Technology

Sales Pulse has received multiple reports from channel contacts indicating that NOW has initiated a significant workforce reduction this week. While the company has not yet publicly disclosed the scope of the restructuring, employee reports and internal discussions suggest ~2,500 employees may be impacted (8% of the workforce). The cuts have impacted multiple organisations, including sales (AEs and Solution Consultants), international operations and engineering teams. The move has surprised employees and observers given recent commentary from the CEO suggesting AI-driven productivity gains and natural attrition would manage headcount. Channel feedback has been notably negative, with one contact saying the process is “creating chaos internally” and that the company has become “so top heavy” it is struggling to execute.

Technology

NTNX's Q3 revenue and EPS beat was aided by exceptionally conservative guidance and accounting / cost factors that may not be sustainable. Management had guided Q3 revenue to just 6-8% growth despite maintaining a higher full-year growth outlook, creating a favourable setup for a beat, similar to Q2. BTN also highlights rapid growth in contract assets, which contributed around three days of sales to revenue recognition over the past two quarters, more than enough to explain the reported beats. Meanwhile, deferred revenue has been broadly flat for two years and continues to decline on a days-of-sales basis, while deferred commissions suggest weaker new customer acquisition. Margins also appear supported by low depreciation, declining capex, and reduced cash R&D and S&M intensity.

Industrials

MYST highlights a short thesis on ANDG, whose shares have risen from a $16 IPO price in Dec 25 to c.$37. The near-term catalyst is a major lockup expiry on 15th Jun, when c.99m shares become available vs. current outstanding shares of c.13m, creating a potential “meaningful amount of supply” as 300+ US partners look to monetise up to $4bn of stock. Fundamentally, ANDG relied heavily on price increases heading into the IPO, but customers already appear to be pushing back. AI is also seen eroding pricing power, as Big Four firms automate workflows and move down-market while AI-native start-ups compete at lower price points. Tax Receivable Agreements that distort reported cash flow are another underappreciated element of the short thesis. TP $25 (30% downside).

Technology

The market has been spooked by ORCL’s AI infrastructure spending, but Richard Windsor thinks the economics may be better than feared. Q4 revenues and adjusted EPS beat expectations, but shares fell after-hours as the company guided to $70bn of investment this fiscal year. The bond market is also flashing caution, with ORCL’s CDS widening to 198bp from 43bp in Sep 25. However, Richard estimates revenue per GW at $15.8bn, based on ORCL's incremental AI/cloud capacity and cloud revenue growth, far better than OpenAI and other neo-clouds are managing to produce, implying an 18% five-year IRR on a Grace Blackwell-based build. Strong AI investment returns could drive upside to medium-term EPS estimates, while the stock's 22x FY27 and 16.5x FY28 PER look reasonable against forecast EPS growth of 18% in FY27 and 35% in FY28.

Greek Equities: Adopting a more cautious stance

ResearchGreece revisits their stock picks and assesses the political outlook ahead of the next parliamentary elections. Macro conditions remain solid, with Q1 real GDP up 2.0% Y/Y, although inflation accelerated to 5.2% Y/Y in May (+0.0% M/M). With the Athens Index up +11% YTD, valuation multiples of non-banks in their universe have expanded to 13.2x P/E and 8.0x EV/EBITDA 2027, leaving more limited upside. Combined with polls pointing to a hung parliament, ResearchGreece is turning more cautious on Greek equities. Banks remain their preferred exposure (solid outlook - volume, rates, asset quality) as a leveraged Greek macro play. They prefer National Bank of Greece, Bank of Cyprus, Piraeus and Optima. Outside banks, they favour selective infrastructure, industrial and defensive names such as OTE, Titan, PPC and Piraeus Port over consumer stocks and cyclicals.

Technology

Limited audit coverage raises questions over the reliability of its consolidated financials, particularly given that a large share of overseas operations is either unaudited or audited by other firms just as the company reports a turnaround. Capital allocation also remains a concern, with substantial net worth tied up in weak subsidiaries, a history of goodwill impairments and profitability heavily influenced by accounting judgements. Earnings quality warrants scrutiny, as recurring impairments, aggressive receivables provisioning assumptions, inventory write-downs and impairment reversals suggest reported profits remain highly dependent on management estimates and recoverability assumptions.

Jet-fuel panic turns contrarian opportunity

In the latest edition of David Scott’s A Strategist’s Diary, he argues that the jet-fuel panic has become an “ex-crisis”, with investors too quick to extrapolate higher fuel prices into a broader inflation problem. Instead, he sees demand destruction, airline fare discounting and rising supply from the US and China as evidence that the shock is already mean reverting. The investment implication is contrarian: sectors he would normally avoid, including airlines and state-owned Chinese oil/refining names, now offer compelling valuations. David highlights PetroChina and CNOOC as surprisingly well-run and still cheap despite strong prior returns, while also finding opportunities across global airlines including Spring Airlines, Delta, Ryanair, Eva Airways, IAG and IndiGo.

