Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Lifco (LIFCOB SS) Sweden

Industrials

Karl Redin (Subsidiary CEO) purchased 26,350 shares at SEK 381, spending €920k. This is his eighth purchase and over 10x what he has spent on prior buys; the most recent was in Jul at SEK 367. The purchase occurred on the same day as the stock rose sharply after reporting Q3 earnings. This is an unusual buy, into unusual strength. Martin Linder (Subsidiary Head) also recently purchased shares spending €190k - a large purchase for him. Smart Insider has had a positive rank on this stock since early last year, based on buying from Per Waldemarson (CEO), Anna Hallberg (Director) and Martin Linder (Senior Officer). The stock has moved higher and insider buying has continued. Waldemarson made his most significant purchase in Jul, spending €1.3m and then spent an additional €300k in Sep. This is now the fourth time Smart Insider has renewed their +1 rank since Apr 24.

Edition: 223

- 31 October, 2025

India: US tariffs hit 50%

Teneo discusses rising US-India trade tensions after the White House announced an additional 25% tariff on Indian imports - lifting the total to 50% - over India’s continued purchases of discounted Russian oil. The move threatens up to USD 20-30bn of India’s USD 41bn goods trade surplus with the US and could trigger 500k-3m job losses in price-sensitive export sectors. India cites market and energy security needs and is unlikely to reverse course in the near term, given political and defence ties to Moscow. While exemptions for electronics or pharma are possible, risks extend to services exports if H1B visa rules tighten and could be a first step in decoupling India’s IT sector from the US. New Delhi’s options range from diversifying export markets to partial accommodation with Washington, but for now it is keeping all negotiating levers open.

Edition: 217

- 08 August, 2025

Communications

NBIS plans to establish a data centre in the UK just a week after raising $1bn via a convertible debt offering, underscoring its accelerated capital expenditure strategy. The announcement coincided with media reports of Nvidia's plans to invest in the UK. The growing availability of Blackwells should benefit revenue mix as the year progresses. Hamed Khorsand forecasts revenue to grow from $55.3m in 1Q25 to $292.2m in Q4 for a full year amount of $607.8m. He expects revenue to reach ~$1.5bn in 2026 with NBIS generating adjusted EBITDA of $379.1m. Reflecting this outlook, he raises his target price from $60 to $80, with the shares already up ~80% since his Jan 2025 initiation.

Edition: 214

- 27 June, 2025

Iran’s potential threat to oil markets

Unsurprisingly, oil prices jumped in the aftermath of Israel’s strikes against Iran. Wolfang Munchau ponders over the reasonable worst-case scenario. One must consider the 3.3m b/d of exports that could be lost, although this will pale in comparison to Russia’s 9-10m b/d before war with Ukraine, not to mention that most of the oil goes to China and is relatively sanctions proof. Should Iranian oil export infrastructure be targeted by Israel, OPEC spare capacity (est. 5.3m b/d) could absorb the damage. However, should Iran try to block the Strait of Hormuz in retaliation, this would potentially severely limit Iraq, Kuwait, Saudi Arabia, and the UAE’s ability to deliver oil to the world market. This would be extremely risky for Iran, with severe diplomatic repercussions with all Gulf states. The US is, so far, keeping its distance from the spat, but directly threatening global oil supplies could change that.

