Gold and silver entering a new phase

In his latest presentation, Jeffrey Christian of CPM Group discusses the recent movements in gold, silver, platinum, and palladium prices, focusing on the sharp decline in gold and silver and the consolidation pattern developing across precious metals markets. He explains why, despite the recent drop, prices remain within the range that CPM Group has been outlining, and why the current environment continues to point toward a period of sideways, volatile trading rather than a sustained breakout. Jeff discusses how seasonal trends, macroeconomic conditions, and investment demand are interacting to shape price behaviour over the coming months. He discusses the growing likelihood of a consolidation phase through the summer, while noting how economic and political developments could still cause short-term price fluctuations.

Click here to watch.

US: Going overweight on tech

The Vermilion team remain bullish on the S&P 500 (SPX), Nasdaq 100 (QQQ), and Russell 2000 (IWM). Market dynamics continue to improve ever since the major bullish false breakdowns at 6480-6520 on the SPX, 24,000 on Nasdaq futures (NQ), and $245 on the IWM, with all of them now breaking out to all-time highs and holding above bullish gaps from April 17. Everything that the team sees suggests bulls remain firmly in control, so the team want to be buying any pullbacks for the foreseeable future to the 20-day MA or 21-day EMA. The team discussed adding exposure to growth, and primarily technology, as growth has taken over as leadership relative to value. RS on the cap-weighted XLK is now breaking above its 2025 highs and they are upgrading Technology to overweight. The team have remained overweight semiconductors (SMH, NVIDIA Corp, Taiwan Semiconductor Manufacturing Co Ltd, Ciena Corp, etc.) and memory (SanDisk Corp, Western Digital Corp, Seagate Technology Holdings PLC, Micron Technology Inc) ever since last June, and these remain their favourite areas within Tech.

China: Support for economic growth

Recently the State Council issued guidance on “productive services” (shengchanxing fuwu) in the Service Sector. This confirms what William Hess has been saying about official expectations for the composition of growth over time, that policymakers see the largest potential share gains coming from services (tertiary) output, and within that category see greater room for “productive services” expansion over “living services”. The State Council wants to see total service sector output surpass RMB 100 trillion by 2030, up roughly 23% from current levels, which should raise services sector output to close to 65% of GDP. Meanwhile William continues to expect Vice Premier He Lifeng to deliver some form of growth support and/or easing measures for financial conditions by mid-May. On activity, China has given back most of the Q1 gains observed in March, presumably as a function of Hormuz crisis effects, and so by now the leadership has a clearer picture of what they need to do.

Drone related investment ideas

Red Cat (RCAT US) - expected to disappoint on its recent and highly speculative marine drone division; management has credibility issues from previously missing on guidance; and the company has yet to be included in the Department of War’s Drone Dominance Program.

Motorola Solutions (MSI US) - has been a dominant name in critical communications equipment for fire, police and government for decades. The long thesis now is based on the company's “transformational” acquisition of Silvus Technologies, a tactical drone networking business.

Fujikura (5803 JP) - tremendous scaling opportunity for selling co-packaged optical connectors for AI data centres, alongside expanding demand for fibre optics in drones - which is poised to become one of the fastest-growing segments within fibre optics - from military kamikaze and loitering munitions to commercial inspection drones, delivery systems and advanced surveying platforms.

Canadian Lifecos: Private credit risk under scrutiny

Financials

Roshan Paunikar’s analysis highlights rising scrutiny around private credit exposure within Canadian lifecos, with risks centred on below-investment-grade assets, valuation opacity and broader fixed-income sensitivity. While portfolios remain skewed towards higher-quality credit, companies are not insulated from a weaker environment, with potential impacts including higher credit losses, fair value marks and pressure on regulatory capital. Manulife Financial appears most exposed driven by a higher proportion of below-investment-grade private credit and a relatively riskier fixed-income portfolio, while Sun Life Financial appears most negatively exposed to wider credit spreads. Great-West Lifeco appears to have the most conservative investment portfolio among peers.

Identifying stock swaps within your portfolio

Mill Street's Swap Shop report reflects frequent interest from equity portfolio managers in using their MAER model (the Monitor of Analysts’ Earnings Revisions) to identify problematic low-ranked holdings and provide high-ranked substitutes that preserve overall portfolio allocations. The screens take advantage of MAER’s strong intra-sector or intra-industry ranking performance to allow managers to stay not only within a benchmark universe but also identify stocks within specific industries as potential swaps to keep sector / industry weightings consistent. This month they include swap screens for Global Technology / Communication Services stocks and Global Energy / Materials sectors stocks to capture the key topical themes of Tech / AI and commodity prices. Also included are the regular screens for the S&P 500 universe and their European stock universe. Click here to access the report.

Iran conflict: A buying opportunity?

