Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

The energy transition just switched time zones

When it comes to the energy transition, developed markets dominate portfolios, yet the real growth and valuation upside lie in EM clean-tech leaders. It appears that the investment map is upside down. The scale of acceleration in EM is staggering, with 80% of new solar and wind capacity in 2025 being built outside of the US and Europe, and solar imports in Africa jumping 60% year-on-year. The original script for the energy transition was that developed markets would lead the way, with their wealth, policies and moral resolve. 2025 has torn up that playbook. The West has been tripping over its own ambition by erroneously investing in premature or uneconomic tech. Portfolios anchored to Western policy cycles remain exposed to subsidy rollbacks, voter mood swings, and bureaucratic inertia — while emerging-market clean-tech firms are growing revenues at roughly twice the global sector average.

Edition: 223

- 31 October, 2025

Why the gold price is falling back (for now)

In this presentation, Jeffrey Christian of CPM Group discusses the recent volatility across the precious metals markets, particularly gold’s sharp retreat from nearly $4,400 to just above $3,900. He explains the role of momentum traders who entered the market aggressively as buyers in October and have since begun unwinding positions, creating the sharp short-term pull back in the markets. Jeff looks at these price movements in the broader context of ongoing political and economic uncertainty; including the continued US government shutdown, expectations for Federal Reserve rate cuts, and shifting investor sentiment. He also discusses similar volatility in silver, platinum, and palladium, noting how speculative and technical factors have overshadowed fundamentals.

Click here to watch.

Edition: 223

- 31 October, 2025

Will China continue to export inflation to the rest of the world?

Andrew Hunt points out that China’s domestic economy remains soft. Domestic policy conditions look to have tightened: fiscal policy is notably less expansionary and liquidity growth has cooled slightly. The corporate sector’s weak financial situation has led to another bout of export price deflation / rising export shipments to the rest of the world, potentially deflationary for the global economy. Markets in general appear complacent on this issue. However, the crucial question is whether the PRC will continue to recycle the proceeds of its current account surplus into outward investment. China ceasing to export inflation via its capital account would represent a major deflationary shock to the world. Andrew is concerned that intensifying domestic credit constraints may force a reduction in capital outflows as companies are obliged to use funds at home. If CNY shows signs of appreciating further, he would view this as a potential warning sign for global markets.

Edition: 223

- 31 October, 2025

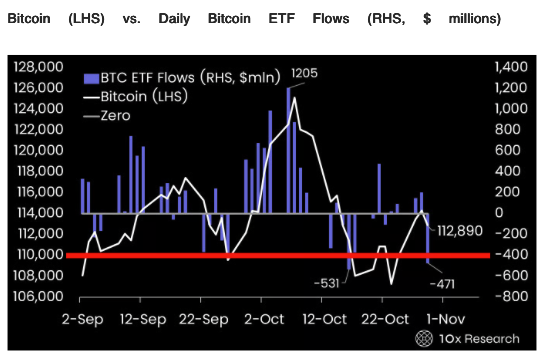

Bitcoin at a line in the sand

Bitcoin trades on shifting sentiment and positioning. The past five months haven’t been because demand disappeared, but rather because a massive transfer has been taking place beneath the surface, with early-cycle OG holders selling and new institutional capital steadily absorbing supply, keeping Bitcoin range-bound. If ETF buyers return following the China-US meeting and the latest FOMC decision, Bitcoin can resume its rally. However, Powell’s slightly hawkish tone and decision to delay QT’s end could keep ETF demand sidelined at a moment when it matters most. As long as Bitcoin holds the $110,000–$112,000 support zone, the 10X Research team are prepared to stay aligned with upside momentum, but a break below $110,000 would trigger a reduction in long exposure – that level remains their hard stop.

Edition: 223

- 31 October, 2025

Full of (soy) beans

Spot soybean meal (USD293.90) has been ranging for many years, finding support at 251.00–290.00 and resistance at USD471.00–554.00. The support area has been intact for 16.5 years and in recent months it has been tested again. With spot soybean meal emerging from the support area, Chris Roberts wants to put on an initial long position. Go 50% long at market. The initial stop loss is a daily close below USD256.00. At the same time, he will exit his long spot soybean oil long position.

Edition: 223

- 31 October, 2025

Fortum (FORTUM FH) Finland

Utilities

Pitched as a long idea at Revelare’s latest investor event, FORTUM operates in Europe’s most attractive market for AI datacentre development. Finland’s grid is mostly hydro and nuclear, with no marginal cost and power prices 60% below mainland Europe, while the cold climate further lowers datacentre cooling needs. All that is required for prices to rise back towards €100/MWh parity is new demand - and that is coming fast. Over 3GW of AI datacentre projects have already been approved, while Google has also bought a huge piece of land in the middle of the country and other hyperscalers are expected to follow. As Finnish power prices increase the company’s earnings should rise from €1 to €3 per share, implying the stock could reach €60 vs. <€20 today.

