China: Externally driven inflation

Paul Cavey says that the rise in China’s producer price index (PPI) that continued in May is of macro significance: it is pushing up industrial sector earnings, and the GDP deflator will likely turn positive in Q2. But it is difficult to find signs of domestically generated inflation that would suggest a real upturn in the economy. PPI inflation did ease MoM in May, but the headline YoY rate climbed to 3.9%, the highest since mid-2022. As would be expected, the driver continues to be upstream commodity prices. The rise in energy prices is also being reflected in CPI, with a 20% YoY rise in fuel costs pushing up the transport and communication component by 5% in May. However, headline CPI was steady at 1.2% YoY. One reason was that food prices in the CPI continued to fall last month. In addition, services inflation remains weak. That reflects the state of domestic demand, though in that regard it is perhaps notable that services inflation isn't deteriorating further.

Japan: Yen under pressure, but data is encouraging

Graham Turner says that the prospect of a rate hike at the FOMC meeting in June casts a harsh spotlight on the Bank of Japan: the BoJ will meet earlier next week, and unless it agrees to tighten policy too, the yen is likely to plumb new lows against the US$. For the Bank of Japan, there is no obvious pressure to hike, as inflation has been well-behaved. The y/y for the Nationwide CPI eased to 1.38% in April. The CPI excluding food, alcohol & energy dipped to 1.06% y/y. Real wages are rising sharply, in part, because of the drop of core inflation as well as fuel subsidies. The labour market in Japan is tight. The unemployment rate fell to 2.5% in April. Total employment jumped to 68.76m, a new high, despite a shrinking population. These are encouraging trends that bode well for Japan’s response to an ageing population, particularly against the backdrop of high government debt.

Australia heads back to the doldrums

According to Gerard Minack, Australia is growing at 2.5% – not particularly strong with working-age population rising by 1.75% – but now seems set to slow. Productivity growth remains poor, so 2.5% growth created inflation pressure that the RBA had to respond to. Gerard says the economy will head back to the doldrums of a low per capita expansion. Weaker growth is a factor behind falling EPS forecasts and the prospect of modest equity returns. Australia has had a poor decade. Average per capita GDP growth was the lowest since the 1930s (excluding the post-1945 demobilisation). What matters for consumers is disposable income, not GDP. Per capita disposable income growth was lower than GDP, payback for the mining boom boost received through the prior decade. Australia’s biggest structural economic problem is poor productivity. Poor productivity reflects low capex relative to fast-growing population, so there is little capital deepening. No capital deepening means no productivity growth.

Real Estate

Craig Huber argues that the near-50% YTD fall in CSGP’s share price has created an attractive entry point, with investor concerns around AI competition and Homes.com losses now overdone. His 2026/2027 adjusted EPS estimates are above consensus at $1.40/$2.00, with revenue forecast to rise 18.0%/15.4% to $3.833bn/$4.424bn and adjusted EBITDA to reach $833.8m/$1.142bn. The group also has $1bn remaining on its share buyback programme (representing ~7.5% of current m/cap). The stock trades at 16.8x 2027 adjusted EPS or 13.9x EBITDA. If you exclude the Homes.com losses (where there is a lot of flexibility in the expense base; sees losses dropping to ~$300m this year), CSGP is trading at only 9.4x 2027 EBITDA. Information services is a sector that historically trades around 25x EBITDA, if not higher. Craig is an “aggressive buyer” at these levels with a conservative $50 12-month price target, implying ~50% upside.

Defence Supply Chains: Hidden chokepoints, mispriced risk

The Iran conflict is not a regional event - it is a structural accelerant for the global Defence-Industrial Base. OMNISIGHT maps three converging chokepoints: China's gallium export controls (directly threatening F-35 radar integration timelines), Hormuz-driven sulphur disruptions cascading into propellant supply chains, and Qatar helium export risk affecting precision electronics. Combined, these create a butterfly chain that materially compresses production cadences for Tier-1 contractors in H2 2026 - a risk the market is currently underpricing. OMNISIGHT's institutional divergence analysis yields explicit ratings: Accumulate Lockheed Martin and BAE Systems; Hold RTX and Northrop Grumman; Reduce Rheinmetall, where a P/E of 90-100x leaves zero margin for delivery disappointment.

Consumer Discretionary

Alex Barron believes the acquisition is an important signal for the US homebuilder sector, supporting his view that the bottom of the cycle is here and now is an opportune time to buy into the sector at great valuations. The deal values TMHC at 1.24x 2Q26 book value, 1.17x Alex’s 2026E book value and 12.9x 2026E EPS. His fair value estimate was $72/share. While Berkshire is unlikely to pursue an immediate acquisition spree, the deal opens the door for TMHC to become a larger consolidator over time. Alex also notes rising sector M&A, including Dream Finders attempted hostile bid for Beazer Homes, which he thinks would likely need to move closer to 0.8-0.9x book value to succeed.

Stock Picking: #1 ranking for 60 straight months

New Constructs highlights a milestone 60 consecutive months of #1 rankings across multiple SumZero categories, underlining the consistency of their stock selection record. They are currently top in Consumer Discretionary and Industrials, alongside strong showings in Value, Large Cap, Micro Cap and Healthcare. New Constructs attributes this track record to their proprietary Robo-Analyst AI, which analyses financial statement footnotes and MD&A disclosures to calculate Core Earnings, a proven superior measure of earnings. Their performance evidence also extends beyond the rankings: since Jan 2021, New Constructs’ Focus List Long portfolio has outperformed the S&P 500 by 20%, while their Short portfolio has outperformed shorting the index by 60%. The three indices that they have developed with Bloomberg’s Index Licensing Group have also all outperformed the S&P 500 over the past five years.