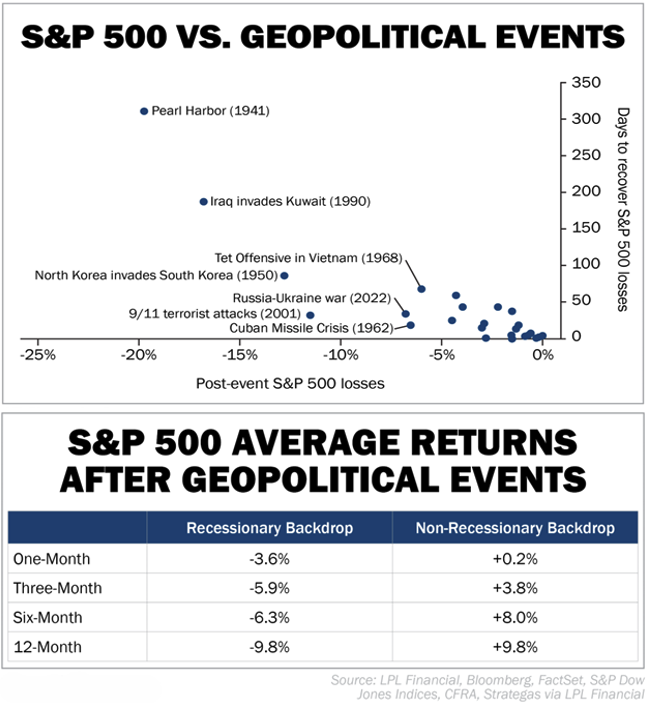

With no clear end to the Iran conflict in sight, investors are preparing for the worst. A look into history reveals that’s probably not necessary, according to Joel Litman and Rob Spivey. While markets typically wobble on geopolitical shocks, they rarely break. The chart shows how stocks have reacted to more than two dozen major geopolitical events since WW2. The S&P 500 Index's average decline during these events is about 4.5%. Markets typically bottom in roughly 18 days and recover fully in less than 39 days. Put simply, these events tend to create more fear than lasting fundamental damage. The recovery tends to arrive faster than investors expect. That's especially true when looking at geopolitical events that occurred nowhere near a recession. After events that happen near a recession, the S&P has averaged negative returns within one, three, six, and 12 months. In non-recessionary backdrops, returns have been positive for all of those time spans.

Hungary: Orban’s fall

Katharina Klotz observes that even a heavily engineered electoral system could not save Hungarian Prime Minister Viktor Orbán. As a record share of voters turned out in yesterday’s parliamentary election, the conservative, anti-corruption, and moderately pro-European Tisza party achieved a landslide victory, securing more seats than Orbán ever achieved. Katharina expects Tisza leader Péter Magyar to take office within the next month. For the EU and Ukraine, this is very good news. She expects Magyar to lift Hungary’s veto on Brussels’ €90BN loan to Ukraine (90% probability) rapidly and play a more constructive role in EU policy from defence to China. With a supermajority in parliament, he will also be able to pass rule-of-law reforms required to unlock at least a high share of the €18BN of frozen EU funds (90% probability)—a crucial lifeline for Hungary’s struggling economy.

Consumer Discretionary

Scott Mushkin upgrades the stock to Buy, arguing the market underestimates the potential to turn around Foot Locker. Proprietary channel checks, including recent visits to “Fast Break” remodelled stores, point to materially improved traffic, ticket and margins, with early comps potentially reaching double digits. Crucially, the rollout appears extremely capital-light, supporting rapid scaling, with c.250 remodels planned by summer. Management confidence is rising, with fewer store closures than previously expected. Further upside could come from scaling clearance via the Going, Going, Gone! format, rolling out of sports trading cards within House of Sport and margin improvement through expanding private label apparel brands as well as DICK’S Media Network to the FL chain.

Memory earnings power has shifted structurally. Valuations haven’t

Technology

The memory cycle is being misread as cyclical rather than structural, with no near-term earnings peak as AI drives sustained demand. Capacity cannibalisation from HBM and SOCAMM is expected to constrain DRAM supply into 2028, with NAND also remaining tight, while LTAs could see future output effectively prepaid - reducing downside risk and reinforcing earnings durability. Yet valuations remain anchored to legacy frameworks, underestimating pricing power and cash generation, with net cash potentially >50% of m/cap by FY27 for players like SK Hynix and Kioxia. Within memory, Arete sees NAND fundamentals as more compelling than DRAM in the near term. They also upgrade Samsung to Buy, with a continued beat-and-raise cycle expected in coming quarters.

Consumer Staples

Following publication of its FY25 annual report Iron Blue lifts their RKT score +2pts to 28/60 (top quartile / fertile grounds for shorting). This reflects 1) 7-year high stripped out restructuring charge; 2) another spike lower in balance sheet trade spend accruals; 3) reduced inventory and bad debtor impairment provisions; 4) various additional risks related to NEC litigation, HS compensation changes and UK Suboxone civil proceedings within RKT’s contingent liabilities disclosures; 5) another increase in KPMG’s non-audit fees; and 6) the 14% discretionary upward adjustment to the CEO’s annual bonus to reflect strong share price performance (which compares with shares -14% FY26 YTD).

The mispriced escalation risk

Markets have transitioned into a new, high-volatility regime where prolonged conflict is now the base case. The Oil Volatility index (OVC) has surged toward 120, in line with Ron William’s projected target, reflecting crisis-level conditions and implying ~35% monthly price swings (see chart). Ron sees the possibility of prices heading to $200/barrel as markets transition from localised disruption to broader macro dislocation, a possibility that historical precedent presents as highly plausible. This reflects a larger, geopolitically driven cycle instead of a short-term spike, and the dynamic is unfolding within a broader commodity super-cycle framework: gold leads during monetary stress, copper confirms late-cycle growth pressure, and Energy ETF (XLE) is already up +35% YTD in line with Ron’s tactical call. The current environment increasingly resembles a 1970s-style regime of rolling inflation waves, with stagflation risks re-emerging.

