Industrials

MYST highlights a short thesis on ANDG, whose shares have risen from a $16 IPO price in Dec 25 to c.$37. The near-term catalyst is a major lockup expiry on 15th Jun, when c.99m shares become available vs. current outstanding shares of c.13m, creating a potential “meaningful amount of supply” as 300+ US partners look to monetise up to $4bn of stock. Fundamentally, ANDG relied heavily on price increases heading into the IPO, but customers already appear to be pushing back. AI is also seen eroding pricing power, as Big Four firms automate workflows and move down-market while AI-native start-ups compete at lower price points. Tax Receivable Agreements that distort reported cash flow are another underappreciated element of the short thesis. TP $25 (30% downside).

Technology

The market has been spooked by ORCL’s AI infrastructure spending, but Richard Windsor thinks the economics may be better than feared. Q4 revenues and adjusted EPS beat expectations, but shares fell after-hours as the company guided to $70bn of investment this fiscal year. The bond market is also flashing caution, with ORCL’s CDS widening to 198bp from 43bp in Sep 25. However, Richard estimates revenue per GW at $15.8bn, based on ORCL's incremental AI/cloud capacity and cloud revenue growth, far better than OpenAI and other neo-clouds are managing to produce, implying an 18% five-year IRR on a Grace Blackwell-based build. Strong AI investment returns could drive upside to medium-term EPS estimates, while the stock's 22x FY27 and 16.5x FY28 PER look reasonable against forecast EPS growth of 18% in FY27 and 35% in FY28.

What are gold miners doing with all of their cash?

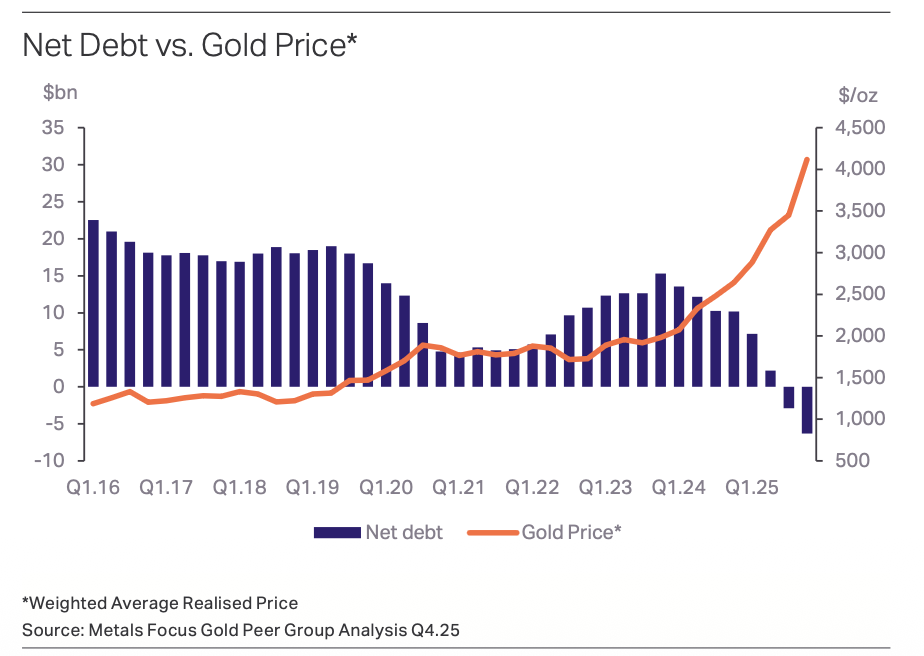

Driven by surging realised gold prices, the group of gold miners tracked by Metals Focus generated a massive $25.8bn in free cash flow in 2025. Rather than repeating the reckless expansion of past commodity cycles, management teams are demonstrating strict capital discipline. A significant portion is channelled into balance-sheet repair, transforming a $15.3bn net debt position into a $6.3bn net cash surplus. Reinvestment back into operations has driven total capital expenditure to $682/oz, alongside increased exploration spending to maintain a stable twenty-year reserve life. Host governments took a 33% effective tax rate, whilst quarterly dividends surged threefold to $3.0bn. Despite this historic financial strength, sector valuations remain subdued at a 5.4x EV/EBITDA multiple, offering a compelling opportunity for equity investors to buy these highly disciplined, cash-rich producers.

Ripples of risk-off

Murray Gunn wrote about the dichotomy between the fortunes of Ripple, the cryptocurrency company, and XRP, its token. He pointed out the booming company that has been securing lucrative and high-profile contracts, yet the price of XRP has been declining. Another Bitcoin bust beckons, as the iconic cryptocurrency was declining in the next wave of its ongoing bear market since its peak last year. Bitcoin also sports at least one head and shoulders top pattern which could give it even more bearish implications. Murray pondered whether the crypto slump was a subtle sign that risk appetite was waning, and it might now be finally feeding through into the stock market with the S&P 500 down over 3% last week. Don’t be surprised to hear and read about people attempting to “buy the dip.” And when the stock market struggles to recover, as he suspects, expect increasing panic to ensue.

How much of a problem is the Polish budget?

Jonathan Anderson points out that broad macro conditions are still very favourable for Poland. On the external front, Poland continues to gain European market share with outperforming exports, which in turn keeps the external economy in balance and the zloty stable. The domestic recovery is also on track, with strong credit growth, durable spending and corporate earnings momentum at home. The equity market has arguably already outrun the underlying story, but this is true for the rest of the emerging European region as well; the one imbalance that stands out in Poland is the dramatic widening of the fiscal deficit, driven by higher defence and social spending. This can't last over the long run, but with moderate overall debt levels and low external exposures there's still not a big impact on macro variables. The only market where budget imbalances are already showing up is sovereign dollar/euro bonds, where favourable yield gaps are all but disappearing.

China: Externally driven inflation

Paul Cavey says that the rise in China’s producer price index (PPI) that continued in May is of macro significance: it is pushing up industrial sector earnings, and the GDP deflator will likely turn positive in Q2. But it is difficult to find signs of domestically generated inflation that would suggest a real upturn in the economy. PPI inflation did ease MoM in May, but the headline YoY rate climbed to 3.9%, the highest since mid-2022. As would be expected, the driver continues to be upstream commodity prices. The rise in energy prices is also being reflected in CPI, with a 20% YoY rise in fuel costs pushing up the transport and communication component by 5% in May. However, headline CPI was steady at 1.2% YoY. One reason was that food prices in the CPI continued to fall last month. In addition, services inflation remains weak. That reflects the state of domestic demand, though in that regard it is perhaps notable that services inflation isn't deteriorating further.

Japan: Yen under pressure, but data is encouraging

Graham Turner says that the prospect of a rate hike at the FOMC meeting in June casts a harsh spotlight on the Bank of Japan: the BoJ will meet earlier next week, and unless it agrees to tighten policy too, the yen is likely to plumb new lows against the US$. For the Bank of Japan, there is no obvious pressure to hike, as inflation has been well-behaved. The y/y for the Nationwide CPI eased to 1.38% in April. The CPI excluding food, alcohol & energy dipped to 1.06% y/y. Real wages are rising sharply, in part, because of the drop of core inflation as well as fuel subsidies. The labour market in Japan is tight. The unemployment rate fell to 2.5% in April. Total employment jumped to 68.76m, a new high, despite a shrinking population. These are encouraging trends that bode well for Japan’s response to an ageing population, particularly against the backdrop of high government debt.