Edition: 223

- 31 October, 2025

US: How come treasuries are so bid?

This is the question James Aitken was asked repeatedly at Citi’s Australia Conference. Treasuries continue to defy the sticky inflation, debasement, fiscal crisis, Trump risk premium narrative. Swaption skews, however, continue to suggest treasuries will remain bid. Some kind of ‘AI productivity’ angle also helps treasuries or at least ensures inflation expectations remain well anchored. James suggests to shave it down with Occam’s Razor. The US budget deficit/GDP is going to end 2025 with a low 5% handle. Pending financial regulatory relief (leverage ratio) means the big US banks have the capacity to add treasury duration. And James thinks several of them will, in scale. An end to QT means the Fed will reinvest to keep treasury holdings constant, and to maintain the WAM of SOMA holdings which is currently ~8.3 years. That, too, probably ensures the ~10-year part of the curve remains well behaved. All in, James bets the ten-year note will remain supported.

Edition: 223

- 31 October, 2025

US equities: The case for value

Tian Yang is changing his long-held bias against value stocks and recommending a shift to overweight value vs growth. He points out that he is finally seeing alignment across A) market behaviour, B) the macro-outlook, and C) bottom-up fundamentals. On his indicators, today's set up is as good as it has been since the GFC for value to outperform. US earnings estimate revisions have broadened since Liberation Day, which has historically been indicative of value vs growth outperformance over the next 12 months (first chart below). At the same time, he notes a sharp fall in the correlation of the Russell 1000 market cap weighted index vs the equal weighted index. As the second chart shows, this correlation collapse has often marked a low in the value-to-growth ratio historically. Tian is also seeing evidence of a rotation into value stocks over the past couple of months.

Edition: 223

- 31 October, 2025

Ready for the contrarian gold trade?

Cam Hui has been bullish on gold, but point-and-figure charts of gold and gold miners now show that they are either very near or have outrun their measured price objectives. Tactically, the contrarian trade would be to sell gold and buy bonds. However, a cycle analysis leads Cam to conclude that the market is undergoing a shift to a hard asset price leadership cycle. Cam’s base case calls for a multi-month correction and consolidation in the manner of the 2004–2006 experience, followed by a second rally to an ultimate top at much higher gold prices. It is within this context that a long-term point and figure objective of 9,800 is achievable in the next 3–5 years.

Edition: 223

- 31 October, 2025

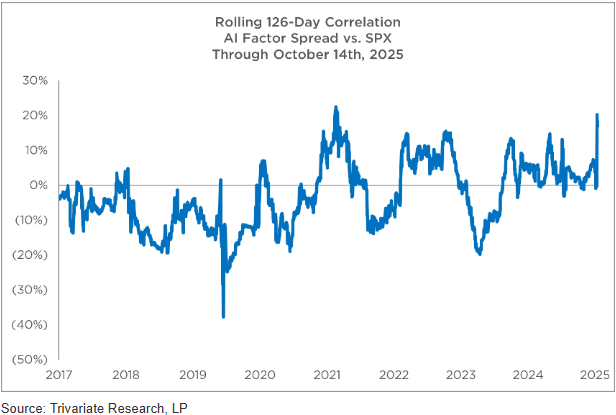

Blow-up avoidance guide - how are you dealing with the S&P500 being an AI factor bet?

While there are plenty of high-quality AI-exposed stocks to own, the challenge is that many non-Tech names have also become correlated to the AI trade. Trivariate screened for stocks with low correlation (<0.2) to their AI Semiconductors basket, that are up >10% in the past 6 months, top-half quality and beta <1 - identifying 28 stocks with a m/cap >$50bn. Given the recent huge moves in speculative names, Trivariate also advises preparing a sell/short list for a potential market rollover. They highlight 24 stocks ($1bn+ m/cap) that are up >100% in 6 months, in the most expensive EV/sales decile and the bottom half of their quality model, companies with high short interest and lower 2026 EPS estimates than at the start of the year, meaning the recent big moves in stock prices are despite a deteriorating nearer-term fundamental outlook.

Edition: 223

- 31 October, 2025

Lifco (LIFCOB SS) Sweden

Industrials

Karl Redin (Subsidiary CEO) purchased 26,350 shares at SEK 381, spending €920k. This is his eighth purchase and over 10x what he has spent on prior buys; the most recent was in Jul at SEK 367. The purchase occurred on the same day as the stock rose sharply after reporting Q3 earnings. This is an unusual buy, into unusual strength. Martin Linder (Subsidiary Head) also recently purchased shares spending €190k - a large purchase for him. Smart Insider has had a positive rank on this stock since early last year, based on buying from Per Waldemarson (CEO), Anna Hallberg (Director) and Martin Linder (Senior Officer). The stock has moved higher and insider buying has continued. Waldemarson made his most significant purchase in Jul, spending €1.3m and then spent an additional €300k in Sep. This is now the fourth time Smart Insider has renewed their +1 rank since Apr 24.