Edition: 213

- 13 June, 2025

Global liquidity continues to slip lower

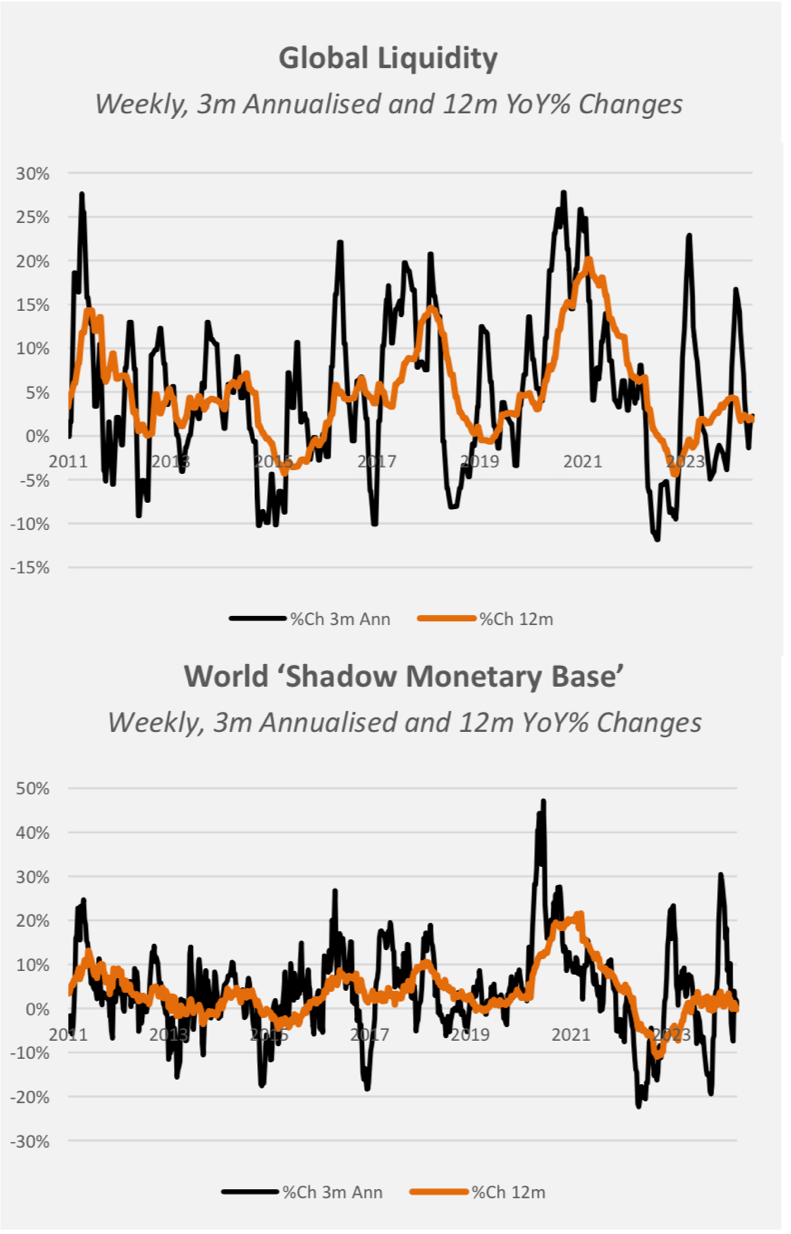

Digging deeper into the data, Michael Howell comments that there has been some improvement in central bank liquidity growth thanks largely to the PBoC, ebbing bond volatility, and a faltering USD. These are liquidity-positive, but ongoing QT among other major central banks – including the Fed despite this week’s better numbers and weakening bond markets are liquidity-negative. Global liquidity growth has dipped to +8.1% in 3m annualised terms. A continued slide in liquidity through the rest of Q2 will put pressure on risk assets and liquidity-sensitive cryptocurrencies in Q3. For now, risk asset markets and cryptocurrencies are being supported by the Q1 liquidity upturn, which saw global liquidity expand by over US$5trn. A typical liquidity cycle lasts 5-6 years trough-to-trough, and although Michael originally expected the current cycle to peak in Q4, the downside risks to economic growth and easing central banks will see the cycle peak in early 2026 instead.

