Europe: Uncontrollable hiccups

Niall Ferguson expects euro area headline inflation, measured by the harmonised index of consumer prices, to peak near 3.5% in late 2026 or early 2027 and to return to 2% in 2H2027. This is a higher peak than consensus and a longer return to target than in the European Central Bank’s adverse scenario. The return to 2% inflation was never sustainable. Imported disinflation from Chinese manufactured goods had been masking broad but shallow inflation in domestic services, and the current shock now arrives with no disinflationary buffer. Accordingly, Niall expects the ECB to hike rates by 50 bps by year-end. His views on US and EU rates and inflation translate to a minimally stronger euro than the market is pricing; Niall sees the EURUSD spot price at 1.178 and the one-year forward at 1.193. Europe’s second inflation shock in four years will prove less acute than the first but harder to shake.

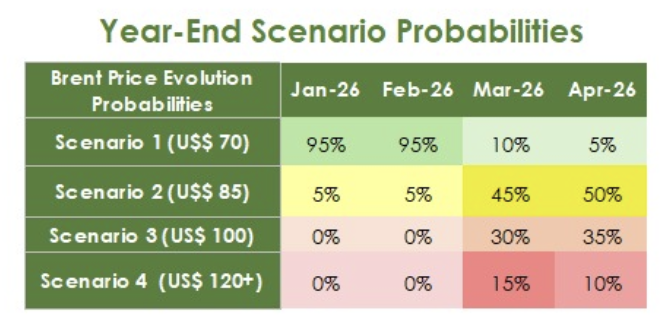

Oil: Predictions for year-end

Brent climbs higher, reflecting the ongoing stalemate between the US and Iran and, above all, the lack of concrete progress in negotiations. The cancellation of the trip of US envoys to Islamabad reinforced the perception that, despite the formal maintenance of the ceasefire, the diplomatic channel remains stalled. At the same time, signs of greater pragmatism from Iran are beginning to emerge, with the possibility of a provisional agreement involving the reopening of the Strait of Hormuz in exchange for partial relief of restrictions imposed on Iranian ports. Even so, US resistance to easing the blockade and regional pressure, especially with the continuation of attacks in Lebanon, keep the geopolitical environment quite fragile. The DayByDay team assign a 50% probability to Brent being priced at $85 by year-end, and 35% that it’ll stay around $100. They see only a 10% chance of prices staying above $120.

Copper: Lack of supply growth vs rising inventories

David Radclyffe's copper coverage totals ~63% of global mine production. Copper supply continues to wrestle with many legacy headaches from 2025, mixed with the Iran conflict and its implications for diesel and sulphuric acid supply. There is therefore downside supply risk. However, the current oil disruption has implications for global growth and copper demand. Worryingly, David points out that copper inventories are rising rapidly. His coverage universe implies 0.9% annual contraction in refined copper supply in 2026, following a strong 2025. Weak supply growth for 2026, even with moderate demand growth, is at odds with strongly rising terminal market inventories, now at 1,267kt, adding to price risk. Copper is a crowded long trade, with caution warranted. The sector is not particularly cheap at spot 1.6x P/NPV10 and 9x EV/EBITDA. Antofagasta PLC is cut to HOLD. Preferred stocks include Lundin Mining Corp, KGHM Polska Miedz SA, Ivanhoe Mines Ltd, Grupo Mexico SAB de CV, Hudbay Minerals Inc and Teck Resources Ltd.

US: Going overweight on tech

The Vermilion team remain bullish on the S&P 500 (SPX), Nasdaq 100 (QQQ), and Russell 2000 (IWM). Market dynamics continue to improve ever since the major bullish false breakdowns at 6480-6520 on the SPX, 24,000 on Nasdaq futures (NQ), and $245 on the IWM, with all of them now breaking out to all-time highs and holding above bullish gaps from April 17. Everything that the team sees suggests bulls remain firmly in control, so the team want to be buying any pullbacks for the foreseeable future to the 20-day MA or 21-day EMA. The team discussed adding exposure to growth, and primarily technology, as growth has taken over as leadership relative to value. RS on the cap-weighted XLK is now breaking above its 2025 highs and they are upgrading Technology to overweight. The team have remained overweight semiconductors (SMH, NVIDIA Corp, Taiwan Semiconductor Manufacturing Co Ltd, Ciena Corp, etc.) and memory (SanDisk Corp, Western Digital Corp, Seagate Technology Holdings PLC, Micron Technology Inc) ever since last June, and these remain their favourite areas within Tech.

Thailand gets even weirder

Stagnant, stagnant, stagnant. Thailand remains completely depressed at home, with no sign of buoyancy in any of the domestic indicators that Jonathan Anderson covers. Trade is exploding ... but it's all "throughput". By contrast, the Thai trade numbers are shooting up dramatically - but just as Jonathan has highlighted for the rest of East Asia, this is (i) all concentrated in IT/electronics goods headed for developed AI investment, and (ii) it's also all "round-tripping", with an explosion of imports from China matched by an explosion of exports to the US and to a lesser extent Europe. As a result, there's surprisingly little impact on the local economy. In the meantime, he doesn’t see much to do in Thai assets. There's not a lot of earnings growth in the equity market, and local yield and carry are extremely low. Basically, Jonathan is waiting for the country to start spending again.

Argentina: Make hay while the sun shines

Marcos Buscaglia comments on a challenging year of debt services ahead for the government and central bank. Even if debt with the IMF and other multilaterals is rolled over, the debt maturing next year is very high with total hard currency debt services nearing $36bn, of which $18bn pertain to bonded debt. The government already squandered an opportunity to tap markets at the beginning of the year, when the risk appetite for Emerging Markets debt was high. Marcos believes the government is reluctant to issue market debt because of the inevitable rise in interest bills, but he finds that this is both inevitable and not worrisome in the short term. He believes the market is more than willing to take on new Argentine debt, with 10-year rates possibly dropping to low 9s. The government should take advantage.

USD / Singapore Dollar

Chris Roberts examines the Singapore Dollar (SGD), which appreciated against the USD from the end of 2001 until the summer of 2011. The USD fell 35% during that time. Following a modest retracement of losses in 2011-2017, the USD was rangebound for 8.5-years. Towards the end of that period, the USD failed to reach the top of the range and in recent months it has broken down again. The breakdown from the rectangle targets a fall to USD/SGD1.1625. Note that the MACD is below the Zero Line again, reflecting negative USD momentum. Go 200% short at market. The stop is a daily close above USD/SGD1.3228.

