Nickel may yet surprise

Report by Global Mining Research

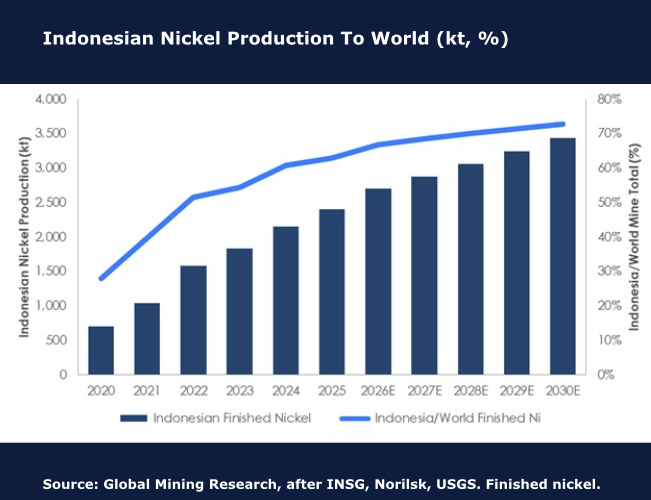

Recent events brought spot nickel up to ~US7.80/lbafterabriefreturnto US8.00/lb. The three major developments that led to this are the Iran war, a decision by the Indonesian government to dramatically cut thermal coal mining permits from 790Mt to 600Mt, and another decision to cut laterite nickel mining permits to 260-270Mt versus 2025 at 379Mt. GMR has calculated an annual nickel demand growth rate at 6.2% CAGR over the last decade, but the unceasing volumes from Indonesia (see chart) have been the issue. New changes may see parts of the global nickel cash cost curve move by ~US$1.50/lb. If laterite ore is really cut back heavily, then the price impact should add to that, but very large inventories could limit substantive price moves for some time. This is all potential; good news for producers like Vale SA, Glencore PLC or MMG Ltd. It’s too late for the Cuban producers where the lack of fuel is triggering closures.