Investor Idea Event highlights several compelling Shorts

Revelare hosted a Buyside Event in London where short theses were shared for companies including: 1) Associated British Foods - Primark is caught in a competitive “no man’s land” and is being squeezed by Shein, Vinted and LEFTIES. 2) CSG - trades at peak earnings, driven by unsustainable, high-margin spot-market ammunition sales to Ukraine and its true revenue visibility is much lower than its headline backlog suggests. 3) IWG - the presenter questioned the company’s highly touted transition to a capital-light management / franchise model; sees the business as plagued by poor disclosure and aggressive accounting. 4) Vestas Wind Systems - utilities moving services in-house puts margins at risk and Chinese competition challenges a peak multiple.

South Africa: Yield curve repricing

South Africa’s yield curve has partially recovered from the March oil shock, which lifted yields across maturities, with the 10-year moving from around 8.1% at the late-February low to 9.4% at end-March, before easing back to around 8.65%. The curve remains materially below the old stress regime, but it is now higher and flatter because the short end has repriced more aggressively than the long end, as markets moved from pricing around 50bp of SARB cuts to roughly 75bp of hikes for the rest of 2026. The March shock did not undo the fiscal-credibility gains that drove the earlier rally, but it has made the route to further long-end compression narrower and more stretched out. The fiscal-credibility narrative remains supported by the stronger 2025/26 fiscal outturn, resilient revenue, lower-than-budgeted debt-service costs and Moody’s positive outlook. Looking ahead, Peter Montalto now sees the 10-year SAGB ending 2026 around 8.5%, from 8.0% before the US-Iran conflict.

US Treasury yields head into a new higher range

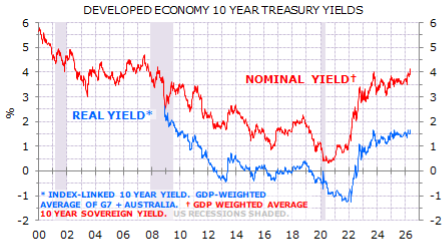

Gerard Minack points out that the post-GFC era of low rates is over: long-end rates are now back in the pre-GFC range (Exhibit 1). Gerard says they will remain high as colossal budget deficits collide with rising investment spending and sticky inflation. Structurally high real rates increase the risk of a fiscal blow-up. AI will add to upward pressure on real yields if it lifts trend growth rates. The increase in yields pre-dated the Gulf conflict, but the conflict accelerated the rise in both expected inflation and real rates. Higher rates will be a big problem for western world public finances. Political populists have little appetite for pre-emptive budget repair, so it seems only a matter of time before a developed economy faces a public sector debt crisis.

US: Warsh’s natural bias

In the last week markets have moved to peg the Fed for about 28bps of hikes in the next year, a substantial shift from the 1-2 cuts priced in late February. Warsh assumes the Chair with a challenge to his natural bias – higher productivity via AI implying stronger GDP growth potential (but less inflation and hence need to hike), weak jobs markets but immigration arguably keeping the U/E rate down (which should point to rate cuts), a tighter and smaller Fed balance sheet (that implies rate cuts to offset) and different measures of inflation (trimmed mean over core PCE which conveniently is lower and implies rate cuts). This set of biases imples that Warsh is more of a cutter than a hiker. While the markets peg the first Fed hike in March 2027, Craig Ferguson thinks that the Fed will get an inflation shock in the next 3-4 months that leads to them hiking in Q3.

Consumer Discretionary

ROST exceeded very high expectations delivering an impressive 17.0% comp with the majority driven by traffic and EPS of $2.02 - ahead of Chuck Grom’s Street high $1.95 estimate and guidance of $1.60-$1.67. Even more impressive, most of the uptick in transactions is coming from new customers thanks to improved branded merchandise, better in-store experience and refreshed marketing initiatives. This should improve confidence in ROST’s ability to “comp-the-comp” later this year despite difficult comparisons. Near term, Chuck raises his 2Q26 SSS estimate to 7.0% with EPS of $1.90, while FY26 and FY27 EPS increase to $7.80 and $8.75, respectively.

Communications

The latest reporting suggests SPCX is targeting a ~$1.75trn valuation, which would make it the largest IPO in history, but New Constructs argues the implied expectations are “out of this world”, with investors materially underestimating execution risk, competitive intensity and capital requirements. Their report highlights rapidly falling Starlink ARPU, misleading non-GAAP reporting and weak internal accounting controls, alongside governance concerns including minimal voting rights for IPO investors, extensive related-party transactions and potentially significant future dilution. They also note that ~80% of IPO proceeds are already earmarked for debt repayment and other obligations, while customer concentration risk remains elevated. New Constructs' reverse DCF analysis suggests the proposed valuation implies SPCX will ultimately generate both the highest revenue and highest NOPAT of any public company; sees >70% downside if revenue growth merely tracks historical rates.

CSN: Bridge loan supports a show me credit

Materials

EM Spreads maintains an Opportunistic Overweight on CSN bonds, arguing the market is pricing the credit closer to a distressed recovery trade than a conventional single B credit, despite no near-term liquidity event emerging from 1Q26 results. While leverage and FCF remain weak, a new US$1.2bn bridge loan materially improves funding visibility and reduces refinancing pressure, buying management more time to execute on deleveraging. The key catalyst remains tangible progress on asset monetisations, while EM Spreads sees the best risk reward in the CSN 4.625% 2031s and CSN 5.875% 2032s. The argument for the 2031s is more defensive, based on shorter duration and slightly better downside control, while the 2032s are the higher upside expression for investors willing to accept modestly more duration in exchange for incremental spread and carry.