US: The Fed’s struggle for financial mastery

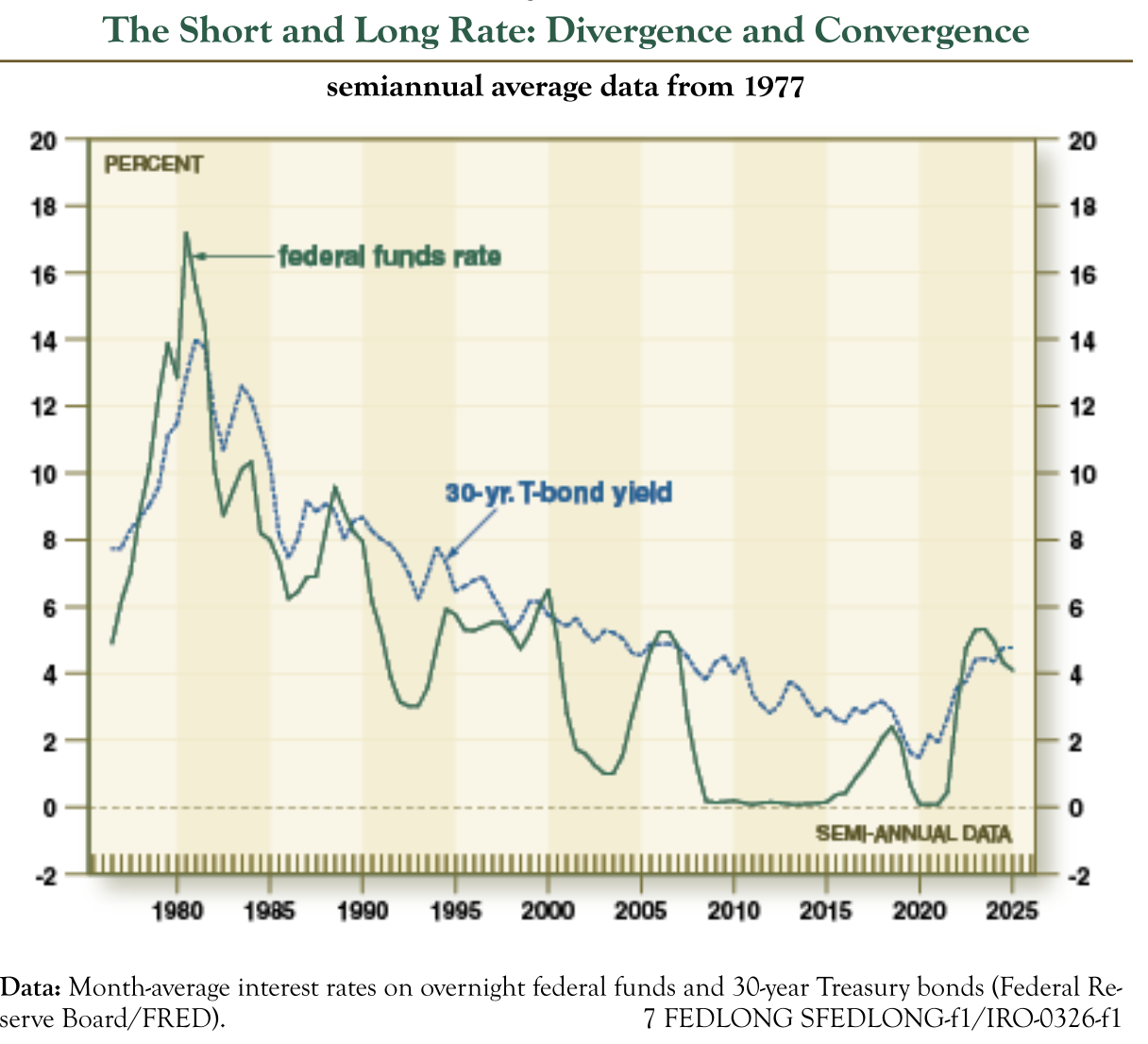

Past research by David Ranson suggests that long rates show very little response to Fed policy. Even after the most vigorous attempts to impose the Fed’s policy rate on the term structure, the short rate tends to converge toward the long end of the curve. This is compatible with evidence that during the past 25 years, the measured influence of changes in the 30-year T-bond yield on real growth and inflation has exceeded that of the Fed’s policy rate (see chart). The chart shows how sudden divergences between the two ends of the yield occur occasionally, in every case crated by a rate cut at the short end. The slope of the yield curve remains steep for a few years until re-convergence begins, which is attributable to a reversal in Fed policy and not a response of the long rate to the Fed’s cutting. On average, complete reversal takes four years. Rates are governed by market forces, not monetary policy.

US: Warsh ready for prime time at the Fed

Based in part on his previous interactions with Kevin Warsh, the prospective next Fed Chairman, John Ryding discusses what he is likely to do when he takes over on 15th May. John says that Kevin understands complex economic arguments but is not wedded to conventional academic wisdom. Kevin hates inflation and firmly believes that it is a monetary phenomenon and that the Fed must take responsibility for it. Although Kevin feared at one point that the Fed might raise its inflation target to 3%, he seemed adamantly opposed to the idea. Kevin brings a great depth of institutional market knowledge to the Fed, which it desperately needs, and is willing to think outside the box. In his prepared statement to the Senate Banking Committee, Kevin made it clear that he believes “monetary policy independence is essential. Monetary policymakers must act in the nation’s interest . . . their decisions the product of analytic rigour, meaningful deliberation, and unclouded decision-making.”

Stagflation not spikeflation

Andrew Hunt points out how the 2026 oil shock is now analogous in duration and (almost) severity to the shock in 1973. This is the third or fourth global price shock in six years - people are learning and inflation expectations are no longer anchored. Weak government credibility and a loss of faith in central banks will play a big part. The fact the US and (to a degree) Chinese central banks are accommodating the oil shock via money creation will further encourage inflation expectations. Elsewhere, other central banks appear to be prevaricating over reactions. The clamour for fiscal measures to help people afford oil they may not physically be able to buy will feed inflation, just as it did during the pandemic when aggregate demand was supported even when supply was compromised. We are on course for a second surge in inflation, and Andrew also expects a global recession – or at least near recession – from the middle of this year.

Financials

Anas Abuzaakouk (CEO since Aug 2017, joined 2012) bought 30,000 shares at €149, spending €4.5m. He has a great track record based on his 21 prior purchases. This is his single largest purchase and the highest price he has paid. He last bought in Oct 2025 at €108. Smart Insider has ranked the stock several times based on his prior activity, with the majority of those signals proving to be very timely. They are ranking the stock +1 (highest rating).

Materials

The closure of the Strait of Hormuz is driving dislocation in ammonia and sulphur markets. AECI is well positioned, sourcing ~85% of ammonia from Sasol’s Secunda plant and avoiding import exposure, while ~50% of global sulphur trade typically transits the Strait. Resulting shortages have triggered sharp price spikes, with AECI monetising existing inventory. Its sulphuric acid business (~R600m revenue, HSD margins) should see a near-term earnings boost (for approx. a quarter based on current conditions). Operations have also improved following stabilisation at Modderfontein. With peer Omnia sourcing ~50% of its ammonia requirements from imports, AECI is better positioned. Chronux expects EBITDA to reach ~R4.5bn by FY27 and increases their HEPS by 10.7% (FY26) and 3.8% (FY27). TP increased to R132 (from R125).

Industrials

Robert Crimes highlights GET as a unique long-duration infrastructure asset with a potential takeout emerging. Eiffage and Mundys will likely soon own ~59.8% of the company, having recently added to their positions. Insight’s buyout scenario IRR is 14.7% (at 25% share price premium of €24/share), +410bps above their deal Ke of 10.6%. While shuttle traffic remains pressured by excess ferry capacity, this has been offset by higher pricing, supporting continued revenue growth. The underlying appeal is the asset’s durable cash generation, with ~€710m recurring FCF (~6.9% yield) and long-term growth driven by pricing, traffic recovery and new high-speed rail routes.