Edition: 212

- 30 May, 2025

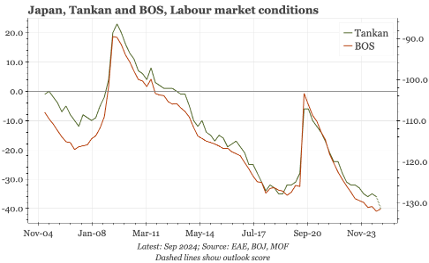

Japan: Solid data again

Paul Cavey notes that the latest data releases were constructive: the December Reuters non-manufacturing Tankan recovered from recent weakness with the outlook looking strong; the Q4 business sentiment survey from the MOF was solid, with the labour market tight; and PPI inflation rose again to the highest in more than a year. While manufacturing sentiment remained soft in the Reuters Tankan for December, non-manufacturing sentiment bounced back towards cycle highs, and respondents were even more optimistic about the next 3M. That helps allay concerns, driven by the recent weakening in both the Reuters and PMI surveys, of a real slowing of non-manufacturing activity. In addition, anecdotes in the Reuters survey suggest that the BOJ's hoped-for virtuous price-wage cycle remains intact.

Edition: 201

- 13 December, 2024

Technology

ARLO recently announced it had reached 4m paid accounts approx. 4 months after achieving 3m accounts. While the pace of growth is most likely the result of catch-up calculations related to ARLO’s partner Verisure, this should not take away from the magnitude of the increase as Hamed Khorsand expects a portion of the sequential increase was the result of retail subscriber additions. He raises his 12-month TP from $17 to $24 (45% upside) ahead of the company reporting Q2 results supported by ARLO exiting 2024 with a higher ARR than he was originally forecasting.

Edition: 190

- 12 July, 2024

Consumer Staples

CFO-Elect Monish Patolawala's ManagementTrack Rating* of 0.8 is in the bottom 4% of the 1,250 CFOs on the platform and is a significant downgrade to the 5.3 MTR of ADM's existing C-Suite. Patolawala destroyed (113%) alpha as a CFO at 3M; he has 9 "Level 2 & 3" career F.L.A.G. Risks (Financial, Legal, Audit, Governance Flags); a mixed incentive hit rate (achieved 50% of his incentive compensation targets 2020-2023); and is classed as an Inconsistent Sandbagger Guidance Forecaster (beats 51% and misses 28% of his financial guidance to investors).

*The MTR model employs a statistical ML algorithm to predict executive / company outperformance relative to their sector. It utilises 200+ signals and over a 10-year back-test a MTR long-short portfolio generated an average annual alpha of 8% with a 90% hit rate.

Edition: 190

- 12 July, 2024

Fourlis (FOYRK GA) Greece

Financials

ResearchGreece are positive assuming Fourlis will sell an additional 13.3% stake and deconsolidate Trade Estates, using the proceeds to reduce net debt and grow retail sales - mostly IKEA with new stores - at E715m with EBIT at E50m by 2027, both lower than guidance of E750m and E60m in 2026. Seasonally weak Q1 results were promising with sales rising +3.8% yoy and EBITDA turning positive at E0.8m from -E0.3m. RG estimate the retail business is currently valued at 3.8x EBITDAL 2025, +50% implied upside.

Edition: 188

- 14 June, 2024

Technology

Questionable quality of 4Q24 results - 1) Revenue had an extra six days but only rose by $8m or 0.6%. MRVL also picked up $13.7m from lower deferred revenues. 2) Ramped up Variable Considerations - a $10m change is worth 1 cent in EPS. Did MRVL load up this account to help sales and EPS going forward? 3) Accrued Warranty Expense fell - $26.9m potential boost in income or 3 cents in a quarter where MRVL only met estimates. 4) Adds back stock compensation - rose to 10.9% of sales - 2.6 cents to non-GAAP EPS. 5) Adjusted EPS also added back $42.3m in product claims that were paid out - 4.6 cents and is not expected to recur going forward. 6) Cuts to R&D spending.