Telfer vs. KCGM: The revival of Aussie icons

Materials

While the market remains cautious on Northern Star Resources given ongoing KCGM execution risks, potential cost overruns and weak near-term news flow, the company is nearing completion of a transformational ~A$1.8bn mill expansion to 27Mt/yr, part of ~A$5bn total investment into KCGM across FY22-FY28, which could ultimately restore production towards ~0.9Moz/yr by FY30. However, with management still needing to rebuild investor trust, GMR retains a Hold rating on NST. In contrast, they are more constructive on Greatland Resources, which is still in the early stages of reinvesting in Telfer / Havieron, with ~A$2.8bn of potential capex through FY32 supporting a pathway back towards ~0.4-0.5Moz/yr production by the end of the decade, alongside exploration upside at SLC and West Dome. Given the scarcity of >300koz/yr gold assets, GMR believes Telfer could become a strategic bolt-on acquisition for peers seeking scale in Australia.

Technology

CORZ moves sharply higher in Arete’s AI infrastructure rankings following a major expansion in its long-term power roadmap, with them now modelling 3.6GW of IT load and $6.3bn of NOI by 2032 - up from prior estimates of 1.9GW and $3.7bn, respectively. Arete argues demand for AI compute remains “off-the-charts”, while CORZ is becoming increasingly attractive to hyperscalers through the expansion of its Pecos and Muskogee campuses into gigawatt-scale AI data centre sites. Importantly, the company has leveraged its existing CoreWeave contract into $3.3bn of financing, giving it sufficient capital to begin pre-building new facilities before signing additional leases, which Arete views as a key competitive advantage. With leasable power expected to nearly triple over the next few years, Arete raises their TP to $55 (100% upside) and now ranks CORZ alongside Applied Digital as a top pick in colocation infrastructure.

How should you think about AI revenue exposure?

Trivariate argues investors need a more systematic way to think about AI revenue exposure, with the S&P 500 increasingly behaving like a giant AI ETF. Using an LLM-based process, they identified 262 US companies with meaningful AI-linked revenue across 13 business categories. They then analysed the daily beta-adjusted returns of those categories and found that many were highly correlated. Principal Component Analysis helped quantify this common factor structure, while correlation-based clustering consolidated the 13 categories into 6 broader AI-revenue groups that better capture both business exposure and how the stocks have actually traded. These 6 categories are: 1) Utilities / Datacentre REITs, 2) Datacentre Buildout, 3) AI Platform, 4) Vertical & Edge, 5) Services & Integration, 6) Memory and Semiconductor Capital Equipment. To access the full report and investment conclusions including long and short ideas contact us below.

Technology

Following publication of its FY25 universal registration document, Iron Blue increase their CAP score +3pts to 30/60 (newly top decile and fertile grounds for shorting). This higher score reflects: 1) Increased stripped out costs (both restructuring and share payments). 2) Higher cost capitalisations. 3) Iron Blue’s conclusion that CAP may have fair value adjusted downwards the software on WNS’s balance sheet. 4) The dropping of organic growth as an alternative performance measure in a year of material acquisition revenue contribution. They also note that in FY26 Grant Thornton will replace PwC as one of CAP’s auditors - PwC had been in place for nearly three decades.

South Africa: Fiscal monitor

The fiscal year finished strong, with many of the key sources of upside and flexibility that Peter Montalto identified post-Budget materialising. Revenue was stronger despite weak growth. This left the primary surplus at 1.1% of GDP – in line with Peter’s view and above NT’s 0.9% Budget estimate. The key point is that the fiscal golden threads have been reinforced, if not strengthened, though this might well only translate into a slow ratings upgrade cycle. Peter sees the primary surplus at 1.5% of GDP in 2026/27, rising to 2.2% in the outer year. The usual caveats remain. Spending quality is still markedly lower than optimal. That the year-end fiscal strength reinforces the case for an S&P ratings upgrade later this year, in Peter’s view. NT is likely to maintain an (overly) conservative line however through the upcoming spending round to the MTBPS – focusing (perhaps too much) on geopolitical risks into the fiscus – again to be surprised to the upside later.

China’s asset revitalisation: An unanticipated growth boost?

In a 24-page special report, Dinny McMahon discusses the “asset revitalisation” measures that could help end the problem of local government austerity. Over the last few years, China’s local governments have significantly ramped up the amount of revenue they generate by leasing state assets and selling concessions – known as “revitalising” assets. This “asset revitalization” has become a major source of income for a handful of provinces, materially improving their fiscal conditions. Chongqing, the leader, funded 15.1% of provincial general expenditures last year from such activities, up from only 6.8% four years earlier. For China’s financially overstretched provinces, “asset revitalisation” is emerging as a much-needed new channel for expanding revenue. It stands to have a potentially transformative impact, creating an unprecedented opportunity for local authorities to repair their finances, and opening the door to an unanticipated boost in growth over the next couple of years.

US: Higher oil and rates, lower equities

David Woo argues that the market has got ahead of itself in reverting the move in 2y breakevens. His short-term market bias is: higher oil - lower equities - higher rates - neutral dollar. (1) Higher oil: Whether we will see resumed fighting or not, the two sides will not reach a deal anytime soon. Iran is not about to capitulate to US demands with support from Russia and China. (2) Lower equities: As the market starts to look beyond Q1 towards Q2, the high oil price will weigh more on growth expectations. European stocks are particularly at risk given their dependence on energy imports and lack of exposure to technology. (3) Higher rates: AI is inflationary in the short-term. The war is driving up prices from energy to crops. Fixed income investors are trying to ignore the war. (4) Neutral dollar: Trump wants to hit the EU with a 25% auto tariff, which the Supreme Court may prevent.