Hang Seng on the launchpad

Erik@YWR argues that the Hang Seng’s sluggish start to 2026 masks a much more attractive setup, with the index described as a “coiled spring” after moving sideways for 15 years in hard-currency terms. He sees 35,000 as achievable, supported by improving fundamentals: based on YWR’s approximation of 89 constituents, earnings growth is expected to accelerate from a 6% CAGR over 2015-2025 to 11% over the next 3 years. Key drivers include 17% EPS CAGRs at Tencent and Alibaba, 6% growth from the major Chinese banks, oil-price support for energy names, 26% growth from BYD and CATL, and a recovery in property stocks. With earnings revisions turning positive, Hong Kong property prices recovering (mainland China prices stabilising) and the index on <10x 2028 earnings, Erik sees meaningful upside.

Real Estate

Craig Huber argues that the near-50% YTD fall in CSGP’s share price has created an attractive entry point, with investor concerns around AI competition and Homes.com losses now overdone. His 2026/2027 adjusted EPS estimates are above consensus at $1.40/$2.00, with revenue forecast to rise 18.0%/15.4% to $3.833bn/$4.424bn and adjusted EBITDA to reach $833.8m/$1.142bn. The group also has $1bn remaining on its share buyback programme (representing ~7.5% of current m/cap). The stock trades at 16.8x 2027 adjusted EPS or 13.9x EBITDA. If you exclude the Homes.com losses (where there is a lot of flexibility in the expense base; sees losses dropping to ~$300m this year), CSGP is trading at only 9.4x 2027 EBITDA. Information services is a sector that historically trades around 25x EBITDA, if not higher. Craig is an “aggressive buyer” at these levels with a conservative $50 12-month price target, implying ~50% upside.

Materials

Hassan Ahmed is increasingly constructive on OLN, arguing that 1Q26 marked a positive inflection across all three segments after several years of estimate cuts and share price underperformance. Chlor-alkali fundamentals are tightening, helped by the cancellation of Chemours’ planned PCC chlorine project, limited North American capacity additions and Middle East-related disruptions, with an estimated 6-9% of global capacity currently shut. ECU pricing also appears to have stabilised after the post-2022 decline. Elsewhere, Epoxy returned to profitability after six consecutive quarterly losses, while Winchester is emerging from trough conditions as commercial ammunition stabilises and higher-visibility military exposure increases. With Beyond250 cost savings ramping, Hassan sees 2026 consensus expectations as undemanding and increases his 12-month TP to $36 (50% upside).

Industrials

ABM’s 2Q EPS beat was driven by stronger-than-expected revenue growth, with sales up 8.4% Y/Y and gains across all five segments for the fifth consecutive quarter. Technical Solutions, Aviation and Manufacturing & Distribution each grew by more than 15%, supported by organic gains and acquisitions. Sidoti’s FY26/FY27 EPS estimates of $4.03/$4.55 imply annual growth of 17.0% and 13.0%, respectively, while their FCF per share estimates of $4.25/$4.42 imply FCF yields of 10.0%/10.4%. ABM’s shares have traded at an average premium of 5% over the last 20 years to the S&P Small Cap 600 Index on a forward P/E basis but currently trade at a 34% discount. Sidoti maintains their Buy rating and $68 target, implying c.50% upside.

Industrials

EFN’s ~25% share price pullback over the past six months reflects concerns around lagging services revenue, moderating originations and potential AI disruption, but Veritas argues the fundamental impact is being overstated. Services revenue should recover as growth in Vehicles Under Management drives demand with a 12-15 month lag, while softer origination volumes have been offset by higher net financing revenue yields and growth in serviced-only VUMs. AI risk appears manageable, with the most exposed services representing only ~20% of annual delivery, while higher-touch offerings remain more defensible. Despite EFN’s stronger ROE profile, the stock trades below its five-year average P/E of 16.5x. They expect ROE to expand into the low-20% range and believe EFN's valuation multiple should re-rate as services revenue grows to the HSD range.

Defence Supply Chains: Hidden chokepoints, mispriced risk

The Iran conflict is not a regional event - it is a structural accelerant for the global Defence-Industrial Base. OMNISIGHT maps three converging chokepoints: China's gallium export controls (directly threatening F-35 radar integration timelines), Hormuz-driven sulphur disruptions cascading into propellant supply chains, and Qatar helium export risk affecting precision electronics. Combined, these create a butterfly chain that materially compresses production cadences for Tier-1 contractors in H2 2026 - a risk the market is currently underpricing. OMNISIGHT's institutional divergence analysis yields explicit ratings: Accumulate Lockheed Martin and BAE Systems; Hold RTX and Northrop Grumman; Reduce Rheinmetall, where a P/E of 90-100x leaves zero margin for delivery disappointment.

Alpha generating Healthcare Shorts

Healthcare

Bios Research publishes a new short idea that they believe is materially overvalued, with a m/cap in the $7-10bn range, significant ADV and ~50% downside potential. They also highlight additional Q2 and Q3 shorts (m/caps >$10bn) across biotech, healthcare services and medtech, alongside several M&A candidates and stocks that are attractive as a basket for investors looking to add exposure in what they believe is a new biotech bull cycle. So far in 2026, they have closed a long idea in Crinetics Pharmaceuticals for a ~59% gain and several shorts: ARS Pharmaceuticals (+46%), AbCellera Biologics (+43%), Summit Therapeutics (+42%), Butterfly Network (+34%) and TransMedics (+22%). Since inception in Feb 2012, Bios has published 194 short ideas with a c.70% absolute hit rate.

