Ripples of risk-off

Murray Gunn wrote about the dichotomy between the fortunes of Ripple, the cryptocurrency company, and XRP, its token. He pointed out the booming company that has been securing lucrative and high-profile contracts, yet the price of XRP has been declining. Another Bitcoin bust beckons, as the iconic cryptocurrency was declining in the next wave of its ongoing bear market since its peak last year. Bitcoin also sports at least one head and shoulders top pattern which could give it even more bearish implications. Murray pondered whether the crypto slump was a subtle sign that risk appetite was waning, and it might now be finally feeding through into the stock market with the S&P 500 down over 3% last week. Don’t be surprised to hear and read about people attempting to “buy the dip.” And when the stock market struggles to recover, as he suspects, expect increasing panic to ensue.

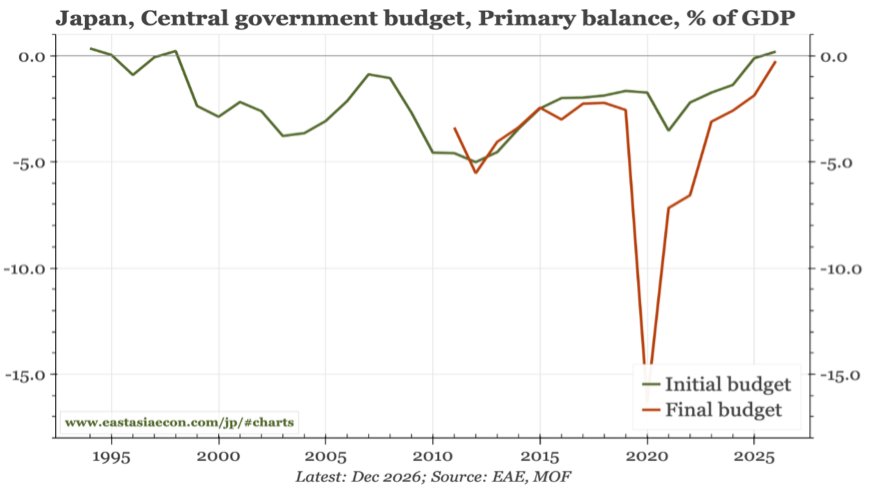

Japan: Yen under pressure, but data is encouraging

Graham Turner says that the prospect of a rate hike at the FOMC meeting in June casts a harsh spotlight on the Bank of Japan: the BoJ will meet earlier next week, and unless it agrees to tighten policy too, the yen is likely to plumb new lows against the US$. For the Bank of Japan, there is no obvious pressure to hike, as inflation has been well-behaved. The y/y for the Nationwide CPI eased to 1.38% in April. The CPI excluding food, alcohol & energy dipped to 1.06% y/y. Real wages are rising sharply, in part, because of the drop of core inflation as well as fuel subsidies. The labour market in Japan is tight. The unemployment rate fell to 2.5% in April. Total employment jumped to 68.76m, a new high, despite a shrinking population. These are encouraging trends that bode well for Japan’s response to an ageing population, particularly against the backdrop of high government debt.

US: Bond volatility matters most

Ahead of the next FOMC in mid-June, Michael Howell questions the importance of the rate-setting ritual. He argues that the bond market, not the US Fed, is the main force shaping the economy and equity markets. More specifically, what matters most is not bond yields but rather bond volatility. Investors should be watching the MOVE index and closely examine the US Treasury’s actions in the bond market, because they may now matter more than the policy rate itself. Michael argues that the Fed has been sidelined, losing much of its traditional influence over financial conditions. Still, it plays an important financial stability role in smoothing funding operations and specifically maintaining harmony in the crucial repo / collateral markets. Also, he notes that lower policy rates are not always stimulative. Because the private sector is a net creditor to the government, rate cuts can reduce interest income to bondholders and potentially dampen spending.

US: The populist backlash against AI

Report by

BCA Research

BC

Matt Gertken and Marko Papic say that the populist backlash against AI could result in bipartisan regulation in 2027, but is especially likely to prompt tax hikes from 2029. Public criticism of the new technology is growing and politicians in the US and abroad are proposing measures such as AI regulation, taxation, redistribution, and restrictions on data centres. Job displacement is the core concern, with opposition to AI strongest in service-oriented economies where workers fear automation. Americans increasingly view AI as developing too quickly, oppose data-centre construction in their backyard, and are becoming less optimistic about the benefits of technology, particularly among younger generations. The investment risk is political, not technological: a recession, AI-driven mass layoffs, inflation, or a major AI-related accident could mobilise voters and lead to aggressive regulation or higher taxes on technology firms as early as next year – and especially after the 2028 election.

Eurozone growth risks mispriced amid hawkish consensus

The Variant Perception team examine the outlook for the Eurozone as inflation leading indicators and breadth remain elevated well above pre-Covid levels. Whilst rising service price surveys put pressure on the European Central Bank to remain hawkish to anchor inflation expectations, matching the market pricing of at least three interest rate hikes over the next year introduces substantial downside growth risks. According to the team, current market dynamics replicate the post-GFC period by overstating inflation fears and underestimating growth destruction. This structural misalignment occurs at a time when Eurozone macroeconomic breadth vs the rest of the G10 remains weak. With the trend component of the firm's tactical outlook model turning decisively negative, the underlying economic setup points toward a sharp growth capitulation rather than a sustained tightening cycle. The team express their bearish view on European growth by selling rallies in the euro.

