No matches for this search

Try adjusting your filters or search criteria

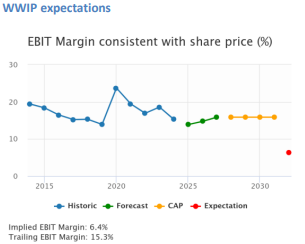

Technology

The group’s year-end update more than confirmed the optimism management showed at the interims. Revenues will be ahead of consensus, with double digit growth and record backlogs. Confidence is also evident in a 21% increase in headcount, albeit with some margin pressure from contractor usage. Consensus revenue forecasts have been upgraded, though EBIT has edged slightly lower. The balance sheet remains a clear strength with £160m of net cash and potential for ~£70m of Y2 FCF. While analysts appear to be recognising the revenue inflection, the implied to Y3 EBITM ratio here is now 40. That is very low for the growth on offer, with Willis Welby arguing the shares could easily rise 50% from current levels.

UK Mid Caps: Cheap Tech

Basic metrics for Willis Welby’s UK mid cap Tech coverage remain compelling - financial productivity is universally strong, the median implied to Y3 EBITM ratio is just 66 and the median consensus Y3 revenue growth is 9.1%. Highlighted stocks include Moneysupermarket - boasts a great balance sheet, decent growth and an implied to Y3 EBITM ratio of just 45. This share price would not feel strange 50% higher. Kainos - impressive growth model with good returns, a strong balance sheet and a cautious share price. The implied to Y3 EBITM ratio is back down at 66. This combination warrants a further move of 30%+ and a share price of at least GBP 14.00.

Seriously cheap UK mid caps

The median implied to Y3 EBITM ratio for Willis Welby’s UK coverage is now 68 for which you get median consensus Y3 revenue growth of 5.4%. And over the last three months the median move in Y2 EBIT is still an UPGRADE of 0.8%. The Q2 reporting season could be a rude wake up call, but so far, they cannot see the huge economic downturn that is priced into this part of their coverage. And if it does not materialise, then UK mid cap shares are seriously cheap. Industrials (Manufacturing & Support Services) look particularly interesting - highlights Coats, Morgan Advanced, Qinetiq, Hays and Serco. They also see decent revisions and a compelling balance of growth and expectations across Technology names such as Team17, Moneysupermarket, Auction Technology and Kainos.

UK Mid Cap Technical Review

The FTSE 250 index finds support at the bottom of the 2023 range but is still losing relative momentum vs. the FTSE 100 index. Messels continues to see selective improvement in IT Services stocks such as Computacenter (renews price and relative bases at 2020 peaks), Kainos (has rallied from support at the bottom of recent ranges) and Softcat (finding 6-year uptrend support). They have a new Buy on Playtech (reaches support from the prior range and holds the relative base). In Real Estate, they highlight opportunities in Big Yellow and Safestore. They have also closed their long in Plus500 after the stock found resistance at the highs and lost relative momentum.