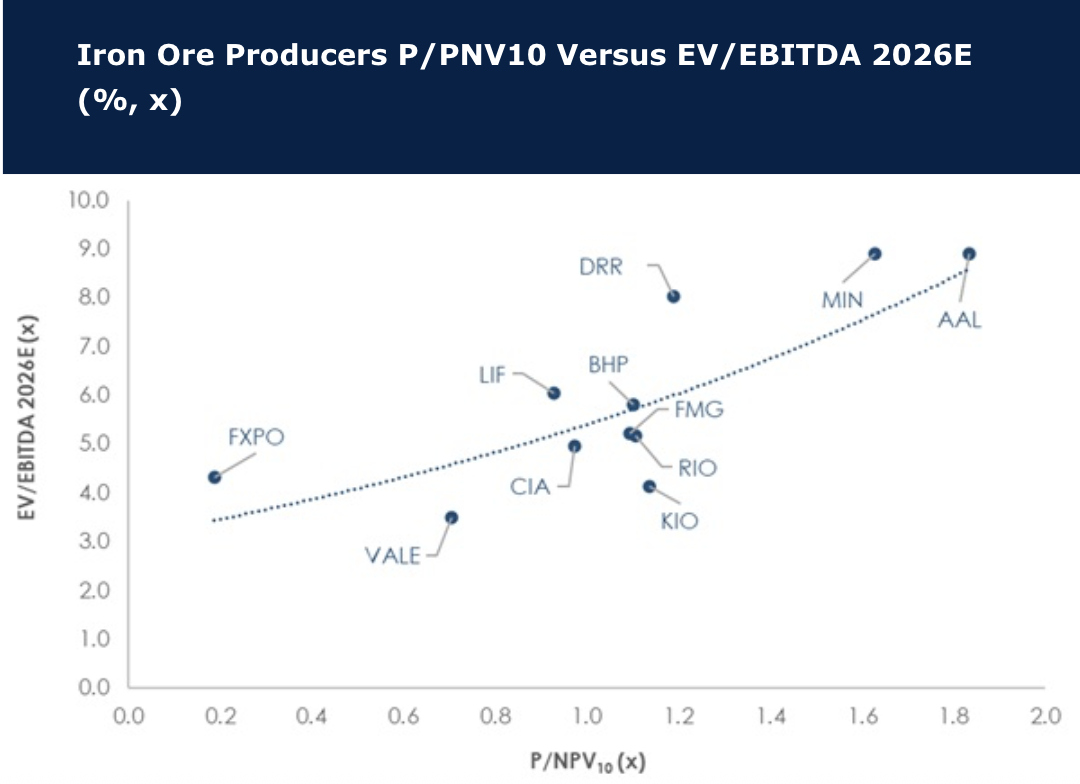

Iron ore is too big to ignore, but headwinds prevail

Iron ore seaborne supply is increasing at a time when steel demand is ailing, and David Radclyffe points out that this rightly makes investors nervous. However, the spot iron ore price has proven to be quite resilient this year at ~US$100/t. The headwinds may have dissuaded some investors, but at $378bn the iron ore market is simply too big to ignore in mining. As demand rolls the cost curve is key to sustaining volumes, and David assesses the LT price at US$95/t (US$101/t). Iron ore pure plays and diversified miners trade at 1.1x P/NPV10, and a prospective next two years average EV/EBITDA of ~5.8x and dividend yield of ~4.4%. Relative to other sectors this is reasonable, but high compared to historic levels. In the diversified iron ore-rich miners David prefers buy-rated BHP, then Vale, while in the pure plays it is Labrador Iron Ore Royalty. Overall, he remains underweight iron ore, with sells on key pure plays. Herein, Champion Iron is upgraded from sell to hold.

Iron ore: Falling prices pausing, or the cycle restarting?

Iron ore prices recently bounced off US$100/t, raising the question whether this represents a pause in the correction, or perhaps early signals that the price cycle is restarting. Sentiment continues to focus on broad demand risks especially in China, nevertheless Chinese crude steel production continues to annualise at +1Bt/yr, with the rest of the world’s demand recovering. David Radclyffe believes investors are getting close to an opportunity to start accumulating iron ore stocks; iron ore producers trade on a prospective 2023 FCF and dividend yield of 9% and 8% respectively. David’s preferred exposures are Vale, Fortescue Metals Group

and Labrador Iron Ore.

Materials

In GMR's view DRR remains well over-priced, although it is easy to see some positive features that have made it a “darling” of the Australian investment community (linkage to production growth is good and as a pure royalty play it has lower risk than regular miners). However, LIF trades 30-50% cheaper (depending on the metric used), has a much higher FCF and dividend yield, and sells a higher quality product. Even looking forward to 2026, when DRR has achieved its growth potential, leaves LIF a better investment proposition.