Consumer Discretionary

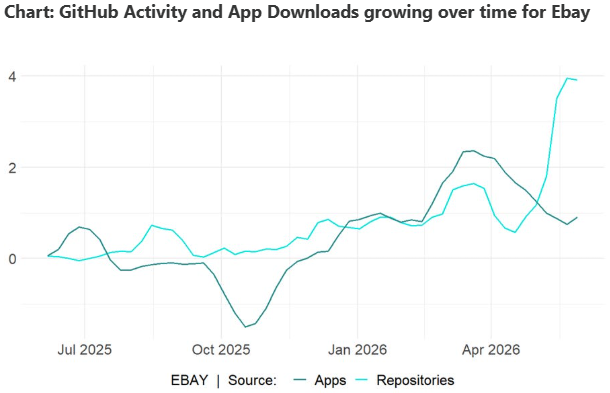

The company ranks in the top 20% of AnteData’s universe, reflecting a strong improvement in coding momentum during 2026. The signal is primarily being driven by rising App activity and exceptionally strong GitHub interest where developers are building pricing tools, arbitrage engines and inventory automations using EBAY as a pricing and transaction platform. AnteData sees the group’s focus on passion-driven goods, including auto parts, collectibles and luxury items, as increasingly important, with these categories now representing >30% of value traded. They believe EBAY can sustain c.8% annual revenue growth over the next 5 years, lifting sales from $11.5bn to $16bn and nearly doubling income to c.$4bn.

Consumer Discretionary

Alex Barron believes the acquisition is an important signal for the US homebuilder sector, supporting his view that the bottom of the cycle is here and now is an opportune time to buy into the sector at great valuations. The deal values TMHC at 1.24x 2Q26 book value, 1.17x Alex’s 2026E book value and 12.9x 2026E EPS. His fair value estimate was $72/share. While Berkshire is unlikely to pursue an immediate acquisition spree, the deal opens the door for TMHC to become a larger consolidator over time. Alex also notes rising sector M&A, including Dream Finders attempted hostile bid for Beazer Homes, which he thinks would likely need to move closer to 0.8-0.9x book value to succeed.

Technology

TEMN’s acquisition of Additiv strengthens its position in wealth management, particularly in the fast-growing mass affluent segment, while adding a cloud-native orchestration platform that accelerates implementation times, enhances customer journey management and supports the company’s AI strategy. Additiv brings attractive growth characteristics, including strong DD ARR growth, 138% NRR and a blue-chip customer base. The acquisition also expands TEMN’s reach across Europe, the Middle East and Asia-Pacific, with opportunities to scale through its global channels. While the price has not been disclosed, GR20’s analysis suggests the deal is unlikely to be expensive, potentially valuing Additiv at c.4-5x revenue. TEMN plans a gradual integration approach, reflecting lessons learned from previous acquisitions and aiming to maximise long-term cross-selling and synergy opportunities while limiting execution risk.

Investor Idea Event highlights several compelling Shorts

Revelare hosted a Buyside Event in London where short theses were shared for companies including: 1) Associated British Foods - Primark is caught in a competitive “no man’s land” and is being squeezed by Shein, Vinted and LEFTIES. 2) CSG - trades at peak earnings, driven by unsustainable, high-margin spot-market ammunition sales to Ukraine and its true revenue visibility is much lower than its headline backlog suggests. 3) IWG - the presenter questioned the company’s highly touted transition to a capital-light management / franchise model; sees the business as plagued by poor disclosure and aggressive accounting. 4) Vestas Wind Systems - utilities moving services in-house puts margins at risk and Chinese competition challenges a peak multiple.

Communications

New Street remains cautious on the stock, arguing that Italy is not large enough to offset the group’s Swiss pressures or justify its 80% FY26 EV/FCF premium to the sector. Switzerland still accounts for 73% of value and faces multiple headwinds, including Salt’s share gains, weak service revenue growth, reliance on sub-brand pricing to defend KPIs and ongoing fibre-driven capex. While Italy is now nearly 30% of value, New Street does not expect a major pricing recovery, as Iliad Italy is already on track to earn a viable c.8% FCF ROIC without raising prices. Even lifting Italy 2030 OpFCF by 20% would only raise SCMN's 2025-2030 OpFCF CAGR from 4.5% to 6.0%, leaving the stock looking expensive in terms of value to growth.

Uranium: Feeling hot

The Global X Uranium ETF (URA US, USD48.96) has been ranging net sideways since peaking at USD60.51 last Oct. The ETF fell as much as 34% from the high. A new classic chart pattern appears to be forming, a 7-month Ascending Triangle. A breakout would target USD90.00 – Chris Roberts will add to his initial long if such a breakout occurs. He remains bullish on Uranium and has established an initial position this week. Go 30% long at market. The initial stop loss is a daily close below USD39.15.