Hong Kong: Hang Seng breakout

Chris Roberts examines the HSI’s (24,962) confirmed breakout from the 27-month rectangle/base, as it targets an advance to 35,000+, a new all-time high. The weekly chart uptrend high remains at 27,382, set in Oct 25. The index has now been ranging for 8 months. A weekly close above 27,800 would be viewed as a breakout from the current range, targeting a move to around 31,000. If such a breakout occurs, Chris will likely add a long HSI position. He is still long the iShares MSCI China ETF and the Shanghai Composite Index. RSI (last 42) continues to support the uptrend view, with lows being set in the 40-50 Neutral Zone since the 2024 low.

Australia heads back to the doldrums

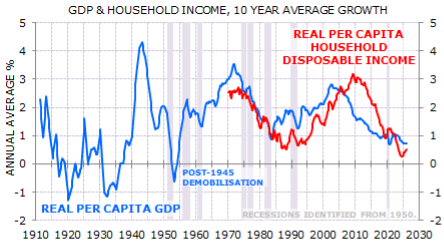

According to Gerard Minack, Australia is growing at 2.5% – not particularly strong with working-age population rising by 1.75% – but now seems set to slow. Productivity growth remains poor, so 2.5% growth created inflation pressure that the RBA had to respond to. Gerard says the economy will head back to the doldrums of a low per capita expansion. Weaker growth is a factor behind falling EPS forecasts and the prospect of modest equity returns. Australia has had a poor decade. Average per capita GDP growth was the lowest since the 1930s (excluding the post-1945 demobilisation). What matters for consumers is disposable income, not GDP. Per capita disposable income growth was lower than GDP, payback for the mining boom boost received through the prior decade. Australia’s biggest structural economic problem is poor productivity. Poor productivity reflects low capex relative to fast-growing population, so there is little capital deepening. No capital deepening means no productivity growth.

Eurozone growth risks mispriced amid hawkish consensus

The Variant Perception team examine the outlook for the Eurozone as inflation leading indicators and breadth remain elevated well above pre-Covid levels. Whilst rising service price surveys put pressure on the European Central Bank to remain hawkish to anchor inflation expectations, matching the market pricing of at least three interest rate hikes over the next year introduces substantial downside growth risks. According to the team, current market dynamics replicate the post-GFC period by overstating inflation fears and underestimating growth destruction. This structural misalignment occurs at a time when Eurozone macroeconomic breadth vs the rest of the G10 remains weak. With the trend component of the firm's tactical outlook model turning decisively negative, the underlying economic setup points toward a sharp growth capitulation rather than a sustained tightening cycle. The team express their bearish view on European growth by selling rallies in the euro.

UK credit expansion set for summer pause

Darren Winder points out that while UK household bank deposits grew at a steady 4% over recent months, a near-term deceleration in credit expansion looms. Driven by an upward revision to market interest rate expectations, quoted mortgage rates jumped from 4% to 5% in April, signalling an abrupt tightening cycle that will soften mortgage approvals and housing transactions in the period immediately ahead. This near-term moderation is expected to pull down mortgage lending growth from its recent 3.25% pace. However, the fundamental evidence reveals significant underlying consumer resilience; household bank deposits expanded by £75 billion in the 12 months to April, propelled by a 15% annual surge in cash ISAs to £475 billion. Winder expects this mortgage slowdown to be transitory, with lending growth projected to pick up as interest rate pressures ease during the second half of the year and into 2027.

Hang Seng on the launchpad

Erik@YWR argues that the Hang Seng’s sluggish start to 2026 masks a much more attractive setup, with the index described as a “coiled spring” after moving sideways for 15 years in hard-currency terms. He sees 35,000 as achievable, supported by improving fundamentals: based on YWR’s approximation of 89 constituents, earnings growth is expected to accelerate from a 6% CAGR over 2015-2025 to 11% over the next 3 years. Key drivers include 17% EPS CAGRs at Tencent and Alibaba, 6% growth from the major Chinese banks, oil-price support for energy names, 26% growth from BYD and CATL, and a recovery in property stocks. With earnings revisions turning positive, Hong Kong property prices recovering (mainland China prices stabilising) and the index on <10x 2028 earnings, Erik sees meaningful upside.

Real Estate

Craig Huber argues that the near-50% YTD fall in CSGP’s share price has created an attractive entry point, with investor concerns around AI competition and Homes.com losses now overdone. His 2026/2027 adjusted EPS estimates are above consensus at $1.40/$2.00, with revenue forecast to rise 18.0%/15.4% to $3.833bn/$4.424bn and adjusted EBITDA to reach $833.8m/$1.142bn. The group also has $1bn remaining on its share buyback programme (representing ~7.5% of current m/cap). The stock trades at 16.8x 2027 adjusted EPS or 13.9x EBITDA. If you exclude the Homes.com losses (where there is a lot of flexibility in the expense base; sees losses dropping to ~$300m this year), CSGP is trading at only 9.4x 2027 EBITDA. Information services is a sector that historically trades around 25x EBITDA, if not higher. Craig is an “aggressive buyer” at these levels with a conservative $50 12-month price target, implying ~50% upside.

Industrials

ABM’s 2Q EPS beat was driven by stronger-than-expected revenue growth, with sales up 8.4% Y/Y and gains across all five segments for the fifth consecutive quarter. Technical Solutions, Aviation and Manufacturing & Distribution each grew by more than 15%, supported by organic gains and acquisitions. Sidoti’s FY26/FY27 EPS estimates of $4.03/$4.55 imply annual growth of 17.0% and 13.0%, respectively, while their FCF per share estimates of $4.25/$4.42 imply FCF yields of 10.0%/10.4%. ABM’s shares have traded at an average premium of 5% over the last 20 years to the S&P Small Cap 600 Index on a forward P/E basis but currently trade at a 34% discount. Sidoti maintains their Buy rating and $68 target, implying c.50% upside.

Consumer Discretionary

Alex Barron believes the acquisition is an important signal for the US homebuilder sector, supporting his view that the bottom of the cycle is here and now is an opportune time to buy into the sector at great valuations. The deal values TMHC at 1.24x 2Q26 book value, 1.17x Alex’s 2026E book value and 12.9x 2026E EPS. His fair value estimate was $72/share. While Berkshire is unlikely to pursue an immediate acquisition spree, the deal opens the door for TMHC to become a larger consolidator over time. Alex also notes rising sector M&A, including Dream Finders attempted hostile bid for Beazer Homes, which he thinks would likely need to move closer to 0.8-0.9x book value to succeed.

Technology

TEMN’s acquisition of Additiv strengthens its position in wealth management, particularly in the fast-growing mass affluent segment, while adding a cloud-native orchestration platform that accelerates implementation times, enhances customer journey management and supports the company’s AI strategy. Additiv brings attractive growth characteristics, including strong DD ARR growth, 138% NRR and a blue-chip customer base. The acquisition also expands TEMN’s reach across Europe, the Middle East and Asia-Pacific, with opportunities to scale through its global channels. While the price has not been disclosed, GR20’s analysis suggests the deal is unlikely to be expensive, potentially valuing Additiv at c.4-5x revenue. TEMN plans a gradual integration approach, reflecting lessons learned from previous acquisitions and aiming to maximise long-term cross-selling and synergy opportunities while limiting execution risk.

