Innolight: AI optics leader targets H-Share listing

Technology

Aequitas offers an early look at Innolight as it aims to raise ~$5bn in an H-share listing (up from ~$3bn in late 2025), potentially making it one of Hong Kong’s largest deals this year. The company is the global leader in optical transceivers and is benefiting from strong demand driven by AI-related data centre capex. Growth has been exceptional, with revenue up 122% in 2024, 61% in 2025 and a further 192% YoY in 1Q26, alongside margin expansion. With revenue heavily concentrated among hyperscalers and shares already trading at elevated multiples (~37x FY26 P/E), the key question for investors is how much of this growth is already priced in.

Industrials

2Xideas latest deep-dive focuses on APG - a high-quality compounder, supported by market leadership and durable advantages in a regulation‑driven, non‑discretionary end market. Demand for fire protection inspection and maintenance is underpinned by stringent compliance requirements, while low customer cost supports pricing resilience. The group differentiates through national scale, premium service and investment in skilled labour. With significant consolidation runway and a proven M&A playbook, APG is well‑positioned for sustained DD earnings growth. 2Xideas forecasts revenue growth of 7.4% p.a. (2025-2032E), adjusted EBITDA margins rising from 13.2% to 17.9% and cumulative FCF of $7.8bn (~45% of m/cap). Applying a 20x exit NTM P/E 2032E, they estimate total shareholder returns of 12.9% p.a. over this period.

Industrials

Grid constraints threaten to slow data centre construction growth, potentially disrupting STRL’s key revenue growth and margin expansion engine. Early signs are already visible, with decelerating construction data, softer backlog and margin pressure in its core E-Infrastructure segment. The CEC acquisition is a desperate move by management to mask a plateau in its site prep business and expand into Texas ahead of increasing competition. With cash flow moderating (and diverging meaningfully from adjusted earnings), insider selling rising and valuation elevated (~22x EV/EBITDA), OWS is targeting more than 30% downside.

Materials

GMR upgraded KGH to Buy, following the recent pullback, arguing the stock offers a cheaper, lower-risk way to gain silver exposure. KGH is a much larger silver producer than often appreciated, with silver contributing ~26% of 2026 revenues (rising to ~32% at higher prices), supported by stable production and assets in low-risk jurisdictions. GMR forecasts earnings to rise ~70% Y/Y, with a base case of $79/oz silver in 2026, falling to $52 and $47 thereafter. The stock trades on ~7.7x 2026 P/E and ~4.4x EV/EBITDA (vs. ~7-8x for peers), with ~6.3% FCF yield. Valuation becomes increasingly compelling above $60-70/oz silver. Additional support comes from net debt trending to zero by 2028 and declining royalty charges.

Equities downgraded to neutral

Sam Burns has downgraded equities to neutral and raised cash in response to a deterioration in his indicators and increased macro risk and may do so further. Since the beginning of March when the US/Israel-led war in the Middle East started, his Equity Risk Model has deteriorated further, now below the 50% level and thus no better than neutral. While equity P/E ratios have declined, higher bond yields have largely offset the rise in earnings yields, leaving his Implied Growth Model still at elevated levels. Macro uncertainty has surged (again) and investors are focusing on how long and how bad the supply disruption in the Middle East will be – markets expect just a few months, but that timeline is gradually lengthening as escape routes for Trump are reduced. The positives are that earnings estimates are holding up so far, and short-term oversold conditions are in place.

Communications

While the market treats APP as an AI play, Andrew Freedman sees it is an infrastructure monopoly story. APP’s true moat is MAX, its mediation platform controlling >60% of mobile gaming impressions and supplying the auction data that powers AXON - without it, AXON’s performance is materially weaker. Andrew’s analysis includes how the company's 2025 game divestiture created a structural data deficit; why the identity graph is more fragile than the market appreciates; how E-Commerce scaling faces a bifurcated reality; why the mediation monopoly is under attack and the spread is unsustainable; and, how the regulatory cascade creates asymmetric downside.

Technology

The group's competitive moat is anchored by three mutually reinforcing advantages: 1) a proprietary, cloud‑native payments infrastructure with direct integrations into 50+ national payment systems across the world, creating a durable cost leadership position that compounds with scale; 2) a Mission Zero pricing philosophy, that continuously reinvests operational efficiencies and scale benefits into lower prices, driving organic volume growth and deepening customer stickiness; and 3) a growing platform business, which is transforming potential competitors into distribution partners, expanding the company's netting pool and lowering unit costs across the entire network. 2Xideas forecasts 14.7% revenue CAGR and 15.9% underlying income CAGR to FY32E. Assuming a conservative 20x exit NTM P/E, this supports ~17.5% annualised TSR.

Consumer Discretionary

John Zolidis’ investment case is based on a positive inflection in same-store sales producing valuation expansion as investors give more credit to unit growth and the longer-term opportunity. He believes this thesis remains intact as comps improved to -1.4% in FY25 (vs. -5.1% in FY24) and have turned positive in early FY26, with Q1 likely >2%. While the recent >10% share price drop reflects macro concerns and weak transaction trends (-6.4% in Q4), John views this as partly intentional, driven by ~10% price increases and a shift towards higher-income customers. This mix shift should support higher gross profit per ticket despite lower traffic. With the shares trading at 8x P/E and 5x EV/EBITDA (FY26 estimates) and a 9% FCF yield, ASO is a “bargain”, with an eye towards the upcoming analyst day as a near-term positive catalyst.