Greek Equities: Adopting a more cautious stance

ResearchGreece revisits their stock picks and assesses the political outlook ahead of the next parliamentary elections. Macro conditions remain solid, with Q1 real GDP up 2.0% Y/Y, although inflation accelerated to 5.2% Y/Y in May (+0.0% M/M). With the Athens Index up +11% YTD, valuation multiples of non-banks in their universe have expanded to 13.2x P/E and 8.0x EV/EBITDA 2027, leaving more limited upside. Combined with polls pointing to a hung parliament, ResearchGreece is turning more cautious on Greek equities. Banks remain their preferred exposure (solid outlook - volume, rates, asset quality) as a leveraged Greek macro play. They prefer National Bank of Greece, Bank of Cyprus, Piraeus and Optima. Outside banks, they favour selective infrastructure, industrial and defensive names such as OTE, Titan, PPC and Piraeus Port over consumer stocks and cyclicals.

Hang Seng on the launchpad

Erik@YWR argues that the Hang Seng’s sluggish start to 2026 masks a much more attractive setup, with the index described as a “coiled spring” after moving sideways for 15 years in hard-currency terms. He sees 35,000 as achievable, supported by improving fundamentals: based on YWR’s approximation of 89 constituents, earnings growth is expected to accelerate from a 6% CAGR over 2015-2025 to 11% over the next 3 years. Key drivers include 17% EPS CAGRs at Tencent and Alibaba, 6% growth from the major Chinese banks, oil-price support for energy names, 26% growth from BYD and CATL, and a recovery in property stocks. With earnings revisions turning positive, Hong Kong property prices recovering (mainland China prices stabilising) and the index on <10x 2028 earnings, Erik sees meaningful upside.

Consumer Discretionary

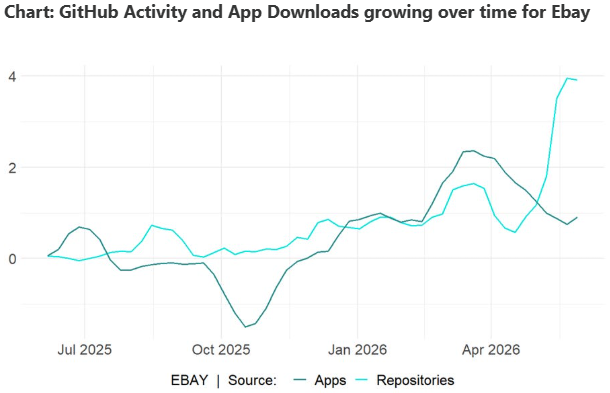

The company ranks in the top 20% of AnteData’s universe, reflecting a strong improvement in coding momentum during 2026. The signal is primarily being driven by rising App activity and exceptionally strong GitHub interest where developers are building pricing tools, arbitrage engines and inventory automations using EBAY as a pricing and transaction platform. AnteData sees the group’s focus on passion-driven goods, including auto parts, collectibles and luxury items, as increasingly important, with these categories now representing >30% of value traded. They believe EBAY can sustain c.8% annual revenue growth over the next 5 years, lifting sales from $11.5bn to $16bn and nearly doubling income to c.$4bn.

Copper’s record prices: What happens next?

In this presentation, Jeffrey Christian of CPM Group gives an update on gold, silver, platinum, and palladium prices before turning to copper. He explains why precious metals appear to be settling into a summer consolidation period, with gold trading near $4,500, silver holding within its recent range, and platinum and palladium also moving within broader trading bands. Jeff then turns the focus to copper, where CPM Group remains constructive on the long-term outlook but less aggressive than many other market forecasts. He discusses why copper demand tied to construction, electrification, vehicles, power grids, AI, and data centres needs to be analyzed with more nuance and less uncritical enthusiasm. While CPM expects the copper market to remain tight, with refined supply falling short of fabrication demand. Jeff also explains why some long-term copper price expectations may be too optimistic.

Click here to watch.

USDJPY: Stable but unsustainable

USDJPY seems stable for now, caught between the upward lift from the negative real interest rates in Japan, and the gravity of valuation and the MoF’s threats of interventions. Stephen Jen believes that the next big move in USDJPY is down. But elevated oil prices may delay the timing of this prospective correction. USDJPY remains elevated near 160. There are several powerful forces pushing USDJPY higher, even though the JPY is already grossly undervalued. Japan’s real interest rates remain very negative. The BOJ’s policy rate is minus-65 bps in real terms, and minus-300 bps relative to the Fed Funds Rate. Further, the negative terms-of-trade shock from higher oil prices is the second driver of USDJPY. In essence, the JPY is the mirror image of the USD, which has been propped up by capital inflows over the years, attracted by the higher carry and capital gains in US equities, pushing the USD deep into overvalued territory.

US: Warsh’s natural bias

In the last week markets have moved to peg the Fed for about 28bps of hikes in the next year, a substantial shift from the 1-2 cuts priced in late February. Warsh assumes the Chair with a challenge to his natural bias – higher productivity via AI implying stronger GDP growth potential (but less inflation and hence need to hike), weak jobs markets but immigration arguably keeping the U/E rate down (which should point to rate cuts), a tighter and smaller Fed balance sheet (that implies rate cuts to offset) and different measures of inflation (trimmed mean over core PCE which conveniently is lower and implies rate cuts). This set of biases imples that Warsh is more of a cutter than a hiker. While the markets peg the first Fed hike in March 2027, Craig Ferguson thinks that the Fed will get an inflation shock in the next 3-4 months that leads to them hiking in Q3.

US: …and the answer is margins

If you want to understand equity markets today, Paul Krake advises to start and end with margins. The blended Q1 2026 net profit margin for the S&P 500 came in at 14.7%, the highest figure since FactSet began tracking the metric in 2009, eclipsing the 13.2% record set just one quarter ago. The direction of travel is unambiguous. What is changing now, and what makes this margin story qualitatively different from the cycle-on-cycle expansions that preceded it, is who participates. The hyperscalers are not building this infrastructure for their own consumption. They are building the road, and the rest of the economy pays a toll to drive on it. The productivity gain accrues to the customer. The S&P at all-time highs is not a puzzle. The cleanest expression of this view in a single trade is long the equal-weight S&P 500 against the cap-weighted index. The next phase of this story is breadth. Equal-weight is how you own it.