UK: The next PM

It is unlikely the factions within the Parliamentary Labour Party (PLP) will be able to vote on one candidate, so the election would be decided by the Labour Party’s electoral college (1/3rd MPs, 1/3rd Trade Unions, 1/3rd party members) between the two candidates selected by the PLP. The main candidates include Wes Streeting; Angela Rayner, the most popular of the Soft Left candidates; Ed Miliband, who is the most likely candidate should Rayner decide not to run; and Andy Burnham, who would need to be elected as an MP to be able to run. The current paralysis is bad for the Gilt market due to the likelihood that it pushes borrowing needs up over the coming months due to higher gilt yields, energy subsidies and the defence budget black hole. The potential timeline for election of a new PM is between 2 and 4 months from today.

Technology

Infineon Technologies AG was presented by a PM at a Revelare event as a long idea with ~50% upside to a €75 price target. The stock trades at ~16x 2027 EPS and ~12x 2028 EPS, below its 10-year median multiple of ~19x. The thesis rests on two tailwinds: analog recovery and AI datacenter demand. Infineon’s industrial and automotive businesses are rebounding, while €800–900M of annual underutilization charges should normalize, driving ~600bps gross margin expansion. Simultaneously, denser AI server racks require advanced power semiconductors, where Infineon leads across silicon, GaN, and silicon carbide. AI revenue is expected to grow from €700M last year to €1.5B this year, with additional upside potential. Gross margins could rise from ~17% to ~25% over 2–3 years, supported by higher-margin AI products and cyclical recovery.

Consumer Discretionary

Despite near-term margin pressure, DFH trades at only 7.5x 2026 earnings and 1.1x book value, well below peer averages. Analysts maintain a fair value estimate of $25 per share, implying significant upside potential. They have the second highest ROE in the sector out of the 17 builders Housing Research Center follows. The stock is trading at $13.02 and peaked at $43 two years ago. They have grown nearly 5x in the past 6 years more than any other builder and recently made a bid to acquire Beazer homes (BZH) at 0.5x book value. That would allow them to grow another 50% in 2027. They should make EPS of $2.00 in 2026 and $3.00 in 2027.

Consumer Staples

Sprouts Farmers Market reported encouraging 1Q26 results, reinforcing QuoVadis Research’s bullish stance. Revenue, same-store sales, margins, and EPS all modestly exceeded company guidance and Street expectations, suggesting management has regained control after the sharp slowdown experienced in 2H25. The company also deployed all 1Q26 free cash flow toward share repurchases, buying back 1.9M shares at an average price of $73.68, with QuoVadis modeling $500M in buybacks for full-year 2026. While guidance was largely maintained, the EPS outlook was slightly raised, signaling improved visibility. At just 13x P/E and 8x EV/EBITDA on consensus 2026 estimates, the stock undervalues Sprouts’ strong ROIC-driven growth and favorable risk-reward profile.

Healthcare

MDC Financial Research’s Event-Driven Legal℠ Investment Research service is closely monitoring Sotera Health Company's (SHC) ongoing EtO litigation in California, Georgia, and New Mexico. A key Summary Judgment Hearing related to the first group of eight Bellwether Cases in California is currently scheduled to be held May 27 - 28, 2026. A favorable Ruling could relieve Sotera from this initial set of Cases and strengthen its position against the 114 total plaintiffs (as of April 1, 2026) alleging harm from Sotera's L.A. area EtO facilities. MDC will attend this Hearing and provide timely insights.

Technology

JNK Research showed ROHM and VSH entered earnings with supply tightness already visible across power and passives. Its April-May Analog Tracker flagged pricing increases across close to 95% of products, while book-to-bill improved from 1.06 to 1.10. ROHM print showed that with FY26 still under-allocated and FY27 Q1 likely to snap back double-digit QoQ on SiC mix and capacity additions. Commentary on discrete SiC mix and FY27 capacity reads across to ON Semi and WOLF. VSH print provided the cleanest US-listed read on the VICR shortage, with Q4 backlog close to 5.1 months and book-to-bill near 1.2.

Europe: Uncontrollable hiccups

Niall Ferguson expects euro area headline inflation, measured by the harmonised index of consumer prices, to peak near 3.5% in late 2026 or early 2027 and to return to 2% in 2H2027. This is a higher peak than consensus and a longer return to target than in the European Central Bank’s adverse scenario. The return to 2% inflation was never sustainable. Imported disinflation from Chinese manufactured goods had been masking broad but shallow inflation in domestic services, and the current shock now arrives with no disinflationary buffer. Accordingly, Niall expects the ECB to hike rates by 50 bps by year-end. His views on US and EU rates and inflation translate to a minimally stronger euro than the market is pricing; Niall sees the EURUSD spot price at 1.178 and the one-year forward at 1.193. Europe’s second inflation shock in four years will prove less acute than the first but harder to shake.

Copper: Lack of supply growth vs rising inventories

David Radclyffe's copper coverage totals ~63% of global mine production. Copper supply continues to wrestle with many legacy headaches from 2025, mixed with the Iran conflict and its implications for diesel and sulphuric acid supply. There is therefore downside supply risk. However, the current oil disruption has implications for global growth and copper demand. Worryingly, David points out that copper inventories are rising rapidly. His coverage universe implies 0.9% annual contraction in refined copper supply in 2026, following a strong 2025. Weak supply growth for 2026, even with moderate demand growth, is at odds with strongly rising terminal market inventories, now at 1,267kt, adding to price risk. Copper is a crowded long trade, with caution warranted. The sector is not particularly cheap at spot 1.6x P/NPV10 and 9x EV/EBITDA. Antofagasta PLC is cut to HOLD. Preferred stocks include Lundin Mining Corp, KGHM Polska Miedz SA, Ivanhoe Mines Ltd, Grupo Mexico SAB de CV, Hudbay Minerals Inc and Teck Resources Ltd.