Investor Idea Event highlights several compelling Shorts

Revelare hosted a Buyside Event in London where short theses were shared for companies including: 1) Associated British Foods - Primark is caught in a competitive “no man’s land” and is being squeezed by Shein, Vinted and LEFTIES. 2) CSG - trades at peak earnings, driven by unsustainable, high-margin spot-market ammunition sales to Ukraine and its true revenue visibility is much lower than its headline backlog suggests. 3) IWG - the presenter questioned the company’s highly touted transition to a capital-light management / franchise model; sees the business as plagued by poor disclosure and aggressive accounting. 4) Vestas Wind Systems - utilities moving services in-house puts margins at risk and Chinese competition challenges a peak multiple.

Uranium: Feeling hot

The Global X Uranium ETF (URA US, USD48.96) has been ranging net sideways since peaking at USD60.51 last Oct. The ETF fell as much as 34% from the high. A new classic chart pattern appears to be forming, a 7-month Ascending Triangle. A breakout would target USD90.00 – Chris Roberts will add to his initial long if such a breakout occurs. He remains bullish on Uranium and has established an initial position this week. Go 30% long at market. The initial stop loss is a daily close below USD39.15.

South Africa: Yield curve repricing

South Africa’s yield curve has partially recovered from the March oil shock, which lifted yields across maturities, with the 10-year moving from around 8.1% at the late-February low to 9.4% at end-March, before easing back to around 8.65%. The curve remains materially below the old stress regime, but it is now higher and flatter because the short end has repriced more aggressively than the long end, as markets moved from pricing around 50bp of SARB cuts to roughly 75bp of hikes for the rest of 2026. The March shock did not undo the fiscal-credibility gains that drove the earlier rally, but it has made the route to further long-end compression narrower and more stretched out. The fiscal-credibility narrative remains supported by the stronger 2025/26 fiscal outturn, resilient revenue, lower-than-budgeted debt-service costs and Moody’s positive outlook. Looking ahead, Peter Montalto now sees the 10-year SAGB ending 2026 around 8.5%, from 8.0% before the US-Iran conflict.

Korea: Everything but a hike

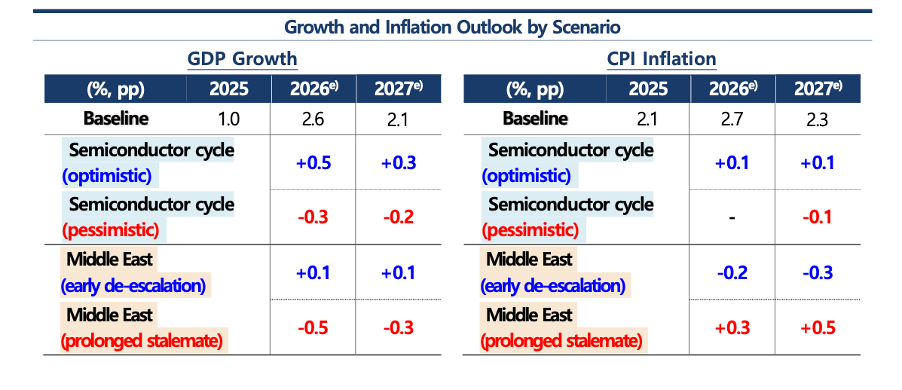

The BOK didn't hike today, but reading through the materials, Paul Cavey comments that it was a surprise that it stayed on hold. The governor made it clear that rate hikes were coming. Three aspects of the forecast stand out for markets. The BOK now thinks the current account surplus will be $250bn in 2026, up from a $72bn forecast just months ago. The bank also thinks core inflation will be 2.4% in 2026. That feels low, given core was at 2% before either of the shocks from Iran and semiconductors, and with the BOK itself flagging that big tech profits will lift nominal wages. If the semiconductor cycle and the Middle East situation were to evolve simultaneously in the pessimistic direction (see chart), adverse feedback loops between financial conditions and the real economy would emerge, further amplifying the growth slowdown.

Where’s China’s fiscal crisis?

Things continue to look absolutely awful on the Chinese public sector front. Not only is China already one of the most heavily indebted economies in the EM universe, it also runs ever-widening public deficits. Then there’s the looming pension crisis. In short, claims Jonathan Anderson, this appears to be a disaster in the making. So, why haven’t things exploded? On the one hand, there are already growing austerity pressures in the economy, as local governments hike levies and fees on businesses and push for higher pension contributions. I.e., the fiscal mess is already becoming a drag on activity and growth. At the same time, however, there is no sign of budgetary funding stress. Why? Because the government completely controls both funding costs and flows via its state-owned monopoly in the commercial banking system, which in turn holds virtually all fiscal and "quasi-fiscal" debt. The real question is about the health of banks, not budgets.

Argentina: A battle of wills

Marcos Buscaglia focuses on the discrepancies between the IMF and the Argentine government that transpired in the recent IMF report. While the IMF sees GDP growth converging to 3%, the government hopes that reforms could lift growth up to 4.5%. The IMF projects inflation reaching single-digits by 2028, yet the government thinks the decline could be earlier and faster. The target set for FX reserve accumulation for the year is $8bn, but the IMF scenario is at least $10bn. The authorities promised to limit FX selling intervention and made no promise on the removal of lingering FX controls. Marcos says the government has implemented a more expansionary monetary policy, without compromising its FX and price stability targets, so far. The economy will continue improving somewhat in the coming month. Inflation will be closer to 2% in May. Marcos expects the central bank will likely keep rates around current 20% levels.