The ECB’s coming hike

According to Mark Bathgate, the ECB is likely to hike at their next policy meeting on June 11th. Mark points out that President Lagarde has clearly stated, “memories of 2022 are very fresh” – hence he says that the ECB is going to prioritise its inflation stability mandate and tighten policy to deliver on that. He thinks they will hike 25bps, then suggest that more hikes are possible. The most likely scenario for further hikes after the initial one is an “end of war” outcome – where business/confidence rises, but inflation continues to rise due to the 12-18 months disruptions/inflation in energy-intensive products. The market has moved between pricing 2 and 3 rate hikes over recent weeks – this seems reasonable pricing. A cash rate around 2-2.5% and 100bps curve to the 10-year part of the curve is seen by the ECB as “back to normal”, and a sustainable place for monetary policy to be (also good for the health of the EU banking sector).

AI and its discontents

The AI buildout is transforming the US economy almost uniformly for the better. Output is increasing both as a result of higher investment and higher productivity. If AI works, the US will have an unassailable dominant position in the global provision of services. It appears not everyone agrees. At a commencement speech at the University of Central Florida, the fairly innocuous comment that the rise of AI is the next industrial revolution was met with booing from students. There is clear political backlash against AI, including in America, the country that stands to benefit the most from its development. Yet, technological change has a habit of steamrolling political concerns over its deployment, and technology tends to determine the political economy rather than the other way around. Dimitris Valatsas is not worried (yet) about political opposition derailing US dominance in AI, but it’s worth watching closely.

Beyond Lithium: The next battery boom

Industrials

Battery technology is at a commercial inflection point with the economics now favouring electrification over fossil fuels across an expanding range of applications, a trend accelerated by higher energy prices from the Iran conflict. China continues to dominate the supply chain, with CATL alone controlling ~39% of the global EV battery market and leading in grid-scale storage deployments, but Korean manufacturers offer accessible, liquid alternatives with deep ties to Western automakers and compelling technology road maps of their own. Given the geopolitical and technology risks, investors should build a basket of stocks: CATL for multi-chemistry platform execution at reasonable multiples; LG Energy Solution for contracted backlog and near-term profitability; Samsung SDI for solid-state battery optionality; and Amprius as a higher-risk tech position. BYD is also highlighted as a play on growing EV demand.

Technology

CORZ moves sharply higher in Arete’s AI infrastructure rankings following a major expansion in its long-term power roadmap, with them now modelling 3.6GW of IT load and $6.3bn of NOI by 2032 - up from prior estimates of 1.9GW and $3.7bn, respectively. Arete argues demand for AI compute remains “off-the-charts”, while CORZ is becoming increasingly attractive to hyperscalers through the expansion of its Pecos and Muskogee campuses into gigawatt-scale AI data centre sites. Importantly, the company has leveraged its existing CoreWeave contract into $3.3bn of financing, giving it sufficient capital to begin pre-building new facilities before signing additional leases, which Arete views as a key competitive advantage. With leasable power expected to nearly triple over the next few years, Arete raises their TP to $55 (100% upside) and now ranks CORZ alongside Applied Digital as a top pick in colocation infrastructure.

Industrials

Investors remain far too apathetic towards European construction stocks, overlooking a multi-year infrastructure and housing investment cycle that could materially benefit BAM. The shares have hardly moved so far in 2026, despite the group reporting FY25 revenues up 9% Y/Y to €7.0bn, adjusted EBITDA up 20% to €400m and net profit almost tripling to €211m, while ending the year with €792m net cash, a €13bn order book and a new €40m buyback. BAM will issue new mid-term targets next year, but Europe’s 2026-2030 infrastructure strategy will release ~€600bn of funds further boosting the group’s order book, while civil infrastructure in UK currently faces a "herculean to-do list" that requires a 30-50% increase in investment over the next decade. TP €15 (55% upside).

China’s asset revitalisation: An unanticipated growth boost?

In a 24-page special report, Dinny McMahon discusses the “asset revitalisation” measures that could help end the problem of local government austerity. Over the last few years, China’s local governments have significantly ramped up the amount of revenue they generate by leasing state assets and selling concessions – known as “revitalising” assets. This “asset revitalization” has become a major source of income for a handful of provinces, materially improving their fiscal conditions. Chongqing, the leader, funded 15.1% of provincial general expenditures last year from such activities, up from only 6.8% four years earlier. For China’s financially overstretched provinces, “asset revitalisation” is emerging as a much-needed new channel for expanding revenue. It stands to have a potentially transformative impact, creating an unprecedented opportunity for local authorities to repair their finances, and opening the door to an unanticipated boost in growth over the next couple of years.

Caution in Cote d’Ivoire

Cote d'Ivoire has done extremely well in the past couple of years on the back of explosive agricultural and metals export price gains, with an improving external and fiscal balance and falling sovereign dollar spreads. The medium-term outlook remains buoyant, with new oil and gas projects already coming online and significant further volume gains expected in the next four to five years. However, Jonathan Anderson points out that the base is still relatively low today as a share of total exports, which leaves near-term market sentiment highly geared to cocoa and gold prices. Cocoa markets have already come down hard, and while gold remains relatively buoyant Jonathan does worry about overvaluation relative to fundamentals. With high public external debt exposures compared to dollar earnings, this could be a source of volatility in the dollar sovereign market and a bit of caution is in order.