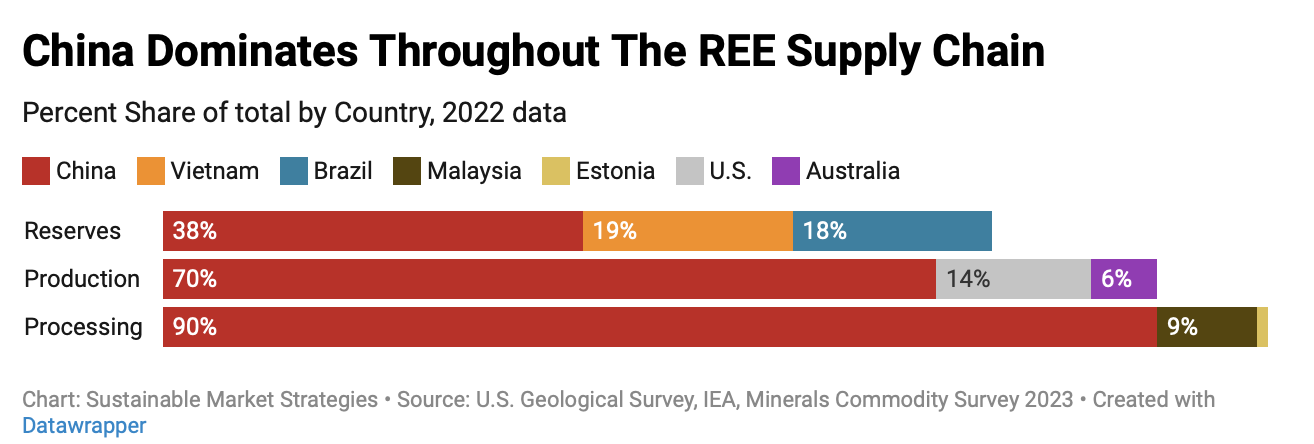

A critical materials reset

The demand story for transition materials has bifurcated: copper's case has strengthened, bolstered by a new AI infrastructure layer on top of persistent electrification demand, while nickel and cobalt face structural headwinds from the shift to new battery chemistry. Today, the bullish transition material thesis is just as much about major supply constraints as it is about structural demand. China's export control regime is a permanent feature rather than a trade negotiating tactic, and the processing bottleneck it exploits cannot be resolved through capital alone on any realistic investment timeline. The country processes 80-90% of the world's rare earth elements (see chart). Within the Sustainable Market Strategies universe, pure-play copper miners and recyclers remain their highest-conviction position. Among rare earth elements (REE) producers, the team add three new promising names to their coverage: Perpetua Resources Corp, 5N Plus Inc and Energy Fuels Inc.

Argentina: A battle of wills

Marcos Buscaglia focuses on the discrepancies between the IMF and the Argentine government that transpired in the recent IMF report. While the IMF sees GDP growth converging to 3%, the government hopes that reforms could lift growth up to 4.5%. The IMF projects inflation reaching single-digits by 2028, yet the government thinks the decline could be earlier and faster. The target set for FX reserve accumulation for the year is $8bn, but the IMF scenario is at least $10bn. The authorities promised to limit FX selling intervention and made no promise on the removal of lingering FX controls. Marcos says the government has implemented a more expansionary monetary policy, without compromising its FX and price stability targets, so far. The economy will continue improving somewhat in the coming month. Inflation will be closer to 2% in May. Marcos expects the central bank will likely keep rates around current 20% levels.

Consumer Discretionary

ROST exceeded very high expectations delivering an impressive 17.0% comp with the majority driven by traffic and EPS of $2.02 - ahead of Chuck Grom’s Street high $1.95 estimate and guidance of $1.60-$1.67. Even more impressive, most of the uptick in transactions is coming from new customers thanks to improved branded merchandise, better in-store experience and refreshed marketing initiatives. This should improve confidence in ROST’s ability to “comp-the-comp” later this year despite difficult comparisons. Near term, Chuck raises his 2Q26 SSS estimate to 7.0% with EPS of $1.90, while FY26 and FY27 EPS increase to $7.80 and $8.75, respectively.

Consumer Staples

Recent fieldwork and earnings results reinforce R5's upgrade from Sell to Buy earlier this year. Their thesis centres on improving merchandising and better store execution driving traffic, sales and gross margin recovery - trends which now appear to be emerging in both store checks and reported numbers, with comp sales (+5.6%) and operating margins (4.5%) beating forecasts. R5’s latest visits across multiple US markets suggest stores are “better, but nowhere near” where they ultimately need to be, supporting the view that the turnaround remains in its early stages. They also highlight a notable re-engagement from store employees, which they see as an underappreciated signal that traffic trends and customer experience could continue improving through 2026. In contrast to Walmart, where continued upside increasingly requires Amazon-like growth and margin characteristics, TGT “doesn’t have to be a superhero” for the equity to work. TP $197 (50% upside).