Edition: 185

- 03 May, 2024

Euro area inflation

Riccardo Trezzi estimates that in April the core harmonised index of consumer prices (HICP) grew 22-24bps MoM (sa). This brings the 3m/3m (ar) to 2.5%. The 3m/3m (ar) is marginally below the YoY, signaling that the annual variation should moderate further in the coming months. However, the 3m/3m is now going sideways (or in moderate acceleration), therefore the 2.5% appears as a reasonable target for the YoY going forward. Overall, the issue remains the same of recent months: yes, the EA is disinflating, but the current most likely scenario is for the YoY of core HICP to reach 2% but then rebound up in H2. An important factor is the persistency of HICP services.

Edition: 185

- 03 May, 2024

In the shadows

Latest weekly measures derived from central bank balance sheet data showed global liquidity growing at a 2.3% 3m annualised clip. This isn’t the full story; the improvement is due to a base effect. In nominal terms, it actually slipped by US$86bn last week, with the Shadow Monetary Base acting as the main driver. Four of the five major central banks are involved but the largest footprints are those of the US Federal Reserve and the People’s Bank of China. Collateral values have also slipped. Michael Howell had warned of a Q2 2024 dip in liquidity, but he continues to expect liquidity conditions to improve in the second half of the year.

Edition: 185

- 03 May, 2024

Industrials

ARLO's stock has underperformed the fundamentals as investors seem keen on guessing when growth will slow down. The leader in home monitoring IP cameras has maintained its rate of quarterly net subscriber adds throughout 2023 and is poised to cross 3m paid subscribers by the middle of 2024. The introduction of a new security service and lower price camera options should enhance its market share and provide greater ability to generate positive FCF. Management anticipates a record-breaking Q4. Hamed Khorsand continues to believe the stock is being treated more as hardware business than for the recuring service revenue. 12-month TP $17 (85% upside).

Edition: 174

- 24 November, 2023

Oil: The pendulum continues to swing

Economic sentiment with respect to the US remains fickle, the pendulum swinging between sanguine optimism and recession fears. Vandana Hari notes the impact on crude of the changes, with Brent and WTI being yanked up from 1-month and 3-month lows after Chairman Powell’s recent comments. Tensions in the Middle East continue to run high around the Israel-Hamas conflict and crude will maintain some fear premium as long as it drags on. Should there be an actual supply disruption, crude could well surge into the triple digits, but that is not Vandana’s base case scenario. The 3m b/d of OPEC/non-OPEC output cuts are set to run into the year-end and hold a floor under crude. Vandana is NEUTRAL sentiment for the near-term (to mid-Nov) and mildly BEARISH for H2 Nov – H1 Dec.

Edition: 173

- 10 November, 2023

VPBank (VPB VN) Viet Nam

Financials

Chi Dung Ngo (Chair since 2010) splashes out more than US$55m as he purchases 70m shares in VPB. This is Ngo's fourth reported acquisition, by far his largest and the highest price he has paid. His most recent buy was five years ago in Dec 2018 when he spent US$18.3m below VND 10,000 per share. This is a confident purchase from the Chair, paying roughly twice the price of his prior purchase. Stock Rank +1 (highest rating).

Edition: 173

- 10 November, 2023

Industrials

SPX’s Iron Blue score increases by +5 y/y to 21/60. This reflects: 1) A decade high (10% PBT adj) in stripped out one-off costs. 2) Balance sheet contract assets rising to £12m from £3m. 3) PPE capex exceeding depreciation by 19% PBT adj, a decade high. 4) Lengthened expected life for plant and machinery (from 8-10 years to 10-15, above Capital Goods peers). 5) Likely higher net finance charge post €225m debt refinancing (Sep 23). 6) Additional accounting policies disclosure highlighting management discretion when accounting for cost of inventories. 7) Bad debtor provisioning at a decade low but debtors overdue by >90 days and not provisioned up to 9% of receivables (2021: 5%, 2020: 3%).

