No matches for this search

Try adjusting your filters or search criteria

Copper: Lack of supply growth vs rising inventories

David Radclyffe's copper coverage totals ~63% of global mine production. Copper supply continues to wrestle with many legacy headaches from 2025, mixed with the Iran conflict and its implications for diesel and sulphuric acid supply. There is therefore downside supply risk. However, the current oil disruption has implications for global growth and copper demand. Worryingly, David points out that copper inventories are rising rapidly. His coverage universe implies 0.9% annual contraction in refined copper supply in 2026, following a strong 2025. Weak supply growth for 2026, even with moderate demand growth, is at odds with strongly rising terminal market inventories, now at 1,267kt, adding to price risk. Copper is a crowded long trade, with caution warranted. The sector is not particularly cheap at spot 1.6x P/NPV10 and 9x EV/EBITDA. Antofagasta PLC is cut to HOLD. Preferred stocks include Lundin Mining Corp, KGHM Polska Miedz SA, Ivanhoe Mines Ltd, Grupo Mexico SAB de CV, Hudbay Minerals Inc and Teck Resources Ltd.

Mining equities in turbulent markets

The US-Israeli war with Iran and oil shock has resulted in some of the most volatile markets of recent times. Higher oil prices are clearly inflationary; however, the larger short-term risk for the miners is arguably the supply of liquid fuel. Slowing global growth could erode copper demand; the copper sector P/NPV10 and +1 year P/CF is trading close to previous tough levels with a spot FCF yield of 5.2% being attractive. Gold equities are still attractive with the market imputing lower spot prices today. The shares are cheap on a cash flow basis with a 6.9% spot FCF yield. Gold sector margins are still robust with better balance sheets compared to peers. Copper and gold equities have corrected, and value opportunities have emerged. Preferred coppers are Antofagasta PLC, Lundin Mining Corp and Ivanhoe Mines Ltd, whilst least preferred are First Quantum Minerals Ltd and Southern Copper Corp. Preferred golds are Barrick Gold Corp, Agnico Eagle Mines Ltd and Kinross Gold Corp.

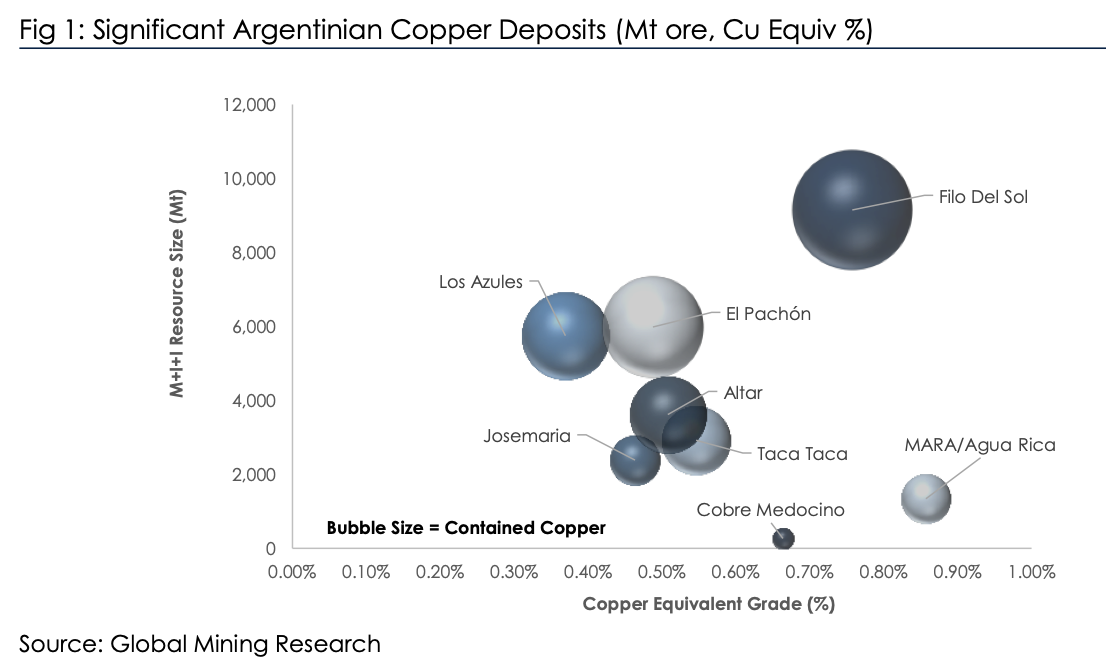

Is Argentina the next big thing?

Argentina has significant copper reserves yet produces no material copper (see chart). The new investment climate (RIGI) in Argentina, spearheaded by libertarian President Milei, is hoping to reverse this. Other volatile countries including DRC have achieved significant growth, so it’s possible. In his latest report, David Radclyffe examines the potential of Argentina copper. He sees potential for the nation to become a 1.0–1.5 Mt per year copper producer (top 10 globally), but comments on the aspirational timelines, with first copper unlikely on this side of 2029. Issues also cannot be discounted, with ESG concerns bubbling alongside a lack of infrastructure and skilled workers. David estimates the total capex at USD $40–50 billion.

Lundin Mining has the most leveraged exposure to Argentina in partnership with BHP and is the preferred exposure. There are a few exploration plays, of which NGEx Minerals (non-rated) and its Lunahuasi discovery is the largest.

Copper: Gold to the rescue

China, the largest copper market, shows no signs of improvement. Meanwhile, the global copper market recorded a 251k-ton surplus in the first half of the year, and some studies are projecting further surpluses for FY2026. Broader commodity signals reinforce this outlook, particularly the sustained weakness in iron ore prices. Expect a 5-10% decline in copper prices by year-end. Interestingly, in Veritas Research’s sample of nine copper producers, costs decreased by an average 16% and 21% in the last two quarters, driven by higher gold prices for which the precious metal is a by-product. Hudbay as a result takes the crown as the lowest cost producer, with strong growth potential and the lowest valuation in their sample. Teck Resources and Lundin Mining are fighting for the dubious honour of being the highest cost producer.

Materials

GMR continues to favour the outlook for zinc, where BOL is a large player (~0.5Mt/yr) and offers hard to find exposure. It is rare to find a company with several near-term events expected to support the business. These include a forecast recovery in Aitik grades; Tara moving back to full production rates; completion of the Odda expansion; Garpenberg throughput upside from permit revision; as well as plans to acquire Lundin’s Neves Corvo and Zinkgruvan mines. BOL is not expensive trading at 0.8x NPV10 and a prospective 2026E EV/EBITDA of 4.2x and FCF yield of 11%. Gearing is expected to peak in 2025 at ~22%.

Materials

Seeking a wealthy partner - the Josemaria project in Argentina carries significant risk, with returns likely below a reasonable cost of capital for LUN. Absent a contribution from a partner, Martin Pradier fears value dilution on an equity issuance to fund the project. Development and associated funding risk, combined with unimpressive ROE, a weaker outlook for copper prices and recession risk, all contribute to his initiation on the stock with a Sell rating and $9.5 per share value estimate. His valuation implies 3.5x and 8.5x 1-yr forward EBITDA and EPS, respectively.

Copper: Risk vs Reward

The post-Covid economic hangover has arrived. For copper this means equities have corrected, yet the metal is close to $4/lb. Markets have repriced risk, especially in small caps, but this is a short-term view. There is a case for investing while there is blood on the street, explains David Radclyffe, as he advises investors to position for a traditionally strong Q4. His preferred exposure is through more attractive and better value larger caps such as First Quantum Minerals

and Lundin Mining Corp. He also upgrades 29Metals to a BUY given its better overall metrics to peers.