Communications

While the company likes to describe itself as strongly cash generative, FY25 results tell a different story. Cash inflow from operating activities fell sharply from £333m to £202m. Forensic Alpha also identified several other red flags, pushing ITV’s Risk Score from '8' to '10' (max. rating). Working capital has been a persistent drag, with the headwind widening from £144m in 2024 to £196m in 2025. Trade receivables rose 12% to £500m despite flat sales, driven largely by long-term balances now representing 18% of the total. Contract assets increased 33%, including a jump in non-current contract assets from £4m to £39m. Meanwhile, exceptional charges related to restructuring and M&A rose from £65m to £107m, further weighing on cash flow. For now, the market is focused on the potential sale of the M&E business. If it falls through, attention will shift back to the company’s underlying fundamentals.

Start slowly closing oil positions on any further rise in price

William (Buff) Brown observes that the US/Israeli-Iranian conflict has spread throughout the region with major interruptions in oil transit in the Arabian Gulf, with Iranian missile strikes in neutral Gulf countries, i.e. Oman, Bahrain, UAE, etc. While most were strikes directed against US assets, there were also strikes against civilian areas. With regard to oil transit, Iran has claimed that the Strait of Hormuz is effectively “closed”. However, it is not closed in the sense that Iran is, as of yet, targeting vessels en masse and/or has mined the 2-mile-wide outbound channel. The situation remains highly dynamic, however, and could change one way or another at any time. In any event, with the prompt NYMEX crude oil contract trading above $70.00 per barrel, he suggests maintaining the status quo for the time being, but on any further material price strength slowly begin closing out long positions. He does not recommend going short as prices rise.

South Korea: Words of warning

Jonathan Anderson observes that Korean equities shot up another 50% in the first two months, making Korea the best-performing market on the planet in 2026 so far. He notes that this is heavily due to the AI boom and Samsung, but "domestic Korea" has continued to rally this year as well. However, there's still no support from domestic macro. As before, Korea's economy is flatlining or contracting almost everywhere he looks: durables, construction, retail, credit, earnings. And while exports are rebounding, memory prices still haven't been able to bring Korea back to the EM-wide average trend. Jonathan says it will be hard to motivate further gains in local names. Equity multiples have already eliminated the famed "Korea discount" and continue to rise at the margin, i.e., corporate reforms have already been priced in well in advance of actual results - and there's no sign that the rally is boosting earnings and growth potential as of yet.

Approaching peak AI hysteria

People are gregarious and instinctively follow the impulses of the herd, remarks James Aitken. The past two weeks have been a reminder of the mob mentality, and with dystopian projections on AI hysteria reaching millions of views, James believes we are approaching peak AI hysteria. Just remember when scouring the news: why am I reading this now and who benefits? XAI, Anthropic and OpenAI are all in windows to raise absurd amounts of money at lofty valuations, so it’s no surprise everyone is getting almost daily updates on LLMs about their improvements. DRAM, NAND and H100 rental prices suggest the AI juggernaut and associated memory shortage continues, yet so violent has been the recent shakedown that companies that would seem to have little risk of being disrupted by AI have been smashed, too. Just look at the current P/E of Microsoft (green) vs the current P/E of Colgate (red).

Energy

A large-cap trading at just ~11x earnings, with a ~12% FCF yield and will pay owners a 10% yield in the very near future. The Coterra deal markedly increases DVN’s stature and shale production in the Delaware Basin without incremental acquisition debt, adding ~4,600 high-return drilling locations, nearly half with sub-$40/bbl breakevens. The combined company expects $1bn+ in annual synergies and plans a $5bn buyback, materially lifting FCF/share and NAV/share. Nevertheless, investors have yet to adequately reflect DVN’s improved fundamentals in its share price, with it continuing to trade at a sharp discount to other E&P players in terms of both P/OCF and at a high required FCF yield. For each 0.5x improvement in its P/OCF multiple or a 1pp decrease in its FCF yield, DVN’s share price will rise by ~$5.

Gross margins are rolling over, but net margin expectations remain high

Median gross margins for the Top 500 peaked at 46.4% in Feb 25 and have since fallen to 44.9% in Jan 26, yet bottom-up forecasts imply continued strong net income growth - likely reflecting embedded AI-driven productivity assumptions. Historically, Trivariate finds valuation multiples correlate more closely with gross profit growth than net income growth, implying further multiple expansion will require renewed gross margin strength or a structural shift in how markets reward earnings. Their quantitatively derived longs (e.g. Merck, T-Mobile, McDonald’s) have had recent multiple expansion and are forecasted to have margin expansion, but not more net margin than gross margin expansion. While shorts (e.g. Amphenol, Salesforce, Arista Networks, Las Vegas Sands) screen for gross margin contraction but net margin expansion, reducing estimate achievability.

Consumer Discretionary

The shift from puffer-only to broader fashion outerwear (wool, shearling, fur) has expanded consumers’ wardrobes, with MONC well positioned at the intersection of function and luxury. Its core styles are not overly trend-led, supporting their status as long-term investment pieces with resale value. Pricing sits above Canada Goose and Herno, but below Prada and Loro Piana, sustaining an attractive premium tier. Beyond outerwear, The Retail Tracker sees opportunity in functional yet fashionable handbags (e.g., a travel line between Rimowa and Away). Footwear remains strong but still lacks a viral breakout moment. Meanwhile, early signs of a streetwear revival could lift visibility for Stone Island and help the brand extend beyond its core. Under new leadership, renewed energy in the stock could support a move back towards the 52-week high.

The best FX trade for 2026

In Stephen Jen’s view, USDJPY may be the best (i.e., with the highest Sharpe ratio) FX trade for 2026. With the dominant election victory, Stephen points out that the LDP has enough popular support for PM Takaichi to go through with her 3%-GDP worth of fiscal stimulus. With inflation still above the BOJ’s target (headline CPI is down to 2.1%, but core-core is still hovering around 3.0%), this prospective fiscal stimulus will likely be met with accelerated or earlier rate hikes by the BOJ. Stephen says that the US Fed and the BOJ will continue to converge in 2026, with the former cutting while the latter is hiking. Stephen argues that the US dollar itself is in a structural descent, and the particular policy mix in Japan should lead to a stronger JPY. He still views 125 as a very reasonable target for USDJPY this year.