Edition: 223

- 31 October, 2025

UK: Anatomy of a rolling fiscal crisis

Helen Thomas says that the totemic Caerphilly Senedd by-election loss for Labour coupled with the inevitable cost-free, protest-vote election of Lucy Powell for Deputy Leader could not have come at a worse moment for budget preparations and for PM Starmer. After the OBR delivers its final pre-measures forecast, Reeves will know what number is required to meet the fiscal rules. By Nov 10th, the OBR will deliver its initial post-measures forecast - essentially a judgement on whether Reeves's shopping list of measures will pass muster. If not, there will be more HMT/OBR back and forth until it does. Except the shifting political landscape means that this is no longer just an optimisation problem between two economic institutions. Helen says that for the embattled prime minister the situation looks terminal, and Starmer will be gone within months, as a result of challenge to his leadership by those in the Labour Party who now oppose him.

Edition: 223

- 31 October, 2025

Consumer Discretionary

A story riddled with risk - Brian McGough argues DKS is priced for perfection despite mounting structural and cyclical headwinds. Core growth is tapped out and the House of Sport concept – its only unit growth driver - is not working; comping down 20% in year 2 and down again in year 3. Inventory issues, including a Critical Audit Matter on carrying value, and gross margin risks from tariffs on private-label apparel add further pressure. Apparel (40% of sales) has turned deflationary and the Foot Locker merger is seen as immediately margin-destructive, with no strategic merits and likely to strengthen competitors such as Academy and JD Sports. Brian is incrementally of the view that the 5-year CAGR for athletic footwear in the US is -300bp below pandemic-era trends and warns that at 10x EBITDA, a historical peak, DKS is over-owned, over-earning and due for a correction.

Edition: 223

- 31 October, 2025

Adyen (ADYEN NA) Netherlands

Technology

Strong net revenue growth and take rate, were both ahead of expectations for Q3. At constant currencies, net revenue growth amounted to 23%. This is the highest quarterly growth rate this year whilst expectations were that revenue growth would remain flattish in the remainder of the year. Its take rate showed a strong improvement as well, driven by the above average growth of Platforms (up 50.2% and increased take rate to 13.2 from 10.8). Another positive element of Adyen’s quarterly update is that FTE growth (9.0%) lagged net revenue growth again. This will result in a further improvement of its EBITDA margin. Investors can expect more clarity on growth targets at the company's upcoming Capital Markets Day, but based on current momentum and fundamentals, the IDEA! maintains that Adyen remains an attractive investment opportunity.

Edition: 223

- 31 October, 2025

Beneficiaries of US-Japan rare earths deal

Asymmetric Advisors highlights Furukawa and Tadano as potential beneficiaries of the US-Japan initiative to revive American mines, aimed at countering China’s resource dominance. Furukawa’s Rock Drill segment (17% of sales, ~30% of OP), derives over half its overseas sales from North America. The recent acquisition of EarthTechnica should more than double this segment’s sales from FY3/27. The Industrial Machinery division (11% of sales but >20% of OP), which includes belt conveyors used to transport mined materials, provides further exposure. Tadano with ~40% global share in Rough Terrain cranes and ~70% of its US demand tied to resources, also stands to gain. Europe remains its main drag and turning this around is a key factor in any share recovery. The stock trades at 0.78x PBR.

Edition: 223

- 31 October, 2025

Materials

EM Spreads initiates coverage on Braskem with an Overweight recommendation. They believe the company’s large domestic footprint, political relevance and partial government ownership make a default event less likely near term, but the credit now hinges less on fundamentals and more on political and strategic decisions involving Petrobras, the federal government and Braskem’s ability to strengthen liquidity. They see asymmetric risk-reward at distressed prices, with outcomes contingent on a secured-liquidity bridge, PRESIQ approval, direct support measures and broader policy backing for Brazil’s petrochemical sector. They favour exposure to the lower-priced bonds within the curve for better downside protection and see greater value in the 2030s at $38.3, 32.1% YTM, 3.1-yr duration.

Edition: 223

- 31 October, 2025

Peru perks up

Exports and markets have really rallied on the back of rising volumes and buoyant prices. And now, Jonathan Anderson points out that the domestic economy is starting to perk up. By contrast, the weight of political turmoil and uncertainty had been killing activity at home - but the recent data now suggest a renewed pickup. “What to do?” asks Jonathan. On equities there's no doubt that external volume gains are coming through with the new port, and with some signs of life at home we see no reason to exit the market now despite strong gains this year. And as before, the combination of a strong external balance and positive real rates make local carry and yield attractive.