Discounters dominate top retail long ideas for Q2

Consumer Discretionary

John Zolidis continues to favour discount retailers for Q2, as persistent inflation from tariffs and high gas prices is expected to outweigh any stimulus tailwinds. Within the space, he highlights Five Below as the best unit growth story in retail, while Dollar Tree offers upside from a successful multi-price transition. Dollar General is improving execution, recovering margin and driving traffic with a lot of room to go relative to previous results. Savers Value Village stands out as a mispriced growth story at <7x EBITDA. Beyond discount, Sprouts Farmers Market should see comps recover on affordability, while National Vision remains an early-stage transformation story. Rounding out the basket are Boot Barn, supported by favourable Western wear trends, and Academy Sports, a cheap, heavily shorted name with comps turning positive.

Minimising losses, maximising gains: Second buy signal activated

ViewRight's Defender Program has activated its second tactical buy signal following the S&P 500’s close below 6,375, bringing deployed exposure to 25% of its predefined allocation (out of a 40% maximum). The framework continues to operate within a healthy bull market regime, with no evidence of deterioration in market breadth or participation preceding the recent pullback. Historical analysis provides important context at this stage. Since 1988, drawdowns reaching this level have typically followed one of two paths: stabilising and recovering near current levels, or progressing into deeper and more prolonged declines. Notably, 91% of such episodes resolved before requiring further deployment. Defender’s rules-based approach is designed to systematically add exposure into periods of weakness within healthy bull markets, removing discretion and maintaining discipline across a range of outcomes.

Financials

The market is missing a key earnings driver as ~20% of AUM is currently fee-free but will convert to fee-paying over the next 6 years. This creates a LDD CAGR on the top line without requiring market growth. With a largely fixed cost base, STJ can deliver ~10 points of margin expansion through 2030. Additional bull points flagged include STJ’s success in capturing the next generation of wealth (one third of clients are under the age of 40); while AI-driven efficiencies could unlock ~30% productivity gains and further consolidation within the advisor ranks. The stock trades on ~15x depressed earnings but ~5x 2030 earnings, with ~70% of cash returned via dividends and buybacks. TP £22.00 (80% upside).

Japan: The balance of payments and the yen’s outlook

Andrew Hunt says that is difficult to gain a clear picture of Japan’s true Balance of Payments trends; some of the relevant data seems contradictory. Rising JGB yields have slowed capital outflows from Japan (predictable) but not reversed them. Elsewhere, foreign investors have been moving back into JGBs (intriguing) and Japanese equities (interesting). The foreign interest in Japanese equities and the importance of these flows within the BoP data arguably makes the JPY more of a “risk on” currency than safe haven. In the near term, Andrew expects the JPY to remain “choppy” with a bias towards being positively correlated with risk appetite, but any sharp falls would likely be resisted in the near term by foreign central banks. Longer term, Andrew says that the fate of the JPY is inexorably linked with that of the BoJ’s credibility, something that he expects to be undermined over time by fiscal primacy.

Technology

Following NVDA's Q4 earnings release, Veritas believes several “Flammable Items” (these are items found in a company’s financial statements or within its operations that are waiting for a spark to ignite) it has previously identified are burning brighter and warrant continued investor attention. Their report examines whether supplier-funded demand is accelerating through channels including equity investments, a step-up in purchase commitments and expanded facility lease guarantees. The scale of these funding channels has increased materially, to the point where NVDA can effectively self-fund most of its reported revenue growth in the quarter. Veritas also isolates the contribution of “other income” in Q4 and presents an adjusted EPS intended to better reflect underlying operating performance. On this basis, they suggest that nearly the entirety of the Q4 EPS beat was attributable to “other income”.

Cycle convergence: Oil, geopolitics and crisis risk

Ron Williams explains how the correctly anticipated Q1 2026 shakeout signals a structural repricing rather than routine macro volatility. Cycle convergence; late-cycle economics, geopolitical tension, and behavioural reflexivity, is pushing markets to price credibility risk and supply fragility ahead of fundamentals. Oil has become central to this shift, increasingly trading as a geopolitical hedge amid rising volatility and renewed attention to chokepoint risk. A longer historical view of Iran shows recurring phases of strain, rupture, consolidation, and renewed pressure. Current developments suggest another inflection window, unfolding within a broader transition in the global order that favours hard assets and resilience over precision.

Consumer Discretionary

Iii conducted channel checks across the 3 companies to assess demand, competition and store economics. Footfall is flat to modestly down, growth is increasingly promotion- or online-led and store-level productivity appears constrained - pointing to normalisation rather than reacceleration in discretionary demand. On FirstCry, consensus expects multichannel growth to reaccelerate to mid-to-high teens via RocketBees and FC Quick, however, Iii believes execution delays and intense competition will keep growth in low single digits. For Bluestone, the Street assumes Q3’s operating leverage and ~12% pre-IndAS EBITDA margin are sustainable, but Iii expects margins to deteriorate within 1-3 quarters as seasonally weaker revenues expose a high fixed-cost base. At AVL, incremental store expansion appears supported by discounting and channel inventory build rather than productivity-led leverage.