Materials

ESI is benefiting from an “acceleration in its growth algorithm”, driven by a structural shift away from consumer electronics to be more data centre / B2B driven. The market continues to underappreciate how materially the portfolio has improved, with enterprise customers now representing ~80% of sales (vs. ~60% in 2022) and gross margins expanding by >600bps (avg. ~50% gross margins and ~26% EBITDA margins over past 5 years when stripping out the effects of metals pricing). Growth drivers include Kuprion’s nano-copper technology, which could exceed a targeted $100m sales run-rate by 2028, alongside strong momentum from Micromax and EFC Gases, which are benefiting from growing demand in advanced electronics, semiconductor manufacturing, electrical infrastructure and aerospace application. Fermium forecasts revenue reaching ~$3.6bn by 2027 alongside mid-teens EPS growth.

Technology

DSG combines one of the logistics software industry’s strongest network-effect moats with a highly disciplined acquisition strategy. The key differentiator is the company's proprietary Global Logistics Network, which processes >24bn transactions annually and embeds DSG deeply into mission-critical compliance and supply-chain workflows, supporting gross retention in the mid-to-high 90% range and NRR above 100%. Management’s acquisition track record is also underappreciated, with 34 deals completed since 2016 generating >15% RoAIC while maintaining a conservatively financed balance sheet. Based on 12% annual revenue growth, stable‑to‑expanding margins, and an exit NTM non‑GAAP P/E of 22x, 2Xideas forecasts mid‑teens annualised total shareholder returns through FY33E.

800 VDC data centre plays

Technology

The shift towards 800 VDC data centre architectures creates a major new opportunity for SolarEdge and Enphase, whose distributed solar engineering expertise positions them well to handle the hyper-fast, chaotic load swings created by AI infrastructure. Both companies are repurposing existing R&D and already have products in testing, with Abacus arguing their architectures could compete effectively against traditional industrial incumbents such as Eaton and Vertiv. Abacus estimates the emerging market opportunity could reach ~$5-6bn by 2031 and believes successful adoption of 800 VDC systems could ultimately double earnings for both companies. Navitas is also highlighted since it provides the chips needed to make solid-state transformers work for companies such as VRT, ETN and ENPH; no matter whose product wins, NVTS benefits.

Beyond Lithium: The next battery boom

Industrials

Battery technology is at a commercial inflection point with the economics now favouring electrification over fossil fuels across an expanding range of applications, a trend accelerated by higher energy prices from the Iran conflict. China continues to dominate the supply chain, with CATL alone controlling ~39% of the global EV battery market and leading in grid-scale storage deployments, but Korean manufacturers offer accessible, liquid alternatives with deep ties to Western automakers and compelling technology road maps of their own. Given the geopolitical and technology risks, investors should build a basket of stocks: CATL for multi-chemistry platform execution at reasonable multiples; LG Energy Solution for contracted backlog and near-term profitability; Samsung SDI for solid-state battery optionality; and Amprius as a higher-risk tech position. BYD is also highlighted as a play on growing EV demand.

Communications

The latest reporting suggests SPCX is targeting a ~$1.75trn valuation, which would make it the largest IPO in history, but New Constructs argues the implied expectations are “out of this world”, with investors materially underestimating execution risk, competitive intensity and capital requirements. Their report highlights rapidly falling Starlink ARPU, misleading non-GAAP reporting and weak internal accounting controls, alongside governance concerns including minimal voting rights for IPO investors, extensive related-party transactions and potentially significant future dilution. They also note that ~80% of IPO proceeds are already earmarked for debt repayment and other obligations, while customer concentration risk remains elevated. New Constructs' reverse DCF analysis suggests the proposed valuation implies SPCX will ultimately generate both the highest revenue and highest NOPAT of any public company; sees >70% downside if revenue growth merely tracks historical rates.

CSN: Bridge loan supports a show me credit

Materials

EM Spreads maintains an Opportunistic Overweight on CSN bonds, arguing the market is pricing the credit closer to a distressed recovery trade than a conventional single B credit, despite no near-term liquidity event emerging from 1Q26 results. While leverage and FCF remain weak, a new US$1.2bn bridge loan materially improves funding visibility and reduces refinancing pressure, buying management more time to execute on deleveraging. The key catalyst remains tangible progress on asset monetisations, while EM Spreads sees the best risk reward in the CSN 4.625% 2031s and CSN 5.875% 2032s. The argument for the 2031s is more defensive, based on shorter duration and slightly better downside control, while the 2032s are the higher upside expression for investors willing to accept modestly more duration in exchange for incremental spread and carry.

Telfer vs. KCGM: The revival of Aussie icons

Materials

While the market remains cautious on Northern Star Resources given ongoing KCGM execution risks, potential cost overruns and weak near-term news flow, the company is nearing completion of a transformational ~A$1.8bn mill expansion to 27Mt/yr, part of ~A$5bn total investment into KCGM across FY22-FY28, which could ultimately restore production towards ~0.9Moz/yr by FY30. However, with management still needing to rebuild investor trust, GMR retains a Hold rating on NST. In contrast, they are more constructive on Greatland Resources, which is still in the early stages of reinvesting in Telfer / Havieron, with ~A$2.8bn of potential capex through FY32 supporting a pathway back towards ~0.4-0.5Moz/yr production by the end of the decade, alongside exploration upside at SLC and West Dome. Given the scarcity of >300koz/yr gold assets, GMR believes Telfer could become a strategic bolt-on acquisition for peers seeking scale in Australia.