Edition: 223

- 31 October, 2025

Healthcare

Leveraging purchase order data from 450 US facilities, MedMine is closely tracking the rollout of Pulse Field Ablation (PFA), the key driver of BSX’s Electrophysiology growth. The US ablation catheter market for AFib is estimated to be growing about 12% Y/Y. BSX has been growing faster in part due to mix shifting from lower-priced Cryo and RF products to its premium FARAPULSE PFA system. However, BSX is facing increasing competition with its PFA market share now at 80%, 10 percentage points lower than its peak. This raises a key question: will BSX’s next growth phase come from converting the larger RF market or expanding the total patient base estimated at 60m globally? MedMine’s near real-time data helps investors track these shifts in market share, pricing and technology adoption as they unfold.

Edition: 223

- 31 October, 2025

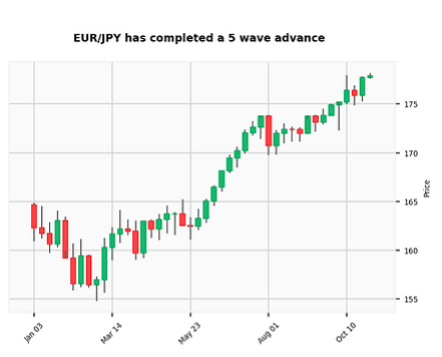

Sell EUR/JPY

David Woo points out that EUR/JPY is trading at its high as a result of domestic politics, with Takaichi being confirmed as PM in Japan, while Lecornu has managed to build a coalition with the socialists for now in France. It seems that EUR/JPY is pricing all this good news, and will struggle to go higher. EUR/JPY has completed a 5-wave advance over the past 9 months. David’s models suggest that this trend is now looking exhausted as JPY shorts are crowded. On the EUR side, Lecornu is coming under renewed pressure over the budget. The government may not collapse this week, but the market might start to price it. EUR may also come under pressure if the rare earth issue isn’t solved by Trump in a way that is friendly to German automakers. David sold the December EUR/JPY (RY) future at 177.56. He'll take profit on a move to 173, and stop out at 179.50.

Edition: 223

- 31 October, 2025

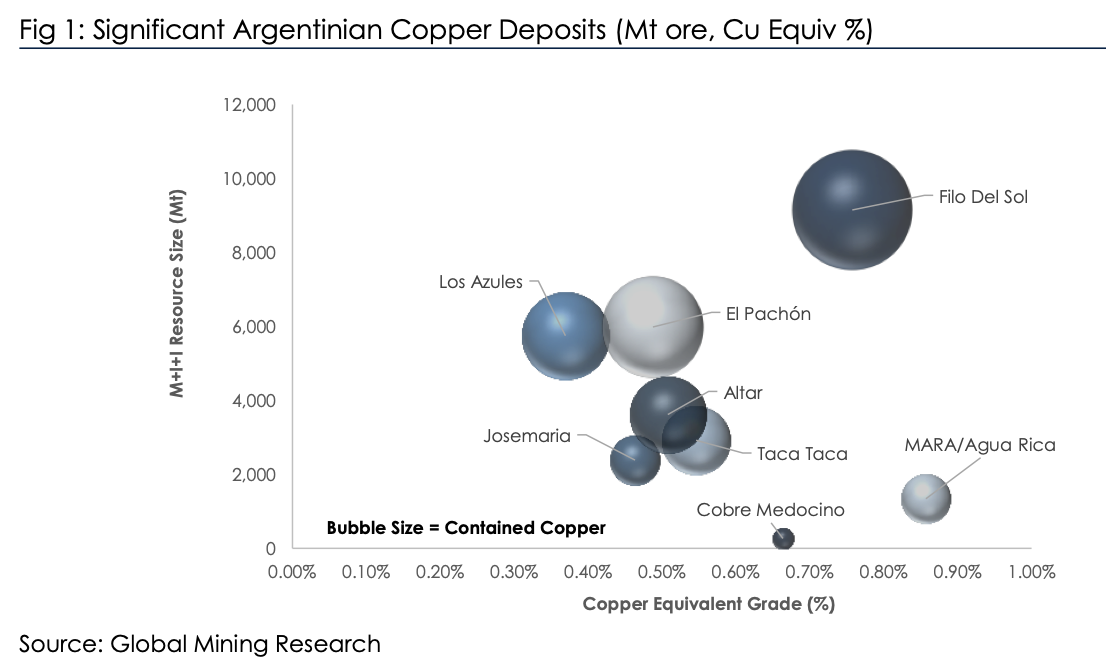

Is Argentina the next big thing?