The Korea rally for 2026?

With the Korean index rallying through year-end, Jonathan Anderson examines the outlook. Part of the trend, of course, is the ongoing massive global IT boom. But, as before, the main story at home is the sharp rerating of the rest of the index; "domestic Korea" jumped dramatically over the past nine months on promises of corporate reforms. There's zero support from domestic macro. Korea's economy is flatlining or contracting almost everywhere Jonathan looks: durables, construction, retail, exports, credit, earnings. As a result, it's hard to motivate further gains. Korean multiples are already converging on EM-wide levels as the "Korea discount" narrows, i.e., reforms have already been priced in well in advance of actual results - and even in the strong success case this may not necessarily impact aggregate earnings and growth potential going forward. In short, at the macro level Jonathan doesn’t see significant upside potential from here.

TikTok’s LatAm move has global reverberations

Report by

Blue Lotus Research Institute

Blue Lotus argues that TikTok Shop (TTS)’s entry into Latin America is the largest e-commerce opportunity in developing countries for 2026. Video and live commerce penetration in LatAm remains <5% of GMV vs. 20-25% in SE Asia, despite larger GMV and strong TikTok engagement - creating a wide opening for disruption. TTS’s traffic advantage is expected to pressure incumbent margins, particularly MercadoLibre and Sea, while driving logistics upgrades. J&T Express emerges as a key beneficiary, with LatAm filling a growth gap as China and SE Asia slow. Blue Lotus also sees strategic upside for Kuaishou, partnership optionality for Grab and longer-term opportunities for Alibaba to reposition internationally.

Consumer Discretionary

A debt-free company with robust cash flows, CHWY boasts a dominant and growing market share in an industry that is not only adding customers each year but also seeing rising spend per customer. KCR - former bears now turned bullish - highlights CHWY’s resilient, subscription-heavy model, with 84% of revenues recurring, strong demographic tailwinds and a fully built, highly automated fulfilment network that drives meaningful operating leverage as volumes scale. Despite offering better growth prospects and carrying lower risk, CHWY trades at ~21x forward P/E, a ~10% discount to the S&P 500 and at <19x EV/adjusted EBITDA vs. ~25x for the index. With margins at ~5.4% and a credible path towards 10%+, each 100bp margin gain could add ~$6 per share, supporting a compelling re-rating case.

Argentina holds the line

So far so good, claims Jonathan Anderson. Not only is the post-election government holding the line on the budget, it is also maintaining the sharp policy changes of last summer, i.e., tight quantitative monetary conditions, positive real interest rates and FX market liberalization. There’s no "landing" yet. Overall credit is still growing at a 50%-plus y/y annualized pace, with inflation also stuck in the 30%-35% y/y range on a sequential basis. And the external balance is worsening again as demand pressures continue to build. There’s still work to do after all. Even so, Jonathan is taking NDF peso exposure. The forward market is pricing a dramatic peso depreciation over the coming quarter, which seems unlikely under current macro conditions, and the team are taking a tactical position here. By contrast, Jonathan remains on the sidelines in the dollar sovereign and equity markets.