China: Medical equipment and IVD outlook

Healthcare

Both segments appear to be approaching the end of a multi-year policy-driven compression cycle, with domestic pricing nearing a rational floor while overseas margins continue to improve through higher-end products and developed-market penetration. Horizon Insights views the sector as a “left-side re-rating” opportunity rather than a confirmed recovery, with investor positioning and expectations already deeply depressed. Among their preferred names, they highlight United Imaging as the clearest premium-equipment and global share-gain story (potentially supporting a US$300-400bn market-cap pathway over time); Mindray is seen as offering attractive value if pricing stabilises, while SonoScape and Snibe are highlighted for improving overseas mix and import-substitution potential.

Consumer Discretionary

New car price deflation continued to pressure WBC in H1, as legacy brands cut prices to compete with lower-cost Asian competitors, forcing inventory repricing and depressing margins. Rowan Goeller argues this is cyclical rather than structural, expecting margins to normalise through 2026, while the increased new car sales are growing the car parc – a positive for WBC in the medium- to long-term. He also highlights the group’s cash-generative model, data-driven pricing advantages and operational initiatives such as Inspectify, its in-house vehicle inspection platform. Rowan continues to view WBC as a growth business and maintains a R52 target price (45% upside).

Technology

CORZ moves sharply higher in Arete’s AI infrastructure rankings following a major expansion in its long-term power roadmap, with them now modelling 3.6GW of IT load and $6.3bn of NOI by 2032 - up from prior estimates of 1.9GW and $3.7bn, respectively. Arete argues demand for AI compute remains “off-the-charts”, while CORZ is becoming increasingly attractive to hyperscalers through the expansion of its Pecos and Muskogee campuses into gigawatt-scale AI data centre sites. Importantly, the company has leveraged its existing CoreWeave contract into $3.3bn of financing, giving it sufficient capital to begin pre-building new facilities before signing additional leases, which Arete views as a key competitive advantage. With leasable power expected to nearly triple over the next few years, Arete raises their TP to $55 (100% upside) and now ranks CORZ alongside Applied Digital as a top pick in colocation infrastructure.

Industrials

Hamed Khorsand’s bearish call on KRMN is already playing out with the shares down ~40% since his Sell initiation earlier this year, yet he continues to see material downside with a 12-month target price of $37. Acquisitions masked underlying weakness in the company’s core business during Q1. Excluding newly acquired maritime defence assets, revenue would have declined sequentially, despite a strong defence spending environment. Hamed also flags KRMN’s rising contract assets (unbilled receivables), which now exceed 32% of the company’s 12-month trailing revenue, alongside weak FCF generation. Valuation remains elevated at ~42x EV/EBITDA, while comps begin to look tougher as the year progresses.

Special Sits Idea Forum

MYST’s buyside events continue to deliver impressive performance (~19% avg. alpha on highlighted ideas at their previous Special Sits Forum). Their latest event featured a high number of potential takeouts / M&A plays, business separations, several Media stocks and various AI-related companies. The most compelling ideas included:

Chemours (CC US) - Refrigerant share gains + “free kicker” from steepening China TiO2 cost curve. TP $46 (110% upside).

ITT (ITT US) - High-quality pumps pure-play experiencing positive mix shift. TP $284 (45% upside).

Valmont Industries (VMI US) - “Non-obvious” AI infrastructure play benefitting from utility pole pricing inflection. TP $709 (35% upside).

Fundrise Innovation Fund (VCX US) - AI / Anthropic proxy trading at ~10x NAV with upcoming lock-up expiry catalyst. TP $50 (75% downside).

Technology

Following publication of its FY25 universal registration document, Iron Blue increase their CAP score +3pts to 30/60 (newly top decile and fertile grounds for shorting). This higher score reflects: 1) Increased stripped out costs (both restructuring and share payments). 2) Higher cost capitalisations. 3) Iron Blue’s conclusion that CAP may have fair value adjusted downwards the software on WNS’s balance sheet. 4) The dropping of organic growth as an alternative performance measure in a year of material acquisition revenue contribution. They also note that in FY26 Grant Thornton will replace PwC as one of CAP’s auditors - PwC had been in place for nearly three decades.

Materials

APAM is evolving from a cyclical European stainless-steel producer into a more diversified materials platform, supported by its integrated recycling activities and higher-value product mix, which VRS believes should improve long-term margin resilience and sustainability alignment. Recent performance reflects a challenging market backdrop rather than a deterioration in core fundamentals, with VRS highlighting operational efficiency improvements, the strategic importance of ELG recycling and the acquisition of Universal Stainless, which expands APAM’s aerospace footprint in the US. Europe’s increasingly protective stance on steel imports could also add ~€200m to EBITDA from 2027 onwards while improving utilisation rates. Their analysis incorporates a valuation framework combining six different methodologies spanning intrinsic, peer-based and probabilistic approaches.