Industrials

AXON is a play on increasing digitisation and AI adoption in police and public safety, with potential for 20%+ revenue growth for many years. Abacus argues AXON is not “just” SaaS but a physical and digital “walled garden”, combining dominant hardware (TASER, body cams) with high-margin, recurring software (96-97% subscription-based) that drives 124% net dollar retention and strong upsell. Multiple product cycles (TASER 10, robotics, Draft One AI, 911 suite) and expansion into enterprise and international markets underpins growth. While the market is focused on weaker incremental EBITDA margins and tariff headwinds, Abacus sees these as short-term risks within a structurally advantaged AI beneficiary.

An early, data-driven read on MedTech trends

Healthcare

Medmine analyses purchase order data from 3,500+ US healthcare providers, providing investors with an early, differentiated read on demand and revenue drivers. Last year, they captured several trends including tariff impact & pricing resilience, supply chain disruptions, Pulsed Field Ablation (PFA) adoption in EP labs, TAVR market resurgence and a robotics supercycle. Crucially, Medmine’s models provide a more accurate read on company performance than comparable market estimates. They averaged a 1.5% error rate, compared to 4.1% for consensus through the first three quarters of 2025. Additionally, their models tracked within 1% of reported actuals in 68% of cases, while consensus estimates met that threshold in only 13% of instances. Their Q4 models, incorporating Dec data, are now available. Contact us below for further information.

The perils of premium valuations

Trivariate analysed the top 900 US equities by m/cap at each point in time to see how many stocks traded above 40x price-to-forward earnings for the first time in at least 3 years. On average this impacted 30 stocks per year. Historically, this valuation “ascension” is most common in Technology, followed by Financials, Real Estate and Consumer Discretionary, and rare in Utilities and Consumer Staples. Once stocks eclipse 40x, multiples typically contract to ~32.6x within 12 months, with 20% falling as low as 14x. Only 38% remain above 40x after one year and just 25% after two years. While the data suggests there is no need to panic sell a stock right when it first reaches a price-to-forward earnings multiple of 40x, it does appear that beginning 6- to 9-months later, the probability of outperformance begins to significantly deteriorate.

Oil: Waiting for a downward spiral?

Vandana Hari doesn’t see a plausible path to an equitable compromise in the Ukraine-Russia peace talks, at least not within the timeframe President Trump has in mind. The market seems to agree, moving no more than 2% on any given day over the past four weeks, with Brent stuck in the low $60s. Glut-watchers are still waiting for a downside spiral that, judging by the more bearish oversupply forecasts, could have materialised at any time since the start of this quarter. However, Vandana says that the idea a Ukraine deal will unleash a flood from floating storage in a step change may be overstated. Before the market can price post-sanctions flows, it must contend with escalating Ukrainian strikes on energy infrastructure; unless Washington leans on Kyiv to halt these, further attacks on refineries/ports and potential sea-drone strikes on “shadow fleet” tankers could keep risk premium embedded.

US monetary policy: QE by another name?

Andrew Hunt says the FRB has U-turned on QT and that other central banks will surely follow as their governments’ fiscal / debt issuance arithmetic bites in a world in which the PBoC now seems less inclined to fund “everyone else’s” deficits. As expected, the Fed has gone down the path of YCC. This is QE-by-another-name, but the “certainty” provided by the Fed’s shift towards guaranteeing stable yields out to three months may have been slightly undermined by the divisions shown in the dot plots and a degree of risk aversion within the banking system. Andrew expects some positive quantity reaction vis-à-vis monetary conditions but perhaps not a large one. The Fed’s move does however confirm that there is little stomach for hard budget constraints in Washington despite the economy’s positive output gap. As such, this will undermine the USD’s internal and external values over the medium term, likely starting with the FX rate.

Gold and silver to remain volatile with underlying strength

Jeffrey Christian of CPM Group discusses the increasingly unstable economic and political environment and what it means for gold, silver, and broader precious metals markets. He compares today’s conditions with the late 1970s, noting both the similarities and critical differences to that period, and what those differences may mean for gold and silver prices. Jeff looks at the volatility across gold, silver, platinum, and palladium, explaining the factors influencing investor anxieties. He also discusses economic shifts, including weakening U.S. influence on the global stage. The video concludes with a look at inflation data, consumer behavior, policy risks, and why CPM Group expects a recession within the next 12–24 months.

Click here here to watch

China’s slump deepens

China’s domestic economy is deteriorating. Andrew Hunt asks if this could lead to a degree of angst within the population? Domestic policy conditions look to have tightened: fiscal policy is notably less expansionary, and liquidity growth has cooled as a result. Equities appear less well bid and the rally may have stalled. Andrew also points out that the corporate sector’s weak financial situation has led to a reduction in China’s once aggressive rate of exportation of private sector capital. China is now a deflationary force within the global economy. The PBoC has acted to suppress the rise in the CNY via hefty FX intervention. Presumably, the weakness in the domestic economy will lead to another round of easing within China’s fiscal policy at some point, although concerns over fiscal sustainability could delay this action. Andrew says global investors should pay close attention to China’s fiscal stance and the nature & quantum of its capital outflows. These may yet hold the key to determining “the top” in global risk markets.