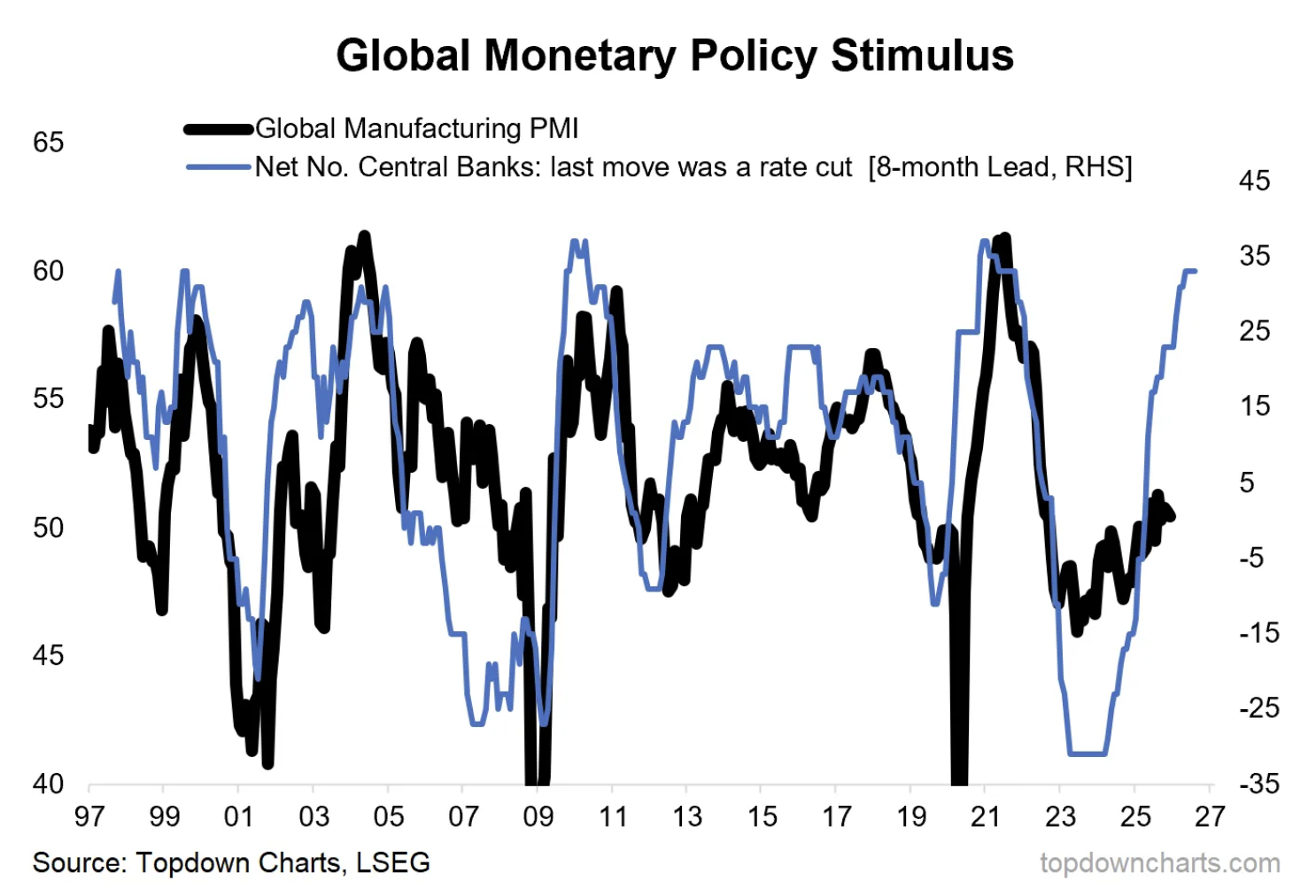

From tightening to tailwinds

Callum Thomas says that the biggest story in macro of the 2020s will echo on into 2026, with monetary policy going from tailwind in 2020 to tightening in 2023, and back to tailwinds again now. This is coming at a time where nascent signs are showing an upturn in the macro pulse from previous stagnation (e.g. the global manufacturing PMI). Callum points out that the path laid out by the monetary policy leading indicator in the graph below is a very interesting one indeed, and it’s not the only sign. The OECD leading indicators are also pointing to a major improvement in the global economy. Aside from monetary tailwinds there are several other factors working into this thesis such as fiscal stimulus, thematic capex, inventory cycles, and so-on. But there are a couple of logical flow-on effects we need to watch should this play out as planned. One key flow-on will almost certainly involve inflation resurgence.

Technology

Arete upgrades SAP to Buy, citing improving demand visibility as the ECC end-of-support deadline drives renewed urgency around S/4 and cloud migrations. Based on their CIO and partner checks, sentiment towards SAP has improved in 2025 vs. 2024, especially in the last few months, with more customers accelerating or restarting migration plans. While large-enterprise resistance persists, RISE adoption has shown clear signs of improvement. Arete sees limited displacement risk from GenAI, which CIOs view as years away from impacting core enterprise platforms; instead, GenAI may act as an indirect catalyst, easing migrations via automation and code clean-up. Applying a ~30x P/E multiple to their higher FY27E EPS yields a new €270 FY26 TP, implying 30% upside.

Industrials

the IDEA! remains bullish on INPST following the announcement of an indicative proposal for a potential takeover. Looking at interested parties, European logistics peers risk facing antitrust hurdles, while e-commerce platforms such as Amazon or Vinted are unlikely to acquire the group outright. Private equity is viewed as the most plausible route, offering long-term capital, strategic support and operational flexibility. A consortium including PPF, Claure Group and Advent would already control ~38% of shares, with INPST CEO Rafal Brzoska’s 12.5% stake potentially tipping control. Re. valuation, the IDEA! sees EUR 16.00 (IPO price) as a floor for any deal, with their DCF analysis suggesting a potential value of EUR 18.12 per share, reflecting INPST’s substantial growth potential and European leadership in OOH deliveries.

The next financial crisis

That we live in a hyper-financialised world is not in dispute, but James Aitken cannot see the net benefits to society from changes like Kalshi, which monetise differences in opinion. He argues that over the long run, monetising any difference in opinion will create negative utility due to the externalities of normalising the idea of betting on everything. And one would think that these betting markets are enormously susceptible to manipulation by state actors; yet such is the path we are on. So what? James says he isn’t tilting against the windmill of the ongoing, hyper-financialisation of everything. Instead, he suggests that the path to the next financial crisis won’t run through (e.g.) private credit, geopolitics or whatever, but instead it will run directly through market structure, period. What happens when, for any period of time from minutes to hours to days, all the machines that intermediate 1x, 2x, or 3x levered ETFs, prediction markets, 0DTE, bonds, stocks etc. decide ‘computer says no’?

Real Estate

JSB is defying Japan’s demographics. Despite the shrinking pool of 18-year-olds, Yuka Marosek argues the student-housing leader continues to compound growth thanks to rising university enrolment, a structural shift away from general rentals toward purpose-built student housing and JSB’s unmatched operational moat. While foreign-student demand adds another tailwind. The company runs ~99,300 units with 18 years of 98%+ occupancy and 11 consecutive years of revenue/profit growth. Valuation-wise, JSB trades at an EV/EBITDA of 8.3x and a P/E of 14.4x - levels that appear low given the group’s ability to deliver steady growth.

Consumer Discretionary

Alibaba’s stepped-up AI investment is pressuring margins, but RFM argues it has now hit critical mass in open-source AI, making it the leading contender in China’s artificial intelligence race. Headline revenue growth in Q2 was only +5% Y/Y, but was +15% adjusting for disposals. The standout was Cloud Intelligence, +34% Y/Y, powered by surging demand for AI services. Qwen now has 180,000+ models on Hugging Face, more than double the No.2 player, giving Alibaba the network-effect scale needed to dominate China’s AI ecosystem. With core e-commerce stabilising and shares far cheaper than Amazon (17x FY26 P/E vs. 29x), RFM sees sentiment turning decisively positive.