Senegal: Ongoing talks but as yet no IMF programme

Maximilian Hess observes that Senegal is in the throes of a financial crisis caused by the revelations of large amounts of ‘hidden’ debt contracted by the previous government, that has seen an additional 20-30% of borrowing as a percentage of GDP uncovered. The government has leaned on its monetary union, WAEMU, to meet its debt service with local currency issuance. While the WAEMU market has demonstrated surprising liquidity, Senegalese and regional banks are approaching (or have met) their regulatory limits for state debt. Senegal is negotiating with the IMF for the resumption of a USD 1.8 billion facility suspended in October 2024. The Fund noted strong GDP growth, better-than-expected primary and current account performance, and moderate inflation, in 2025, though it expects Senegal’s fiscal and macroeconomic picture to materially deteriorate in 2026. The IMF said that ongoing talks are “complementary to a programme” but are primarily on structural reforms and capacity development.

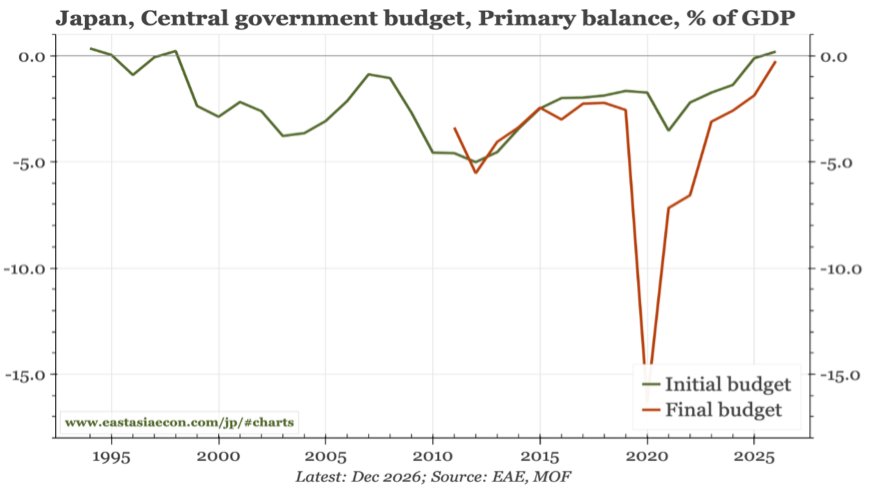

Japan: Yen under the cosh

The yen breached Y/$1.60 on Thursday and JGBs are under pressure again after Trump signalled that a prolonged blockade on the Strait of Hormuz may be necessary. Ironically, Graham Turner points out that it may not be the inflation numbers that undo the Japanese bond market: the data had been benign in recent months and the BoJ has time on its side and can wait. The problem is the Japanese Government’s insistence that it can hike defence spending, without compromising on other areas of spending. Markets had been persuaded by the new prime minister’s claim that a "responsible expansionary fiscal policy" could work. Ironically, the trade and manufacturing data in Japan suggests that the Takaichi Government can be more prudent: it can afford to accommodate higher defence spending without resorting to more borrowing. It just chooses not to. The long end of the JGB market will react before too long.

Financials

Anas Abuzaakouk (CEO since Aug 2017, joined 2012) bought 30,000 shares at €149, spending €4.5m. He has a great track record based on his 21 prior purchases. This is his single largest purchase and the highest price he has paid. He last bought in Oct 2025 at €108. Smart Insider has ranked the stock several times based on his prior activity, with the majority of those signals proving to be very timely. They are ranking the stock +1 (highest rating).

Technology

JNK’s analysis suggests LSCC is tracking ahead of guidance, with Q1 supported by strong bookings extending into 1H27 and a book-to-bill above 1.2. However, this strength is partly driven by Greater China customers pulling forward demand ahead of a ~15% price increase implemented in March 2026, with regional shipments running ~25% above Q4 levels. Lead times remain elevated at over 26 weeks, constrained by substrate and packaging rather than wafer capacity. With servers accounting for ~60% of revenue and exposure to Intel and AMD platforms, the company also benefits indirectly from AI-related demand. JNK's analysis suggests pricing can support growth even if volumes soften.

Materials

GMR cuts FCX to Sell following further production downgrades at Grasberg, with the ongoing impact of the 2025 “Mud Rush” now expected to persist through 2027. They estimate cumulative production losses of 952kt of copper, 1.5Moz of gold and 6.6Moz silver over 2025-2029, equating to $19.2bn of lost revenue at spot prices (or $15.4bn on GMR’s base case price forecasts). GMR has cut 2026/27 EBITDA forecasts by 15-21% and reduced its valuation by 27%, arguing the recent share price reaction underestimates the severity and duration of the impact. With risks of further downgrades and rising capex, downside remains.

Identifying stock swaps within your portfolio

Mill Street's Swap Shop report reflects frequent interest from equity portfolio managers in using their MAER model (the Monitor of Analysts’ Earnings Revisions) to identify problematic low-ranked holdings and provide high-ranked substitutes that preserve overall portfolio allocations. The screens take advantage of MAER’s strong intra-sector or intra-industry ranking performance to allow managers to stay not only within a benchmark universe but also identify stocks within specific industries as potential swaps to keep sector / industry weightings consistent. This month they include swap screens for Global Technology / Communication Services stocks and Global Energy / Materials sectors stocks to capture the key topical themes of Tech / AI and commodity prices. Also included are the regular screens for the S&P 500 universe and their European stock universe. Click here to access the report.