Argentina has significant copper reserves yet produces no material copper (see chart). The new investment climate (RIGI) in Argentina, spearheaded by libertarian President Milei, is hoping to reverse this. Other volatile countries including DRC have achieved significant growth, so it’s possible. In his latest report, David Radclyffe examines the potential of Argentina copper. He sees potential for the nation to become a 1.0–1.5 Mt per year copper producer (top 10 globally), but comments on the aspirational timelines, with first copper unlikely on this side of 2029. Issues also cannot be discounted, with ESG concerns bubbling alongside a lack of infrastructure and skilled workers. David estimates the total capex at USD $40–50 billion. Lundin Mining has the most leveraged exposure to Argentina in partnership with BHP and is the preferred exposure. There are a few exploration plays, of which NGEx Minerals (non-rated) and its Lunahuasi discovery is the largest.

Edition: 222

- 17 October, 2025

US: A bubble in bubble fears

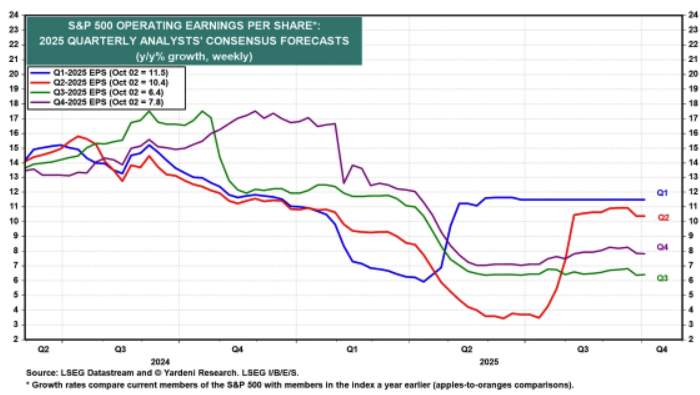

Ed Yardeni is raising his S&P500 year-end back to 7,000. He reckons that the V-shaped stock market rebound since April is discounting the economy’s resilience, which reduces the odds of a recession. Right now, we’re experiencing a slow-motion melt up, a result of the Fed rate cut in September and expectations of an additional one or two cuts before 2026 arrives. Ed sees the odds for a melt up at 30% and reduces the base-case for a sustainable bull market (without correction) at 50%. When the tech bubble emerged in the 90s there wasn’t as much chatter about the bubble, unlike this time; from a contrarian perspective, Ed sees this as comforting. He is counting on another better-than-expected quarter earnings season for Q3 to support the stock market’s rally to record highs. He expects a 10.7% increase compared to the 6.4% consensus (see chart).

Edition: 222

- 17 October, 2025

US: It’s not time to be bearish

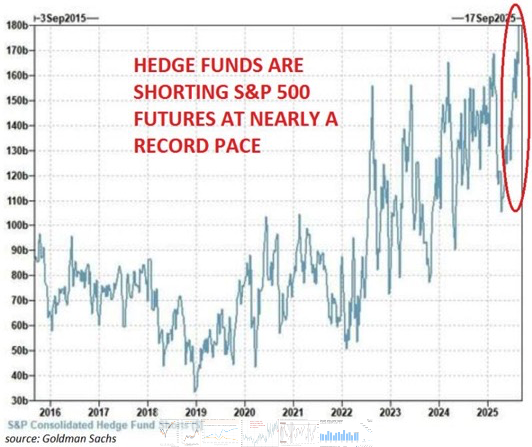

Forget the argument that this is a new dot.com bubble, argues Gaius King. The top 10 countries in the S&P500 are the ones delivering real growth whilst the remaining 490 and the broader economy are remarkably weak. Ironically, fund managers shorting this market is actually a contrarian indicator. There is little or no seasonality this year, and recall that asset and fund managers remain seriously under invested since the Tariff Tantrum. Actively shorting this market (see chart) in such a low volatility environment is hopium that they will match the index if the market falls. Gaius expects an additional year of market craziness ahead of us, peaking in Q3/2026, and draws remarkable parallels to the 1970s. Investors should buy momentum stocks. If you want a market canary, look at AI’s forward order book.

