No matches for this search

Try adjusting your filters or search criteria

Consumer Discretionary

ROST exceeded very high expectations delivering an impressive 17.0% comp with the majority driven by traffic and EPS of $2.02 - ahead of Chuck Grom’s Street high $1.95 estimate and guidance of $1.60-$1.67. Even more impressive, most of the uptick in transactions is coming from new customers thanks to improved branded merchandise, better in-store experience and refreshed marketing initiatives. This should improve confidence in ROST’s ability to “comp-the-comp” later this year despite difficult comparisons. Near term, Chuck raises his 2Q26 SSS estimate to 7.0% with EPS of $1.90, while FY26 and FY27 EPS increase to $7.80 and $8.75, respectively.

Retail predictions for the year ahead

Consumer

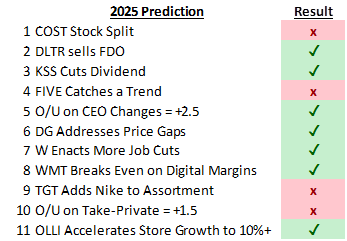

Looking back at GHRA’s 2025 Top 10 (+1) predictions, their batting average was good, hitting on 7 of 11 (see above). For the year ahead, their forecasts include: 1) Target announces an investment cycle on Mar 3rd with adjusted FY26 EBIT margin in the ~3.0%-4.0% range and a 2030 view of ~5.0%-6.0%. 2) Five Below launches Digital Loyalty Card. 3) Academy Sports adds another big brand…likely HOKA. 4) Costco unveils a special dividend and/or ramps share buybacks. 5) Ollie's embarks on large scale sales productivity effort. 6) Burlington takes a page (or two) out of the Ross Stores marketing playbook. 7) Someone gets acquired; BJ’s and Arhaus the most likely candidates. 8) Home improvement recovery gets pushed out…again.

Retail Cross Currents: 4 key themes & top stock ideas

Consumer

GHRA highlights an unusually volatile retail backdrop through late 2025 and early 2026, noting multiple “cross currents” affecting both consumers and retailers. Recent rating changes include downgrades for Dollar Tree (Reduce) and BJ's Wholesale Club (Hold), while upgrades cover Williams-Sonoma (Buy), Wayfair (Accumulate), Kohl's (Accumulate) and Dick's Sporting Goods (Hold). GHRA’s key investment themes emphasise: 1) stocks offering both EPS upside and multiple expansion (Five Below, Ross Stores, Burlington); 2) underappreciated turnaround stories (Kohl's, Dollar General); 3) selective “rate-trade” exposure favouring home furnishings over home improvement (Williams-Sonoma, Wayfair, Tractor Supply); and 4) secular winners / “Coffee Can” stocks (Walmart, Costco, TJX, Ollie's Bargain Outlet, Casey's).

Bulls continue to run

Vermilion’s outlook remains bullish on global equities (MSCI ACWI). David Nicoski and Ross LaDuke viewed the recent pullback as a buying opportunity and they were watching for $116-$117 support to hold on ACWI-US – an important resistance-turned-support level dating back to July 2024. $116 support held perfectly and they expect immediate upside to continue with both ACWI-US and the S&P 500 breaking above their 1+ month bull flag patterns. They are also upgrading Germany to overweight with RS on the DAX breaking out from a 2-year base. This leaves the US (S&P 500) and Germany as their only two country overweights. Buying Europe is easily their favourite idea currently, following the 9-month base breakout. As long as ACWI-US is above $116, the S&P 500 is above 5650-5670, and the EURO STOXX 50 is above 5030, the team see every reason to remain bullish.

Consumer Discretionary

New CEO Jim Conroy added to Paragon’s research pipeline - Conroy joins ROST from Boot Barn, where he created 640% alpha as CEO since 2012. However, his ManagementTrack Rating of 5.7 is a modest downgrade vs. the outgoing CEO Rentler's MTR of 7.0. Other stats include: Conroy is a "Builder" capital allocator: 70% of career capital allocated towards CapEx (Rentler is a "Capital Returner", allocating 69%+ towards Dividends & Buybacks). Conroy is an "Inconsistent Guidance Forecaster": Beats 49% & Misses 39% of the time (Rentler is a "Guidance Sandbagger": Beats 87% & Misses 7%). He has a low F.L.A.G. Risk Concern and very low historical Earnings Call Q&A Evasiveness (Conroy averaged 10% vs. Rentler's 27% over the last 5 years).