Innolight: AI optics leader targets H-Share listing

Technology

Aequitas offers an early look at Innolight as it aims to raise ~$5bn in an H-share listing (up from ~$3bn in late 2025), potentially making it one of Hong Kong’s largest deals this year. The company is the global leader in optical transceivers and is benefiting from strong demand driven by AI-related data centre capex. Growth has been exceptional, with revenue up 122% in 2024, 61% in 2025 and a further 192% YoY in 1Q26, alongside margin expansion. With revenue heavily concentrated among hyperscalers and shares already trading at elevated multiples (~37x FY26 P/E), the key question for investors is how much of this growth is already priced in.

Technology

The group’s year-end update more than confirmed the optimism management showed at the interims. Revenues will be ahead of consensus, with double digit growth and record backlogs. Confidence is also evident in a 21% increase in headcount, albeit with some margin pressure from contractor usage. Consensus revenue forecasts have been upgraded, though EBIT has edged slightly lower. The balance sheet remains a clear strength with £160m of net cash and potential for ~£70m of Y2 FCF. While analysts appear to be recognising the revenue inflection, the implied to Y3 EBITM ratio here is now 40. That is very low for the growth on offer, with Willis Welby arguing the shares could easily rise 50% from current levels.

Industrials

Hamed Khorsand highlights Azul as a post-restructuring opportunity following its emergence from Chapter 11 bankruptcy, which materially reset its capital structure and reduced net leverage to ~2.3x EBITDA. The company eliminated ~$2.5bn of debt and lease obligations, cut interest costs by >50% and is now positioned to generate sustainable FCF. Despite this, the stock trades at ~3.9x 2026 EV/EBITDA, a significant discount to regional peers. The key catalyst is a planned NYSE listing, which should broaden investor awareness and drive a rerating. With a differentiated domestic network and improving profitability, Hamed sees ~70% upside to his (12-month) TP of R$50.

Industrials

Misumi appears to be at the early stages of a meaningful re-rating, as it begins to demonstrate the success of its transition from a domestic parts catalogue company to a global digital manufacturing platform provider. Over recent years, this previously highly regarded “growth” name has derated from trading at 25-40x to 15-20x, but has quietly transformed itself and now boasts a unique combination of software, hardware and logistics, which should support a re-acceleration in earnings. At the same time, there is increasing scope for enhanced shareholder returns as management optimises its cash-rich balance sheet.

Technology

The market is misdiagnosing structural share loss as a temporary slowdown. OWS’s industry checks suggest enterprise weakness is driven by competition from Microsoft Teams and Zoom, while a lack of innovation is reflected in Gartner’s Magic Quadrant rankings. Management’s expectations for high growth from AI and RingCX products appear optimistic, with feedback indicating these offerings are largely undifferentiated. At the same time, aggressive cost cuts in R&D and sales are cited as contributing to customer dissatisfaction and weaker retention. With RPOs (backlog) flat for nearly two years and FCF overstated (adjusting for buybacks reduces 2025 FCF to $196m from $530m and the FCF yield was 5.6% rather than the 15% bulls use to argue that RNG is a cheap stock), OWS sees continued pressure on growth and valuation.

Technology

JNK’s analysis suggests LSCC is tracking ahead of guidance, with Q1 supported by strong bookings extending into 1H27 and a book-to-bill above 1.2. However, this strength is partly driven by Greater China customers pulling forward demand ahead of a ~15% price increase implemented in March 2026, with regional shipments running ~25% above Q4 levels. Lead times remain elevated at over 26 weeks, constrained by substrate and packaging rather than wafer capacity. With servers accounting for ~60% of revenue and exposure to Intel and AMD platforms, the company also benefits indirectly from AI-related demand. JNK's analysis suggests pricing can support growth even if volumes soften.

Materials

GMR cuts FCX to Sell following further production downgrades at Grasberg, with the ongoing impact of the 2025 “Mud Rush” now expected to persist through 2027. They estimate cumulative production losses of 952kt of copper, 1.5Moz of gold and 6.6Moz silver over 2025-2029, equating to $19.2bn of lost revenue at spot prices (or $15.4bn on GMR’s base case price forecasts). GMR has cut 2026/27 EBITDA forecasts by 15-21% and reduced its valuation by 27%, arguing the recent share price reaction underestimates the severity and duration of the impact. With risks of further downgrades and rising capex, downside remains.

Consumer Discretionary

Paragon’s executive diligence memo was originally published when Heidi O’Neill was being discussed as a potential CEO successor at Nike and they viewed her as a poor fit for that role. At LULU, she is somewhat better matched to the brief, but their core reservations remain. She has tended to look stronger as an operator and internal brand steward than as a true strategic architect. That matters at LULU, where the challenge requires a sharper product vision, stronger innovation instincts and a willingness to make harder calls on strategy and talent. So, while the fit is better than it would have been at NKE, Paragon still views her as more of a stabiliser than an obvious answer to LULU’s deeper issues.

Communications

The competitive landscape is intensifying and the existential risk for IRDM is getting bigger, according to Hamed Khorsand. The direct-to-device market is attracting well-capitalised entrants, with Amazon’s acquisition of Globalstar and Starlink’s expansion significantly increasing capacity and bandwidth relative to IRDM’s legacy network. At the same time, a proposed FCC rule could erode the exclusivity of IRDM’s spectrum, undermining a key pillar of its valuation. Customer behaviour is also shifting, with evidence of dual-sourcing and pricing pressure. While positive FCF has supported the equity story, Hamed expects rising investment needs to weigh on future generation. The recent advance in IRDM's stock makes it a good place to short/sell shares.

Why Wall Street gets gold and silver wrong

In the final segment of the Silver Facts and Fantasies series, Jeffrey Christian of CPM Group discusses how investors should interpret gold and silver price forecasts, and why large shifts in bank price targets are often misunderstood. He explains how many institutions adjust their projections based on changes in current price levels rather than shifts in market conditions, which can lead to seemingly dramatic revisions. The presentation concludes with a discussion on portfolio construction, including how investors can think about allocating between physical metal and mining equities. Jeff explains how mining stocks behave differently from physical metals, sometimes lagging and at other times outperforming, depending on market conditions.

Click here to watch.

Pulp market gainers and losers

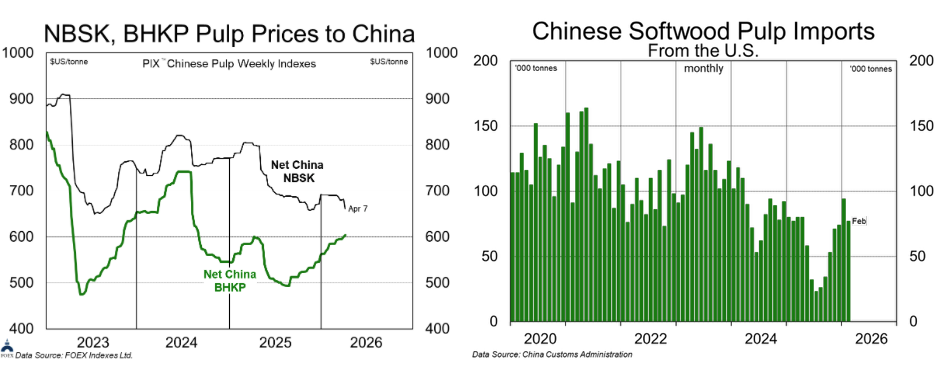

NBSK prices have been lingering at unprofitable levels for over a year now, far longer than thought possible. Current price levels are unsustainable for many mills: Back in December, Suzano indicated they believed ~35% of global BSK production was “loss-making” at $670 in China. Now, with rising fibre, energy and freight costs, that proportion is likely even higher. NBSK producers are under the greatest pressure, with more capacity closures likely and needed. With the January sale of IP’s fluff assets to GFC, there are no large, publicly traded fluff producers. Domtar and GFC cash flows should benefit from fluff price increases (as will smaller producer RYAM). If fluff/SBSK prices rise in line with announcements, it would also be supportive for NBSK producers, including MERC. Despite rising hardwood and fluff pulp markets, the team remain cautious on all pulp names. Without larger global NBSK industry supply reductions, prices will have little near-term upside and will lag any fluff pulp pricing gains.