Industrials

Investors remain far too apathetic towards European construction stocks, overlooking a multi-year infrastructure and housing investment cycle that could materially benefit BAM. The shares have hardly moved so far in 2026, despite the group reporting FY25 revenues up 9% Y/Y to €7.0bn, adjusted EBITDA up 20% to €400m and net profit almost tripling to €211m, while ending the year with €792m net cash, a €13bn order book and a new €40m buyback. BAM will issue new mid-term targets next year, but Europe’s 2026-2030 infrastructure strategy will release ~€600bn of funds further boosting the group’s order book, while civil infrastructure in UK currently faces a "herculean to-do list" that requires a 30-50% increase in investment over the next decade. TP €15 (55% upside).

Roche - SERD: Is lidERA being over-extrapolated?

Healthcare

Foveal published on adjuvant SERDS and sees a mispricing emerging between Roche and AstraZeneca, with the market potentially extrapolating lidERA into a broader commercial opportunity than is warranted, while underappreciating a more practice-aligned pathway elsewhere. The core debate is whether investors should be underwriting a broad SERD backbone in early breast cancer today, or positioning for a narrower outcome with a different catalyst path into 2027 that could shift relative value across the group.

Communications

CEO Johan Svanstrom is the wrong leader for RMV’s critical transformation. Despite bringing a background as a “digital native” who scaled Expedia’s Hotels.com to over $3bn in revenue, more recent roles at BIMobject and RMV reveal a polarising leader who is disinterested in operational details and relies on a closed circle of advisors. Svanstrom will continue to champion an AI strategy with high-level, buzzword-driven directives while delegating core business oversight, creating significant execution risk and key-person dependency on a team he has already begun to alienate. His chaotic leadership and lack of operational discipline are a direct mismatch for the rigorous execution and financial control the company desperately needs. Paragon’s research includes interviews with former senior executives who worked with Svanstrom for more than 32 years combined.

Financials

86Research recommends investors aggressively buy Futu following its 14% post-1Q26 preview selloff, arguing the decline significantly overstates temporary market-driven weakness with a US$231 price target, implying 59% upside from current levels. Analysts believe downward earnings revisions and geopolitical tensions triggered excessive selling despite strong rebounds in global equity markets since early April. According to channel checks, Futu’s user acquisition and net asset inflows have already recovered to pre-March levels, positioning the company to achieve its 2026 target of 800,000 net new funded accounts. 86Research also highlights FUTU’s dominant Hong Kong brokerage position, Southeast Asia expansion plans, strong management team, and industry-leading margins. Trading at only 11x 2026 earnings, the stock remains deeply discounted relative to historical averages and peers.

Industrials

Alstom shares fell 27% on 17 April and 36% since being added to Alumbra’s high conviction Active List in January, after the company issued a profit warning and disappointing FY27 free cash flow and EBIT margin guidance. In its 16 January initiation report, Alumbra had flagged that a significant year-on-year increase in unbilled receivables across H1 2026 and H2 2025 could indicate project cost overruns, weighing on future margins and cash generation. This was supported by its review of local subsidiary filings. Alumbra had also questioned consensus expectations for €700m of FY27 FCF, given recent cash flow benefited from €639m of unsustainable items.

Industrials

Epiroc remains a strong BUY despite lagging sector peer Sandvik’s recent surge. Since its 2018 spin-off from Atlas Copco, Epiroc has delivered consistently high returns, averaging 24% ROCE, well above its cost of capital. Its strength lies in a service-led business model: recurring services generate most revenue, while mining contributes 80% of sales. Global operations and extensive service networks create barriers to entry against rivals such as XCMG and Sany. Demand is supported by strong copper and gold markets, electrification trends, and growth in underground mining. With strong Q1 2026 orders, low debt, and expanding high-margin aftermarket services, AlphaValue sees around 30% upside and continued long-term growth potential.

Industrials

Another very successful Short idea from the Alumbra team as Primoris declined 50% on earnings last week after reporting disappointing Q1’26 results and significantly reducing FY’26 guidance due to cost overruns on renewables projects and lower-than-expected renewables revenue. Alumbra still have high conviction that the stock will decline further due to continued cost overruns on renewables projects and difficult revenue comps.

Consumer Discretionary

Stellantis’ latest results reinforce concerns that its finance arm is masking weakness in the core car business. While the market is focused on the potential for a recovery in earnings, the report argues that rapid growth in leased vehicles and heavy use of off-balance-sheet JVs is helping support sales and industrial free cash flow. With credit ratings now close to junk, higher funding costs could undermine this support and create further pressure.

Materials

Guangzhou Tinci Materials Technology plans to raise over US$1bn through a Hong Kong H-share listing in 2026. The company leads globally in lithium-ion battery electrolytes, LiPF6 and LiFSI, benefiting from EV and AI energy storage demand. Profitability appears to have bottomed in FY24, with FY25 recovery supported by volume growth, vertical integration and overseas expansion into Morocco, the US and Southeast Asia.