Edition: 164

- 07 July, 2023

Industrials

Xiuguo Tang (Non-Executive since 2014) purchases more than 1m shares, spending ~US$1.3m and increasing his holding by 29%. Tang has a good record as a buyer and Smart Insider previously ranked the stock twice based on his purchases: in May 2018, when he bought at HKD 2.69 and in Mar 2021 at HKD 8.53, both proved to be very well-timed. It's encouraging to see him buying again at this higher price level with the stock close to a multi-year high. Stock Rank +1 (highest rating).

Edition: 163

- 23 June, 2023

Financials

Six insiders spent a total of $4.8m buying stock at ~$57 per share. Gregory Norden (CEO) splashed out $3m. John Adams (Non-Exec) purchased $297k of stock in his largest buy and his first since 2016. Stephen Ellis (Non-Exec) spent $379k - his only purchase in the last 10 years. Furthermore, Peter Crawford (CFO), Richard Wurster (President) and Todd Ricketts (Non-Exec) all bought stock for the first time. While this is likely a co-ordinated cluster of buying post SVB's collapse, these are material purchases. Stock Rank +1.

Edition: 156

- 17 March, 2023

Asian central banks lead the upturn

Latest weekly data show major Central Banks’ aggregate liquidity edging higher (+0.4%) in local currency terms. The numbers confirm the trends noted in recent weeks; Asian Central Banks are leading the liquidity upturn and with some vigour. Next in line is the US Federal Reserve where liquidity conditions have stabilised. The ECB and Bank of England are lagging. Liquidity expansion in US dollar terms has decelerated to 13% (3m annualised rates). The sharp slowdown from the previous week’s +27% rate reflects a pause in the US dollar’s downwards trajectory.

Edition: 154

- 17 February, 2023

Jio (RELIANCE IN) India

Communications

It is rare for a single company to be able to change the direction of an industry globally, but New Street thinks that is what happened at Reliance Industries AGM where Mukesh Ambani, the Chairman of RIL and founder of Reliance Jio announced a target of 100m 5G FWA subscribers in India in coming years. For context, New Street estimates there are currently around 2-3m FWA subscribers globally. Jio’s announcement on its own therefore turbocharges the entire FWA industry. FWA in EM today is analogous to 2G mobile in 2000, with outsized returns likely given modest market expectations and strong underlying demand.

Edition: 144

- 16 September, 2022

Consumer Discretionary

A complete disaster - six quarters in a row of declining results, despite management talking about a turnaround. Yes, negative cash flow is now (only!) $411m, instead of -$600m, but there is now no growth in subs (4Q22 was the lowest quarter for net sub adds in PTON history; 1Q23 will be worse) and the churn rate almost doubled! PTON is hitting the wall at 7m total members and <3m paying members. This is exactly what Tom Chanos predicted when he first shorted the stock at $102 back in Sep 2021. The whole bull story is destroyed. Tom cuts his target price to $5.00, but the stock will most likely go to zero without a buyout.

Edition: 143

- 02 September, 2022

Fed’s QT summer lull weakens US Dollar

Michael Howell comments that the latest weekly balance sheet data from major Central Banks show aggregate liquidity in local currency terms shrinking by just 3.5% (3m ann.). The same trend is evident in global liquidity measured in USD but to a much greater degree. The lull in Fed QT continues and has coincided with dovish comments by Fed Chair Powell that the Fed funds rate has reached a “neutral” level. This has thus far outweighed a faster pace of tightening at the ECB and BoJ. The USD has reacted accordingly; from its mid-July peak, when the US unit hit parity with the €, it has lost some 3% versus the euro and pound sterling, and nearly 4% against the yen.

Edition: 142

- 19 August, 2022

ECB and Bank of Japan add to QT

Michael Howell reveals that major Central Banks’ balance sheet data shows aggregate liquidity shrinking at an increasing pace (-13.7% 3m ann. in local currency terms). ECB liquidity is shrinking at the fastest rate in three years (-9.9% 3m ann.) and reflects the end of net asset purchases from the start of July. The sharp downturn in the BoJ data (-1.8% vs. previous +21.7%) is puzzling, given the BoJ’s repeated commitment to a loose policy stance. Whether it turns out to be a temporary blip to iron out the previous spike, or the start of liquidity tightening, remains to be seen.

