No matches for this search

Try adjusting your filters or search criteria

Telfer vs. KCGM: The revival of Aussie icons

Materials

While the market remains cautious on Northern Star Resources given ongoing KCGM execution risks, potential cost overruns and weak near-term news flow, the company is nearing completion of a transformational ~A$1.8bn mill expansion to 27Mt/yr, part of ~A$5bn total investment into KCGM across FY22-FY28, which could ultimately restore production towards ~0.9Moz/yr by FY30. However, with management still needing to rebuild investor trust, GMR retains a Hold rating on NST. In contrast, they are more constructive on Greatland Resources, which is still in the early stages of reinvesting in Telfer / Havieron, with ~A$2.8bn of potential capex through FY32 supporting a pathway back towards ~0.4-0.5Moz/yr production by the end of the decade, alongside exploration upside at SLC and West Dome. Given the scarcity of >300koz/yr gold assets, GMR believes Telfer could become a strategic bolt-on acquisition for peers seeking scale in Australia.

Materials

GMR maintains a Buy rating on NST following their KCGM site visit, reaffirming the mine’s Tier 1 status with a US$6.7bn NPV5 valuation. The A$1.5bn expansion remains the key near-term focus and risk, but appears on track for completion within 12 months. While the market remains concerned about lower near-term FCF and high capex (~A$500m/year), GMR sees KCGM as strategically critical, with meaningful upside from displacing low-grade stockpiles with higher-grade ore, improving mill throughput and ramping up the Fimiston underground. The mine’s long life, production growth potential (to 850-900koz by FY29) and exploration upside through high historical OVMs make it NST's crown jewel, but successful delivery in the near term remains crucial for realising that value.

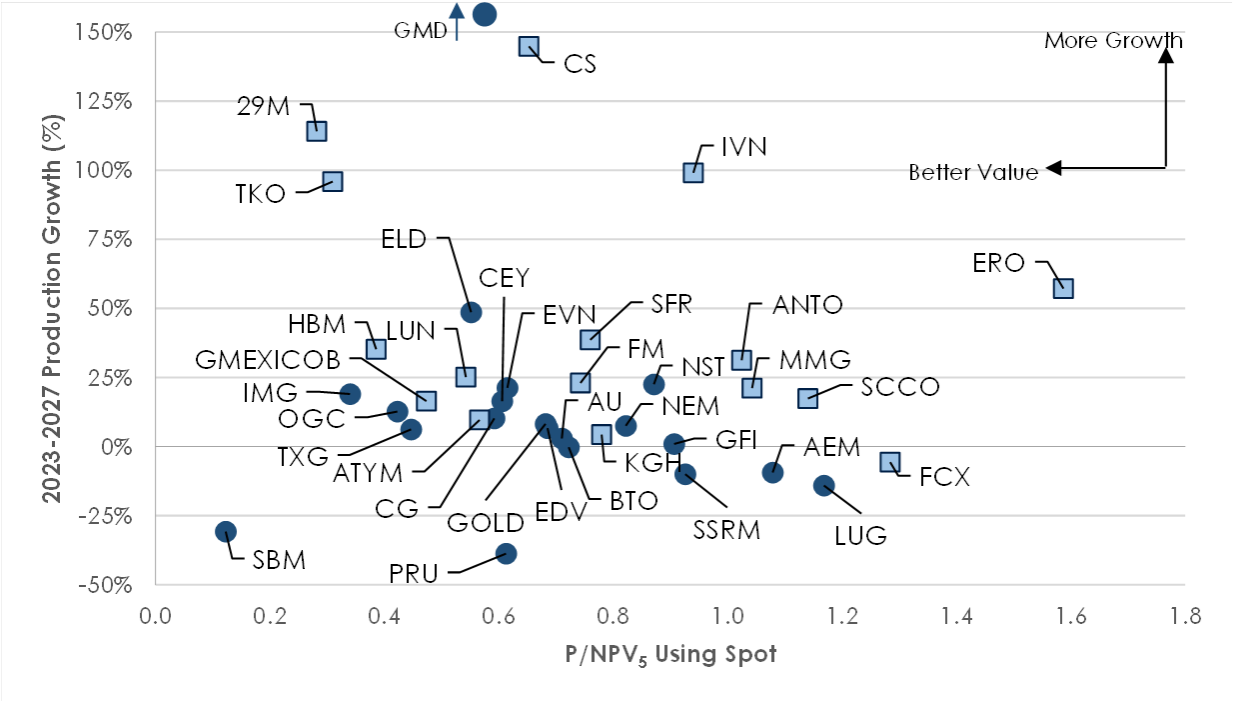

Copper vs Gold

Gold has outperformed copper for the past two years, but David Radclyffe comments that the stocks have achieved similar performance. This has resulted in copper stocks trading at a valuation premium, having attracted investor attention for future growth prospects due to the EV thematic. Overall, gold stocks offer better value and yield than copper stocks that are often more growth oriented. Gold has also shrugged off the pessimism of higher interest rates, rallying as a safe-having destination. The high beta of gold stocks to metal price presents an opportunity as the price gains traction. Preferred equities are LUG, GOLD and NST. Copper remains attractive as supply weakness and low inventories are offset by macro concerns. Investors should look towards ATYM and TKO as junior miners, and SFR amongst the mid-to-larger names.

More gold miners addressing greenhouse gas emissions (GHG)

David Radclyffe’s latest report examines the GHG reporting structures and emission reduction/mitigation plans for gold stocks covered by Global Mining Research (GMR). Interestingly, scope 1 & 2 GHG intensity increased by 35% for CO2-e t/GEO from 2015 to 2021, highlighting the challenges ahead for miners to achieve reduction targets. Within the GMR universe, Barrick continues to provide the clearest pathway. Newmont

has a list of GHG initiatives, while GFI and NST provide timelines to 2030. Most other gold miners need to lift their game as few show a tangible commitment to GHG reduction.

Materials

Sub-A$9.00 this gold producer offers great value for a lower risk / higher growth senior - NST trades at 1.6x P/NPV (1.1x spot - close to an 18-month low), and FY23 FCF and dividend yield of 8.4% and 3.1%

respectively. There is a clear pathway to ~2Moz/yr and GMR sees a potential cash surplus of ~A$0.8bn over FY23-FY25 which could be used to fund organic growth such as the KCGM mill expansion and / or increase returns to shareholders (dividend could be raised closer to A$0.5bn/yr). TP A$12.00 (40% upside).