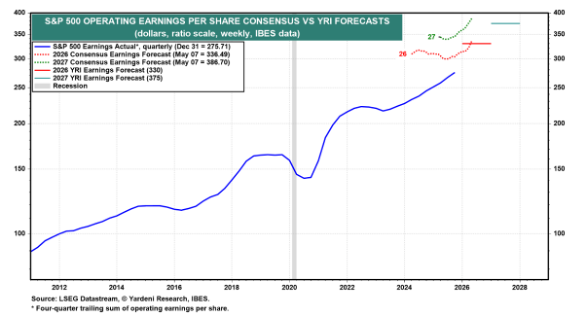

US S&P: Feeling good

Ed Yardeni is raising his year-end S&P 500 target from 7700 to 8250. He has never seen consensus earnings expectations rise so quickly for the current and coming years as they have in recent months. The result has been an earnings-led meltup in the stock market. Ed is raising his EPS estimates to $330 this year and $375 next year, while sticking with his forward P/E range of 18.0-22.0, resulting in a year-end range for the S&P 500 of 6750-8250. His key assumption is that the economy will remain resilient, and so will earnings. Ed is also raising his probability of a continuation of the Roaring 2020s to 80% from 60% simply by merging it with his meltup scenario (previously at 20%), since he believes that any meltdown will be a buying opportunity and won't trigger a recession or bear market similar to the 1999-2000 Tech Bubble and Tech Wreck.

UK: The next PM

It is unlikely the factions within the Parliamentary Labour Party (PLP) will be able to vote on one candidate, so the election would be decided by the Labour Party’s electoral college (1/3rd MPs, 1/3rd Trade Unions, 1/3rd party members) between the two candidates selected by the PLP. The main candidates include Wes Streeting; Angela Rayner, the most popular of the Soft Left candidates; Ed Miliband, who is the most likely candidate should Rayner decide not to run; and Andy Burnham, who would need to be elected as an MP to be able to run. The current paralysis is bad for the Gilt market due to the likelihood that it pushes borrowing needs up over the coming months due to higher gilt yields, energy subsidies and the defence budget black hole. The potential timeline for election of a new PM is between 2 and 4 months from today.

UK: Everybody hurts

This week’s elections worked out very much as Niall Ferguson expected, with the governing Labour Party mauled, and the populist Reform UK party surging. Nationalist parties ended up in charge of Scotland and Wales. Niall sees the change as being more profound than mere shifts in the balance of party politics, with Britain breaking up into a patchwork of electoral backgrounds in a way that bodes ill for state structure and party coherence. Niall doesn’t see Starmer resigning soon but is certain he will not fight the next election. Badenoch will lead the Tories as her strong personality is beginning to get across to the public. Yet, the country is drifting towards a deeply uncertain election result in 2028/29 where nobody wins and nobody loses. It is hard to be anything but bearish about the country’s future.

Consumer Discretionary

Lululemon shares are trading at both 52-week and five-year lows after a difficult period marked by product challenges and pressure on the brand’s core offering. The source notes that the company had strayed too far from its brand DNA, with limited colour in parts of the range and the departure of its senior merchant. However, early signs of improvement are emerging, including a tighter product offering, more colour and the appointment of a former Nike executive as CEO. While a full turnaround is likely to take time, The Retail Tracker sees potential for the stock to reach $175 over the next 12 months.

Technology

SK Hynix benefits from better demand visibility and reduced investment risk whilst demand for mid- to long-term agreements is increasing as customers seek volume security and price stability. Arete expects these agreements to materially reduce industry volatility and improve earnings stability, supporting its structural AI-driven thesis. They see two key catalysts for sector re-rating: substantial free cash flow generation driving higher capital returns, with details expected by year-end, and the market underestimating earnings durability over the next several years. With SK Hynix trading on 5.5x FY27 earnings and 2.5x book value, there is significant upside ahead.

Argentina: Make hay while the sun shines

Marcos Buscaglia comments on a challenging year of debt services ahead for the government and central bank. Even if debt with the IMF and other multilaterals is rolled over, the debt maturing next year is very high with total hard currency debt services nearing $36bn, of which $18bn pertain to bonded debt. The government already squandered an opportunity to tap markets at the beginning of the year, when the risk appetite for Emerging Markets debt was high. Marcos believes the government is reluctant to issue market debt because of the inevitable rise in interest bills, but he finds that this is both inevitable and not worrisome in the short term. He believes the market is more than willing to take on new Argentine debt, with 10-year rates possibly dropping to low 9s. The government should take advantage.

US: Warsh ready for prime time at the Fed

Based in part on his previous interactions with Kevin Warsh, the prospective next Fed Chairman, John Ryding discusses what he is likely to do when he takes over on 15th May. John says that Kevin understands complex economic arguments but is not wedded to conventional academic wisdom. Kevin hates inflation and firmly believes that it is a monetary phenomenon and that the Fed must take responsibility for it. Although Kevin feared at one point that the Fed might raise its inflation target to 3%, he seemed adamantly opposed to the idea. Kevin brings a great depth of institutional market knowledge to the Fed, which it desperately needs, and is willing to think outside the box. In his prepared statement to the Senate Banking Committee, Kevin made it clear that he believes “monetary policy independence is essential. Monetary policymakers must act in the nation’s interest . . . their decisions the product of analytic rigour, meaningful deliberation, and unclouded decision-making.”

Financials

MRX is a beneficiary of geopolitical instability, particularly in commodity markets, where it is a leading player. The shares have pulled back from recent highs but are only ~12% above the 2025 peak, despite 1Q26 profits likely to rise c.50% Y/Y - implying meaningful multiple compression. Fighting Financials sees scope for this to reverse as volatility persists. Consensus Q1 PBT forecasts sit c.13-14% below management’s end of March guidance, while FY26 consensus implies flat Y/Y performance for the remaining quarters, which is clearly inconsistent with the current earnings trajectory. With the potential to return >60% of its m/cap via dividends and buybacks over the next 5 years, MRX stands out as one of the cheapest, high-quality financials in their investment universe and is one of the few compelling long ideas in a market, where opportunities are largely on the short side.

