Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

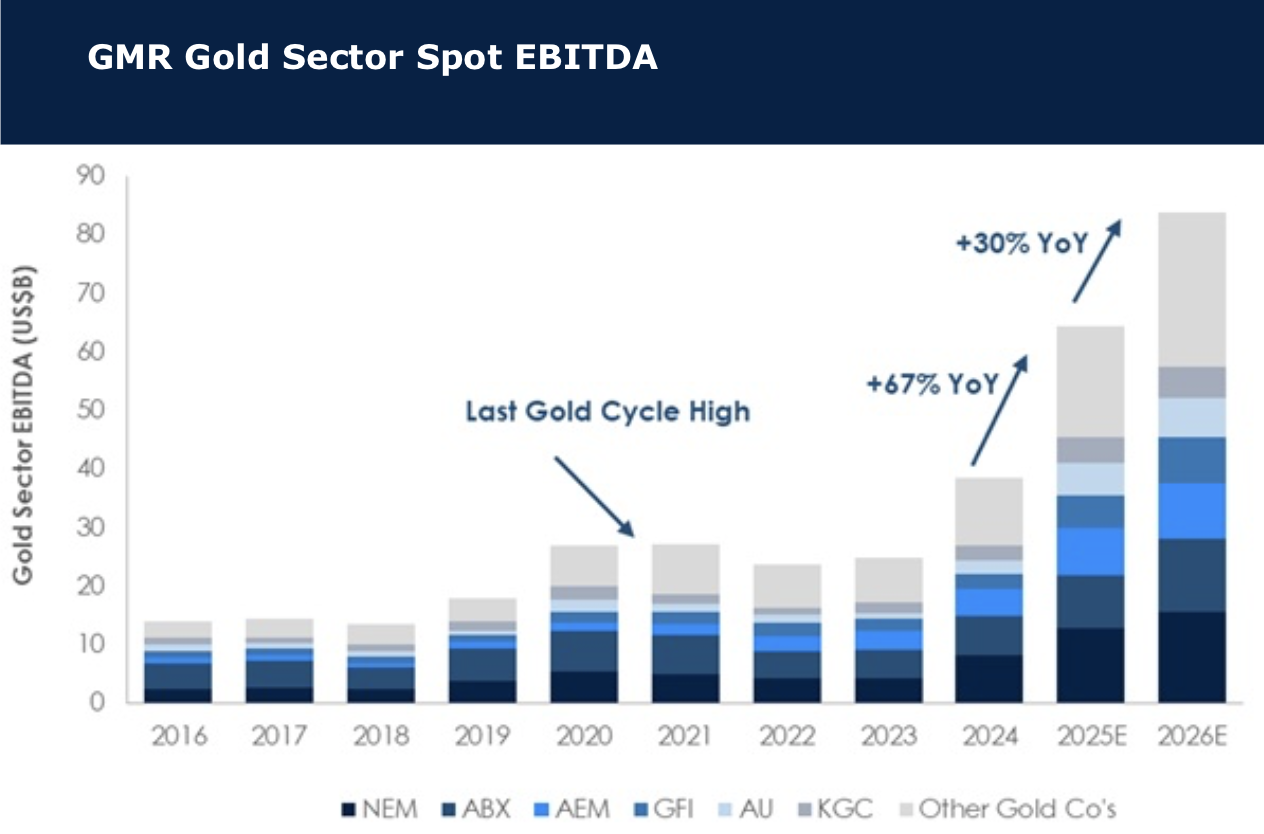

All that glitters is gold

Gold has been setting new highs through 2025 as the best performing major commodity. The music will come to an end, but David Radcliffe says that until that happens, a spot gold price over US$3,800/oz will generate some extraordinary returns. He examines the impact that spot prices could make to a sector that has already benefited from a robust 18 months. The 2026 consensus gold price is ~US$470/oz below spot, implying further upside if prices are maintained. On David’s expectations, spot prices into 2026 could lift sector EBITDA another 30% after an expected 67% lift in 2025. His covered gold stocks trade at a discount with spot P/NPV5 of 0.87x, or an implied gold price of ~US$3,330/oz, a 13% discount. There remains a value argument for gold miners, plus earnings momentum. David’s preferred exposures remain Agnico Eagle, Kinross and Northern Star of the seniors, and IAMGOLD, Equinox and Alamos of the more leveraged intermediates.

