Report by Willis Welby

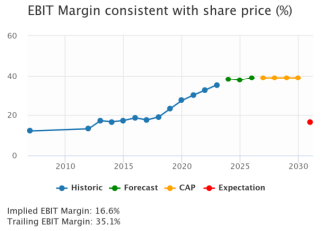

This business has a lot to like - high margins, good growth and plenty of opportunity for more accretive M&A. The Healthcare deal has also left a strong financial base from which to move forward. FY numbers last month were no surprise. Revenues were up 4% and adjusted margins were flat. Analysts had put through some upgrades with the trading statement in early Jan and though the share price has collapsed they put through another round in March. The implied to Y3 EBITM ratio is now back to 43. Willis Welby can see the share price doubling.