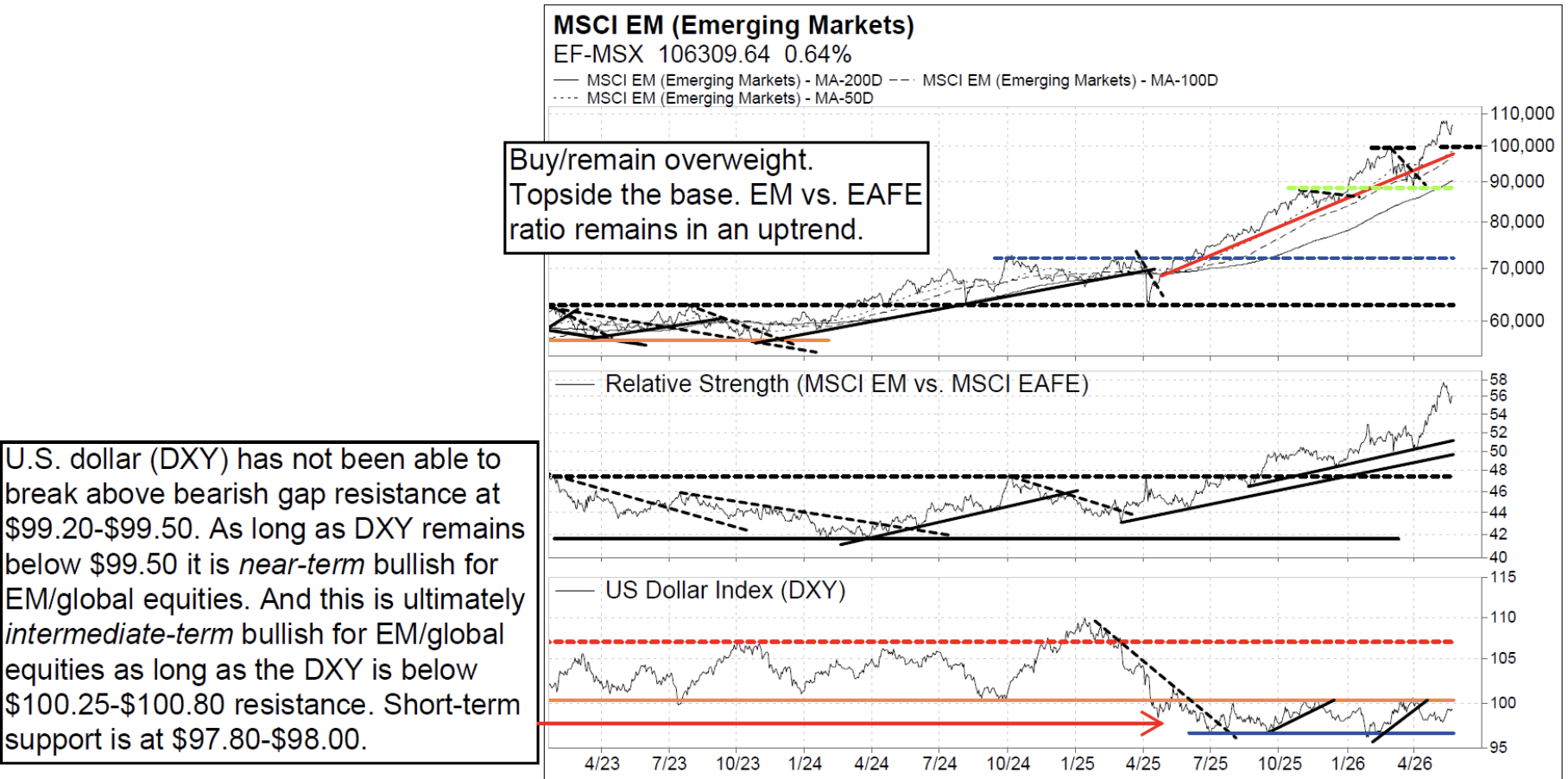

EM strategy

The Vermilion team remain overweight MSCI EM vs MSCI ACWI since Jan and continue to be overweight EM vs EAFE since August 2026. The team also remain intermediate-term bullish from a price perspective as long as EEM-US is above $57 (up from $55), and near-term bullish as long as $61.50-$62.00 and $59.50 supports hold. EEM-US supports to buy are at $63.50, $61.50-$62.00 and $59.50. A new uptrend has begun. When it comes to specific countries, the team especially like Taiwan and South Korea, with no other countries coming close. For sectors, the team’s overweights include EM tech and EM Industrials. EM Technology has been so strong, and has such a large weighting in EM, that it has become increasingly difficult for any other sectors to outperform relative to MSCI EM. Many leading Technology stocks that we have recommended in recent months are quite extended, and we would be buying on any pullbacks.

US: …and the answer is margins

If you want to understand equity markets today, Paul Krake advises to start and end with margins. The blended Q1 2026 net profit margin for the S&P 500 came in at 14.7%, the highest figure since FactSet began tracking the metric in 2009, eclipsing the 13.2% record set just one quarter ago. The direction of travel is unambiguous. What is changing now, and what makes this margin story qualitatively different from the cycle-on-cycle expansions that preceded it, is who participates. The hyperscalers are not building this infrastructure for their own consumption. They are building the road, and the rest of the economy pays a toll to drive on it. The productivity gain accrues to the customer. The S&P at all-time highs is not a puzzle. The cleanest expression of this view in a single trade is long the equal-weight S&P 500 against the cap-weighted index. The next phase of this story is breadth. Equal-weight is how you own it.

Europe and China: An upcoming full-blown trade war?

The European Union has laid the groundwork for a more robust industrial policy amid anxiety over the bloc’s growing trade imbalance with China. On May 18th the FT reported that the EU is developing new rules that would require European companies to buy critical components, including chemicals and industrial machinery, from at least three separate suppliers, not all from the same country. Additionally, a growing chorus of EU voices is backing tougher action on China, such as French President Emmanuel Macron calling for the EU to adopt anti-dumping and anti-monopoly measures akin to Section 301 of the US Trade Act of 1974 to counter dependence on China. There are also signs that China’s strategic patience with Europe is running out. Dinny McMahon says MNCs exposed to both Europe and China need to urgently conduct supply chain audits and develop contingency plans for a sharp downturn in ties between Beijing and Brussels.

The ECB’s coming hike

According to Mark Bathgate, the ECB is likely to hike at their next policy meeting on June 11th. Mark points out that President Lagarde has clearly stated, “memories of 2022 are very fresh” – hence he says that the ECB is going to prioritise its inflation stability mandate and tighten policy to deliver on that. He thinks they will hike 25bps, then suggest that more hikes are possible. The most likely scenario for further hikes after the initial one is an “end of war” outcome – where business/confidence rises, but inflation continues to rise due to the 12-18 months disruptions/inflation in energy-intensive products. The market has moved between pricing 2 and 3 rate hikes over recent weeks – this seems reasonable pricing. A cash rate around 2-2.5% and 100bps curve to the 10-year part of the curve is seen by the ECB as “back to normal”, and a sustainable place for monetary policy to be (also good for the health of the EU banking sector).

AI and its discontents

The AI buildout is transforming the US economy almost uniformly for the better. Output is increasing both as a result of higher investment and higher productivity. If AI works, the US will have an unassailable dominant position in the global provision of services. It appears not everyone agrees. At a commencement speech at the University of Central Florida, the fairly innocuous comment that the rise of AI is the next industrial revolution was met with booing from students. There is clear political backlash against AI, including in America, the country that stands to benefit the most from its development. Yet, technological change has a habit of steamrolling political concerns over its deployment, and technology tends to determine the political economy rather than the other way around. Dimitris Valatsas is not worried (yet) about political opposition derailing US dominance in AI, but it’s worth watching closely.

AI and Say's Law

Without a doubt, AI is a transformative tech with a strong future. However, Andrew Hunt says that some of the markets’ assumptions appear wayward to him. To “believe” in the AI Boom and in current market valuations, one must assume that the risk-free rate in the economy is at an equilibrium level currently; that there is minimal misallocation of capital occurring; that this is not simply just another credit boom; that forecast rates of likely AI take-up are accurate; and that Say’s Law will prevail (i.e. supply will create demand). Andrew finds evidence that many of these preconditions have likely already been invalidated. In previous manias, the “bell-was-rung-at-the-top” by often esoteric events within the plumbing of the credit system. It remains to be seen whether Mr Warsh will begin a quantitative tightening in the face of rising inflation, or bow to the political realities.

Beyond Lithium: The next battery boom

Industrials

Battery technology is at a commercial inflection point with the economics now favouring electrification over fossil fuels across an expanding range of applications, a trend accelerated by higher energy prices from the Iran conflict. China continues to dominate the supply chain, with CATL alone controlling ~39% of the global EV battery market and leading in grid-scale storage deployments, but Korean manufacturers offer accessible, liquid alternatives with deep ties to Western automakers and compelling technology road maps of their own. Given the geopolitical and technology risks, investors should build a basket of stocks: CATL for multi-chemistry platform execution at reasonable multiples; LG Energy Solution for contracted backlog and near-term profitability; Samsung SDI for solid-state battery optionality; and Amprius as a higher-risk tech position. BYD is also highlighted as a play on growing EV demand.