Edition: 140

- 22 July, 2022

Technology

No surprise that management continues to be unable to find an anchor shareholder - no doubt they are hoping for a full acquisition to help extricate themselves from the mess that has been created, but Teun Teeuwisse suspects that any interested party will come to the same conclusion that he has: 1) Real cash generation is non-existent. 2) Net debt is materially different from the net cash reported - normalising trade working capital alone increases debt by €153m, normalised VAT and social securities adds another €55m. 3) The equity is almost worthless - €54.3m or €0.51 per share vs. current share price of €5.30.

Edition: 135

- 13 May, 2022

Eyebright Medical Technology (688050 CH)

Healthcare

The global market potential for ophthalmic drugs, consumables and devices will exceed US$100bn in the coming years - as a highly innovative company with strong R&D capability Eyebright looks well placed to benefit. Its existing major product lines are: 1) Cataract Intraocular Lens (IOL) - Eyebright’s market share has doubled from 5% in 2018 to 10% in 2021 (without profit margin erosion) and domestic brands are expected to continue to take market share from foreign brands. 2) Orthokeratology Lens (OK Lens) - Eyebright has seen a phenomenal increase in sales having sold 21.5m pieces in 2021 vs. 2.3m pieces in 2019!

Edition: 135

- 13 May, 2022

The big liquidity squeeze continues

Weekly balance sheet data from major Central Banks show liquidity in local currency terms edging lower (latest -6.3% 3m ann.). The US Federal Reserve has led the 2022 downturn. This tightening has propelled the USD higher, forcing monetary adjustments in USD-linked economies. Mid-week saw not only the Fed hike rates but also the Reserve Bank of India and Brazil among others. Furthermore, non-US Central Bank liquidity is being devalued as the dollar strengthens. In USD terms, global liquidity is shrinking by some 24% (3m ann.): Michael Howell’s liquidity indicator started in 2010 and has never been so low.

Edition: 135

- 13 May, 2022

Analysing share transactions made by directors & senior employees

Identifying ‘Smart Insiders’ enables clients to generate alpha. Recent highlighted transactions include…

Puma (PUM GR) - Bjorn Gulden (CEO) purchases €512,000 at €63.99, taking advantage of recent share price weakness - he is a rare buyer and previous purchases have been timely.

Watches of Switzerland (WOSG LN) - Two directors make their largest purchases. Teresa Colaianni increases her stake by 56% and Robert Moorhead by 42%.

Kezar Life Sciences (KZR US) - Franklin Berger purchases $1.3m of stock at $16.25. He has a great record in Essa Pharma, another company where he is a director. Interesting to see him making this large purchase given the stock has more than doubled in a year.

Edition: 132

- 01 April, 2022

MENA emerges as a key growth region for the video game industry

Saudi Arabia, UAE and Egypt will have a combined 85.8m gamers (vs. 65.3m in 2021) generating $3.1bn in games revenue by 2025 (5-year CAGR of 13.8%) - growth will be driven by higher spending per user, additional government support (e.g. Saudi Arabia and UAE have introduced policies to encourage game localisation as well as hosting major esports tournaments) and more gamers entering the market. Nearly half of the MENA population is under 25 years old and have grown up as digital natives with gaming playing a huge role in their entertainment.

Edition: 127

- 21 January, 2022

Consumer Discretionary

Don’t get run over by this IPO - the proposed $80bn valuation is equivalent to the Mkt/Cap of General Motors and implies it will sell 3m vehicles in 2030, nearly four times the number of Tesla vehicles produced over the past 12 months. RIVN has yet to manufacture a meaningful number of vehicles and competes with well-capitalised EV upstarts as well as incumbents which have decades of experience and multi-billion dollar plans to expand EV production. The stock is worth $13bn at best (84% downside).

Edition: 122

- 29 October, 2021