Identifying stock swaps within your portfolio

Mill Street’s Swap Shop report responds to strong demand from equity portfolio managers seeking to use their MAER model (the Monitor of Analysts’ Earnings Revisions) to identify problematic low-ranked holdings and find high-ranked substitutes that preserve overall portfolio allocations. By leveraging MAER’s powerful intra-sector and intra-industry ranking performance, Mill Street highlights potential swaps within the same benchmark universe and industry, helping managers avoid “portfolio inertia” while keeping sector and style exposures consistent. This month’s screens include global large-cap Value stocks amid the recent rotation from Growth to Value, US Financials and Health Care following Mill Street’s sector allocation changes, and additional screens across the S&P 500 and their European equity universe. Click here to access the report.

Technology

PATH has repositioned itself as an “agentic automation” platform riding the AI narrative, but the fundamentals point to slowing growth. Expansion within existing customers is under pressure and the company’s ARR metric - built on future invoice value rather than reported revenue - overstates momentum relative to true performance. Guidance has improved modestly, but it is based almost entirely on FX tailwinds and timing shifts, rather than underlying demand. Deferred revenue and billing trends point towards a normalised growth rate several hundred basis points slower than reported results and management’s increasingly promotional tone around partnerships leaves much to be desired. With federal spending already pressured in the first half and a government shutdown threatening further disruptions to its US federal pipeline, Corto believes that near-term risk is clearly to the downside.

Materials

GMR upgrades GMD to Buy, viewing it as a compelling gold play in Western Australia’s Leonora–Laverton region, which accounts for ~20% of national production. The business has continued to advance organic opportunities and strategically bolt-on stranded resources, and now has the resource base to justify mill expansions, with an updated strategy release due in 1H26. GMR assumes a 2Mt/yr expansion at Gwalia, fed by Tower Hill and Laverton, supporting production growth towards 350-400koz/yr. Trading at 0.6x spot NPV5, GMD screens attractively vs. peers, offering appealing growth and rising NPV potential. Regional consolidation remains a key theme, with the company positioned as both a predator and potential target within a competitive Northern Goldfields landscape.

Ready for the contrarian gold trade?

Cam Hui has been bullish on gold, but point-and-figure charts of gold and gold miners now show that they are either very near or have outrun their measured price objectives. Tactically, the contrarian trade would be to sell gold and buy bonds. However, a cycle analysis leads Cam to conclude that the market is undergoing a shift to a hard asset price leadership cycle. Cam’s base case calls for a multi-month correction and consolidation in the manner of the 2004–2006 experience, followed by a second rally to an ultimate top at much higher gold prices. It is within this context that a long-term point and figure objective of 9,800 is achievable in the next 3–5 years.

UK: Anatomy of a rolling fiscal crisis

Helen Thomas says that the totemic Caerphilly Senedd by-election loss for Labour coupled with the inevitable cost-free, protest-vote election of Lucy Powell for Deputy Leader could not have come at a worse moment for budget preparations and for PM Starmer. After the OBR delivers its final pre-measures forecast, Reeves will know what number is required to meet the fiscal rules. By Nov 10th, the OBR will deliver its initial post-measures forecast - essentially a judgement on whether Reeves's shopping list of measures will pass muster. If not, there will be more HMT/OBR back and forth until it does. Except the shifting political landscape means that this is no longer just an optimisation problem between two economic institutions. Helen says that for the embattled prime minister the situation looks terminal, and Starmer will be gone within months, as a result of challenge to his leadership by those in the Labour Party who now oppose him.

Financials

OWS’s short thesis continues to play out as growth slows and profitability erodes. Total Written Premium (TWP) growth is decelerating, converging toward a long-term low double-digit rate, while management’s talk of 40% growth within five years appears unrealistic. Agent growth has stalled (+3.8% Y/Y vs. +11.1% last quarter) and productivity per agent has essentially been flat for 3 straight quarters. Meanwhile, operating costs per agent continue to rise, leading to margin compression that management expects to persist into 2026. OWS argues that GSHD’s franchise-heavy model is becoming less attractive to experienced agents and increasingly reliant on costly recruitment of new ones, leaving valuation vulnerable to further downside. TP $52 (25% downside).

Materials

EM Spreads initiates coverage on Braskem with an Overweight recommendation. They believe the company’s large domestic footprint, political relevance and partial government ownership make a default event less likely near term, but the credit now hinges less on fundamentals and more on political and strategic decisions involving Petrobras, the federal government and Braskem’s ability to strengthen liquidity. They see asymmetric risk-reward at distressed prices, with outcomes contingent on a secured-liquidity bridge, PRESIQ approval, direct support measures and broader policy backing for Brazil’s petrochemical sector. They favour exposure to the lower-priced bonds within the curve for better downside protection and see greater value in the 2030s at $38.3, 32.1% YTM, 3.1-yr duration.

Debt Risk Monitor

Report by

TT Equity Research

TT has launched their first Debt Risk Monitor, highlighting 53 companies across Europe and the Americas, that have been flagged by their proprietary tool as potential debt risks. Previously integrated within TT’s accounting risk framework, the new monitor flags firms where debt concerns exist regardless of whether they see any other accounting issues (i.e. earnings manipulation). The tool detects signs of hidden on- and off-balance-sheet debt, an approach that previously identified Steinhoff and NMC Health ahead of their collapses. Similar to the accounting risk score, the higher TT’s debt risk score, the more indication they have that companies have hidden debts. Clients can access the full monitor, covering 7,500+ listed companies, via TT’s website, alongside historical data, background reports and ongoing monthly updates.