Telfer vs. KCGM: The revival of Aussie icons

Materials

While the market remains cautious on Northern Star Resources given ongoing KCGM execution risks, potential cost overruns and weak near-term news flow, the company is nearing completion of a transformational ~A$1.8bn mill expansion to 27Mt/yr, part of ~A$5bn total investment into KCGM across FY22-FY28, which could ultimately restore production towards ~0.9Moz/yr by FY30. However, with management still needing to rebuild investor trust, GMR retains a Hold rating on NST. In contrast, they are more constructive on Greatland Resources, which is still in the early stages of reinvesting in Telfer / Havieron, with ~A$2.8bn of potential capex through FY32 supporting a pathway back towards ~0.4-0.5Moz/yr production by the end of the decade, alongside exploration upside at SLC and West Dome. Given the scarcity of >300koz/yr gold assets, GMR believes Telfer could become a strategic bolt-on acquisition for peers seeking scale in Australia.

Industrials

Hamed Khorsand’s bearish call on KRMN is already playing out with the shares down ~40% since his Sell initiation earlier this year, yet he continues to see material downside with a 12-month target price of $37. Acquisitions masked underlying weakness in the company’s core business during Q1. Excluding newly acquired maritime defence assets, revenue would have declined sequentially, despite a strong defence spending environment. Hamed also flags KRMN’s rising contract assets (unbilled receivables), which now exceed 32% of the company’s 12-month trailing revenue, alongside weak FCF generation. Valuation remains elevated at ~42x EV/EBITDA, while comps begin to look tougher as the year progresses.

Special Sits Idea Forum

MYST’s buyside events continue to deliver impressive performance (~19% avg. alpha on highlighted ideas at their previous Special Sits Forum). Their latest event featured a high number of potential takeouts / M&A plays, business separations, several Media stocks and various AI-related companies. The most compelling ideas included:

Chemours (CC US) - Refrigerant share gains + “free kicker” from steepening China TiO2 cost curve. TP $46 (110% upside).

ITT (ITT US) - High-quality pumps pure-play experiencing positive mix shift. TP $284 (45% upside).

Valmont Industries (VMI US) - “Non-obvious” AI infrastructure play benefitting from utility pole pricing inflection. TP $709 (35% upside).

Fundrise Innovation Fund (VCX US) - AI / Anthropic proxy trading at ~10x NAV with upcoming lock-up expiry catalyst. TP $50 (75% downside).

Communications

CEO Johan Svanstrom is the wrong leader for RMV’s critical transformation. Despite bringing a background as a “digital native” who scaled Expedia’s Hotels.com to over $3bn in revenue, more recent roles at BIMobject and RMV reveal a polarising leader who is disinterested in operational details and relies on a closed circle of advisors. Svanstrom will continue to champion an AI strategy with high-level, buzzword-driven directives while delegating core business oversight, creating significant execution risk and key-person dependency on a team he has already begun to alienate. His chaotic leadership and lack of operational discipline are a direct mismatch for the rigorous execution and financial control the company desperately needs. Paragon’s research includes interviews with former senior executives who worked with Svanstrom for more than 32 years combined.

Financials

86Research recommends investors aggressively buy Futu following its 14% post-1Q26 preview selloff, arguing the decline significantly overstates temporary market-driven weakness with a US$231 price target, implying 59% upside from current levels. Analysts believe downward earnings revisions and geopolitical tensions triggered excessive selling despite strong rebounds in global equity markets since early April. According to channel checks, Futu’s user acquisition and net asset inflows have already recovered to pre-March levels, positioning the company to achieve its 2026 target of 800,000 net new funded accounts. 86Research also highlights FUTU’s dominant Hong Kong brokerage position, Southeast Asia expansion plans, strong management team, and industry-leading margins. Trading at only 11x 2026 earnings, the stock remains deeply discounted relative to historical averages and peers.

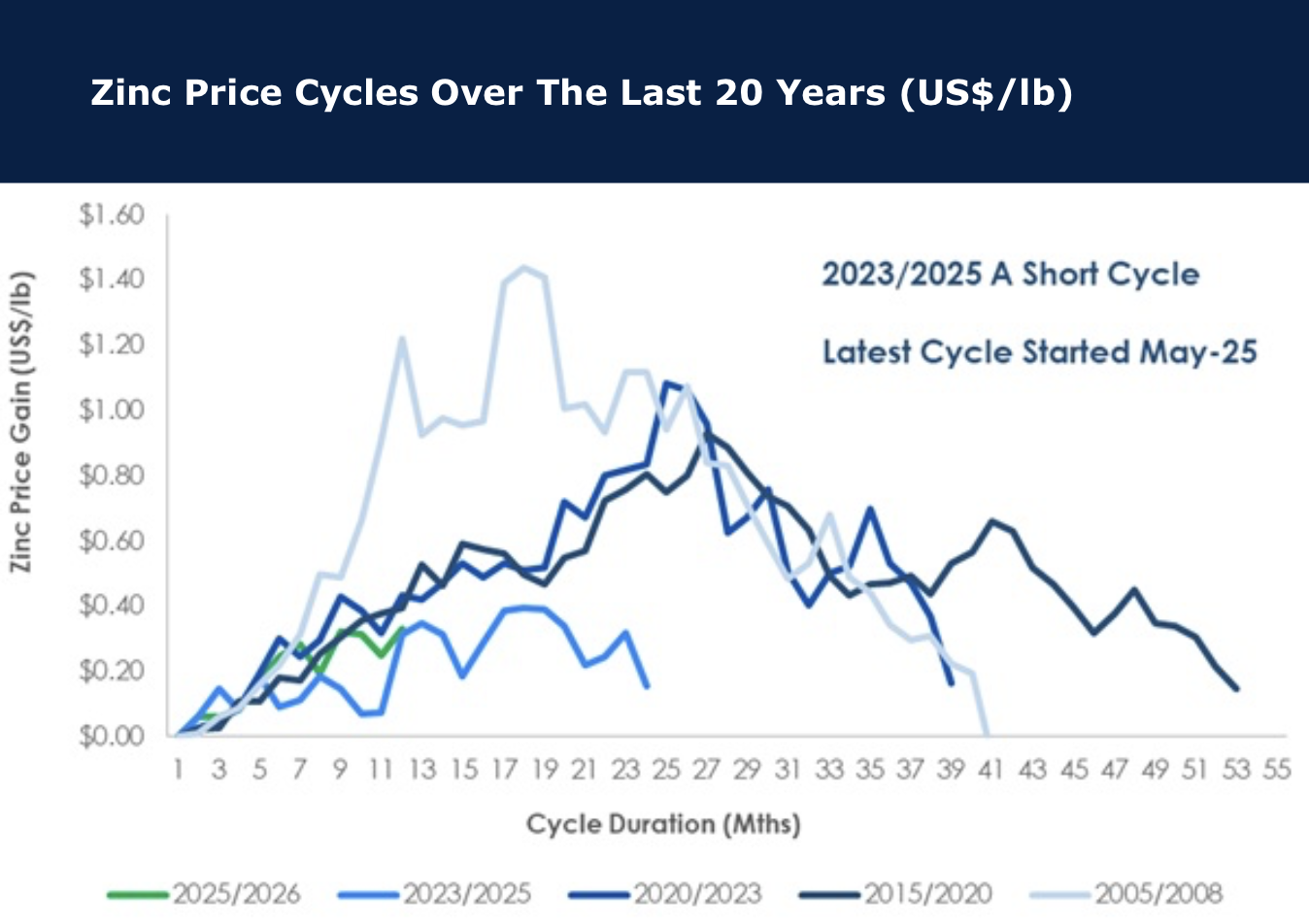

Zinc: Weak demand, weak supply

The zinc price is up ~12% in 2026 and as such has been broadly tracking the copper price momentum. However, David Radclyffe discusses some of the several recent setbacks impacting both the near- and mid-term outlook. These include recent production downgrades at both Grapenberg and Golden Grove, and the significant cost blowout / deferral of production at Hermosa. Good news has been sparse. Although global mine supply of zinc is estimated to exceed 12.5Mt in 2026, GMR’s coverage, representing a quarter of supply, is forecast to decline by ~16% this year implying downside risk to market expectations. Zinc price cycles tend to last 3-4 years with the last ending early, therefore the current cycle could extend for some time (see chart). David’s preferred choices include BOL and IVN based on value and metal exposure.