Global liquidity will not bottom before 2027

Michael Howell points out that the global liquidity cycle peaked in Q3/2025 and is not slated to bottom before 2027. He has pared back risk exposure as the underlying currents driving liquidity lower will ultimately dominate geopolitical twists and turns. Economic activity is still slated to recover through 2026, even if the Iran conflict extends. Global liquidity looks more vulnerable than the broader economy. It was already falling pre-conflict, and higher oil prices, bond volatility (MOVE), and a stronger USD have further dented it, with the Global Liquidity Index (GLI™) falling to 44.1 in March from a December peak of 56.1. Bond market moves confirm this deterioration in global liquidity. Yield curves are inflecting lower and falling term premia highlight a demand for safety. Gold, meanwhile, is underpinned by China’s ongoing ‘monetisation’. Higher gold must translate into higher oil and other commodity prices.

The best 3 space exploration stocks to buy in 2026

Technology

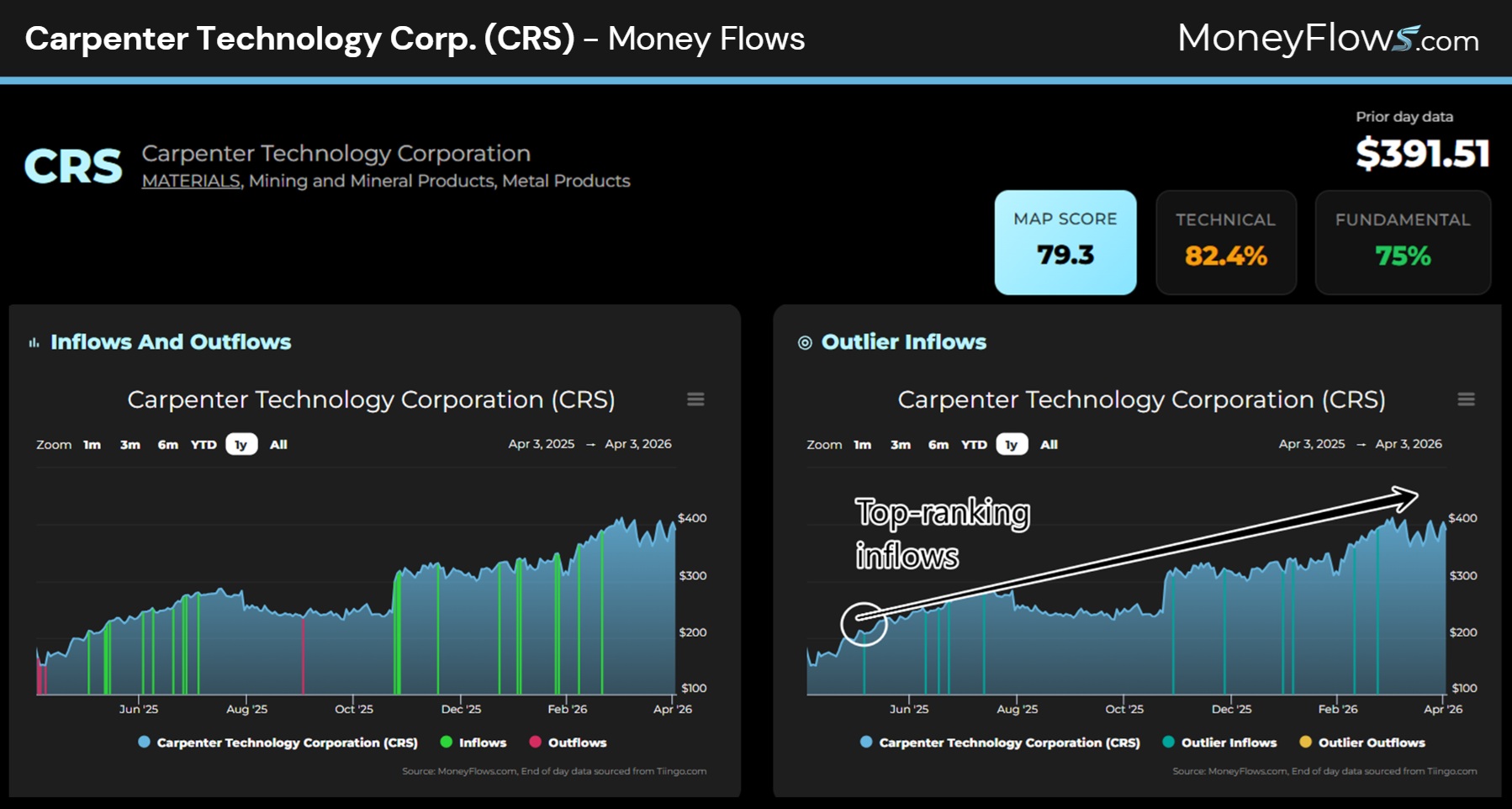

The space economy is a major structural growth theme, expected to expand from ~$614bn in 2024 to >$1.8tn over the next decade, with opportunities extending beyond rockets into the broader infrastructure stack. MAPsignals’ edge lies in identifying institutional inflows before the narrative becomes consensus, using its “Big Money” framework to find winners early. For example, Teradyne was flagged at ~$90 last June and has since surged to ~$342 on sustained inflows, with further upside anticipated. Applying the same process, they also highlight Carpenter Technology and Palantir as beneficiaries of the space buildout, supported by persistent institutional buying - including “non-stop” inflows into Carpenter. Tomorrow’s leaders are found by following the flows, not the headlines.

