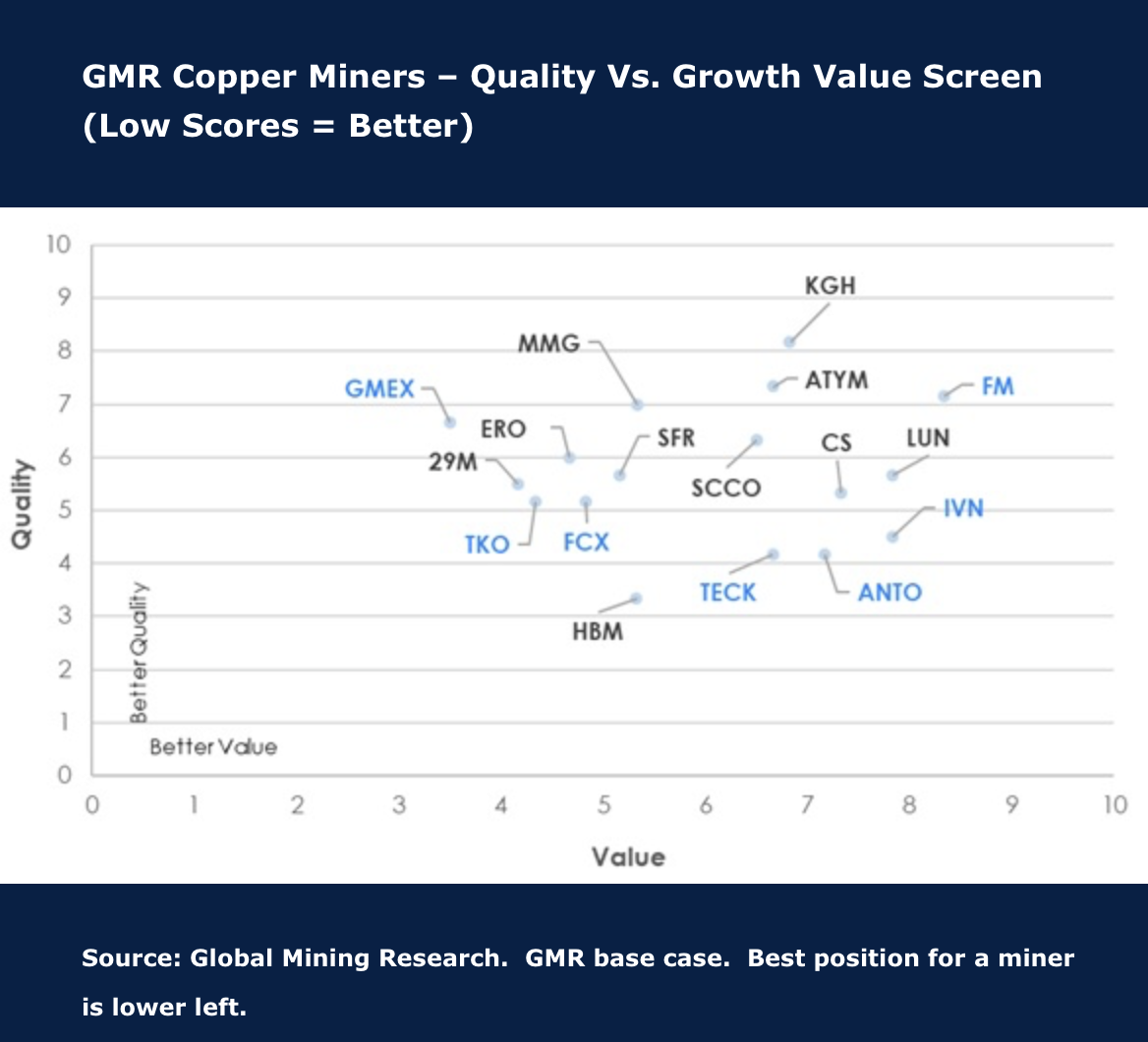

With the metal starting 2026 with strong price momentum, David Radclyffe’s team examines the “what if” upside for the nine senior copper pure plays. In the year ahead, David estimates a 410kt copper deficit, as Grasberg and other issues feed through, and that is before production guidance downgrades are announced for some. The copper market is tight. Best leverage to higher copper prices is with First Quantum Minerals Ltd and Teck Resources Ltd, showing high EPS upside near term and with long-term upside to NPV assuming copper stays at US$7/lb indefinitely. Least upside is with Grupo México S.A.B. de C.V. and Ivanhoe Mines Ltd, albeit still good. GMR’s quality vs value screen highlights Grupo México S.A.B. de C.V. and Freeport-McMoRan Inc. as offering better value, although not with the best leverage. The chief risk is the obvious one, that copper is near-term overbought with long-term prices expected lower.