How to beat the S&P500 - the Q&A that matter

Trivariate examines six core issues for long-only managers benchmarked to the S&P500: 1) Beta: despite long-term data favouring sub-1.0 beta portfolios, this is currently nearly impossible given the high-beta “Great 8”. 2) Alpha vs. Risk: ~75% of holdings should be for risk management. 3) Diversification: run both a broad risk book and a concentrated alpha book - essentially two portfolios in one; holding a higher number of stocks vs. history. 4) Position Sizing: take large, conviction-weighted bets in names with high company-specific risk / hard to replicate (e.g. Healthcare). 5) Blow-up Avoidance: avoid large exposures to bottom-decile FCF converters, large increases in inventory-to-sales, large intangible accruals and extreme valuations. 6) Macro: portfolio managers must consider what set of macro conditions are best for their portfolio performance.

Consumer Discretionary

Trading at the cheapest valuation since listing (9x FY25 P/E) and offering a 10% dividend yield, FDJU has more than discounted temporary headwinds. While regulatory tightening and higher taxes in France, the UK and the Netherlands will cut FY25 EBITDA by ~€55m (145bps margin drag), it is a small dent vs. the €3.3bn in lost market value since 2021. Beyond this, FDJU’s technology-focused, online-diversified model post-Kindred integration is more attractive than ever, underpinned by stable lottery cashflows. AlphaValue expects sentiment and the share price to recover sharply, calling it an exceptional risk/reward setup. Their TP offers more than 100% upside.

Consumer Discretionary

Katitas has mastered a business model that many find difficult to replicate: buying, renovating and reselling pre-owned homes with consistent success. With 36% foreign ownership, investors clearly recognise the company’s ability to address Japan’s vacant housing problem and the stock trades at a premium P/E of 18x vs. single-digit averages for residential construction peers. Following strong H2 results and raised guidance on Nov 7th, the stock jumped 10%. Yuka Marosek’s latest piece explains why Katitas’ unique business model deserves that premium.

Technology

Richard Windsor argues that data centre revenue is the “elephant in the room” the market is ignoring, with substantial contributions now expected in FY27 rather than FY28. He estimates QCOM’s A200/A250 products could add ~$2bn in incremental data centre revenue, with potential upside if a hyperscaler deal closes soon. Combined with stronger PC growth (he views current forecasts as far too low) and upside optionality from its BMW-linked ADAS stack, QCOM’s diversification beyond smartphones is ahead of schedule. Q4 results beat across all metrics, but the real story is the growth visibility emerging in new segments. With Street EPS forecasts for FY26-27 still overly conservative and the stock trading at ~14x 2026 P/E, it’s easy to see how both multiple expansion and upward estimate revisions could drive a strong rally in the shares.

Industrials

Sidoti lifts their target price by 45% following another record-breaking quarter for FIX. 3Q25 EPS and sales beat forecasts by 32% and 16%, respectively, as the company continues to steer its project mix towards the technology sector (mostly data centres). FCF hit $516m (177% of net income) while the order backlog rose 15% sequentially (all organic) and 65% Y/Y (62% organic) to $9.4bn. Expanding modular capacity remains a potential near-term catalyst, while beyond 2026, Sidoti views no shortage of end markets experiencing secular growth (e.g. reshoring, advanced manufacturing, chip plants), or other hyperscalers for that matter, that would like a greater chance to compete for FIX’s services, were current customers to decrease their expenditures. Sidoti now models 2025 EPS of $25.60 (from $22.91), 2026 EPS of $30.34 (from $26.50) and introduces 2027 EPS of $38.50.

Consumer Discretionary

PLNT is well positioned in the growing high‑value‑low‑price gym segment with scale and ample runway for growth. New CEO Colleen Keating brings relevant hospitality franchise experience to drive the next phase of growth in the US and internationally. Gen Z is the fastest‑growing membership cohort for the company, supported by initiatives like the “High School Summer Pass”. PLNT continues to refine club formats and contractual terms to improve efficiency and unit economics. 2Xideas expects 2024-31E system‑wide sales CAGR of 11.7%, driven by 6.6% annual net unit growth and 5.0% same‑club sales growth. They forecast an 11.1% EBITDA CAGR and a 44.6% margin in 2031E. European expansion remains an upside not reflected in their forecasts. They see 17.2% annualised total returns based on an exit NTM P/E of 28.0x (17.7x EV/EBITDA).

Debt Risk Monitor

Report by

TT Equity Research

TT has launched their first Debt Risk Monitor, highlighting 53 companies across Europe and the Americas, that have been flagged by their proprietary tool as potential debt risks. Previously integrated within TT’s accounting risk framework, the new monitor flags firms where debt concerns exist regardless of whether they see any other accounting issues (i.e. earnings manipulation). The tool detects signs of hidden on- and off-balance-sheet debt, an approach that previously identified Steinhoff and NMC Health ahead of their collapses. Similar to the accounting risk score, the higher TT’s debt risk score, the more indication they have that companies have hidden debts. Clients can access the full monitor, covering 7,500+ listed companies, via TT’s website, alongside historical data, background reports and ongoing monthly updates.

Oil: WTI to fall below $50/bbl?