Edition: 221

- 03 October, 2025

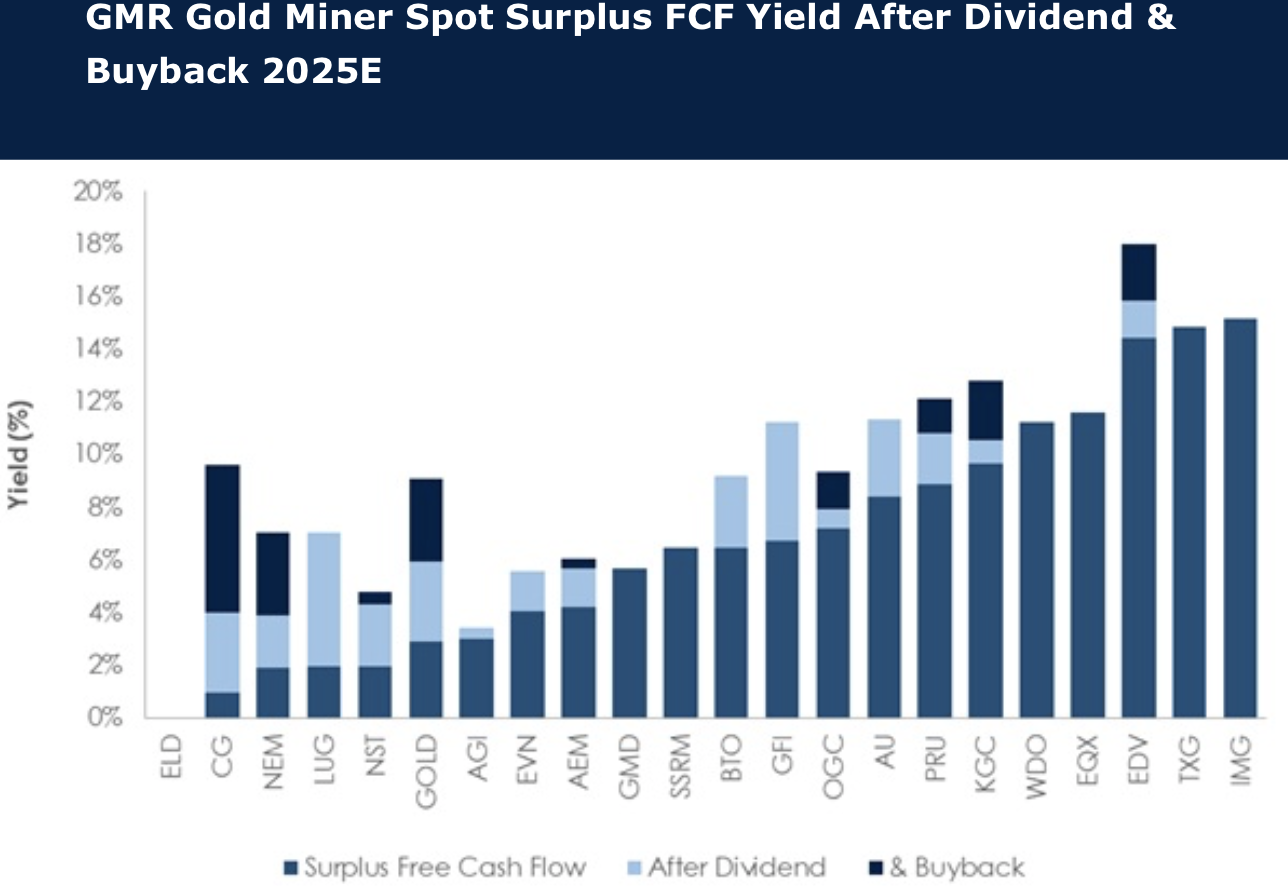

Gold: Are buybacks a fad?

