Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Nexperia dispute highlights Europe’s semiconductor dilemma

Technology

The escalating dispute between the Dutch government, China and chipmaker Nexperia has become a flashpoint in the global semiconductor power struggle. With parent company Wingtech already on a US trade blacklist and facing tighter restrictions, Nexperia’s plan to separate its Chinese and European operations is now in jeopardy. The export ban poses an immediate risk to Europe’s industrial supply chain, especially in the automotive sector. Finding and certifying alternative suppliers could take months, echoing the chip shortages of 2021/22. Strategically, it spotlights the West’s push for technological sovereignty and the Netherlands’ pivotal role in the China–West tech decoupling. Several (Dutch) companies could be affected including ASML, NXP, Philips and ASM International.

Edition: 222

- 17 October, 2025

ASML (ASML NA) Netherlands

Technology

Arete’s report titled "The Capex Conundrum" focuses on: 1) The broader growth backdrop for leading-edge semi demand and the disconnect in ASML and wider WFE estimates into 2026/27. 2) Capex for key customers which should see significant upside over this cycle, boosting EUV demand and delivering above consensus revenues and EPS through 2027E. 3) The ongoing China capex contraction which is now captured in consensus numbers and stock sentiment. 4) Why there has been a disconnect between N2 capacity growth and EUV unit shipments. 5) Risks around the EUV roadmap and the possible move to 3D DRAM and how that might impact unit demand. 6) Valuation risk/reward, especially against the backdrop of recent sell-side downgrades and negative broader investor sentiment towards WFE, looks attractive.

Edition: 221

- 03 October, 2025

Overlooked opportunities in YWR’s QARV rankings

Why do China, shipping, iron ore, hardware, Brazil… all stand out if you screen high ROE’s with low valuation? Erik@YWR sees it as scepticism about global growth on which he is taking a contrarian view. Following this month’s review of YWR’s QARV rankings key themes include: 1) A massive China bull market has only just begun. 2) Opportunities in iron ore, where Fortescue, Rio Tinto and Kumba are delivering ~20% ROEs at <12x P/E despite China’s property crash. 3) The Taiwanese semiconductor supply chain stands out as highly profitable and undervalued. Everyone focuses on Nvidia and the datacentre buildout but misses the whole Taiwanese supply chain behind this. Tokyo Electron and ASML also screen well. 4) Brazil is overlooked, with names like Itau, Vale, Ambev and B3 all screening well. 5) Container shipping - supply-chain diversification could sustain tighter freight rates than investors expect.

Edition: 220

- 19 September, 2025

ASML (ASML NA) Netherlands

Technology

AIR raises their TP to EUR 1,000 (45% upside) - 1Q25 sales hit EUR 7.7bn with gross margin improving to 54%, driven by EUV demand. Despite order normalisation from Q4 highs, Upgrades and Services reached EUR 2bn, bolstering earnings stability. ASML’s High NA EUV systems, now priced at EUR 350m, further boost profitability and widen its tech lead. Long-term, ASML expects EUR 44–60bn in annual sales by 2030. With the shares trading at a -35% discount to their 5-year average, the US semiconductor industry set to pay 100% of the extra levy charged by Mr Trump on ASML equipment shipped to the US and Chinese rivals far behind, AIR sees this as a compelling entry point into a global semiconductor monopoly.

Edition: 211

- 16 May, 2025

ASML (ASML NA) Netherlands

Technology

Kinngai Chan argues that most of the risk for FY25 such as slower than expected demand recovery and expanded export restriction into China have been priced into the stock. He expects the demand for ASML's EUV lithography tools to recover and accelerate through 2025 as he sees higher performance requirements for AI-related applications in both the datacentre infrastructure as well as endpoints products. While there remains some uncertainty about the growth of AI-infrastructure capex in the near-to-medium term due to the discovery of new more efficient LLM model algorithms, Kinngai thinks the AI adoption in the client devices could easily offset the possible weaker WFE spend for infrastructure.

Edition: 204

- 07 February, 2025

Technology

While revenue guidance was largely in line with Street expectations what caught investor attention was the "insane" margin outlook. TSMC is clearly doing a good job extracting value from Nvidia’s high margin AI business. The steady tone of management is likely to temper a surge in negative sentiment in response to ASML’s caution. There was no change to TSMC’s capex outlook, which ought to help investors return to the deeply sold-off Lam Research and Applied Materials. KC Rajkumar expects the stock to drift up, but not without volatility driven by investor concerns regarding sustainability of the AI rally and potential new restrictions on the export of AI chips. He raises his 2024 estimate to NT$2.87tn/NT$44.6 and 2025 estimate to NT$3.67tn/NT$56.7. TP NT$1250.

Edition: 197

- 18 October, 2024

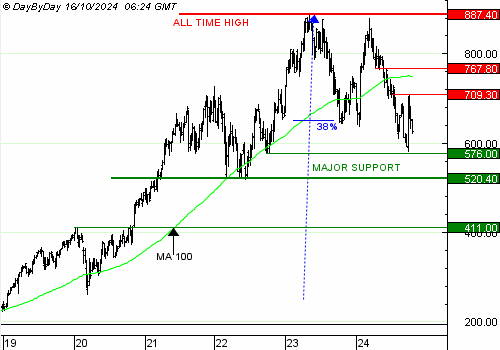

LVMH and ASML drag Europe down

European stocks fell earlier this week as ASML’s guidance cut was compounded by disappointing sales at LVMH. Recent share price action at LVMH (see chart) has resulted in the medium-term trend switching to neutral, but not bearish, meaning buying weakness is still a reasonable strategy. €520/€500 is the level investors should expect to be tested in the near term. Meanwhile, ASML is playing around its major support, the 38% Fibo of the rally since 2020. It had briefly been broken a few weeks ago, hence this new test has a very low probability of re-establishing a rise. Buying will not be an option for a while.