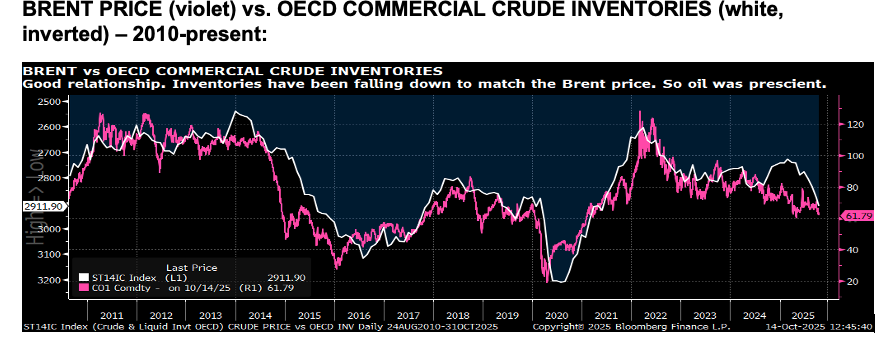

Michael Churchill says if we are in an oil glut, one has to be open to the risk of oil falling below $50/bbl for WTI. Moreover, if Trump has made a deal with Arab leaders to keep that glut going, then there is no floor until some of the North American players lay down rigs or shut in production. Gas is less at risk for this kind of event since it is already so cheap relative to oil. Michael points out that if the new race for global power is focused around AI domination, it stands to reason that the old E&P elites will be gradually losing their power in geopolitics – particularly geopolitical moves meant to keep oil prices firm. Oil prices began falling in January, in anticipation of an increase in OECD crude inventories. Brent peaked at $82/bbl in January. Shortly thereafter (in February) OECD commercial crude inventories hit a low of 2.73b barrels. Since then, Brent has fallen to $62/bbl and OECD inventories have risen 5% to 2.91b barrels.

Technology

BTN continues to see several areas where OSIS's results may be unsustainable. The company has reduced its bad debt reserve to just 2% of receivables (vs. a 5-7% historical range), adding ~11 cents to Q4 EPS (OSIS only beat Street estimates by 5 cents). The current reserve for bad debts is at least 200 bps too low; if OSIS had to raise it by 100 bps, it would be a 39-cent headwind for EPS. DSOs have surged to 151 days (historically ~90), making Q4's revenue increase more suspect and the $372m forecast for 1Q26 tougher to reach. Warranty expense was cut again (added 3.7 cents to EPS), while OSIS continues to let its PP&E age and is using fully depreciated equipment - saving 29 cents in EPS last year. Finally, FCF remains weak (negative in 5 of the last 8 quarters).

Unpacking China’s growing pet market

Consumer Discretionary

Marie Boyé examines China’s rapidly expanding pet industry, projected to reach $114bn in 2025, or 10% of global market share - tripling in size since 2020. Growth is led by pet food, followed by veterinary services and accessories, with emerging segments in pet tech, premium nutrition and luxury care. Cats now outnumber dogs, driven by urban lifestyles and regulatory shifts. Despite inflationary pressures, spending on pet essentials remains resilient, underscoring the sector’s defensive nature. Competition is fierce between multinationals and digital-savvy domestic brands leveraging influencer marketing and e-commerce dominance. Changing attitudes towards family and younger consumers’ growing attachment to pets are expected to drive continued spending, innovation and investment across China’s pet sector.

Technology

Could the stock soar over 100%? KCR argues that CSCO isn’t just cheap vs. AI peers - it is cheap relative to the broader market, trading at roughly the same multiple as Kimberly-Clark despite far stronger growth. Networking product orders have risen 10% Y/Y for 4 consecutive quarters, suggesting investor concerns about a slowdown are unwarranted. Meanwhile, the company’s rapidly growing exposure to AI infrastructure products and shift towards subscription-based revenue both support multiple expansion. CSCO trades at one-third of Arista Networks’ P/E multiple and one-quarter of its EV-to-revenue ratio - even a modest narrowing of the valuation gap would translate into substantial gains for CSCO shares. Finally, a ~5% FCF yield is far too high for a company of CSCO’s quality.

Industrials

Under new leadership, Kyodo is accelerating its pivot from the declining paper-printing business towards higher-margin niches such as high-performance packaging materials, flexible packaging and tube products. Margin gains in recent years already reflect this shift and the company’s 10-year plan aims to scale these efforts further. The key question for investors: with DNP and Toppan well ahead in diversification, can Kyodo leverage its niche strengths to establish itself as a viable third player in a consolidating industry. Yuka Marosek argues it can. While Kyodo’s OP recovery appears partially priced in (13.9x P/E vs. DNP at 14x and Toppan at 18.4x), a 4.8% dividend yield should appeal to income investors and with FY26 OP projected +20% y/y and ROE rising to 6.1%, further upside remains possible.