In the face of meaningful cash surpluses, miners are repurchasing shares in record amounts. Some 40% of the Global Mining Research team’s gold coverage have active buybacks in 2025E, equating to ~US$3.7B of cash returns, a record level for the sector and equivalent to ~US$110/GEO. The impact on share prices is subject to debate. The team find that at spot gold the 2025E FCF yield of the sector after expected dividends and buybacks is ~4.6% (and ~8.5% in 2026E). So, shareholder return potential is still to the upside whilst gold prices remain elevated. Stocks least progressed (~20% or less) with buybacks include Carlyle Group, OceanaGold, Barrick Gold, Kinross Gold and Agnico Eagle Mines. Stocks trading at larger discounts to 2025E spot FCF include IAMGOLD, Torex Gold, Endeavour Mining, Equinox Gold and Wesdome Gold Mines. Preferred stocks of these are Kinross Gold, Agnico Eagle Mines, IAMGOLD and Equinox Gold.

Edition: 211

- 16 May, 2025

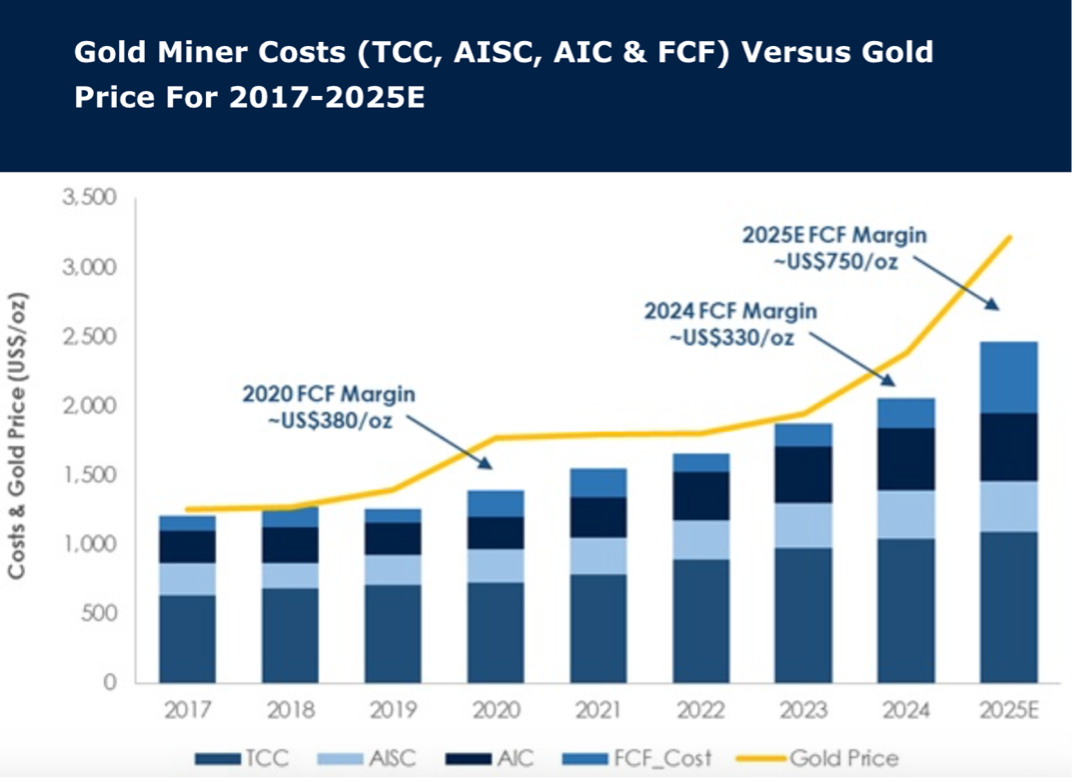

Gold: Higher prices, higher costs

As markets focus on record spot prices in 2025, price-linked costs and general mining inflation are also driving operating costs to record highs. In 2025 gold miner FCF costs are expected to reach a record ~US$2,465/oz, in line with inflation expectations. Positively, gold prices are rising faster and the 2025E FCF spot margin at ~US$750/oz is near double the last high in 2020. Gold miners (covered by Global Mining Research) with the lowest FCF costs in 2025 are Lundin Gold, Wesdome, Kinross and Agnico. Stocks with improvement in FCF costs from 2024 to 2025 are IAMGOLD, Torex and Equinox. Preferred gold stocks are BUY-rated Agnico (delivery and lower-risk portfolio), Kinross (risk reduction and execution), Equinox (transitions from project development to cash generation), IAMGOLD (Côté ramp up and derisking) and Lundin Gold (FDN continues to outperform).