Copper: Moving away from a 19-year ceiling

Spot Copper (USD5.87) is finally moving away from a 19-year Ceiling that extends from USS4.00-5.00. The minimum long-term target is USD8.00-10.00. A multi-year ceiling is rarely broken easily but copper has been fighting for 4.5 years, and Chris Roberts comments that after a number of attempts it looks to have succeeded. The encouraging development since the 2022 low has been the series of higher lows. If Chris’s view is correct, going forward investors should expect a cleaner trending market with less volatility. The weekly chart features a 4-year Ascending Triangle, which is viewed as the launching pattern for the move away from the 19-year Ceiling at USD4.00-5.00 to USD8.00-10.00+. Go 20% long at market. Add 10% at USD5.8220, 10% at 5.7720 and 10% at 5.7220. The recommended stop is a daily close below USD5.2170.

Mexico: Caught between SLAMLO and a productivity problem

Caught between macro inefficiencies caused by the dominance of oligopolies (typified by the sprawling empire of Carlos Slim) and the poor allocation of fiscal policies of the AMLO administration, Mexico’s growth suffered in that 'SLAMLO' regime. Sheinbaum’s austerity promised a new future of 2% growth and 2% primary surpluses. The Sheinbaum administration is now caught between a return to the SLAMLO regime if its policy intervention doesn’t work and the need to address the productivity downturn. Manoj Pradhan asks: can the new policy easing restore the promise of a fundamental alpha, or will it put both the growth and fiscal legs at risk? Partly due to weakness and in part due to risk premia, MBonos provide value given the fundamental backdrop, which Manoj explores in his latest report.

Mexico’s domestic economy starts to pick up

Mexican exports continued to hold up well despite all the uncertainties around tariff policies and the USMCA, as well as the volatility in US auto import spending. So far so good. And now the economy is picking up at home, with better consumption and earnings numbers in the most recent data. It's still early days, and private borrowing and lending activity remains weak, but Jonathan Anderson will be watching closely for a broader-based recovery ahead. He doesn’t worry about balance sheet risks in Mexico; the external balance is solid, debt levels are moderate and inflation continues to fall. The main two variables to watch are (i) the worsening budget position and (ii) what still appears to be a somewhat expensive peso. If Mexico hits further volatility ahead, it's likely to come from one of these two sources.

China: Beijing meets with Taiwan’s opposition party

Mainland China’s government has pledged a package of policy deliverables aimed at improving cross-strait relations, following a visit to Beijing by the leader of the KMT, Taiwan’s main opposition party. After the visit, the mainland’s Taiwan Affairs Office announced a ten-point list of measures to promote cross-strait engagement. The measures include loosening restrictions on mainland residents travelling to Taiwan; restoring passenger flights from five large mainland cities; improved infrastructure links between Fujian province and the Taiwan-controlled Kinmen islands; and easier access for exports of Taiwanese agriculture and fishery products to the mainland. The PRC’s 10-point pledge lacks any timeline for implementation. Gabriel Wildau notes that Beijing may delay some or all of the measures pending KMT gains in local elections, or even until after a potential KMT presidential victory in 2028, thereby reinforcing the message that benefits to Taiwan are linked to the KMT’s electoral success.

Iran conflict: A buying opportunity?

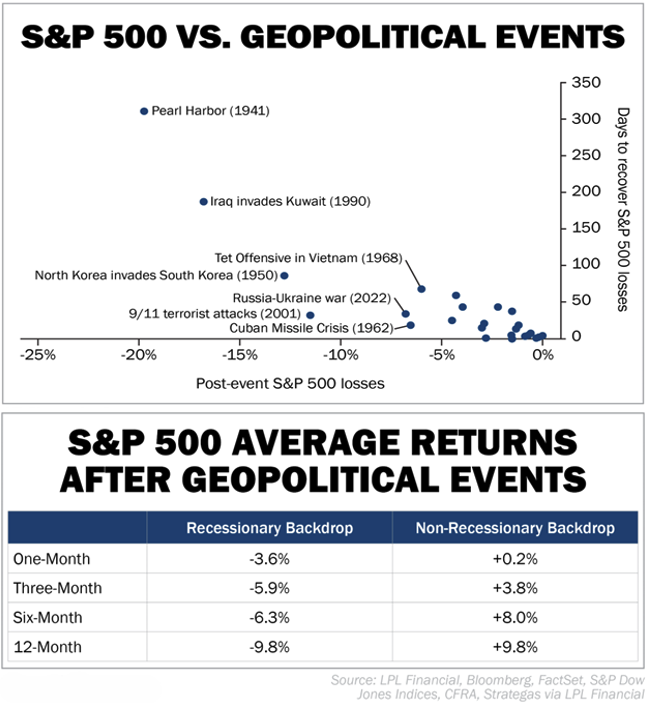

With no clear end to the Iran conflict in sight, investors are preparing for the worst. A look into history reveals that’s probably not necessary, according to Joel Litman and Rob Spivey. While markets typically wobble on geopolitical shocks, they rarely break. The chart shows how stocks have reacted to more than two dozen major geopolitical events since WW2. The S&P 500 Index's average decline during these events is about 4.5%. Markets typically bottom in roughly 18 days and recover fully in less than 39 days. Put simply, these events tend to create more fear than lasting fundamental damage. The recovery tends to arrive faster than investors expect. That's especially true when looking at geopolitical events that occurred nowhere near a recession. After events that happen near a recession, the S&P has averaged negative returns within one, three, six, and 12 months. In non-recessionary backdrops, returns have been positive for all of those time spans.