MSCI EM Index reversing 3-month downtrend

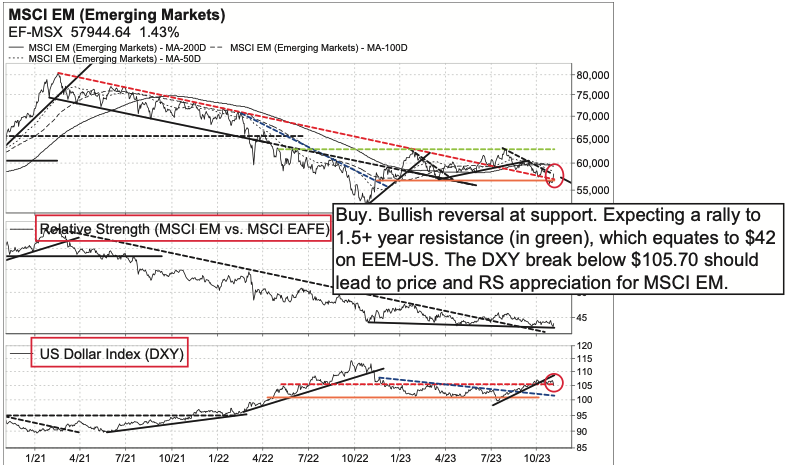

In Vermillion’s prior EM Strategy, Ross LaDuke discussed that MSCI EM (EEM-US) was again approaching major 10.5-month support at $37-$37.50, which has been their important line-in-the-sand throughout 2023, and that as long as EEM-US is above $37, Vermillion are buyers on this pullback. This support level held and EEM-US now displays a bullish 3-month downtrend reversal as the US dollar (DXY) appears to be breaking below $105.70 – all rather bullish signals suggesting this rally is just getting going -- BUY. Ross is bullish as long as $36.50-$37 support holds on EEM-US. His first target is $42, which is 1.5+ year resistance. Additionally, he remains neutral on EM vs. EAFE; the EAFE vs. EM ratio is moving sideways following the 2.5-year downtrend reversal.

Consumer Discretionary

Time to add more Off-Price Retail exposure - while Chuck Grom turned incrementally more positive on the OPR space when he recently upgraded TJX to Buy, he has been waiting for more “evidence” that middle-income shoppers would begin to trade down, while simultaneously looking for proof that inventory levels would improve. Commentary from Walmart, Target and Kohl’s suggests that this trade down is now occurring, while most retailers have made commendable progress since 2Q on the inventory front. As a result, Chuck upgrades ROST to Buy and increases his EPS estimates for FY22 to $4.30 and FY23 to $5.40.

Consumer Discretionary

Report by

A Line Partners

A

In their weekly report A Line uses a proprietary ranking system to build individual company performance history. Companies are graded A-C based on factors including product design, promotional activity and store feedback. Key takeaways last week:

ATZ - Grade A; scores 28/30, +2pts vs. previous week. Consistently positive feedback across the stores. The Super Puff is flying off the shelves (gone TikTok viral).

ROST - Grade B; 18/30, +2pts. Improved traffic trends driven by markdowns. Discounts are deep (e.g. women’s jeans at $7.99, $3 cheaper than last year). Sales boosted by cold weather.

Michael Kors - Grade B; 14/30, -3pts. Oct has slowed vs. Sept (lack of tourists and domestic customers who are not shopping as much in anticipation for the holidays). Increasingly aggressive promotions.

These retailers are primed for growth in 2022

Consumer Discretionary

Consumer stocks are climbing the wall of worry reflecting supply chain challenges, higher distribution expense, rising prices and tough comps. Hence, there is limited visibility on the consumer sector delivering yoy F22 earnings gains. JJK highlight a select few who are well positioned for growth, including the value focused off-price retailers (TJX, Burlington, Ross) and beauty leaders (Bath & Body Works, Estee Lauder, Ulta). Upgraded growth strategies and Europe’s emerging rebound should also drive strong upside at A&F, Capri Holdings, Lululemon, PVH, Ralph Lauren and Victoria’s Secret.