Edition: 210

- 02 May, 2025

Buy Canada

Analysts at Veritas provide their best ideas for taking advantage of volatile markets. This series of reports features: 1) Veritas President and CEO Anthony Scilipoti providing an overview of why he is more bullish on Canada than the US. 2) Martin Pradier (Materials Analyst) on why he favours gold with Agnico Eagle Mines his preferred play. 2) Darryl McCoubrey (Energy) discusses why he favours pipeline infrastructure with Enbridge and TC Energy his best ideas. 3) Ben Butler (Utilities) looks at valuations in the sector with Fortis his top pick. 4) Liam Gallagher (Communications & IT) on why Quebecor is the best positioned operationally and from a valuation perspective. 5) Shalabh Garg (REITs) covers long-term interest rate trends and why he believes Chartwell Retirement Residences and Granite REIT are best positioned to take advantage of market dislocations.

Edition: 209

- 18 April, 2025

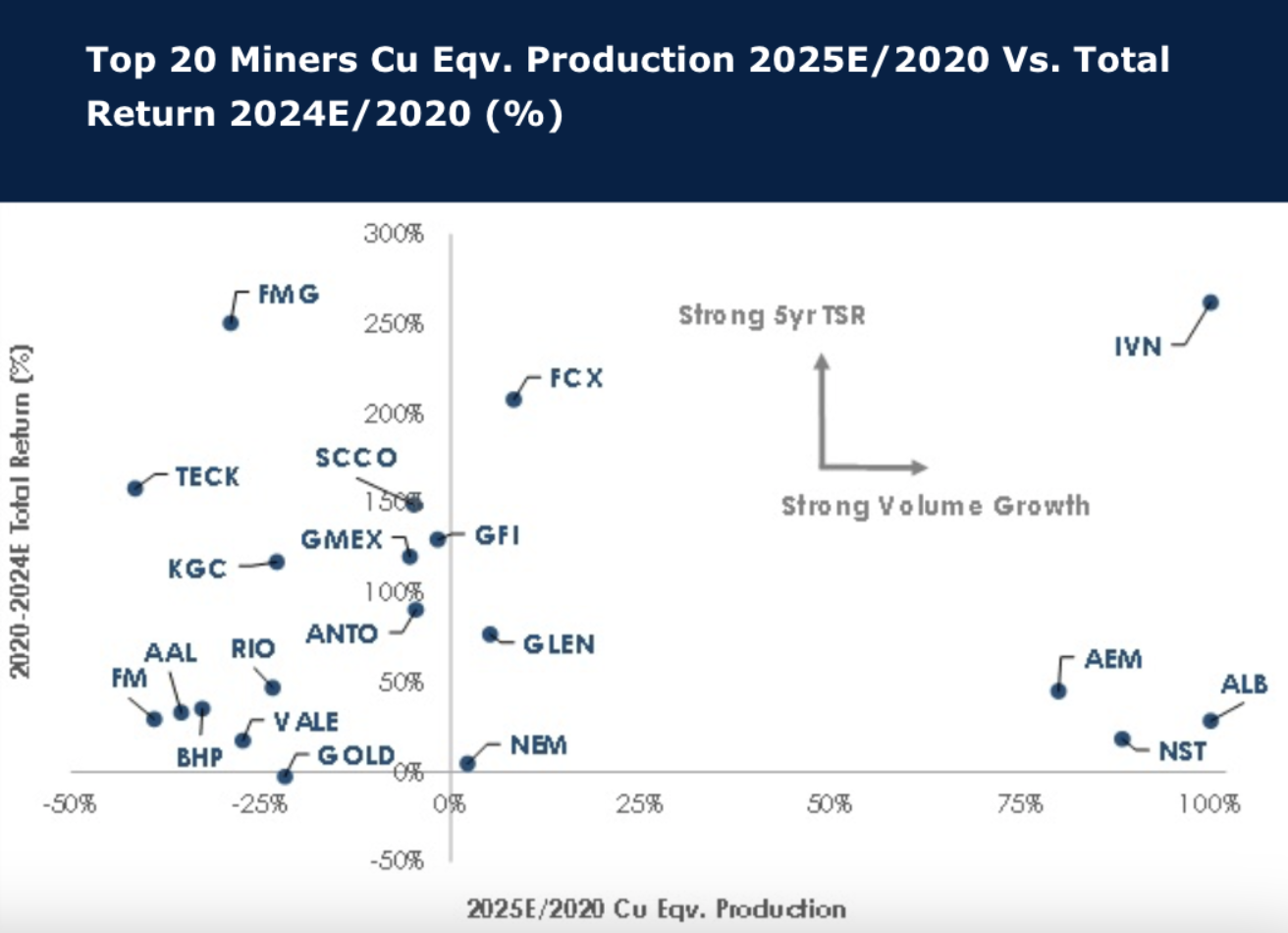

Large cap miners: Performance and growth are not related

As Sellside and Buyside set expectations for 2025, Global Mining Research examines the recent history of the leading miners. Interestingly, only Agnico Eagle Mines Limited, Albemarle Corporation, Ivanhoe Mines Ltd, and Northern Star Resources Limited are estimated to have materially grown through investment and M&A over 2020-2025E. In fact, most miners have shrunk in terms of Cu Eqv. Production, and exiting coal was a clear trend. The copper miners have outperformed, despite iron ore miners clearly returning the most cash to shareholders in dividends. Buybacks should have helped the share price return but there is little evidence this works. For over half the group, a ‘buy and hold’ strategy has not generated a robust return over the period. This reinforces the view that miners are to be traded.

Edition: 202

- 10 January, 2025

Gold: Can higher prices translate into cash?