South Africa: Absorbing an external shock

According to Peter Attard Montalto, what started the year as a macro “big bang” has shifted decisively into an external oil-shock management, with Q2 centred on resilience rather than momentum. Q2 will be dominated by the implications of the Middle East conflict. South Africa is moving from a position of relative macro strength into a live test of its ability to absorb an external shock. Peter notes that considerable resilience is still being shown, especially in the currency, and the impacts are likely to be less severe than in historical counterfactuals. Nonetheless, Peter does not want to gloss over what remains a serious shift. Growth has been trimmed, inflation raised, and rates are now expected to rise in May before easing only next year. Peter assumes there will only be a temporary oil shock through May, but a prolonged conflict remains a key risk that would start to lead to domestic security and supply concerns.

Hungary: Orban’s fall

Katharina Klotz observes that even a heavily engineered electoral system could not save Hungarian Prime Minister Viktor Orbán. As a record share of voters turned out in yesterday’s parliamentary election, the conservative, anti-corruption, and moderately pro-European Tisza party achieved a landslide victory, securing more seats than Orbán ever achieved. Katharina expects Tisza leader Péter Magyar to take office within the next month. For the EU and Ukraine, this is very good news. She expects Magyar to lift Hungary’s veto on Brussels’ €90BN loan to Ukraine (90% probability) rapidly and play a more constructive role in EU policy from defence to China. With a supermajority in parliament, he will also be able to pass rule-of-law reforms required to unlock at least a high share of the €18BN of frozen EU funds (90% probability)—a crucial lifeline for Hungary’s struggling economy.

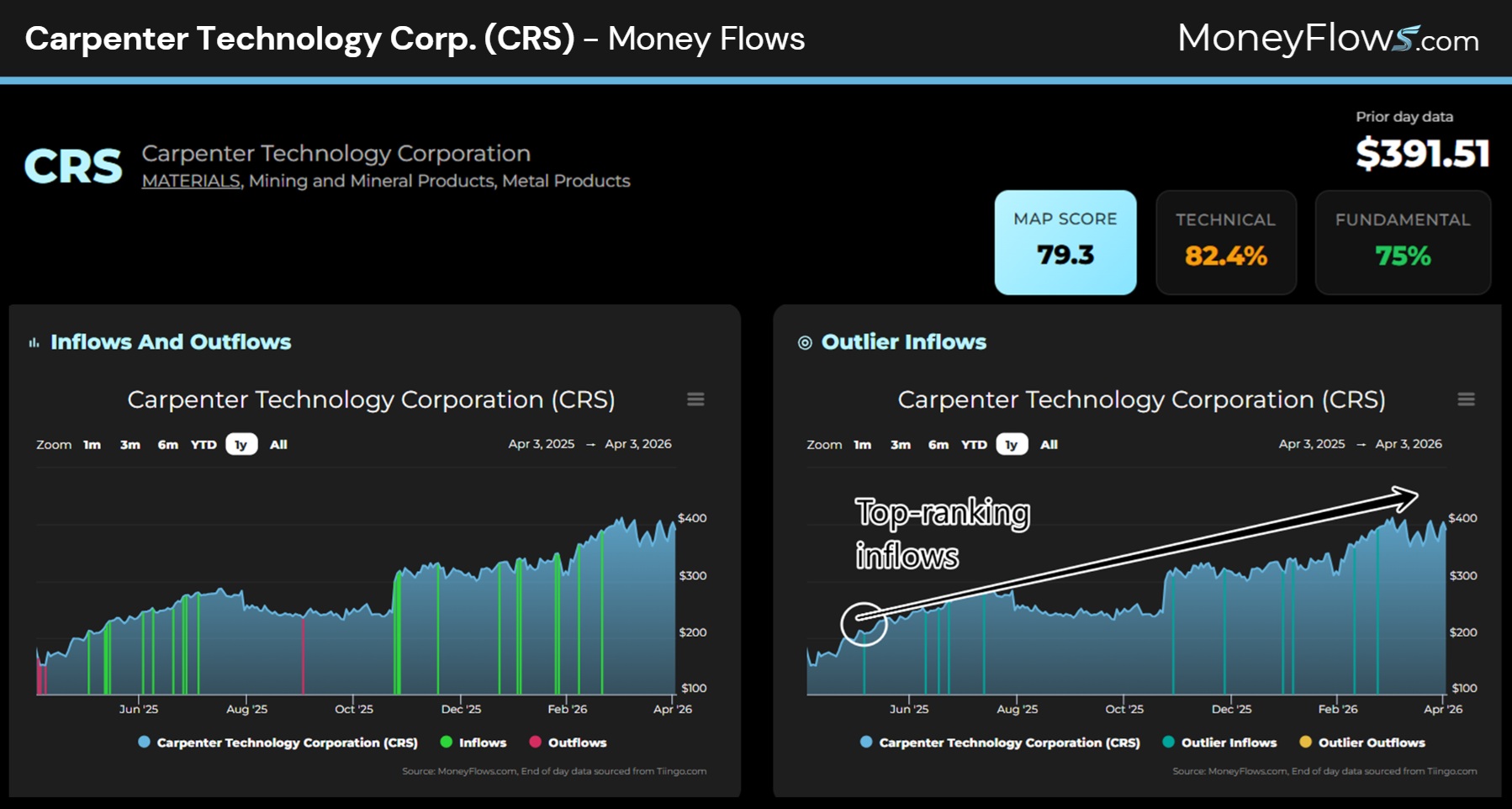

The best 3 space exploration stocks to buy in 2026

Technology

The space economy is a major structural growth theme, expected to expand from ~$614bn in 2024 to >$1.8tn over the next decade, with opportunities extending beyond rockets into the broader infrastructure stack. MAPsignals’ edge lies in identifying institutional inflows before the narrative becomes consensus, using its “Big Money” framework to find winners early. For example, Teradyne was flagged at ~$90 last June and has since surged to ~$342 on sustained inflows, with further upside anticipated. Applying the same process, they also highlight Carpenter Technology and Palantir as beneficiaries of the space buildout, supported by persistent institutional buying - including “non-stop” inflows into Carpenter. Tomorrow’s leaders are found by following the flows, not the headlines.

