Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Overlooked opportunities in YWR’s QARV rankings

Why do China, shipping, iron ore, hardware, Brazil… all stand out if you screen high ROE’s with low valuation? Erik@YWR sees it as scepticism about global growth on which he is taking a contrarian view. Following this month’s review of YWR’s QARV rankings key themes include: 1) A massive China bull market has only just begun. 2) Opportunities in iron ore, where Fortescue, Rio Tinto and Kumba are delivering ~20% ROEs at <12x P/E despite China’s property crash. 3) The Taiwanese semiconductor supply chain stands out as highly profitable and undervalued. Everyone focuses on Nvidia and the datacentre buildout but misses the whole Taiwanese supply chain behind this. Tokyo Electron and ASML also screen well. 4) Brazil is overlooked, with names like Itau, Vale, Ambev and B3 all screening well. 5) Container shipping - supply-chain diversification could sustain tighter freight rates than investors expect.

Edition: 220

- 19 September, 2025

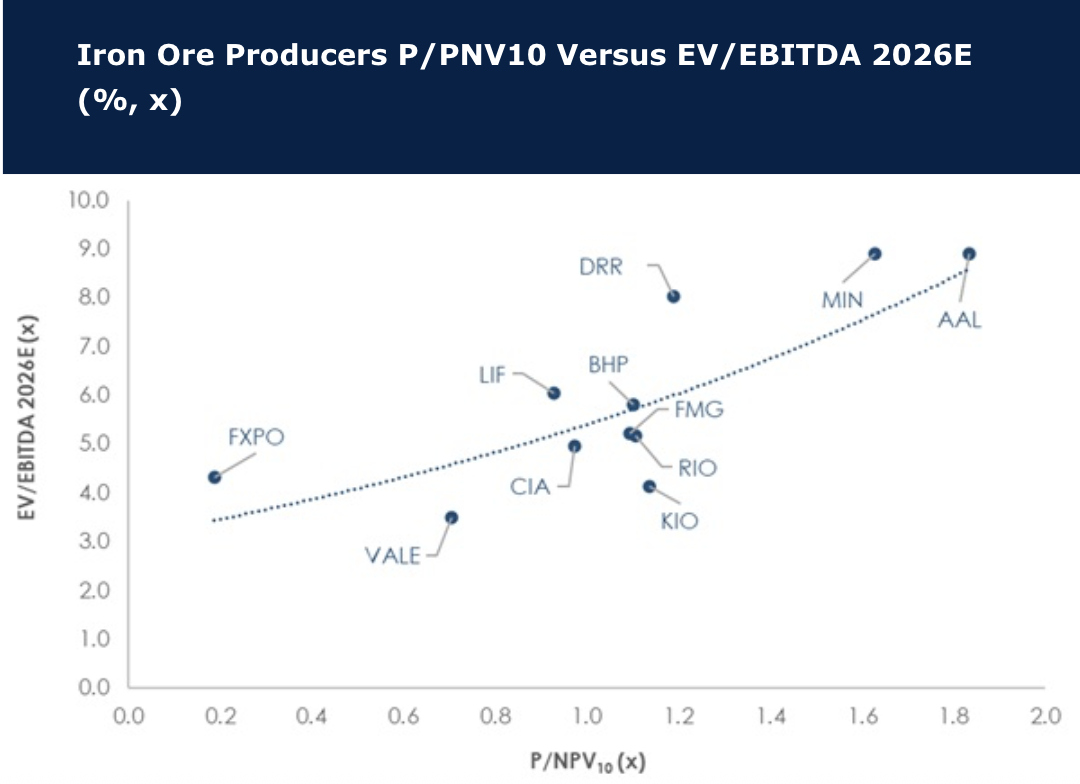

Iron ore is too big to ignore, but headwinds prevail

Iron ore seaborne supply is increasing at a time when steel demand is ailing, and David Radclyffe points out that this rightly makes investors nervous. However, the spot iron ore price has proven to be quite resilient this year at ~US$100/t. The headwinds may have dissuaded some investors, but at $378bn the iron ore market is simply too big to ignore in mining. As demand rolls the cost curve is key to sustaining volumes, and David assesses the LT price at US$95/t (US$101/t). Iron ore pure plays and diversified miners trade at 1.1x P/NPV10, and a prospective next two years average EV/EBITDA of ~5.8x and dividend yield of ~4.4%. Relative to other sectors this is reasonable, but high compared to historic levels. In the diversified iron ore-rich miners David prefers buy-rated BHP, then Vale, while in the pure plays it is Labrador Iron Ore Royalty. Overall, he remains underweight iron ore, with sells on key pure plays. Herein, Champion Iron is upgraded from sell to hold.

Edition: 219

- 05 September, 2025

Is the diversified model dead?

Materials

GMR recently published a review of the leading mining stocks’ performance over the last five years. For the diversified miners this highlighted weak TSR and overall negative returns stripping out cash payouts. A critical issue facing the group, especially the iron ore-dominated miners, is how to restructure their portfolios for the long-term. GMR reviews six key questions: 1) Is the diversified model dead? 2) Can dividends be sustained? 3) Miners exited coal but should it have been iron ore? 4) Shrinking to greatness might have merit? 5) How to increase EV materials exposure & in which commodity? 6) Is M&A the answer? BHP is their preferred pick, with Glencore second. Vale is very cheap, but it is hard to see a catalyst.