Edition: 222

- 17 October, 2025

Eurozone: Consensus too optimistic on disinflation

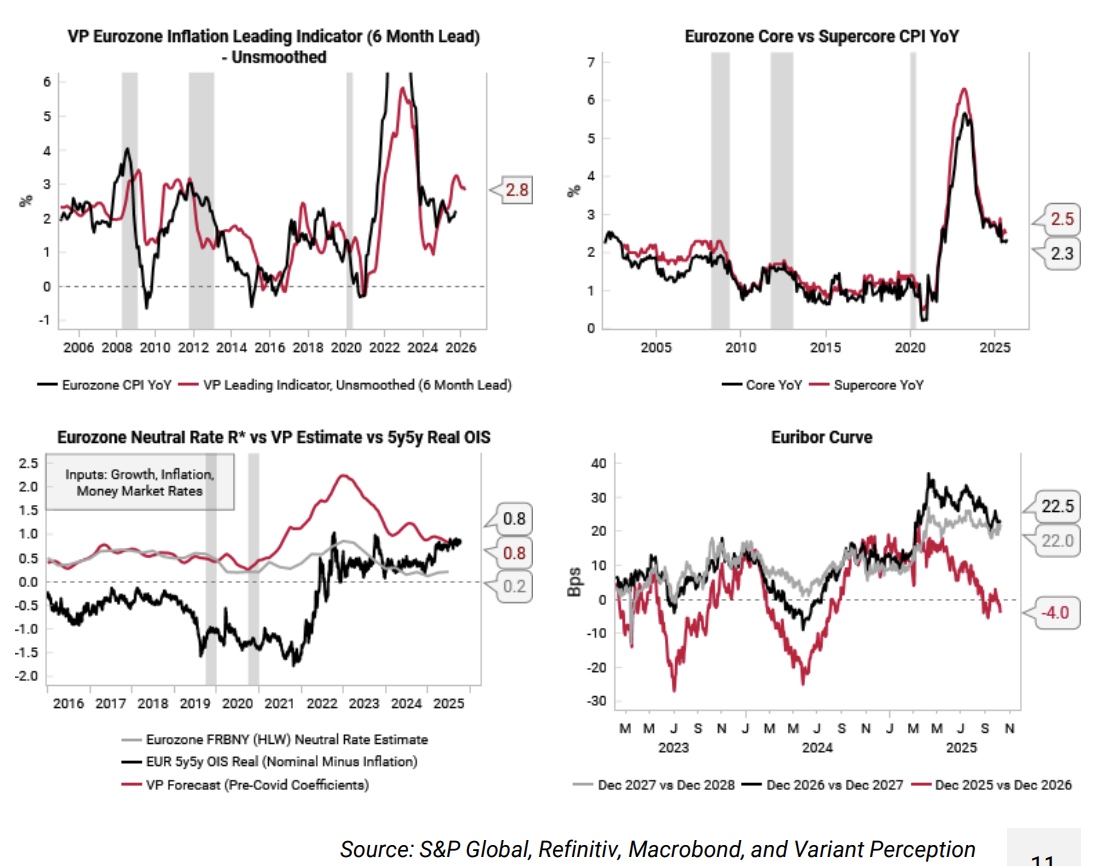

Consensus expectations see 2026 eurozone headline CPI at 1.8% and core CPI at 2%. The Variant Perception team suspects that inflation risks are tilted to the upside from here given the recovery in their eurozone growth leading indicators and the ECB rate cuts so far this year. Their main inflation leading indicator is rolling over from a high level, but the point estimate remains elevated at 2.8% (top left chart). Core and supercore CPI have also been slower to fall, still at 2.3 to 2.5% YoY (top right). The team put the real neutral rate (R*) for the eurozone at 0.8%, which is also where the 5y5y EUR real OIS is trading (bottom left). With headline CPI at 2%, there is good chance that ECB policy is already stimulatory, potentially creating inflation upside in 2026. The team take profits on their SOFR vs Euribor Dec 25/26 convergence trade established last month.