Gold’s next move

In his latest video, Jeffrey Christian of CPM Group reviews the latest developments in gold, silver, platinum, and palladium markets, explaining why prices are rising again and what may come next. He discusses the recent price movements in gold and silver, including the sharp rally earlier in the year, the pullback following Federal Reserve policy signals, and the renewed strength tied to political tensions and broader concerns about global economic stability. Jeff also addresses recent commentary around Russian gold sales, clarifying how the Russian central bank has been managing its reserves since the start of the Ukraine conflict and why recent sales are not unusual in that context. He then turns to the growing interest in hedging, particularly among mining companies, and explains how producers and investors can protect profits while maintaining upside exposure.

Click here to watch.

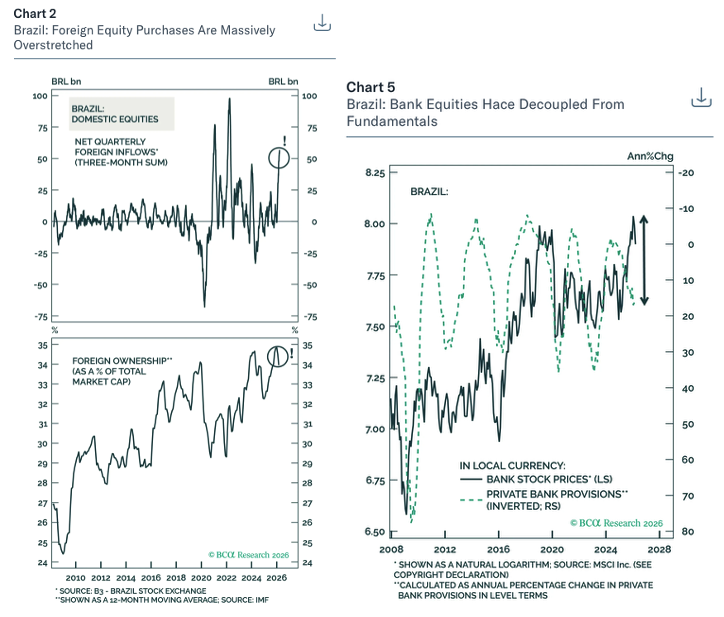

Brazil: Overhyped

Report by

BCA Research

BC

Should investors buy the dip? The BCA team think not. The recent bull market has been fuelled by unsustainable foreign inflows and is massively overstretched (see left chart). The divergence between rising stock prices and worsening macro fundamentals has become untenable (right chart) – investors are too sanguine. Domestic demand will worsen, with odds of a recession rising for the next 6-12 months. The only factor that can prevent such a drastic economic slowdown is major fiscal easing, yet this would cause markets to sell off. Some investors argue that high commodity prices will bail out Brazil, which is theoretically correct, yet in the past this has brought down equities due to the global growth recession it causes. Commodities also matter far less to Brazil’s stock market today. Stay underweight Brazil in equity and fixed-income portfolios. The team also recommend a new short-term trade (three-month horizon): Pay 10-year Brazilian swap rates.

US: The Private Credit Crunch

US money and credit growth has slowed over recent weeks, and Andrew Hunt believes the Private Credit Crunch may be intensifying. If private finance had indeed become the principal source of external funding over recent years for the now significantly cash flow negative US corporate sector, then the ongoing problems in the private channels will now be causing a binding credit crunch that will likely further suppress economic growth, even before the impact of higher energy prices. This will impact the AI sector. The impact of the Big Bill may offer some near-term support to growth, but Andrew suspects that by Q2 the economy may be soft – a recession may be due to arrive in H2. Investors can expect the FRB to remain active in the debt markets and to press ahead with rate cuts next quarter. If global capital flows continue to stall then the USD will weaken. Under this scenario, UST yields could continue to rise until the FOMC is forced into YCC.

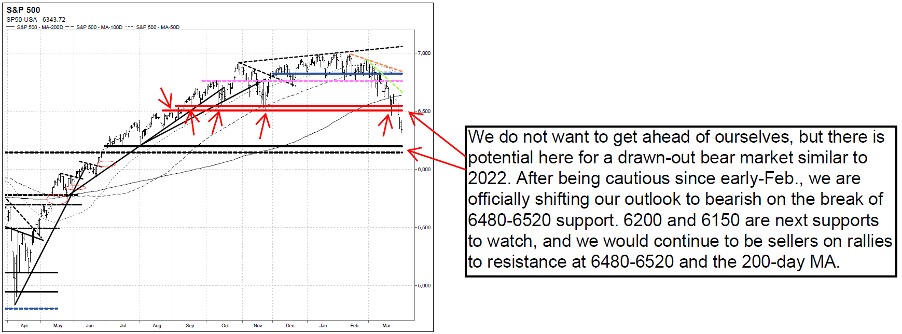

US: Down to bearish

The Vermilion team are officially downgrading their outlook to bearish with the S&P500 (SPX) violating major support at 6480-6520, Nasdaq futures (NQ) violating 24,000 support, and the Russell 2000 (IWM) breaking down below crucial $245 support. This comes the team downgraded their outlook to neutral early in March. Concerns that they discussed since early-February stemmed from deteriorating market dynamics, and ever since then they been concerned about a deeper pullback, likely to 6720-6776, 6690, or 6480-6520 on SPX, while also discussing since mid-March how downside capitulation is likely needed before finding a reliable bottom. With continued deterioration in market dynamics, their report last week discussed how they were closely watching for a breakdown below 6480 and that the SPX likes to test the 200-day MA as resistance (from below) before continuing lower, and this is likely what happened on 3/23/26. 6200 and 6150 are the next supports to watch, and they would continue to be sellers on any rallies to 6480-6520 and 200-day MA resistances.