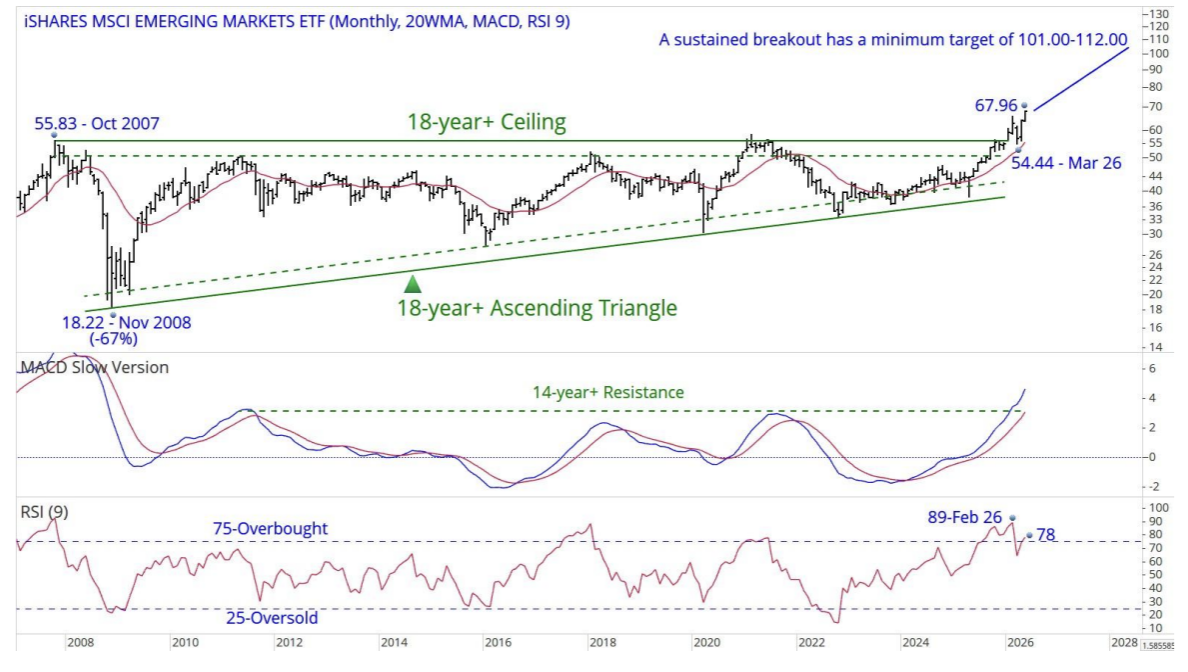

MSCI EM: The return of the Dodo

The iShares MSCI EM ETF (EEM US, last USD67.94) has successfully broken out from an eighteen-year-plus ascending triangle and is currently attempting to move beyond an eighteen-year-plus ceiling. While Chris Roberts points out that a sustained breakout above this resistance level suggests a minimum price target between USD101.00 and USD112.00, and the MACD indicates a significant improvement in momentum by clearing a fourteen-year resistance level, the nine-month RSI of 78 is approaching the very overbought threshold of 80. Consequently, it is prudent not to chase the current price; instead, the strategy is to wait for a setback toward the key support level at USD54.44 before considering a buy. Chris thinks he has found a dodo.

US S&P: Feeling good

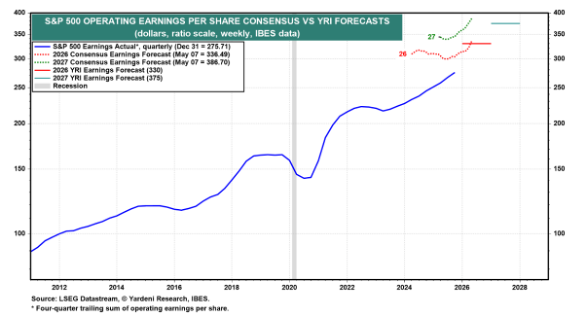

Ed Yardeni is raising his year-end S&P 500 target from 7700 to 8250. He has never seen consensus earnings expectations rise so quickly for the current and coming years as they have in recent months. The result has been an earnings-led meltup in the stock market. Ed is raising his EPS estimates to $330 this year and $375 next year, while sticking with his forward P/E range of 18.0-22.0, resulting in a year-end range for the S&P 500 of 6750-8250. His key assumption is that the economy will remain resilient, and so will earnings. Ed is also raising his probability of a continuation of the Roaring 2020s to 80% from 60% simply by merging it with his meltup scenario (previously at 20%), since he believes that any meltdown will be a buying opportunity and won't trigger a recession or bear market similar to the 1999-2000 Tech Bubble and Tech Wreck.

Consumer Discretionary

Lululemon shares are trading at both 52-week and five-year lows after a difficult period marked by product challenges and pressure on the brand’s core offering. The source notes that the company had strayed too far from its brand DNA, with limited colour in parts of the range and the departure of its senior merchant. However, early signs of improvement are emerging, including a tighter product offering, more colour and the appointment of a former Nike executive as CEO. While a full turnaround is likely to take time, The Retail Tracker sees potential for the stock to reach $175 over the next 12 months.