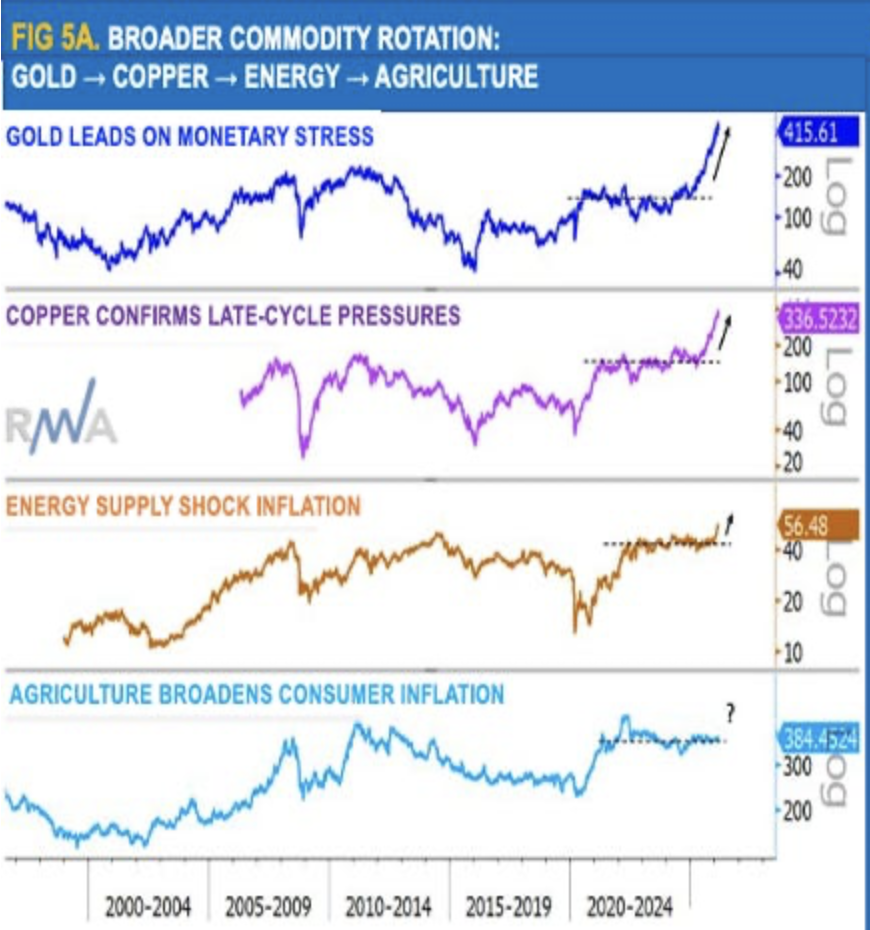

A commodity supercycle

Ron William’s latest market review continues to highlight the early stages of a developing commodity super-cycle, a theme that is already demonstrating clear outperformance fuelled by a resurgence in inflation and reinforced by second-order effects from the energy complex. What began as a concentrated move in precious metals, driven by debasement concerns, has progressively rotated into energy, reflecting supply-side constraints, and is now extending into agriculture. This broadening is significant: agriculture sits at the intersection of input costs and end-consumer prices, making it a key transmission channel for inflation, and accordingly, it remains top-ranked within Ron’s model. For the wider backdrop, Ron describes it as “shaken, but not yet stirred”: markets are absorbing a series of macro shocks – most notably inflationary pressures and the ongoing oil disruption – but these forces have not yet fully translated into a coherent, late-cycle regime.

South Africa: Fiscal monitor

The fiscal year finished strong, with many of the key sources of upside and flexibility that Peter Montalto identified post-Budget materialising. Revenue was stronger despite weak growth. This left the primary surplus at 1.1% of GDP – in line with Peter’s view and above NT’s 0.9% Budget estimate. The key point is that the fiscal golden threads have been reinforced, if not strengthened, though this might well only translate into a slow ratings upgrade cycle. Peter sees the primary surplus at 1.5% of GDP in 2026/27, rising to 2.2% in the outer year. The usual caveats remain. Spending quality is still markedly lower than optimal. That the year-end fiscal strength reinforces the case for an S&P ratings upgrade later this year, in Peter’s view. NT is likely to maintain an (overly) conservative line however through the upcoming spending round to the MTBPS – focusing (perhaps too much) on geopolitical risks into the fiscus – again to be surprised to the upside later.