ECB is stuck

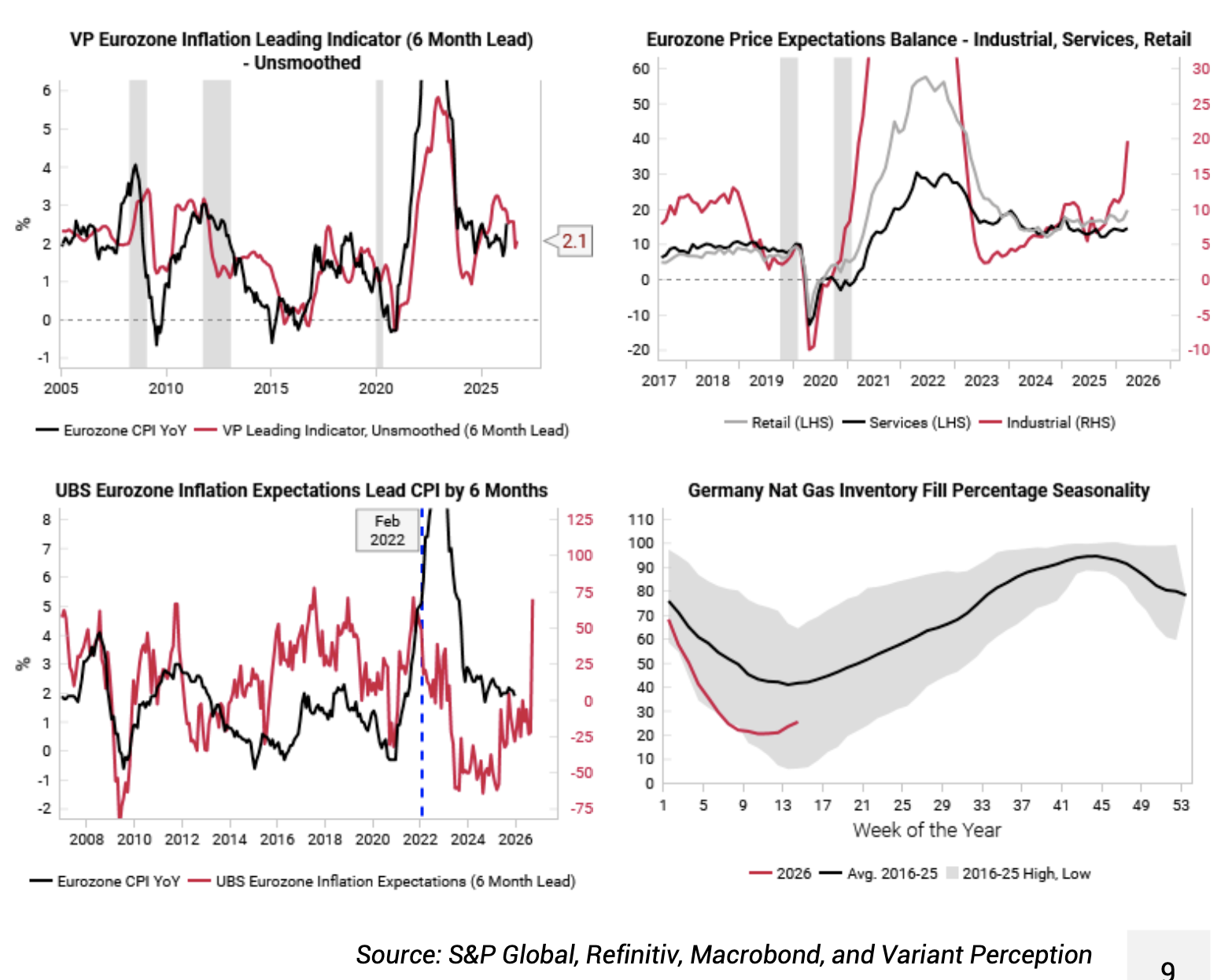

Variant Perception’s inflation leading indicator (top left chart) ticked higher this month, but there has been a much more pronounced move higher in eurozone price expectation surveys (top right and bottom left). As the team previously noted, the energy shock could not be coming at a worse time for the eurozone after a harsh 2025 winter already depleted natural gas inventories (bottom right chart). The ECB is risking a 2011-style policy error, hiking policy rates into a genuine growth slowdown. The ECB pivoted more hawkish at the March meeting, keen to avoid making the mistakes of 2022 when they were too slow to hike. There is a real danger that today's ECB is fighting the last war on stagflation, with the eurozone economy now more vulnerable to a growth slowdown. Receiving EUR 1y1y is a clean way to express this view, with the ECB likely to be forced into more rate cuts later.

Hungary: Orban’s fall

Katharina Klotz observes that even a heavily engineered electoral system could not save Hungarian Prime Minister Viktor Orbán. As a record share of voters turned out in yesterday’s parliamentary election, the conservative, anti-corruption, and moderately pro-European Tisza party achieved a landslide victory, securing more seats than Orbán ever achieved. Katharina expects Tisza leader Péter Magyar to take office within the next month. For the EU and Ukraine, this is very good news. She expects Magyar to lift Hungary’s veto on Brussels’ €90BN loan to Ukraine (90% probability) rapidly and play a more constructive role in EU policy from defence to China. With a supermajority in parliament, he will also be able to pass rule-of-law reforms required to unlock at least a high share of the €18BN of frozen EU funds (90% probability)—a crucial lifeline for Hungary’s struggling economy.