Turning cautious ahead of the obvious

Konstantin Fominykh’s tools turned cautious before the markets saw the obvious, having initiated sell signals on the S&P500 and US industrials on Feb 9th (before the 9% and 8% drops), US healthcare since Feb 3rd (7% drop), US tech (11% drop) and Bitcoin (38% drop). The Middle East situation is worsening. Private credit signals a prolonged contraction; default rates appear low on the surface, but adjusted measures suggest significantly higher stress, with effective defaults closer to ~6.4%. Konstantin is selling US financials. He also remarks that the AI/tech trade is not working because everyone already owns a lot of it, and has a fresh sell on AI and Next Gen Software ETF (March 23rd). There is a likely recession ahead catalysed by a reversal in AI capex and the energy supply shock; expect earnings to peak Q1-Q2. Investors were spoiled by the 16-year bull market, so it’s no surprise that people still believe in "strong earnings" and "buy the dip".

Financials

The market is missing a key earnings driver as ~20% of AUM is currently fee-free but will convert to fee-paying over the next 6 years. This creates a LDD CAGR on the top line without requiring market growth. With a largely fixed cost base, STJ can deliver ~10 points of margin expansion through 2030. Additional bull points flagged include STJ’s success in capturing the next generation of wealth (one third of clients are under the age of 40); while AI-driven efficiencies could unlock ~30% productivity gains and further consolidation within the advisor ranks. The stock trades on ~15x depressed earnings but ~5x 2030 earnings, with ~70% of cash returned via dividends and buybacks. TP £22.00 (80% upside).

Technology

A broken IPO trading ~60% below its $25 listing price, with potential to double over the next year and deliver a 3x return over 4 years. Recent share price weakness is due to a market that has indiscriminately punished the entire software sector, as well as the company's usage yield compressing, which bearish analysts have misinterpreted as an erosion in pricing power. NAVN is the technological leader in a $185bn corporate travel and expense market, disrupting legacy incumbents with a unified platform and a differentiated model. The stock trades at ~2.9x EV/FY26 sales based on guided revenue of ~$685m - a clear dislocation for a platform growing ~29% with 74% gross margins and 13% operating margins. A path to 30%+ margins exists at scale. The setup is likened to Booking.com in 2009 when it was trading under $100/share.

Silver futures (SIK26) forecasts

With the attainment of the new low under 78.06, the Technical Analysis Group have closed half of their NT Strategic Short position, established into strength at 95/96, and are placing a trailing stop at 87.70 on the remainder of the trade. Price action from 97.30 has yet to reveal any urgency or impulsiveness to the downside. The team are expecting near term relative outperformance in gold vs silver, and are bullish the 'RATIO' whilst above 57.59, seeking upside in the near term to 67 +/-, and 72.66+. Since raising risk, they have seen a +12% rise to 64.47. The team continues to remain long term bullish and regardless of whether or not they’re in the higher degree 4th wave, they do not expect downside under their proposed 60 +/- 10 LT Long Term Range Base, before ultimately eclipsing this year’s 121.78+ high in the resumption of the underlying bull trend, exposing their next major upside attraction levels of 138 and 165 (see chart).

Iran: The War in English

The “War in English”, as jokingly referred to by Israeli officials, has settled into an intense but steady pace. Niall Ferguson believes that US and Israeli objectives remain on track despite a geopolitical expansion of the war. Should Iran prove unable to muster larger missile or drone salvos by the end of the week, it would seem likely that it has no remaining capacity to do so. This should give shipping firms and insurers more confidence to begin transiting the Strait of Hormuz next week. If disruptions to the Strait continue into next week, Niall expects a major and coordinated SPR release from net importers to take place to reduce the stress in global crude markets. However, the potential costs of a protracted conflict and closure of the Strait is being underestimated by markets. It is imperative not only for the Trump administration’s political self-interest but also for global economic stability that the duration of this war be measured in weeks, not months.

Consumer Discretionary

Hedgeye provides updates on 3 of their top Retail shorts. For GIII, they expect the next guide for the year to be an absolute disaster; forecasting a 20%+ cash flow hit from the the loss of major Calvin Klein and Tommy Hilfiger licenses back to PVH, while prior channel stuffing and tougher retail conditions could force the company to increase markdown support to key partners. Meanwhile, VFC is caught between a heavy debt burden and weakening brand momentum; Hedgeye believes a massively dilutive equity raise will ultimately be required. And finally, DDS remains a mispriced security, trading at ~12x EBITDA despite a sharply decelerating model and the company overearning by 800-1,000bp. That suggests that the real earnings power is between $10-20 per share. 5x earnings, is an appropriate department store multiple, suggesting 80-90% downside.

Healthcare

Sidoti reiterates their constructive stance on LMAT, arguing the company’s increasingly dominant niche positioning supports durable pricing power, margin expansion and visible multi-year growth. With price increases contributing meaningfully to organic growth and ~8% additional pricing expected in 2026, Sidoti sees LMAT as insulated from reimbursement and tariff pressures given its focus on critical, non-deferrable vascular procedures and predominantly single-use devices. The company will continue to benefit from the continued sales force expansion and additional European product approvals over the next several years. Backed by a strong balance sheet and capacity for accretive M&A, Sidoti increases their 2026 revenue estimate to $275.5m (from $264m) and EPS estimate to $2.86 (from $2.39). For 2027, they raise their revenue estimate to $291m (from $278m) and EPS estimate to $3.09 (from $2.67).

Technology

US expansion is the key swing factor for TEMN over the next 12 months. With a well-resourced US sales team, a localised product suite and a pipeline growing faster than any other region, GR20 sees favourable conditions for deal conversion in 2026. They also believe the recent “Claude Cowork effect” that weighed on software valuations is fading, with sector multiples appearing to have bottomed. In GR20’s view, current valuations imply limited terminal value in DCF models - an anomaly given TEMN’s positioning and growth prospects. The stock trades at an undemanding 4.2x/3.9x 2026/27 EV/sales and 11.9x/10.9x EV/adjusted EBIT.