Edition: 222

- 17 October, 2025

Global bulls

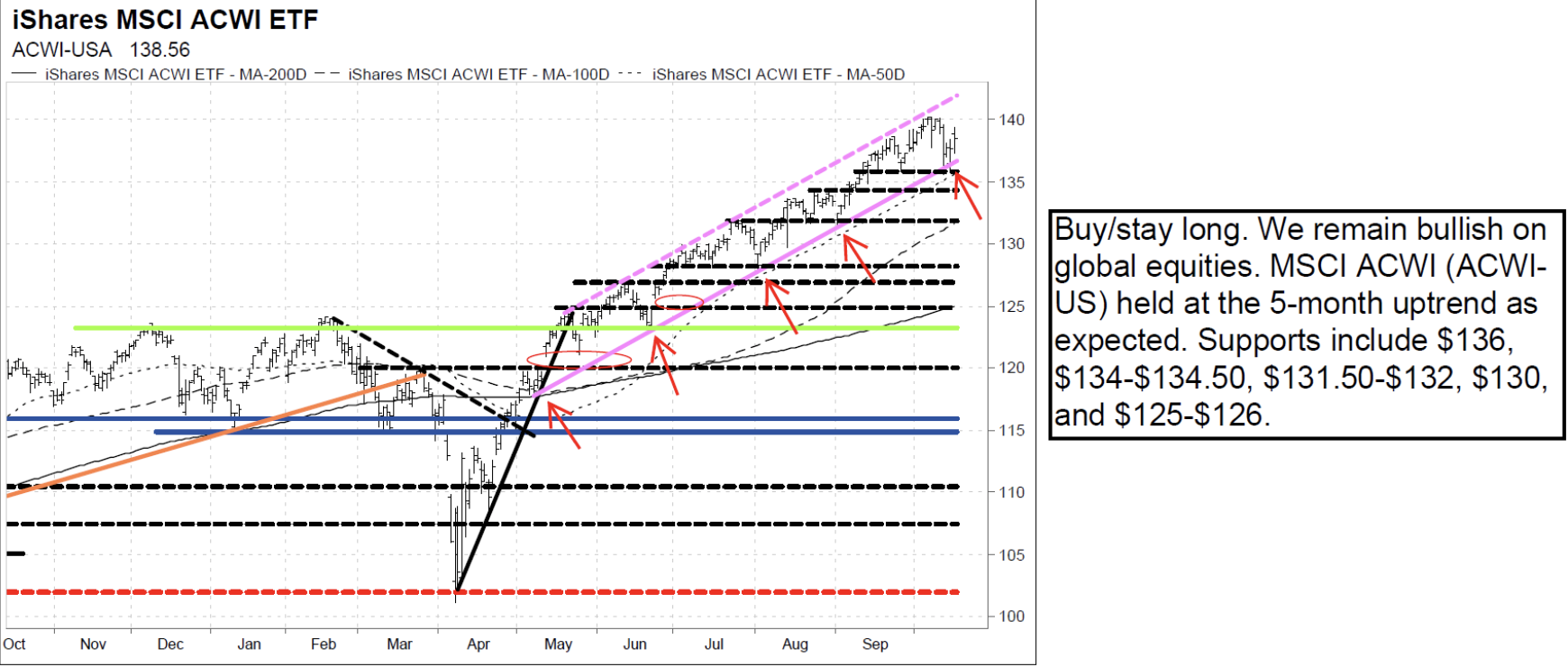

The Vermilion team remain near-term bullish since their April report, with their intermediate-term outlook also remaining bullish. They will maintain this view for as long as market dynamics remain healthy and the SPX and ACWI-US are above 6028-6059 and $125-$126. Their bullish near-term outlook will remain in place as long as the 5+ month uptrend continues on ACWI-US. So far, the latest pullback is testing the uptrend -- buy/stay long. Short-term supports to watch on ACWI-US include the 5+ month uptrend (currently at $136), $134-$134.50, $131.50-$132, $130, $128, and $125-$126. Expect more upside into year-end and early 2026. Remain overweight Taiwan, China, Korea and the US, and bullish on EM particularly MSCI EM Tech and Materials.

Edition: 222

- 17 October, 2025

How the Gulf is saving Pakistan

Foreign remittances from the Gulf are still exploding upwards, as Saudi, UAE and other GCC states continue to borrow and spend at a rapid pace, employing overseas workers in the process. Jonathan Anderson points out that remittances now overwhelm exports and official financing as the single biggest source of dollar income in Pakistan. The inflow has kept the current account in balance and the rupee stable, leading to equity gains too. It’s also pushing dollar sovereign spreads lower still. Jonathan had already exited his dollar bond position last year and had been cautious on further equity upside, but he has to admit that markets look more attractive today. Without remittances, Pakistan has a moribund export economy, much wider fiscal imbalances, an unworkably rising debt load and no exit strategy, but as long as Gulf earnings are flooding in it's difficult to be short this story.

Edition: 222

- 17 October, 2025

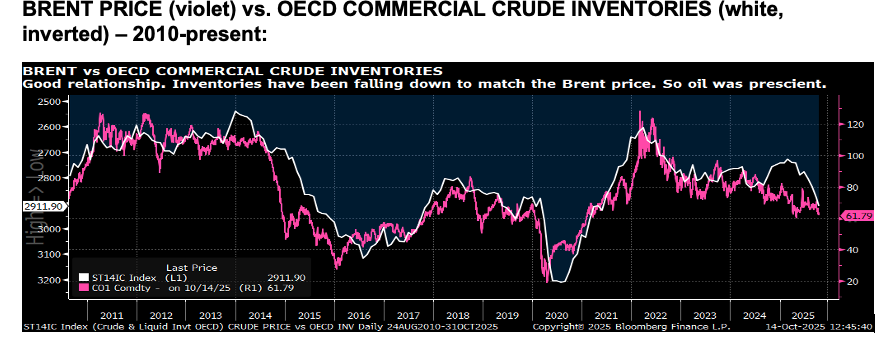

Oil: WTI to fall below $50/bbl?