The best 3 space exploration stocks to buy in 2026

Technology

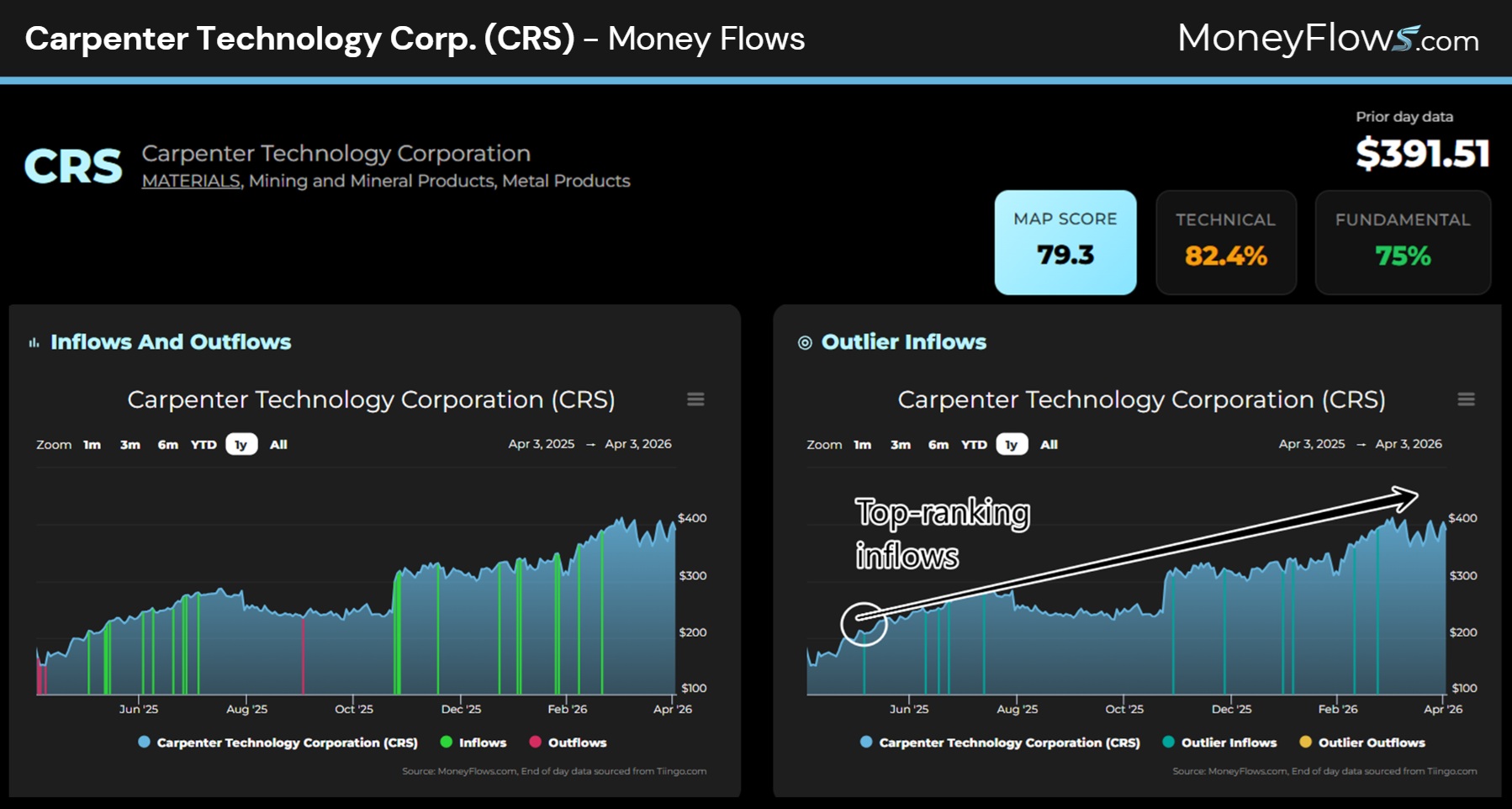

The space economy is a major structural growth theme, expected to expand from ~$614bn in 2024 to >$1.8tn over the next decade, with opportunities extending beyond rockets into the broader infrastructure stack. MAPsignals’ edge lies in identifying institutional inflows before the narrative becomes consensus, using its “Big Money” framework to find winners early. For example, Teradyne was flagged at ~$90 last June and has since surged to ~$342 on sustained inflows, with further upside anticipated. Applying the same process, they also highlight Carpenter Technology and Palantir as beneficiaries of the space buildout, supported by persistent institutional buying - including “non-stop” inflows into Carpenter. Tomorrow’s leaders are found by following the flows, not the headlines.

Energy stocks structurally mispriced

Energy

Energy stocks sit at the intersection of extreme under ownership, sector-leading FCF generation, a decade of starved capital investment and a valuation spread that has historically been a precursor to massive outperformance. Since KCR's first bullish publication in Mar 20, energy has returned ~500%, trouncing tech's ~300% and crushing the S&P 500's ~210% - and that outperformance has repeated across multiple entry points spanning wildly different market regimes. The bull case doesn't need a crisis as every data point in KCR’s analysis uses realised company financials when WTI averaged <$65. Contact us to see how energy companies are currently weighted across KCR’s various model portfolios as well as their highest ranked stocks.

Consumer Discretionary

Tapestry has been on a roll, driven by Coach’s use of technology, customer insight and strong design team, but momentum now appears past its peak “buzz”. While Kate Spade is beginning to show signs of life, The Retail Tracker would avoid the name at current levels - with the stock up ~135% over the past year and +16% YTD, it looks fully valued at ~22x earnings. Investors could instead own LVMH or Moncler at similar valuations, or Capri Holdings as a turnaround. For aspirational exposure, The RealReal and Lululemon are seen as more compelling.

Materials

GMR upgraded KGH to Buy, following the recent pullback, arguing the stock offers a cheaper, lower-risk way to gain silver exposure. KGH is a much larger silver producer than often appreciated, with silver contributing ~26% of 2026 revenues (rising to ~32% at higher prices), supported by stable production and assets in low-risk jurisdictions. GMR forecasts earnings to rise ~70% Y/Y, with a base case of $79/oz silver in 2026, falling to $52 and $47 thereafter. The stock trades on ~7.7x 2026 P/E and ~4.4x EV/EBITDA (vs. ~7-8x for peers), with ~6.3% FCF yield. Valuation becomes increasingly compelling above $60-70/oz silver. Additional support comes from net debt trending to zero by 2028 and declining royalty charges.

Industrials

The stock was pitched as a long idea at MYST’s latest Industrials Idea Forum, with prior events generating +11.4%, +10.4% and +9.5% average alpha. The presenter argued ENR’s recent underperformance vs. GE Vernova reflects macro-related fears among European investors, not fundamentals, leaving a valuation gap set to close. Multiple catalysts were highlighted, including “super cycles” in Gas Services and Grid Technologies and a profitability inflection in Siemens Gamesa expected in 3Q26. Street estimates are too low, with additional upside from potential changes to the Siemens AG trademark licensing fee and an end to the war in Ukraine. With strong backlog visibility and a clean balance sheet, the presenter has a TP of €225, offering 35% upside.

China: Game plan

Niall Ferguson’s takeaway from China’s response to the Third Gulf War and from the design of its new Five-Year Plan is that Beijing is focused on further supply-chain diversification and greater self-sufficiency. He remains sceptical that China can deliver the household consumption revival it seeks. What is clear, however, is that the leadership sees technological innovation as the only way out of China’s socio-economic challenges. The longer the Middle Eastern conflict goes on, the more likely it is to accelerate CNY-denominated trade. When the dust finally settles over Iran, the regional balance may well shift modestly toward China and its currency, at the expense of the United States and the dollar. Niall also believes that an escalation in the Middle East will fuel inflationary pressures, causing the PBoC to wait until 2Q/2026 to start cutting rates via both the reserve requirement ratio (RRR) and the loan prime rate (LPR).

Time’s up for just-in-time supply chains

When the US and Israel launched their initial strikes on February 28th, the market priced in a swift resolution. Here at Commodity Intelligence, James Burdass initiated a "30-Day Supply Chain Clock", representing the maximum structural buffer built into the modern, just-in-time global economy. This week, that clock officially struck zero. As the City lawyers are actively witnessing, the logistics have failed, and the contracts are now being torn up. James notes that for the last month, algorithms have traded the rhetoric of peace plans. But peace on paper does not put diesel in an Australian truck, it does not process Chilean copper, and it does not force a supplier to honour a contract when a force majeure has been legally triggered. As the 30-day threshold is crossed, the global market is violently bifurcating between those who own the physical molecules and those who only own the paper promises. Markets also now face the real prospect of accelerating inflation.

Iran: What lies ahead

Every time Trump pushes back the deadline for reaching an agreement with Iran, the credibility of his threat wanes and Brunello Rosa sees little reason as to why the Iranians would now feel compelled to give ground. There is a deeper issue: Iran does not trust Trump. The only strategy may be for Iran to impose enough pain by prolonging the conflict until the US and its allies feel the pain, which could send oil prices soaring toward $200/barrel. Brunello explores the scenarios that lie ahead should Washington target Kharg Island. One sees Tehran being toppled, but at an extraordinary cost of hundreds of thousands of troops and trillions of dollars. The second scenario is worse, one that involves a prolonged war of attrition mirroring that of Vietnam. Brunello sees the third possibility of the US achieving its objectives in a matter of months as unrealistic.

India: Monitoring for a potential short

The iShares MSCI India ETF (INDA US, USD45.82) has broken below the Mar 2025 low of USD47.60 trading down to USD45.71 last week. Last week’s decline completed an 18-month Descending Triangle, targeting a fall to USD38.00. RSI is at an Oversold 27 after peaking around/below High Neutral 60 for 15 months. If a weak rebound rally occurs, Chris Roberts will consider a short, but his base view is that the current global decline is a dislocation, so he would keep risk tight. Chris would only consider buying if one of the USD Indian ETFs formed an acceptable classic chart pattern buy setup.

