No matches for this search

Try adjusting your filters or search criteria

Discounters dominate top retail long ideas for Q2

Consumer Discretionary

John Zolidis continues to favour discount retailers for Q2, as persistent inflation from tariffs and high gas prices is expected to outweigh any stimulus tailwinds. Within the space, he highlights Five Below as the best unit growth story in retail, while Dollar Tree offers upside from a successful multi-price transition. Dollar General is improving execution, recovering margin and driving traffic with a lot of room to go relative to previous results. Savers Value Village stands out as a mispriced growth story at <7x EBITDA. Beyond discount, Sprouts Farmers Market should see comps recover on affordability, while National Vision remains an early-stage transformation story. Rounding out the basket are Boot Barn, supported by favourable Western wear trends, and Academy Sports, a cheap, heavily shorted name with comps turning positive.

Consumer Discretionary

John Zolidis’ investment case is based on a positive inflection in same-store sales producing valuation expansion as investors give more credit to unit growth and the longer-term opportunity. He believes this thesis remains intact as comps improved to -1.4% in FY25 (vs. -5.1% in FY24) and have turned positive in early FY26, with Q1 likely >2%. While the recent >10% share price drop reflects macro concerns and weak transaction trends (-6.4% in Q4), John views this as partly intentional, driven by ~10% price increases and a shift towards higher-income customers. This mix shift should support higher gross profit per ticket despite lower traffic. With the shares trading at 8x P/E and 5x EV/EBITDA (FY26 estimates) and a 9% FCF yield, ASO is a “bargain”, with an eye towards the upcoming analyst day as a near-term positive catalyst.

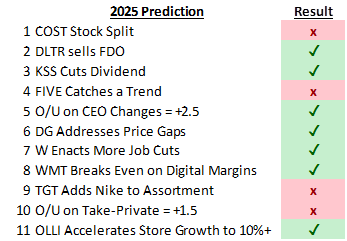

Retail predictions for the year ahead

Consumer

Looking back at GHRA’s 2025 Top 10 (+1) predictions, their batting average was good, hitting on 7 of 11 (see above). For the year ahead, their forecasts include: 1) Target announces an investment cycle on Mar 3rd with adjusted FY26 EBIT margin in the ~3.0%-4.0% range and a 2030 view of ~5.0%-6.0%. 2) Five Below launches Digital Loyalty Card. 3) Academy Sports adds another big brand…likely HOKA. 4) Costco unveils a special dividend and/or ramps share buybacks. 5) Ollie's embarks on large scale sales productivity effort. 6) Burlington takes a page (or two) out of the Ross Stores marketing playbook. 7) Someone gets acquired; BJ’s and Arhaus the most likely candidates. 8) Home improvement recovery gets pushed out…again.

Consumer Discretionary

A story riddled with risk - Brian McGough argues DKS is priced for perfection despite mounting structural and cyclical headwinds. Core growth is tapped out and the House of Sport concept – its only unit growth driver - is not working; comping down 20% in year 2 and down again in year 3. Inventory issues, including a Critical Audit Matter on carrying value, and gross margin risks from tariffs on private-label apparel add further pressure. Apparel (40% of sales) has turned deflationary and the Foot Locker merger is seen as immediately margin-destructive, with no strategic merits and likely to strengthen competitors such as Academy and JD Sports. Brian is incrementally of the view that the 5-year CAGR for athletic footwear in the US is -300bp below pandemic-era trends and warns that at 10x EBITDA, a historical peak, DKS is over-owned, over-earning and due for a correction.

Which unit growth stories can be bought at a discount?

Consumer Discretionary / Staples

John Zolidis reviewed 18 unit growth stories in the consumer space, breaking out the value of the existing business from the implied value of the growth option. He then calculated the value of future unit growth using a store level DCF. He compared the implied value of the growth option in the first exercise to expected value creation from store growth in the second. From this John solved for where the market was paying the largest premium to the value of future growth and where growth could be purchased at a discount. The most interesting names on the long side were Academy Sports & Outdoors, Luckin Coffee and Yum China. Sprouts Farmers Market still looks very cheap even after +50% move YTD. Investors are paying the biggest premium for Dollarama, Chipotle and Dollar Tree.

Consumer Discretionary

The market is ascribing zero value to the company’s store opening plans - ASO is currently at a growth inflection making it especially susceptible to being misvalued in the current market. John Zolidis considers a range of outcomes for earnings and cash flow from the existing business in addition to the impact of adding 80-100 new stores from FY22-FY26. Shares are <$38, just 5x FY22E EPS, if ASO can trade at 10x, it suggests a $110 price by early 2026 (190% upside). Alternatively, a 10%-12% FCF on the current business plus $25 for the discounted value of future stores suggests a $75 value today (~100% upside).