Energy

Following publication of the company's FY25 annual report, Iron Blue increases their DCC rating +3 pts to 27/60 (newly top quartile / fertile grounds for shorting). Key changes vs. FY24: 1) Higher one-off costs: FY25 stripped out restructuring expense increased to 7% of PBT adj, highest in 7 years. DCC also stripped out from headline earnings £74m goodwill impairment. 2) Took £17m profits on disposal of PPE inside underlying profits in FY25, the highest figure in the past decade. 3) P&L expense for inventories write-downs dropped to a decade-low of £5m. 4) DCC continued its strategy of promoting top management from within, with internal promotions to the CFO and newly created COO roles. 5) In its principal risks assessment, DCC highlighted Y/Y risk increases concerning the DCC Technology strategic review and also the impact on its operations from higher tariffs.

UK: A governing party in denial

Helen Thomas sums up the Labour Party Conference with one word: denial. Denial about the scale of the economic challenge, the breadth of discontent within the party and the country, and what must be done to resolve the situation. The message of the conference was that we are in "a fight for the soul of our country", with Starmer pitching himself against Farage. Despite Andy Burnham rowing back on his ambitious coup attempt, everyone is discussing who the replacement for Starmer will be. Meanwhile, Chancellor Reeves is fighting the Gilt market daily for her political life, but she is in denial about what is required. Helen says that we remain in a hiatus ahead of the budget, where even the Chancellor doesn't know yet what will be in it on 26th November, in part because she does not yet know how the Office of Budget Responsibility (OBR) will model her choices.