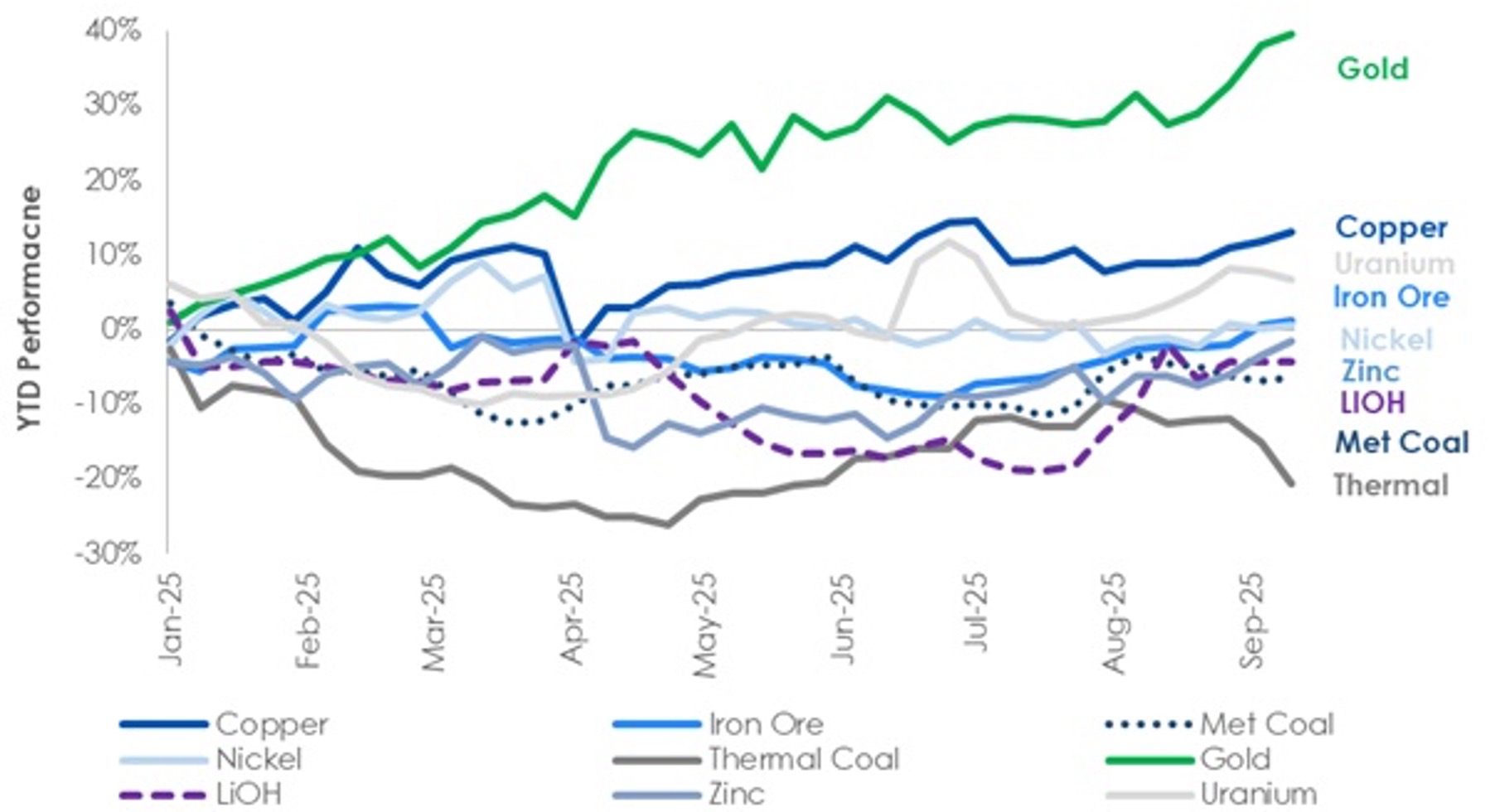

Uranium: A quirky year for a quirky commodity

Several commodities have their quirks, and uranium certainly fits into that group. Despite such a strong future outlook, and limited new mine production, this year has feen strong for neither the commodity itself nor many of the producers. Uranium spot prices recently peaked in 2024 at over US$100/lb and have traded lower since. The 2025 price has been pretty much range bound between US$65-80/lb. Annual demand of U3O8 is ~80kt (or ~175Mlb) is heavily reliant on power plant demand with contracts signed years ahead of consumption. Year to date the price is up some 7%, making it one of the better performing commodities, i.e. one of the few that hasn’t fallen on global uncertainty and growth concerns. However, supply-demand would have argued for a price move much better, and it has been well overshadowed by others.

On the topic of fiscal velocity

Stephen Jen and Faith Yilmaz introduce the concept of ‘fiscal velocity’, which measures the ratios of changes in nominal GDP to nominal fiscal spending. They find that Asian countries (ex-Japan) may be more efficient in their fiscal spending compared to European countries, a result of their higher spending on investment goods. In contrast, European countries tend to emphasise consumption (e.g. welfare spending). Highly indebted countries such as Japan and Italy allocate a larger proportion of their budget to debt servicing, resulting in little to show for it in terms of GDP. It has also become somewhat fashionable for developed countries to engage in proactive fiscal and monetary policies; this ‘Alt-Keynesian’ posture of ‘doing-more-is-better-than-doing-less’ has helped contribute to the large fiscal deficits and debt, with modest impact on actual GDP growth. On their measure of fiscal velocity, roughly speaking, Asian countries’ fiscal spending may be 7 times more efficient than their European equivalents.

Overlooked opportunities in YWR’s QARV rankings

Why do China, shipping, iron ore, hardware, Brazil… all stand out if you screen high ROE’s with low valuation? Erik@YWR sees it as scepticism about global growth on which he is taking a contrarian view. Following this month’s review of YWR’s QARV rankings key themes include: 1) A massive China bull market has only just begun. 2) Opportunities in iron ore, where Fortescue, Rio Tinto and Kumba are delivering ~20% ROEs at <12x P/E despite China’s property crash. 3) The Taiwanese semiconductor supply chain stands out as highly profitable and undervalued. Everyone focuses on Nvidia and the datacentre buildout but misses the whole Taiwanese supply chain behind this. Tokyo Electron and ASML also screen well. 4) Brazil is overlooked, with names like Itau, Vale, Ambev and B3 all screening well. 5) Container shipping - supply-chain diversification could sustain tighter freight rates than investors expect.

Technology

While China’s e-commerce sector is mired in subsidy fuelled competition, Arete argues this is outweighed by strength in gaming and online entertainment. Record approvals and blockbuster titles underpin upgrades for Tencent and NetEase, while Alibaba shows early signs of a turnaround in quick commerce and cloud. The report also examines mounting cost pressures at Meituan, the lack of near term catalysts at Xiaomi and SEA, and the structural headwinds still facing JD and Baidu.