Consumer Staples

Following publication of its FY25 annual report Iron Blue lifts their RKT score +2pts to 28/60 (top quartile / fertile grounds for shorting). This reflects 1) 7-year high stripped out restructuring charge; 2) another spike lower in balance sheet trade spend accruals; 3) reduced inventory and bad debtor impairment provisions; 4) various additional risks related to NEC litigation, HS compensation changes and UK Suboxone civil proceedings within RKT’s contingent liabilities disclosures; 5) another increase in KPMG’s non-audit fees; and 6) the 14% discretionary upward adjustment to the CEO’s annual bonus to reflect strong share price performance (which compares with shares -14% FY26 YTD).

Mining equities in turbulent markets

The US-Israeli war with Iran and oil shock has resulted in some of the most volatile markets of recent times. Higher oil prices are clearly inflationary; however, the larger short-term risk for the miners is arguably the supply of liquid fuel. Slowing global growth could erode copper demand; the copper sector P/NPV10 and +1 year P/CF is trading close to previous tough levels with a spot FCF yield of 5.2% being attractive. Gold equities are still attractive with the market imputing lower spot prices today. The shares are cheap on a cash flow basis with a 6.9% spot FCF yield. Gold sector margins are still robust with better balance sheets compared to peers. Copper and gold equities have corrected, and value opportunities have emerged. Preferred coppers are Antofagasta PLC, Lundin Mining Corp and Ivanhoe Mines Ltd, whilst least preferred are First Quantum Minerals Ltd and Southern Copper Corp. Preferred golds are Barrick Gold Corp, Agnico Eagle Mines Ltd and Kinross Gold Corp.

China: Tapping SOE profits

Dinny McMahon notes that in a recent explainer, the finance ministry (MoF) revealed that last year it hiked up SOE profit remittance ratios, as he anticipated. In China wholly owned SOEs are obliged to remit a portion of their profits to the government. Most non-financial, centrally-owned SOEs are classified into one of five categories depending on their business line, subjecting them to profit remittance rates ranging from 0%-25%. In 2025, MoF merged Tier-1 and 2 SOEs into one group and raised their remittance ratio to 35%. This covers China Tobacco, the three major telecommunication and petroleum firms, and electricity utilities and grid firms. MoF also raised the profit remittance ratio for what had previously been Tier-3 firms – which cover SOEs operating in competitive sectors like mining, transportation, and trade – from 15% to 30%. It raised the ratio for Tier-4 firms from 10% to 20%. Dinny wonders if local governments will follow suit and ramp up profit remittance ratios for locally-owned SOEs?

Technology

The semiconductor distribution channel is posting ~40% Q/Q revenue growth in 1Q26, but the composition tells a more nuanced story than the headline suggests. JNK's supply chain checks show 800G optical module demand at a 2-year high, with all global Tier 1 makers pulling orders and Broadcom Tomahawk 6 extending the cycle into 2H26; simultaneously, the ASIC-to-GPU semi revenue mix is shifting from 80/20 towards 60-70/30-40, positioning MRVL as the most direct beneficiary. On the consumer side, Apple/iOS is outperforming seasonal patterns (+10% Q/Q vs. flat expected in Q4), though component buyers stocking ahead of tariff increases are raising H2 inventory correction flags. The divergence between data centre acceleration and consumer pull-in risk shapes the setup for H2.

Financials

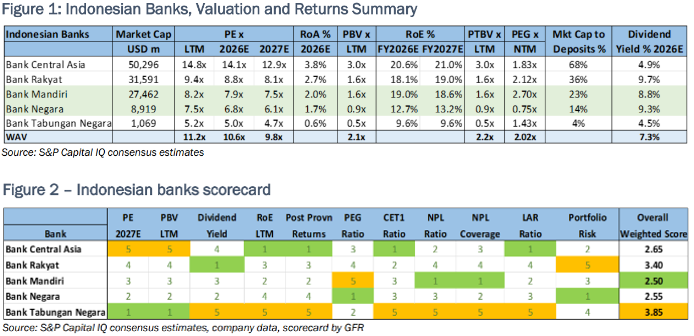

Victor Galliano upgrades Bank Mandiri and Bank Negara to Buy on better-than-expected credit quality, attractive valuations and signs the government is reining in market-unfriendly policies. Both banks screen well on fundamentals (fig 1) and in his proprietary scorecard (fig 2). Mandiri is his top pick, driven by strong credit quality and solid returns, supported by mid-ranking valuations. Low NPLs underpin a declining cost of risk and improving post-provision returns, while returns relative to valuation are very attractive. With PBV near a three-year low and bond yields elevated, he sees scope for a valuation uplift if yields ease. Negara’s valuations are close to deep value and, although return trends remain uninspiring, it has the lowest MSME exposure of the peer group and second best NPL coverage.

Technology

The group's competitive moat is anchored by three mutually reinforcing advantages: 1) a proprietary, cloud‑native payments infrastructure with direct integrations into 50+ national payment systems across the world, creating a durable cost leadership position that compounds with scale; 2) a Mission Zero pricing philosophy, that continuously reinvests operational efficiencies and scale benefits into lower prices, driving organic volume growth and deepening customer stickiness; and 3) a growing platform business, which is transforming potential competitors into distribution partners, expanding the company's netting pool and lowering unit costs across the entire network. 2Xideas forecasts 14.7% revenue CAGR and 15.9% underlying income CAGR to FY32E. Assuming a conservative 20x exit NTM P/E, this supports ~17.5% annualised TSR.

Europe: Uncontrollable hiccups

Niall Ferguson expects euro area headline inflation, measured by the harmonised index of consumer prices, to peak near 3.5% in late 2026 or early 2027 and to return to 2% in 2H2027. This is a higher peak than consensus and a longer return to target than in the European Central Bank’s adverse scenario. The return to 2% inflation was never sustainable. Imported disinflation from Chinese manufactured goods had been masking broad but shallow inflation in domestic services, and the current shock now arrives with no disinflationary buffer. Accordingly, Niall expects the ECB to hike rates by 50 bps by year-end. His views on US and EU rates and inflation translate to a minimally stronger euro than the market is pricing; Niall sees the EURUSD spot price at 1.178 and the one-year forward at 1.193. Europe’s second inflation shock in four years will prove less acute than the first but harder to shake.