Edition: 197

- 18 October, 2024

ASML (ASML NA) Netherlands

Technology

The combination of economic-related delays and China realising that stockpiling ASML equipment ahead of further bans might not help them very much has caused the company to lower its outlook for 2025 resulting in a large correction. Furthermore, while AI demand currently shows no sign of abating, when the AI correction comes, as it inevitably will, this will set back expectations further. The net result is a stock that is on 25x 2025 PER and has a question mark over its medium-term growth profile. Semiconductor companies that do the manufacturing tend to be cyclical and at this valuation Richard Windsor is still not a buyer.

Edition: 197

- 18 October, 2024

ASML (ASML NA) Netherlands

Technology

ROCGA’s Cash Flow Returns On Investments based online platform provides a systematic framework to compare and value companies. ASML scores high on multiple Factors and their DCF valuation tools points to significant upside. Apart from their proprietary economic returns and conventional valuation indicators, data points such as EV/IC against ROIC/WACC are also available. Their interactive tools allow you to model and value one of 2000 companies across Europe and the US. A free consultation and trial can be arranged on request.

Edition: 195

- 20 September, 2024

ASML (ASML NA) Netherlands

Technology

ASML really does not want to talk about China. Richard Windsor's biggest concern following the company's disappointing Q1 results is the fact that China made up a colossal 49% of revenues. China is currently buying everything it can get its hands on in anticipation of further restrictions from the US, Japan and Netherlands. This means that demand for equipment is being pulled forward and is setting the equipment industry up for a correction once Chinese buying slows dramatically. The net result is that at 45x 2024 PER and the risk of a miss in 2025, ASML’s shares look far too expensive.

Edition: 184

- 19 April, 2024

BE Semiconductor (BESI NA) Netherlands

Technology

Chip design is going through a Copernican revolution, switching focus from “small is good” to “big is good”, and hybrid bonding is a key enabler going forward. Like ASML did in lithography, New Street expects BESI to strengthen its competitive position towards the domination of die attach, as it continuously improves the accuracy and throughput of its tools. They expect the shipment of hybrid bonding tools to take off this year, and to grow steadily, as the technology is increasingly adopted across all leading-edge manufacturing segments. This, along with an upcoming cyclical recovery, gives BESI’s EPS the potential to grow 18-26% p.a. over the next 5 years.

Edition: 157

- 31 March, 2023

ASML (ASML NA) Netherlands

Technology

New forensic red flags - sharp rise in DSI is particularly noteworthy for a company that is fanatical about managing its working capital cycle. DSI broke out of its narrow range in Q3 rising by 26% y/y to 226 days. With nearly €7bn of inventory now on the balance sheet, if ASML is slow to resolve its supply chain issues, inventory would remain elevated into 2023, leaving it vulnerable particularly if the outlook for customer capex takes another step down or if geopolitical tensions continue to escalate. In this context it is also concerning that the reserve against inventories fell LY to just 7.5% of the gross inventory balance (5-yr low).

Edition: 147

- 28 October, 2022

Technology

One of four high conviction plays on China's new industrial ambitions - as the country's largest chip foundry SMIC is totally aligned to Beijing policy priorities and is making faster than expected progress in moving towards 7nm process technology while being able to supply domestic companies with their needs at 14nm and above (which is where the majority of demand lies). It's on the entity list but can use older generation ASML technology, with ASML likely to breach US sanctions and supply it with its latest UV technology to enter what would be a bigger market than the US by 2030. ASML and Brussels are bridling against the trans-territoriality of US sanctions.

Edition: 120

- 01 October, 2021

Technology

ASML on steroids - Lasertec offers EUV-exposure with more upside beta vs. ASML since it can continue to beat numbers, while the Dutch giant will be unable to do so given supply constraints from their two main German suppliers. Only a matter of time before China begins to adopt EUV technology which will significantly expand the TAM for Lasertec’s equipment. The company offers “scarcity value” - there are very few Japanese firms growing revenues ~40% p.a.; share price can compound in the high-20%s over the next few years.

Edition: 117

- 20 August, 2021

Semiconductors: The new oil; East Asia to benefit the most

Rory Green explores the mounting importance of semiconductors. Over the next three years the winners will be the ones that have a physical integrated circuit trade surplus and/or a technical one; East Asia has both, and the US possesses the former. China is a semiconductor twin-deficit country with insufficient domestic production and a dearth of advanced IP, and leading-edge production will remain out of their hands for the future despite Beijing’s efforts. Investors should take a “buy on dips” approach for leading semiconductor capital providers and firms with monopolies (TSMC, ASML, etc.). Consider Chinese national champions, for they are too big to fail from a political and national security perspective. For short-term trading ideas, early signs of Dutch disease point to a strong secular tailwind to TWD and KRW, both tied increasingly to semiconductor cycles - the FX weakness provides an entry point for long KRW and TWD positions against EUR.

Edition: 109

- 30 April, 2021