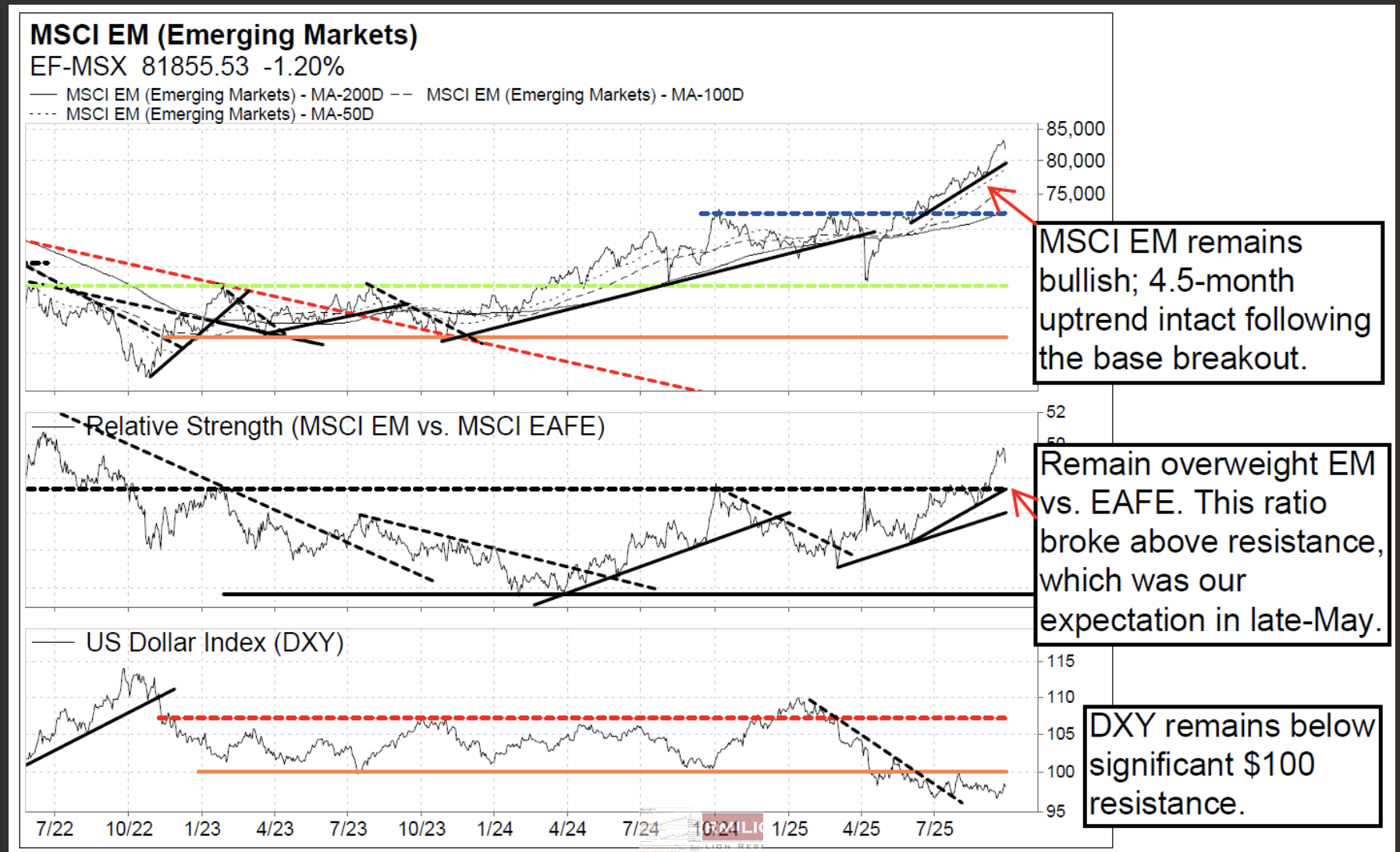

Remain overweight Taiwan, China and Korea

According to David Nicoski, the MSCI Emerging Markets index (local currency) and EEM-US (USD) are both trading within 4.5-month uptrends, and he remains bullish. David expects support at the uptrend, which also coincides with the 50-day MA and $50.65 horizontal support on EEM-US. He would view any pullback to $48 support on EEM-US as a buying opportunity. For EM countries, while price remains attractive, he is downgrading Greece to market weight due to RS deterioration. EM countries where he remains overweight include Taiwan, China, and South Korea. Additional leadership countries include Vietnam, Romania, and Pakistan. For EM sectors, defensive EM sectors (staples and utilities) continue to underperform and are at YTD RS lows; underperformance has continued, as expected -- avoid. Meanwhile, attractive EM sectors where David expects outperformance include: MSCI EM technology, consumer discretionary, materials, and communications. He is also monitoring for a RS bottom on EM health care.

Deutsche Boerse integrates social media intelligence in market surveillance software

While Deutsche Boerse has been an early adopter of social media monitoring for years, they have now taken the critical step of integrating Stockpulse's social analytics directly into their core Scila surveillance system. This integration provides comprehensive monitoring of 70,000+ global equities and cryptocurrencies with real-time social sentiment analysis, buzz metrics and seamless workflow integration within their mission-critical market oversight platform. This signals a broader trend toward holistic market surveillance encompassing trading data, news feeds and social sentiment. As social media increasingly shapes market dynamics, similar integrations are likely to follow globally. For investors, Stockpulse's insights into social sentiment, help spot emerging risks and opportunities before they hit the market. Contact us for a free trial / demo.

US: Shutdown

With just over two weeks left until the US government runs out of funding, the odds of a government shutdown are rising. Unlike recent funding cliffs, both sides are facing competing political incentives to push the funding debate to the brink. At the heart of the issue is the backlash within the Democrats over the last government funding fight. Senate Minority Leader Schumer and a handful of Democratic senators ultimately supported the bill, believing that staving off a shutdown was the least bad option, resulting in weeks of backlash over his decision. Although government shutdowns are often averted at the last moment, there are reasons to believe a last-minute deal won’t materialize this time around. In this case, Democrats believe their healthcare-focused message is a political winner while the GOP believes that offering Democrats a clean funding bill and letting them vote it down will put the blame for the shutdown squarely on them.

Compounding at the curb

Industrials

The waste sector has proven to be one of the most durable compounders in the industrials sector. Essential services support stable cash flow across the cycle, reinforced by pricing discipline and steady volumes. Growth is amplified through ongoing consolidation and optionality in RNG and EPR. Within this backdrop, Veritas sees diverging investment cases for Waste Connections and GFL. WCN, with modest leverage, FCF conversion returning to 50% post-RNG build and balanced capital returns, offers steady compounding. Attractive end-market exposure and visibility to double-digit FCF growth support a premium valuation and Veritas’ Buy rating. By contrast, GFL has ~70% more FCF growth priced in than peers, while longer-term margin and FCF convergence remain uncertain, particularly vs. a structurally advantaged peer like WCN. Accounting adjustments add complexity and LFL comparisons highlight its shortfall vs. larger peers.

DR Congo: Murmurs in the military

The military prosecutor indicated that the state has sought prison sentences ranging from three to 15 years for 40 military officers accused of plotting a coup. The military officers were arrested in April, after being filmed at a hotel declaring an end to President Felix Tshisekedi’s governance and stating that they would seize power. The development comes on the back of scores of arrests of military officers in recent months for various alleged infractions. While the risk of a coup in the near term is considered low, the risk will escalate to moderate over the longer term, particularly as the 2028 elections approach. If Tshisekedi fails to resolve the M23 conflict, it will likely worsen lingering public grievances with the statesman. This could undermine Tshisekedi’s position within the ruling Sacred Union coalition and the military, and may even lead to elections being cancelled.

UK: Under the weather

Mark Bathgate’s exceptional level of dialogue and understanding of Westminster/Gilt markets has allowed him to accurately call changes over the past few tumultuous months. Mark warned clients through May and June that Labour MPs were unwilling to accept any curbs on welfare spending, and hence a much larger deficit, gilt funding needs and tax cuts would be the main political and market talking points for the second half of the year. He sees the upcoming Autumn budget being dominated by an internal debate within Labour over which taxes to hike, which will play out via media leaks until a last-minute resolution. There is little reason to expect a change from the story of excess inflation, overshoots in borrowing needs, higher taxes and weak household real income growth and spending. Hence, the market trend to higher long term gilt yields and underperformance of other DM sovereign bond markets is well founded, and investors should expect no reason for change.

