No matches for this search

Try adjusting your filters or search criteria

Financials

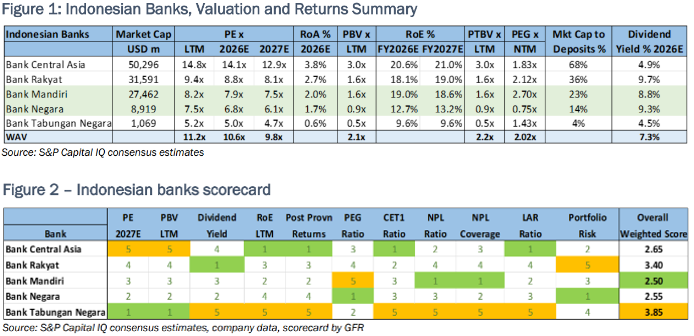

Victor Galliano upgrades Bank Mandiri and Bank Negara to Buy on better-than-expected credit quality, attractive valuations and signs the government is reining in market-unfriendly policies. Both banks screen well on fundamentals (fig 1) and in his proprietary scorecard (fig 2). Mandiri is his top pick, driven by strong credit quality and solid returns, supported by mid-ranking valuations. Low NPLs underpin a declining cost of risk and improving post-provision returns, while returns relative to valuation are very attractive. With PBV near a three-year low and bond yields elevated, he sees scope for a valuation uplift if yields ease. Negara’s valuations are close to deep value and, although return trends remain uninspiring, it has the lowest MSME exposure of the peer group and second best NPL coverage.

Financials

BBNI is Victor Galliano’s top pick among the Indonesian banks, based on its compelling value and growth credentials. It has the lowest PEG ratio of the big four, undemanding prospective PE multiples and the best PBV ratio to ROE combination. Return trends continue to improve; pre-provision returns have risen after bottoming out in 3Q23, which combine with declining cost of risk to drive better post-provision returns. In addition, the bank’s efficiency ratios have begun to improve. With its CET1 ratio of 19%, BBNI has bridged the gap with Mandiri on capital adequacy and on credit quality it also has the second highest NPL coverage of its peer group, after Permata.

Financials

Victor Galliano reviews 6 large and mid-cap Indonesian commercial banks on the back of recently announced 4Q23 results to identify those that are attractive value, have good earnings growth prospects and have the potential to deliver higher returns. BMRI is his top pick for its quality attributes, its premium and growing pre- and post-provision returns; it also provides a better valuations to returns mix than Bank Central Asia. Bank Negara is his value pick with its low PE multiples, its attractive PEG ratio, whilst also improving pre- and post-provision returns with cost of risk well controlled.

Financials

Indonesia is seeing a strong recovery in lending growth, which adds to the positive trifecta for BNI - improving margins (NIM up from 4.5% to 4.9% in 2Q22 Q/Q. There are few banks in Asia-Pacific that show this type of NIM expansion), with improving loan volume, and better credit metrics (BNI is one of those banks that appears to have taken far too much credit costs during FY20 and FY21). It just so happens, that BNI’s market capitalisation of IDR154tr is a fraction of the IDR970tr for comparable peer bank Bank Central Asia.