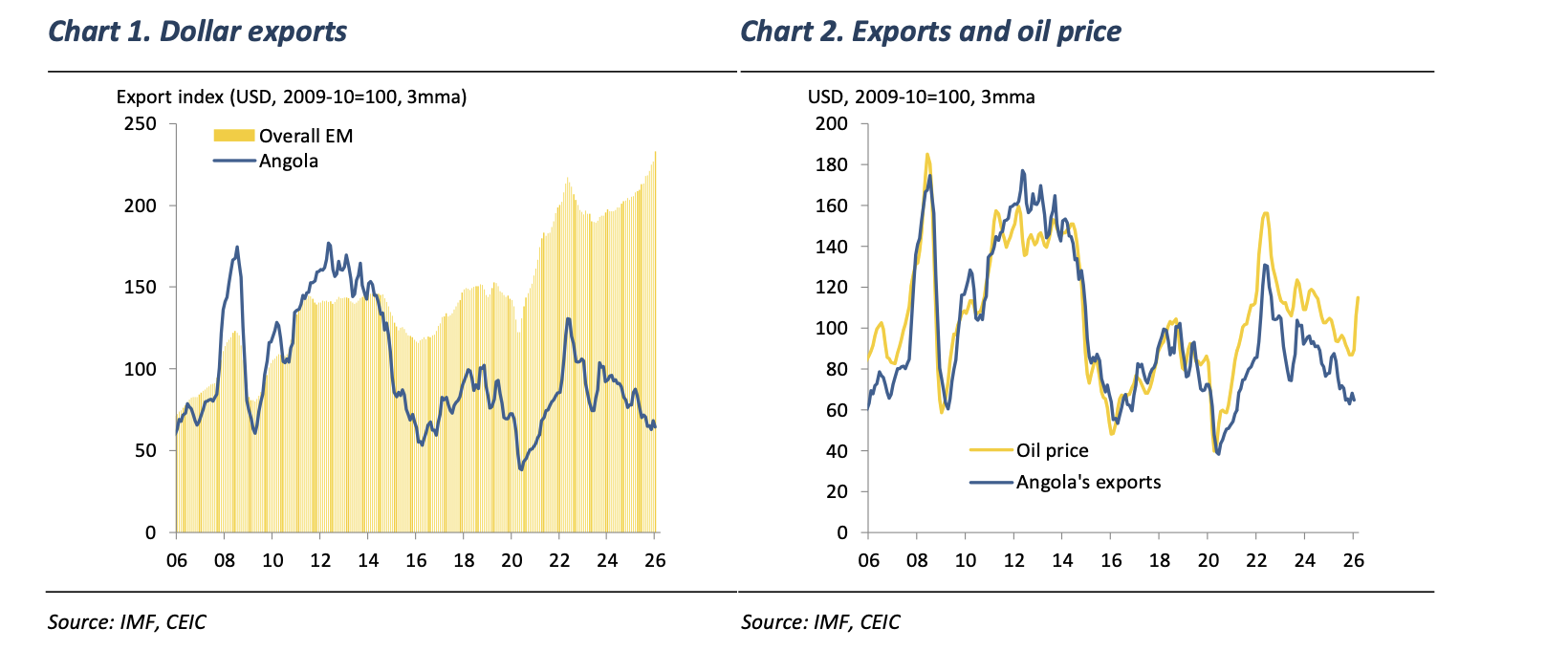

Angola could really use higher oil prices

In the first of a series of African frontier countries that Jonathan Anderson is covering in the coming weeks, he takes a look at Angola. The country did a strong job of stabilizing macro conditions in the aftermath of the late-2010s crisis, but over the past couple of years that stabilisation has been fraying, with worsening external and fiscal conditions on the back of lower crude oil prices and weak petroleum production. This leaves export earnings far below the rest of EM and well below what current oil prices would normally imply (see graph). The dismal picture may start to change soon with new energy projects that are expected to meaningfully increase oil and gas production in the near term. In the absence of this year's big oil shock Jonathan would have expected renewed FX pressures and rising spreads and yields ... and Angola's best hope is that dollar crude prices stay solidly in the triple digits.

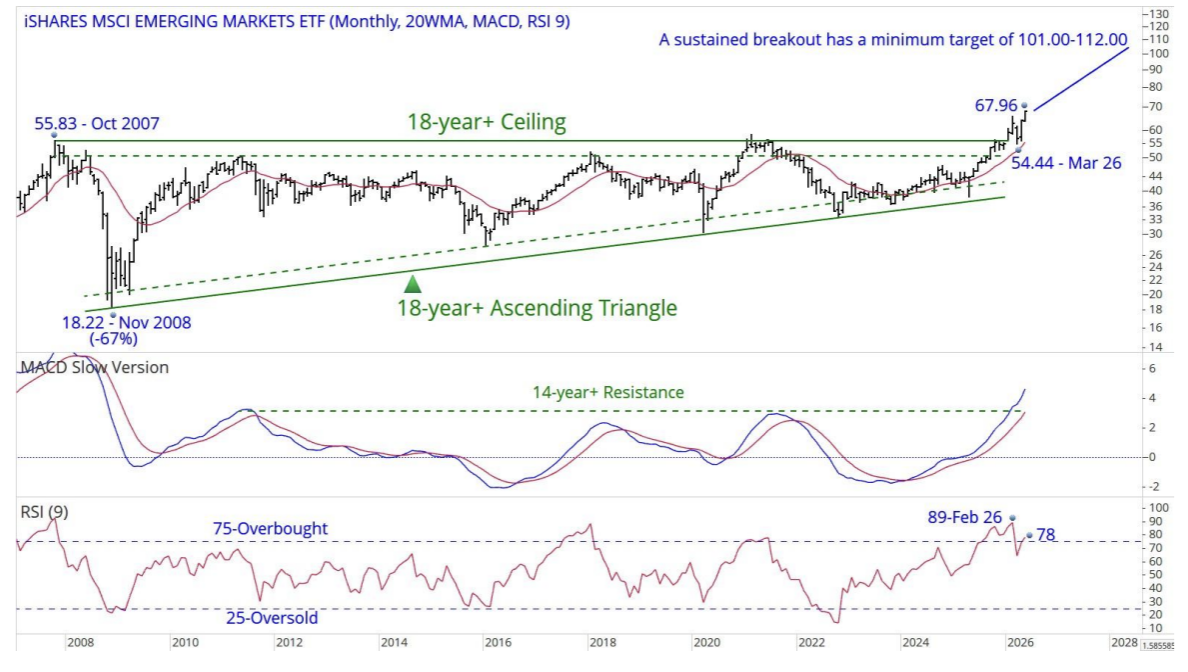

MSCI EM: The return of the Dodo

The iShares MSCI EM ETF (EEM US, last USD67.94) has successfully broken out from an eighteen-year-plus ascending triangle and is currently attempting to move beyond an eighteen-year-plus ceiling. While Chris Roberts points out that a sustained breakout above this resistance level suggests a minimum price target between USD101.00 and USD112.00, and the MACD indicates a significant improvement in momentum by clearing a fourteen-year resistance level, the nine-month RSI of 78 is approaching the very overbought threshold of 80. Consequently, it is prudent not to chase the current price; instead, the strategy is to wait for a setback toward the key support level at USD54.44 before considering a buy. Chris thinks he has found a dodo.

US S&P: Feeling good

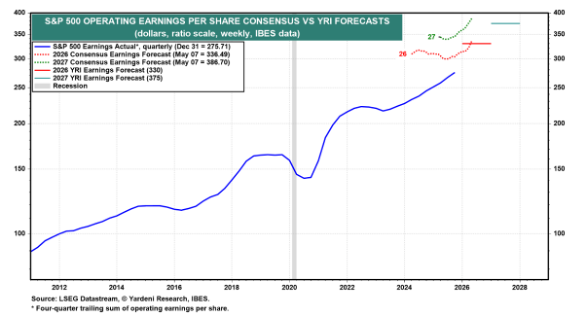

Ed Yardeni is raising his year-end S&P 500 target from 7700 to 8250. He has never seen consensus earnings expectations rise so quickly for the current and coming years as they have in recent months. The result has been an earnings-led meltup in the stock market. Ed is raising his EPS estimates to $330 this year and $375 next year, while sticking with his forward P/E range of 18.0-22.0, resulting in a year-end range for the S&P 500 of 6750-8250. His key assumption is that the economy will remain resilient, and so will earnings. Ed is also raising his probability of a continuation of the Roaring 2020s to 80% from 60% simply by merging it with his meltup scenario (previously at 20%), since he believes that any meltdown will be a buying opportunity and won't trigger a recession or bear market similar to the 1999-2000 Tech Bubble and Tech Wreck.

US: Higher oil and rates, lower equities

David Woo argues that the market has got ahead of itself in reverting the move in 2y breakevens. His short-term market bias is: higher oil - lower equities - higher rates - neutral dollar. (1) Higher oil: Whether we will see resumed fighting or not, the two sides will not reach a deal anytime soon. Iran is not about to capitulate to US demands with support from Russia and China. (2) Lower equities: As the market starts to look beyond Q1 towards Q2, the high oil price will weigh more on growth expectations. European stocks are particularly at risk given their dependence on energy imports and lack of exposure to technology. (3) Higher rates: AI is inflationary in the short-term. The war is driving up prices from energy to crops. Fixed income investors are trying to ignore the war. (4) Neutral dollar: Trump wants to hit the EU with a 25% auto tariff, which the Supreme Court may prevent.