Quantum computing primer unveils two new Buy ideas

Technology

Rosenblatt initiates coverage on D-Wave (Buy, $30 TP) and IonQ (Buy, $70 TP), identifying them as differentiated, high-conviction ideas in the rapidly expanding quantum computing market. QBTS offers unique exposure to quantum annealing - particularly suited for optimisation workloads - and is expected to grow revenues at a +66% CAGR from 2025-2030. IONQ, a leader in trapped-ion architectures, is positioned to exceed $1bn in revenue within the next few years, with significant upside from its product roadmap and ecosystem development. These initiations are framed by Rosenblatt’s comprehensive quantum computing primer, which outlines the core principles, architectures and commercialisation pathways shaping the industry’s next era and underpins the firm’s bullish stance on both names.

Communications

Report by

Blue Lotus Research Institute

Blue Lotus expects Tencent to beat 2Q25 revenue, IFRS operating profit and net income forecasts, supported by success in the extraction shooter genre, which has exploded in popularity within the Chinese market recently. Tencent’s Delta Force has surged from ~5m MAUs in Jan to 38m in July, making it the company’s 3rd largest game. Arena Breakout is also proving to be extremely popular. While both Tencent and NetEase have blockbuster titles in development, the former appears to be moving faster - likely due to its generative modelling strengths. With upside to valuation and near-term catalysts, Blue Lotus names Tencent as their Top Pick in the gaming sector.

Materials

GMR maintains a Buy rating on NST following their KCGM site visit, reaffirming the mine’s Tier 1 status with a US$6.7bn NPV5 valuation. The A$1.5bn expansion remains the key near-term focus and risk, but appears on track for completion within 12 months. While the market remains concerned about lower near-term FCF and high capex (~A$500m/year), GMR sees KCGM as strategically critical, with meaningful upside from displacing low-grade stockpiles with higher-grade ore, improving mill throughput and ramping up the Fimiston underground. The mine’s long life, production growth potential (to 850-900koz by FY29) and exploration upside through high historical OVMs make it NST's crown jewel, but successful delivery in the near term remains crucial for realising that value.

Iron Ore: Higher prices, but still within medium-term trading range

Recently SGX 62% iron ore futures initially traded to lows of US$98.00/t CFR China in response to the release of a plethora of disappointing macroeconomic data. That said, there were several indications that some policy measures would be introduced soon to cut back overcapacity. Although the government's intentions will have a negative impact on China's iron ore consumption, the positive impact on Steel margins has counterintuitively dragged iron ore prices kicking & screaming higher. Accordingly, Atilla Widnell has updated his short-term target to US$100.14-101.55/t CFR China. As to the medium-term outlook, markets are entering a period of seasonably tighter iron ore supply through the third quarter. Atilla can't see how 62% iron ore futures trade outside of the current range unless there's a material black swan event. As such, he is only tightening the upper boundary given that he feels the upside potential is relatively limited, maintaining his medium-term outlook to US$95.70-105.15/t CFR China for Q3 2025.

Technology

Despite a solid Q3 beat and raise, MU shares fell on misplaced concerns over HBM oversupply. Arete sees strong FY26 growth, with HBM projected to reach ~40% of DRAM sales by late 2026, reinforcing MU’s status as an essential yet still undervalued AI stock. Nvidia continues to request additional HBM and potential resumption of H20E (with HBM3E-8Hi) sales could act as a catalyst for further global supply tightening. MU must demonstrate HBM4 competitiveness (16-layer stacking capability) within 6-8 months to ease investor concerns. Arete also expects MU to gain eSSD market share at the expense of Samsung and SK Hynix. A combination of stable traditional DRAM pricing and rising HBM mix to drive a 63% Y/Y rise in FY26 EPS to $12.78. TP increased to $150 (35% upside).

Technology

Forensic Alpha has raised PAYX’s risk score to the highest level (10/10), citing a sharply rising trend in DSO as a key flag in the company’s latest 10-K. The increase stems from significant growth in “Purchased Receivables” tied to PAYX’s Funding Solutions business, which provides non-recourse payroll advances to staffing agencies. These receivables rose 23% Y/Y to $1.2bn, now ranking among the largest items on the balance sheet. Given its growth and size, Forensic Alpha was surprised there is only one passing reference to it within the investor presentation and no mention of it on the Q4 earnings call. Changes in cash flow presentation and more optimistic revenue recognition assumptions further raise concerns about transparency and earnings quality.

Utilities

Tom Beevers of Forensic Alpha pitched ORSTED as a short at our latest Best Equity Short Ideas Conference, arguing that the company’s balance sheet is materially weaker than the market appreciates, with true leverage significantly higher than reported and free cash flow overstated. The stock scores a maximum 10/10 risk rating on Forensic Alpha’s platform, which leverages proprietary machine intelligence to detect red flags buried within financial statements and governance disclosures, across 35 risk categories. Click here to listen to Tom's presentation and here to access the slides.

Industrials

CAT ranks among Two Rivers’ top short ideas within its Declining Business Model framework. Despite deteriorating fundamentals, the stock trades at historically high multiples - over 20x 2025 earnings. Sales have declined for multiple quarters (-9.8% in Q1), estimate revisions remain deeply negative and margins are rolling over from peak levels. Working capital is rising. Finished goods are slowing. Forecasts project cash balances to dwindle on large maturity payments leaving the company with a negative cash position without refinancings. At the last earnings release, CAT missed on the sales, EBITDA and earnings lines.