US: Any easing rally may be short lived

The ongoing wave of T bill issuance looks to be crowding out private sector borrowers in the US credit markets. It’s early days, but Andrew Hunt points out that the data seems to be leaning that way. The US economy is slowing, with little going on outside of the AI boom, and nominal growth currently seems to have a high price / low real growth composition. The crowding out phenomenon will bring about a bear steepening effect in the near term, supporting the USD, although Andrew expects the Fed to respond aggressively. He sees markets being strong and USD weak in 2025/Q4 as a Pavlovian response to rate cuts, and that the new easing will cast the economy’s inflation expectations adrift, leading to nominal growth accelerating for the wrong reasons (i.e. prices not volumes). At some point in the coming year, markets will have to worry about an FOMC tightening and/or entrenched inflation.

USD: A race to the bottom?

According to Charles Hess, the US strategy is to lower the value of the dollar - without affecting its status as the world’s reserve currency - and encourage domestic manufacturing by increasing the price of imports and lowering the price of exports. Trade will shrink among some trading partners and increase between others (i.e., India and Russian oil), as they rearrange their economic relationships. As the US pulls away from the alliances and allies that have granted it primacy as a global superpower and as the provider of the world’s reserve currency, China is attempting to make available a substitute for the dollar-centred international economy via Beijing-centred international organizations and alliances. These Beijing-centred coalitions increasingly trade in their own currencies. Gold, silver and other hard assets will hold their value and increase in price as the dollar declines.

Technology

Boyar argues investor fears around the stock are overblown. While the loss of a respected CEO, macro uncertainty and competitive pressures in the Merchant business have weighed on sentiment, Boyar sees the past year’s share price swing as a textbook case of exuberance turning into excessive pessimism. The company retains leading market positions, a strong operating track record and a mid-teens earnings growth outlook, yet trades at just ~12x forward P/E - its cheapest valuation in over a decade. Wall Street’s intense focus on Clover's short-term performance overlooks the company's host of other valuable business lines, which together contribute ~83% of revenue. Applying a 19x multiple to 2027E EPS of $13.33, Boyar values the stock at $253, implying ~80% upside.

High-conviction short ideas

Dick’s Sporting Goods (DKS) - the Foot Locker acquisition will go down as one of the most value-destructive deals in retail history. The first time DKS misses a quarter because of perennial weakness at FL, this newco will trade at 3-4x EBITDA.

Best Buy (BBY) - 100% of EBIT comes from extended warranties, credit and membership - all of which are facing cyclical and secular pressure. Tariffs could take margins to zero, spurring a massive round of store closures.

Lam Research (LRCX) - the most complacent name in semicaps with 2026 WFE expectations set too high especially in DRAM. P/E now 4.5x turns above 3-yr average despite little growth in 2026. Domestic competition in China intensifying longer-term.

Why smart money isn’t buying crypto stocks yet

Crypto stocks are unwinding sharply and some of the most hyped names are now down 30-50% from their highs. Markus Thielen says this isn’t just about short-term corrections - it’s about the deeper repricing of crypto’s equity narrative. Some names may still have room to fall, while others could be nearing high-conviction entry points. In June, Markus flagged that several crypto-related stocks were losing momentum, prompting his take-profit recommendation on Coinbase and warning that others could follow - notably Kakaopay, Metaplanet and Circle. Since then, the damage has been significant with all three names falling heavily. Valuations remain stretched - Circle still trades at a forward P/E of 153x, compared to 102x for Coinbase and 69x for Robinhood, leaving room for further downside. A 30% correction in Circle, or similarly in Kakaopay with its 128x P/E, would not be surprising.

Healthcare

A growing, cash-generative specialty physician group with limited downside risk. MD offers a nationwide focus on neonatal and paediatric care, and stands to benefit from rising preterm birth rates and increasing demand for complex infant care. Despite these defensive and attractive characteristics, MD trades at just 8x P/E and 7x EV/EBITDA - over a 50% discount to the S&P 500. In recent years, private equity buyers have paid a median 13x EV-to-EBITDA for similar assets. Even a modest multiple re-rating could unlock significant upside - each 1x EV-to-EBITDA multiple improvement would equate to ~$2.75 boost in MD’s share price.

The trade war is dead, long live the trade war!

Despite all of the dire headlines about the imposition of a 25% tariff rate on Canada and 30% on Mexico and the European Union, Cam Hui says the only trade war that matters is effectively over. China has won. In the short run, economic policy uncertainty is receding but it’s not fully normalized. According to Cam, it’s time to adopt a risk-on posture. US equities lagged most during the trade war panic, and they are recovering and should be the leadership in the short term. In the long run however, Trump’s America First policies of continuing trade wars and efforts to reshore low value-added industries are likely to erode U.S. productivity and competitiveness. The S&P 500 is already trading at a highly elevated forward P/E of 22.2. Cam believes that equity investors should not expect US equities to continue to outperform global stocks in the next expansion cycle.

China’s digital yuan: Ain’t no dollar killer

As China drives forward the world-leading digital yuan project, Ed Yardeni dispels the notion that we are seeing a growing challenge to dollar supremacy. True, Trump’s trade war could be dollar negative, but the US economy isn’t having to deal with the Xi era’s glacial pace of economic and financial reform in a nearly $18trn economy. Although BRICS is gunning for a less dollar-centric future, the yuan sees only a 2.2% share of global foreign exchange reserves – the dollar sits on top with 58%. The PBOC also suffers a trust deficit – why would global institutions trust their e-CNY? There are some arguments that a digital yuan would help solve the country’s weak household demand, but Ed disregards the potential of this bringing enough significant change to cover the festering economic problems. At the end of the day, the nature of the digital asset a country chooses matters far less than the resilience of the economy that undergirds it.