Argentina: A once-in-a-generation opportunity

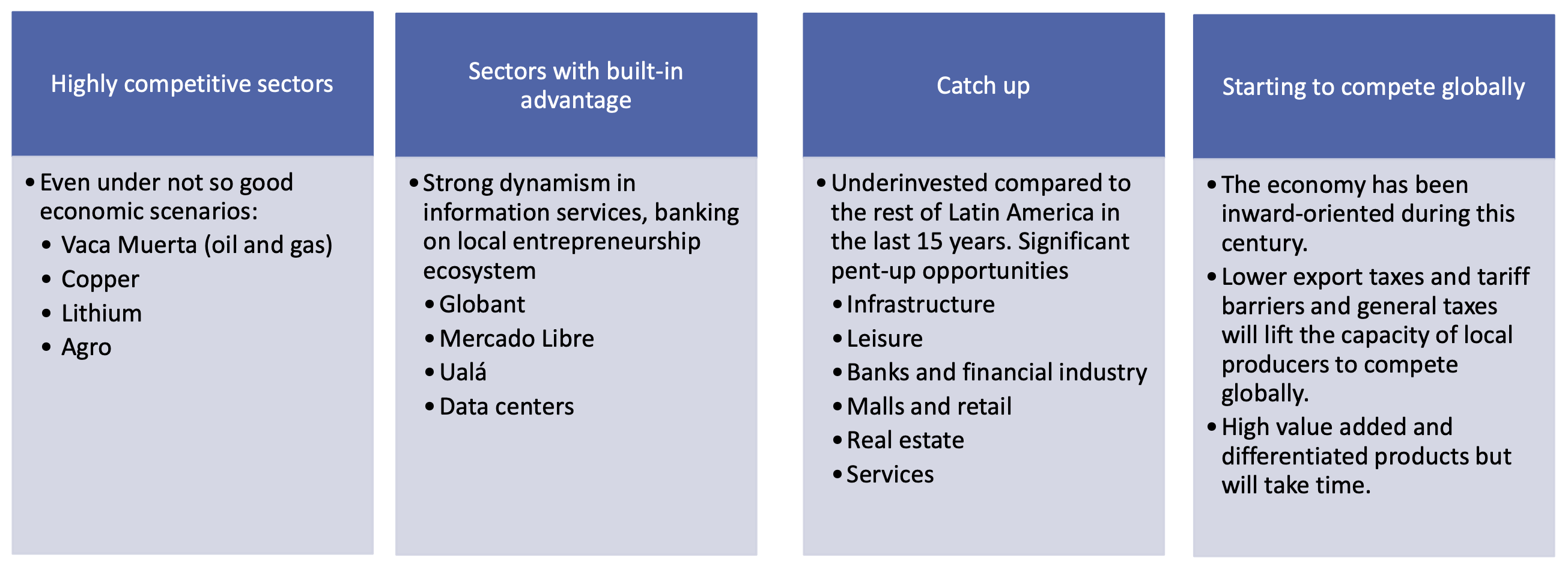

Marcos Buscaglia deep dives into Argentina and points out how the government is implementing two important transitions at once. First, a structural change in growth strategy from a protected economy to an export-oriented one and from regulation to deregulation. Second, the implementation of an inflation stabilisation effort. The last two years have seen an impressive set of reforms, although the labour market has deteriorated, the credit market remains slow and troublesome, and interest rates jumped into high and volatile territory. Marcos sees the economy remonetising with credit penetration rising, allowing the central bank to purchase reserves without a big sterilisation effort. He also sees investment rising, with high capex and soaring exports, particularly in energy, mining and agro. Opportunities lie in several sectors and themes, including copper, lithium, agro and information services (see chart).

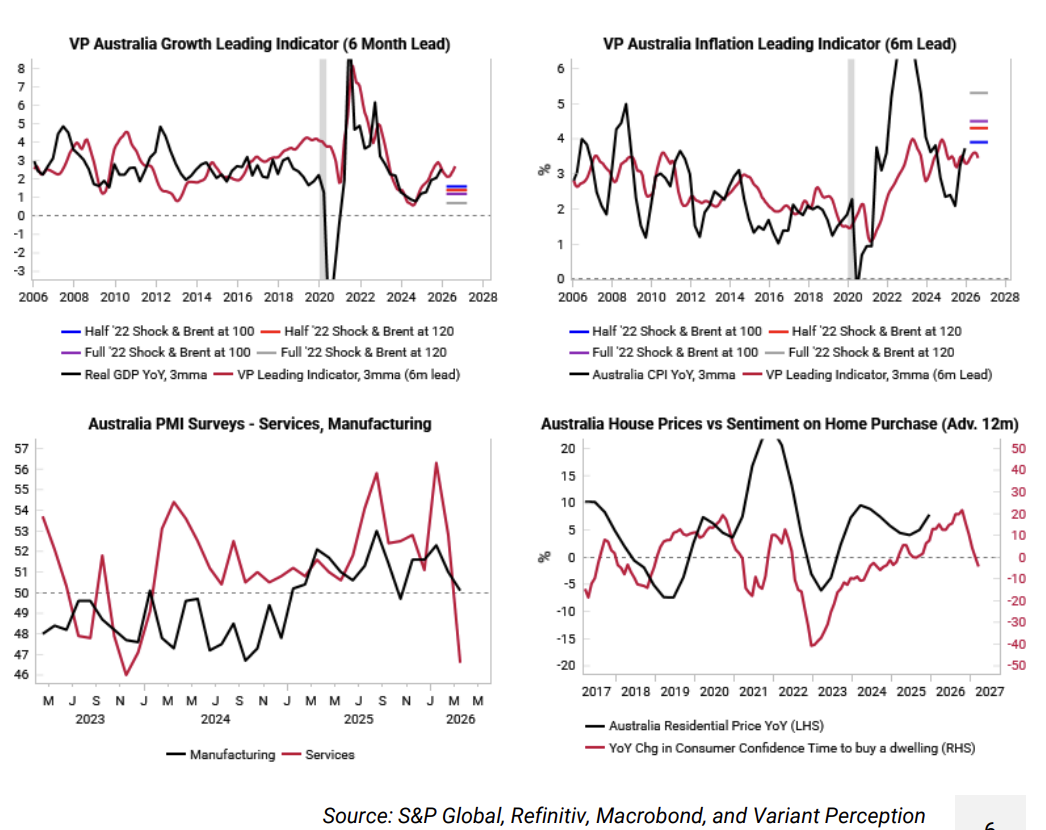

Australia: The lucky country

Variant Perception stress-tested countries to identify the ones most resilient to energy shocks, with Australia coming out on top thanks to its coal and LNG exports. The team’s range of scenarios show that inflation should remain below the 2022/23 highs. This outlook should reinforce the RBA’s ongoing hawkish stance; at face value, a hawkish RBA and positive terms of trade shift would point to a stronger AUD, but there are signs that a bigger downside growth shock is possible. Both services and manufacturing PMIs were already rolling over before the Iran conflict, which should give the RBA reason for pause, and housing sentiment is weaker today than 3 years ago. Long AUD has been a popular trade that has worked well YTD, but it is going through a correction now given elevated long speculative positioning and a previous LPPL sell signal. The team are waiting for their tactical models to signal a better time to go long the AUD again.