All too often in the last decade for the gold sector, fully loaded costs have come close to equalling the received price. Therefore, one reason gold equities have likely recently lagged spot prices reflects a degree of market scepticism of the sector's ability to translate higher prices into “cash”. Unfortunately, the senior producers have often been key protagonists, but this isn’t the case for all gold stocks. Herein, David Radclyffe updates the sector cost analysis including highlighting Free Cash Flow (FCF) costs and FCF costs plus dividends, seeking to identify those stocks that could bank the proceeds of higher spot prices in 2024. The notional spot margin after base case dividends in 2024E for Agnico Eagle Mines / Barrick Gold Corp / Newmont is ~US$395/GEO, up from US$200/GEO in 2023. However, the best cash notional margins in 2024E could be delivered by Evolution Mining, Lundin Gold, Centerra Gold, and Barrick Gold Corp.

Edition: 186

- 17 May, 2024

Barrick Gold (ABX CN) Canada

Materials

Defence wins championships - gold's precedent of outperforming amidst real GDP loss and high inflation offers a defensive diversification opportunity for Veritas’ V-list model portfolio (1-yr +8.95% vs. S&P/TSX Composite -3.87%). The new ABX combines low-cost assets with a proven CEO that will not destroy value in expensive acquisitions. ABX is trading at low P/E and EV/EBITDA multiples compared to Newmont and Agnico Eagle despite higher profitability per ounce of gold produced, a higher dividend pay-out and an attractive buyback programme in place. TP C$32 (40% upside).

Edition: 139

- 08 July, 2022

How to pick a gold stock in 2022

Global Mining Research’s BUY and SELL signals served investors well in 2021 despite some market disconnect between equity price and numerous variables, including dividends. This year, David Radclyffe sees the gold sector shifting more to a growth/scale focus over returns/balance sheets; so, more M&A, growth investment, inflation impacting margins, lower dividends and a focus on ESG. David’s latest report looks for stocks that match the investment themes within the sector. Key picks include Agnico Eagle (new BUY signal), Barrick Gold, Northern Star Resources and Endeavour Mining.

Edition: 129

- 18 February, 2022