Consumer Discretionary

Lululemon shares are trading at both 52-week and five-year lows after a difficult period marked by product challenges and pressure on the brand’s core offering. The source notes that the company had strayed too far from its brand DNA, with limited colour in parts of the range and the departure of its senior merchant. However, early signs of improvement are emerging, including a tighter product offering, more colour and the appointment of a former Nike executive as CEO. While a full turnaround is likely to take time, The Retail Tracker sees potential for the stock to reach $175 over the next 12 months.

Vision adds liquid, low-crowded US shorts

So far in 2Q26, Shorting Specialists Vision Research has closed shorts on Tractor Supply and Insulet (both initiated in 4Q24 at much higher levels) and has initiated 2 new US shorts. The first a consumer company that trades greater than $100mn/day, facing intense Chinese competition gaining share with both local and foreign manufacturers, customers that are losing share, announced orders that do not seem to ever fully materialise into sales, weak organic sales growth, and overly optimistic estimates for 2H26 and 2027. The other short idea is an industrial company facing demographic headwinds, potential regulatory changes, increasing input costs, negative volume trends, potentially peak margins, and bullish forward estimates. Both stocks have short interest % of free float below 8%.

Consumer Discretionary

Zach Shannon initiates a Short recommendation on Shoe Carnival which experienced a rapid deterioration in same store sales in Q4 FY25, with declines across all three of its store banners. This caused the company to walk away from its plan to rebanner more than 100 Shoe Carnival locations as Shoe Station (its higher-priced storefront) as converted stores significantly underperformed expectations. As a result, the company's CEO left abruptly (resigned or terminated) in February, with the company pulling its prior CEO out of retirement to serve on an interim basis. With inventory at a 10+ year high (inventory was up 14% last year on a 6% sales decline), the company faces pressure to rightsize the business and turn its stores around. However, guidance for FY26 is backend weighted, while FY27 consensus estimates appear aggressive. As a result, Corto believes SCVL shares have material downside risk (-20% to -50%).

Technology

Infineon Technologies AG was presented by a PM at a Revelare event as a long idea with ~50% upside to a €75 price target. The stock trades at ~16x 2027 EPS and ~12x 2028 EPS, below its 10-year median multiple of ~19x. The thesis rests on two tailwinds: analog recovery and AI datacenter demand. Infineon’s industrial and automotive businesses are rebounding, while €800–900M of annual underutilization charges should normalize, driving ~600bps gross margin expansion. Simultaneously, denser AI server racks require advanced power semiconductors, where Infineon leads across silicon, GaN, and silicon carbide. AI revenue is expected to grow from €700M last year to €1.5B this year, with additional upside potential. Gross margins could rise from ~17% to ~25% over 2–3 years, supported by higher-margin AI products and cyclical recovery.

Consumer Discretionary

Despite near-term margin pressure, DFH trades at only 7.5x 2026 earnings and 1.1x book value, well below peer averages. Analysts maintain a fair value estimate of $25 per share, implying significant upside potential. They have the second highest ROE in the sector out of the 17 builders Housing Research Center follows. The stock is trading at $13.02 and peaked at $43 two years ago. They have grown nearly 5x in the past 6 years more than any other builder and recently made a bid to acquire Beazer homes (BZH) at 0.5x book value. That would allow them to grow another 50% in 2027. They should make EPS of $2.00 in 2026 and $3.00 in 2027.

Consumer Staples

Sprouts Farmers Market reported encouraging 1Q26 results, reinforcing QuoVadis Research’s bullish stance. Revenue, same-store sales, margins, and EPS all modestly exceeded company guidance and Street expectations, suggesting management has regained control after the sharp slowdown experienced in 2H25. The company also deployed all 1Q26 free cash flow toward share repurchases, buying back 1.9M shares at an average price of $73.68, with QuoVadis modeling $500M in buybacks for full-year 2026. While guidance was largely maintained, the EPS outlook was slightly raised, signaling improved visibility. At just 13x P/E and 8x EV/EBITDA on consensus 2026 estimates, the stock undervalues Sprouts’ strong ROIC-driven growth and favorable risk-reward profile.

Europe: Uncontrollable hiccups

Niall Ferguson expects euro area headline inflation, measured by the harmonised index of consumer prices, to peak near 3.5% in late 2026 or early 2027 and to return to 2% in 2H2027. This is a higher peak than consensus and a longer return to target than in the European Central Bank’s adverse scenario. The return to 2% inflation was never sustainable. Imported disinflation from Chinese manufactured goods had been masking broad but shallow inflation in domestic services, and the current shock now arrives with no disinflationary buffer. Accordingly, Niall expects the ECB to hike rates by 50 bps by year-end. His views on US and EU rates and inflation translate to a minimally stronger euro than the market is pricing; Niall sees the EURUSD spot price at 1.178 and the one-year forward at 1.193. Europe’s second inflation shock in four years will prove less acute than the first but harder to shake.

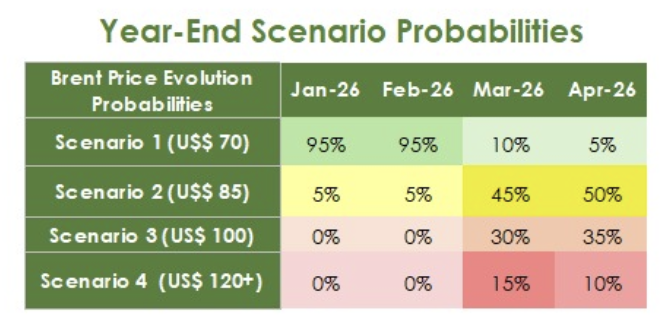

Oil: Predictions for year-end

Brent climbs higher, reflecting the ongoing stalemate between the US and Iran and, above all, the lack of concrete progress in negotiations. The cancellation of the trip of US envoys to Islamabad reinforced the perception that, despite the formal maintenance of the ceasefire, the diplomatic channel remains stalled. At the same time, signs of greater pragmatism from Iran are beginning to emerge, with the possibility of a provisional agreement involving the reopening of the Strait of Hormuz in exchange for partial relief of restrictions imposed on Iranian ports. Even so, US resistance to easing the blockade and regional pressure, especially with the continuation of attacks in Lebanon, keep the geopolitical environment quite fragile. The DayByDay team assign a 50% probability to Brent being priced at $85 by year-end, and 35% that it’ll stay around $100. They see only a 10% chance of prices staying above $120.

Copper: Lack of supply growth vs rising inventories

David Radclyffe's copper coverage totals ~63% of global mine production. Copper supply continues to wrestle with many legacy headaches from 2025, mixed with the Iran conflict and its implications for diesel and sulphuric acid supply. There is therefore downside supply risk. However, the current oil disruption has implications for global growth and copper demand. Worryingly, David points out that copper inventories are rising rapidly. His coverage universe implies 0.9% annual contraction in refined copper supply in 2026, following a strong 2025. Weak supply growth for 2026, even with moderate demand growth, is at odds with strongly rising terminal market inventories, now at 1,267kt, adding to price risk. Copper is a crowded long trade, with caution warranted. The sector is not particularly cheap at spot 1.6x P/NPV10 and 9x EV/EBITDA. Antofagasta PLC is cut to HOLD. Preferred stocks include Lundin Mining Corp, KGHM Polska Miedz SA, Ivanhoe Mines Ltd, Grupo Mexico SAB de CV, Hudbay Minerals Inc and Teck Resources Ltd.