Technology

Electronic-grade solvent allocation stopped for non-contract customers across Asia as of early Mar 26. No spot supply is available at any price in Taiwan, South Korea or Singapore. Force majeure from Formosa Petrochemical and PCS, combined with cracker cuts at LG Chem and Lotte Chemical to 54-73% utilisation, pushed naphtha-derived feedstock prices ~30% higher. The disruption spans legacy analog, DRAM, NAND and leading-edge logic with no node insulated. Conductive carbon black, a separate petroleum-derived passive component input, is developing a parallel shortfall into a supply chain already running at near-80% utilisation. China based foundries serving MPWR and STM are the base case for 2Q26 impact. Click here to access JNK’s note.

Real Estate

MRL sees a double upgrade from Smart Insider, moving to +1 (highest rating) following two notable insider purchases. The initial upgrade was driven by Senior Officer Fernando Ramírez Baeza (€152k at €14.05), a larger-than-usual buy into strength from an insider with a strong track record. This was followed by a €1m purchase from long-serving Non-Executive Fernando Ortiz Vaamonde - the largest of his 5 buys, at the highest price he has paid and his first since 2020.

Consumer Discretionary

John Zolidis’ investment case is based on a positive inflection in same-store sales producing valuation expansion as investors give more credit to unit growth and the longer-term opportunity. He believes this thesis remains intact as comps improved to -1.4% in FY25 (vs. -5.1% in FY24) and have turned positive in early FY26, with Q1 likely >2%. While the recent >10% share price drop reflects macro concerns and weak transaction trends (-6.4% in Q4), John views this as partly intentional, driven by ~10% price increases and a shift towards higher-income customers. This mix shift should support higher gross profit per ticket despite lower traffic. With the shares trading at 8x P/E and 5x EV/EBITDA (FY26 estimates) and a 9% FCF yield, ASO is a “bargain”, with an eye towards the upcoming analyst day as a near-term positive catalyst.

Nickel may yet surprise

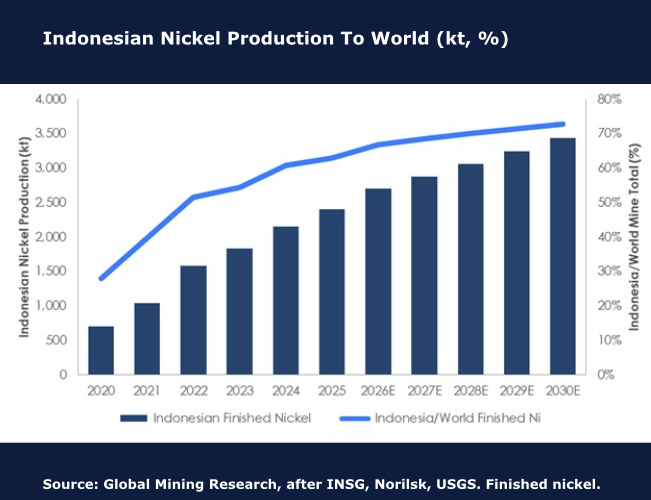

Recent events brought spot nickel up to ~US7.80/lbafterabriefreturnto US8.00/lb. The three major developments that led to this are the Iran war, a decision by the Indonesian government to dramatically cut thermal coal mining permits from 790Mt to 600Mt, and another decision to cut laterite nickel mining permits to 260-270Mt versus 2025 at 379Mt. GMR has calculated an annual nickel demand growth rate at 6.2% CAGR over the last decade, but the unceasing volumes from Indonesia (see chart) have been the issue. New changes may see parts of the global nickel cash cost curve move by ~US$1.50/lb. If laterite ore is really cut back heavily, then the price impact should add to that, but very large inventories could limit substantive price moves for some time. This is all potential; good news for producers like Vale SA, Glencore PLC or MMG Ltd. It’s too late for the Cuban producers where the lack of fuel is triggering closures.

US: The case for 10% unemployment

Paul Krake’s latest report rebukes the argument that AI-driven job displacement will be absorbed by new industries generating new work. It is an argument that Paul claims is taken seriously in policy circles, investment committees, and corporate boardrooms, yet it is deeply flawed. The hiring data already shows this, with the hire rate having falling 29% since the post-pandemic peak yet GDP has grown by 8% (see chart). AI is amplifying the pattern that labour is not required for growth. Just a 1 in 10 displacement of knowledge workers, which represent 45% of the US labour force, is enough to push unemployment towards 9% without a recession. Paul claims that the frameworks used to detect labour market stress are not built for an economy where growth and hiring decouple permanently. By the time the unemployment rate confirms what the hire rate has been signalling since 2022, the adjustment will have been compounding for a decade. 10% unemployment in the years ahead is not a tail risk, it is the base case.

The Euro’s extremely important juncture

The Euro’s (€1.1416) monthly chart shows a breakout from a 17-year Down-channel, with the currency trading as high as €1.2083 in January this year, up 27% from the Sep 2022 low. Chris Roberts comments how a sustained breakout from the channel, following the 14-year, 40%+ fall in 2008-22, could potentially be very bullish. The near 6% fall from the recent high has taken the Euro back to the rising 20-month WMA and the 9-month RSI back to Neutral 50. Chris is 40% long from €1.1572 and would look to add on a break above the Jan high. His stop stays at a daily close below €1.0954.