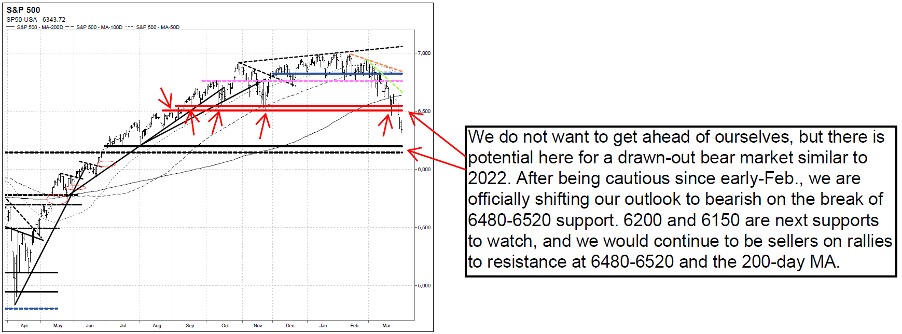

US: Down to bearish

The Vermilion team are officially downgrading their outlook to bearish with the S&P500 (SPX) violating major support at 6480-6520, Nasdaq futures (NQ) violating 24,000 support, and the Russell 2000 (IWM) breaking down below crucial $245 support. This comes the team downgraded their outlook to neutral early in March. Concerns that they discussed since early-February stemmed from deteriorating market dynamics, and ever since then they been concerned about a deeper pullback, likely to 6720-6776, 6690, or 6480-6520 on SPX, while also discussing since mid-March how downside capitulation is likely needed before finding a reliable bottom. With continued deterioration in market dynamics, their report last week discussed how they were closely watching for a breakdown below 6480 and that the SPX likes to test the 200-day MA as resistance (from below) before continuing lower, and this is likely what happened on 3/23/26. 6200 and 6150 are the next supports to watch, and they would continue to be sellers on any rallies to 6480-6520 and 200-day MA resistances.

The US faces sharper inflation from crude than the UK

It is true that the UK is more susceptible than most to energy fluctuations, which is slightly ludicrous given its access to North Sea oil & gas reserves. It is also true that due to duties & taxes British drivers pay roughly 80% more to fill up their cars than their American counterparts. Yet these very taxes shield consumers from crude oil volatility. So far in March, even as oil prices rise over 30% y/y, petrol prices on British forecourts have risen by 9.6% y/y whereas US comparative “gas” inflation at the “pump” is 22% y/y. In other words, twice as bad, despite the US’s much acclaimed self-sufficiency (which is not entirely true). Despite what many believe, the reality is that the US inflationary impulse is greater than the UK’s with respect to petrol.

Equities downgraded to neutral

Sam Burns has downgraded equities to neutral and raised cash in response to a deterioration in his indicators and increased macro risk and may do so further. Since the beginning of March when the US/Israel-led war in the Middle East started, his Equity Risk Model has deteriorated further, now below the 50% level and thus no better than neutral. While equity P/E ratios have declined, higher bond yields have largely offset the rise in earnings yields, leaving his Implied Growth Model still at elevated levels. Macro uncertainty has surged (again) and investors are focusing on how long and how bad the supply disruption in the Middle East will be – markets expect just a few months, but that timeline is gradually lengthening as escape routes for Trump are reduced. The positives are that earnings estimates are holding up so far, and short-term oversold conditions are in place.

UK equity market briefing

As a direct result of higher petrol prices, CPI inflation is likely to increase to around 3.25% in March. Darren Winder explains that this needs to be balanced against the impact of base effects and the reduction in the energy price cap. Overall, his arithmetic shows inflation dipping below 3% in April. If maintained at recent levels, sharply higher wholesale gas prices are likely to result in the energy price cap rising by around 20% over July-September. Without policy interventions (which are likely), this would add ~0.5% to CPI and contribute to higher government debt interest payments. On his current arithmetic, CPI averages around 3.25% in 2026. As energy price pressures subside, CPI will fall towards the 2% target during 2027. This allows policy interest rates to resume a downward path. The jump in market interest rate expectations, to well over 4%, will, in Darren’s view, prove to be relatively short-lived as Bank Rate is maintained at 3.75%.

Technology

The semiconductor distribution channel is posting ~40% Q/Q revenue growth in 1Q26, but the composition tells a more nuanced story than the headline suggests. JNK's supply chain checks show 800G optical module demand at a 2-year high, with all global Tier 1 makers pulling orders and Broadcom Tomahawk 6 extending the cycle into 2H26; simultaneously, the ASIC-to-GPU semi revenue mix is shifting from 80/20 towards 60-70/30-40, positioning MRVL as the most direct beneficiary. On the consumer side, Apple/iOS is outperforming seasonal patterns (+10% Q/Q vs. flat expected in Q4), though component buyers stocking ahead of tariff increases are raising H2 inventory correction flags. The divergence between data centre acceleration and consumer pull-in risk shapes the setup for H2.

Discounters dominate top retail long ideas for Q2

Consumer Discretionary

John Zolidis continues to favour discount retailers for Q2, as persistent inflation from tariffs and high gas prices is expected to outweigh any stimulus tailwinds. Within the space, he highlights Five Below as the best unit growth story in retail, while Dollar Tree offers upside from a successful multi-price transition. Dollar General is improving execution, recovering margin and driving traffic with a lot of room to go relative to previous results. Savers Value Village stands out as a mispriced growth story at <7x EBITDA. Beyond discount, Sprouts Farmers Market should see comps recover on affordability, while National Vision remains an early-stage transformation story. Rounding out the basket are Boot Barn, supported by favourable Western wear trends, and Academy Sports, a cheap, heavily shorted name with comps turning positive.

Healthcare

Aaron Fletcher’s short thesis on IBRX centres on a disconnect between hype and fundamentals. The company remains a single-product story with a limited bladder cancer indication. Despite a +280% YTD stock surge and a stretched ~73x P/S multiple, revenues are modest (~$113m) and Anktiva sales growth is already slowing, while the business continues to burn ~$350m annually. The rally has been driven by CEO-led hype, culminating in an FDA warning letter. Aaron also highlights increasing competition and near-term catalysts. He pitched IBRX at our latest Best Equity Short Ideas Conference - click here to listen.

Minimising losses, maximising gains: Second buy signal activated

ViewRight's Defender Program has activated its second tactical buy signal following the S&P 500’s close below 6,375, bringing deployed exposure to 25% of its predefined allocation (out of a 40% maximum). The framework continues to operate within a healthy bull market regime, with no evidence of deterioration in market breadth or participation preceding the recent pullback. Historical analysis provides important context at this stage. Since 1988, drawdowns reaching this level have typically followed one of two paths: stabilising and recovering near current levels, or progressing into deeper and more prolonged declines. Notably, 91% of such episodes resolved before requiring further deployment. Defender’s rules-based approach is designed to systematically add exposure into periods of weakness within healthy bull markets, removing discretion and maintaining discipline across a range of outcomes.