Materials

Lucror broadly agrees with Moody’s downgrade, consistent with their “Negative” Credit Bias since Aug 24. Weak metrics are set to deteriorate further amid higher-than-budgeted capex at the Awak Mas gold project and subdued thermal coal prices. Leverage is projected to rise to c.7.0x Debt/EBITDA in FY26 (from c.6.0x in FY25) before easing toward c.4.0x in FY27 as gold operations stabilise. Liquidity is viewed as adequate over the next 12-18 months, but covenant headroom will tighten, particularly around the 3.75x Net Debt/EBITDA test. That said, the Newcastle coal benchmark has stabilised for almost a year now, so, Indika’s credit metrics may not worsen much more going forward and Lucror agrees with Moody’s outlook revision to stable. They maintain a "Buy" recommendation on the INDYIJ 8.75 '29s at 99.6/8.9%/2.7Y, as the high yield more than compensates for the weak and deteriorating credit profile.

Gold & Silver: Where prices move from here

In this presentation, Jeffrey Christian of CPM Group discusses what comes next for gold, silver, platinum, and palladium following last week’s sharp selloff, and explains why the pullback was not surprising after the rapid surge in prices. Jeff begins by looking at the US dollar, showing why claims of a “collapsing dollar” do not hold up. He emphasizes the importance of time horizons in market analysis, explaining how prices can be unsustainably high or low in the long run while remaining volatile for months or even years in the short run. Jeff then looks at the role of COMEX contract rolls and positioning, including how large open interest can affect price moves without implying any shortage of metal. He also reviews ETF activity across gold, silver, platinum, and palladium, explaining how gold ETF investors were net buyers through January, while silver ETF investors were net sellers, even as prices spiked.

Click here to watch.

Communications

Josh D’Amaro’s mix of leadership and operational qualities make him a strong choice to succeed Bob Iger as CEO. A 27-year Disney veteran, D’Amaro is viewed as a high-EQ leader who balances creative ambition with financial discipline. He is currently tasked with overseeing a $60bn capital plan over the next 10 years to turbocharge growth in parks, cruise lines and resorts, generating the FCF required to support the company’s riskier media transformation. While he lacks direct media experience, he has a proven track record of turning around underperforming assets and successfully navigating crises, including rebuilding the Experiences’ division profitability post-Covid. Paragon’s report includes interviews with former senior executives who worked with D'Amaro for more than 75 years combined.

Materials

Asymmetric highlights Daido Steel as an under-followed stock that is increasingly coming into its own. The stock has surged ~85% since they turned bullish in Jun 25, helped by a strong H1, driven by rare earth free magnet demand amid tighter Chinese export controls and robust marine valve orders. Even after the rally, Daido only trades at 0.86x PBR and ~13x FY3/27E earnings (+20% Y/Y), with relatively low foreign ownership. Looking ahead, Asymmetric flags multiple profit catalysts: potential synergies from acquiring Kobe Steel’s Koshuha specialty furnace, an improving semiconductor cycle, rising demand for rare earth-free magnets for HEVs, and expanding exposure to engine shafts and components across aerospace, energy, shipping and gas turbines - supporting margin and earnings upside over the next 1-2 years.

US Healthcare + Merger / Arb Catalysts: What’s next from DC

Healthcare

2026 is shaping up to be an active year for US healthcare policy, with President Trump's focus on affordability impacting Congressional and Administration priorities. Near term, Congress is considering spending legislation impacting clinical labs (Quest Diagnostics, Labcorp), diagnostics (Natera) and life science tools (Danaher, Thermo Fisher). Investors are also awaiting clarity on MFN deals and their impact on companies that have not yet signed agreements with the Administration. Beyond HC, Aldis also leverages their connectivity to provide timely insights and updates around M&A with regulatory catalysts, including Nexstar-Tegna and Union Pacific-Norfolk Southern. Contact us below for further information on events hosted by Aldis and access to their content library.

Earnings season screens

Mill Street has developed an "Earnings Screen Score" ranking methodology that draws on selected inputs from their MAER (Monitor of Analysts’ Earnings Revisions) stock database to identify companies which have strong near-term fundamental momentum going into an earnings report. Mill Street’s research indicates that companies scoring highly in their ranking have a much higher chance of near-term improvements in analyst expectations than those that score poorly. Stocks most likely to produce positive near-term analyst estimate activity in the next couple of weeks include Lam Research, Regeneron Pharmaceuticals and Teradyne. Bottom ranked stocks include LyondellBasell, Eaton and Marathon Petroleum. Click here to access the full report.

Materials

GMR is sceptical on a potential tie-up between RIO and GLEN, citing material integration and execution risks. They highlight stark contrasts in management culture and business models, alongside challenges around thermal coal exposure, sovereign risk tolerance and regulatory scrutiny given combined copper output. Assuming US$1.5bn of annual synergies, GMR estimates RIO could bid up to £5.40 per GLEN share for the merger to be, on average, neutral on Earnings/share and NCFO/share out to 2028. Following GLEN’s recent rally, GMR downgrades the stock to Hold and moves RIO to Sell on deal risk. Their proprietary Acquisition Rationale score reinforces caution: GlenRio scores just 9/18, a level that historically underperforms peers over the next 24 months.

Precious metals: What happens next?

In this presentation, Jeffrey Christian of CPM Group provides a market update on gold, silver, platinum, and palladium prices as metals continue to reach record levels. He explains why political developments, both in the United States and internationally, have become one of the dominant drivers of investment demand for precious metals, moving away from traditional economic fundamentals. Jeff discusses how rising political uncertainty and strained international relationships contribute to elevated investor anxiety and renewed buying interest in gold and silver. Jeff also addresses persistent misinformation in the silver market, including claims about shrinking inventories, paper versus physical silver, and alleged shortages.

Click here here to watch