Edition: 204

- 07 February, 2025

BHP (BHP AU) Australia

Materials

On several metrics Rio Tinto now looks more attractive than BHP, but the difference is not that marked and partly explained by BHP’s large market cap. P/E, P/CF, EV/EBITDA, FCF yields and dividend yields are somewhat similar. For the coming year which one outperforms may be as simple as aluminium vs. met coal price moves, with copper favouring BHP. However, information flow in 2024 possibly favours RIO with good news from Oyu Tolgoi. With a positive outlook for copper and met coal, GMR prefers BHP for 2024 (upgrades to Buy; TP A$52). This is a non-consensus call with most preferring RIO. For best value and yield they prefer Vale.

Edition: 175

- 08 December, 2023

Falling nickel prices hitting higher cost producers

After a good 2022, nickel prices are now feeling the pressure of rising Indonesian production and generally soft economic conditions. Although nickel equities don’t appear expensive for the long-term, shares are now fighting a headwind of lower prices and margins are compressed enough that several would be in difficultly should prices weaken another 10-20%. David Radclyffe’s views are mostly negative to neutral, his preferred nickel equities are IGO and Sherritt, while he has SELL ratings on Vale Indonesia, Norilsk Nickel and Nickel Industries.

Edition: 166

- 04 August, 2023

Materials

GMR examines how much Vale Base Metals is worth - this includes the former Inco assets predominantly in Canada, and two copper and one nickel mine in Brazil. They forecast attributable ~325kt copper and ~160kt nickel in 2023, with 30% growth long term. GMR estimates a value of $14bn or ~$3.00/share, based on DCFs, or 23% of the miner's M/Cap. However, with typical premiums Base Metals could see ~$4.00/share, representing a significant hidden option value. A partial sale would allow investors to see more clearly what the assets are worth, and by difference, see how cheaply the iron ore and pellet side of the business is trading (at 0.6x P/NPV10).

Edition: 163

- 23 June, 2023

Iron ore: Falling prices pausing, or the cycle restarting?

Iron ore prices recently bounced off US$100/t, raising the question whether this represents a pause in the correction, or perhaps early signals that the price cycle is restarting. Sentiment continues to focus on broad demand risks especially in China, nevertheless Chinese crude steel production continues to annualise at +1Bt/yr, with the rest of the world’s demand recovering. David Radclyffe believes investors are getting close to an opportunity to start accumulating iron ore stocks; iron ore producers trade on a prospective 2023 FCF and dividend yield of 9% and 8% respectively. David’s preferred exposures are Vale, Fortescue Metals Group and Labrador Iron Ore.

Edition: 141

- 05 August, 2022

Diversified miners becoming less diversified

The three leading diversifieds have worked hard in un-diversifying themselves in recent years, becoming more and more iron ore focused, with fewer points of differentiation. David Radclyffe finds that nearly all investment ratios favour Vale (FCF yield 15%, EV/EBITDA 2.6x), then Rio Tinto and finally BHP Billiton. For as long as iron ore can hold around US$100/t, expect average cash return yields of 8-12% in 2022E. BUY Vale with a target price of $15.40.

Edition: 140

- 22 July, 2022

Investment opportunities in iron ore despite uncertainty

Despite uncertain Chinese growth rates and hence iron ore demand, along with rising inflation and the Russo-Ukrainian war, David Radclyffe believes there may be more time to stay invested in the iron ore sector. With FCF yields remaining high for pure plays and diversifieds (~14%), investors should look for strong dividend yields (~9%) and cash returns this year. The big global diversifieds continue to offer better value than the pure plays, with Vale the preferred single entry, followed by Rio Tinto. For pure plays, David’s preferred exposure is Fortescue Metals Group, a non-consensus call.

Edition: 133

- 14 April, 2022

Nickel in turmoil after hitting $100,000 per ton

David Radclyffe’s team reviews the listed nickel equities in a world of increasing geopolitical and LME market tension, and volatile price swings that will continue throughout 2022. After a very large market deficit last year of ~130kt he estimates a balanced market in 2022 with price forecasts raised from US$7.45/lb to US$11.75/lb. There are very few investable nickel equities left, but GMR prefers IGO and Nickel Mines, and Vale among the diversified miners.

Edition: 131

- 18 March, 2022

Materials

Pass-the-parcel - you can only give so much away before there’s little left to unwrap. Divesting the Petroleum business leaves BHP with little to differentiate it from Rio Tinto and Vale. BHP should have used its petroleum expertise and customer base to build a hydrogen / ammonia business taking a leaf from Fortescue’s playbook. From a ROCE and CO2-e perspective the met coal business would have a greater overall impact on the business if it were divested. However, the problem appears to be a lack of interested buyers.

Edition: 117

- 20 August, 2021

Steel Gaining Strength: EM active fund ownership has a lot further to run

Materials

While the turnaround started last year, allocations to the steel sector still remain well below even the levels seen in late 2018. Only 55% of the funds in Copley’s analysis currently hold exposure to the sector. That is 10% lower than in Dec 2018 and some 40% lower than early 2008. Vale, Kumba Iron Ore and Posco are currently fund managers' preferred stocks, but all 3 remain a long way off previous peaks in ownership, so if this is a cycle similar to the one that lasted between early 2016 and late 2018, EM fund ownership has a lot further to go.

Edition: 111

- 28 May, 2021