Michael Churchill says if we are in an oil glut, one has to be open to the risk of oil falling below $50/bbl for WTI. Moreover, if Trump has made a deal with Arab leaders to keep that glut going, then there is no floor until some of the North American players lay down rigs or shut in production. Gas is less at risk for this kind of event since it is already so cheap relative to oil. Michael points out that if the new race for global power is focused around AI domination, it stands to reason that the old E&P elites will be gradually losing their power in geopolitics – particularly geopolitical moves meant to keep oil prices firm. Oil prices began falling in January, in anticipation of an increase in OECD crude inventories. Brent peaked at $82/bbl in January. Shortly thereafter (in February) OECD commercial crude inventories hit a low of 2.73b barrels. Since then, Brent has fallen to $62/bbl and OECD inventories have risen 5% to 2.91b barrels.

Edition: 222

- 17 October, 2025

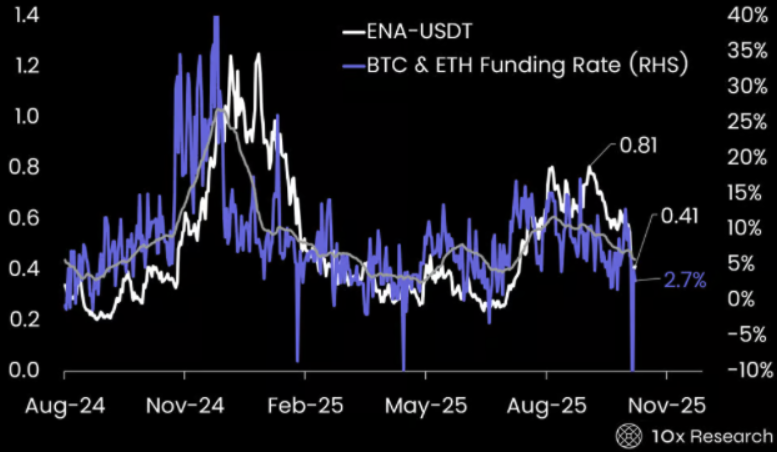

The Altcoin that might have 100% upside soon

Markets rarely break this violently twice in a cycle, yet this time the catalyst came from Washington, with a single tweet on tariff triggering one of crypto’s largest liquidations on record. Once market structures normalise, one altcoin in particular stands out as a potential winner. The recent volatility caused Ethena’s USDe stablecoin, along with Binance’s liquid staking tokens, to lose their intended pegs. USDe liquidity on Binance was exceptionally thin, yet it was being widely used as margin collateral for large leveraged positions — despite lacking the strict peg protections and risk parameters found on platforms like Aave. ENA-USDT now trades at $0.41, which the 10x team say is fair relative to BTC and ETH funding levels. If funding rates continue to normalise, the upside potential could see ENA-USDT rebound toward its previous $0.81 level, presenting an asymmetric upside of 100%.

Edition: 222

- 17 October, 2025

Peru: Under Pressure

Mario Marconini and Nicholas Watson point out that the new President Jose Jeri is under mounting pressure to name his cabinet as soon as possible. The delay in unveiling the new 19-strong ministerial line-up suggests that Jeri is struggling to recruit fresh faces; Jeri has already ruled out re-appointing ministers who served under his predecessor Dina Boluarte, who was impeached on October 10th. The final poll carried out in the days before Boluarte was ousted put her approval rating at just 3%. A cabinet needs to be in place as soon as possible. Even though Boluarte has gone, the protests by Gen Z protestors and transport unions have continued, having been reframed as an act of repudiation against the “mafia pact” of corrupt parties in Congress that are widely perceived as pulling the strings of power. If protests turn violent, Jeri’s could see his position come under threat.

Edition: 222

- 17 October, 2025

Technology

BTN continues to see several areas where OSIS's results may be unsustainable. The company has reduced its bad debt reserve to just 2% of receivables (vs. a 5-7% historical range), adding ~11 cents to Q4 EPS (OSIS only beat Street estimates by 5 cents). The current reserve for bad debts is at least 200 bps too low; if OSIS had to raise it by 100 bps, it would be a 39-cent headwind for EPS. DSOs have surged to 151 days (historically ~90), making Q4's revenue increase more suspect and the $372m forecast for 1Q26 tougher to reach. Warranty expense was cut again (added 3.7 cents to EPS), while OSIS continues to let its PP&E age and is using fully depreciated equipment - saving 29 cents in EPS last year. Finally, FCF remains weak (negative in 5 of the last 8 quarters).

Edition: 222

- 17 October, 2025

Chile: Policy rate should stabilise at ~4.5%

Igal Magendzo points out that the market — which in recent weeks had been converging toward a scenario with a policy rate somewhat higher than the Central Bank’s baseline projection — has slightly adjusted the timing of the final cuts expected in this cycle. Specifically, the highest probability of a rate cut shifted from next January to this December, in line with the medians of both the Economic Expectations Survey and the Financial Operators Survey, and consistent with Igal’s baseline scenario. Regarding the final cut, although the probability of a 25-basis-point move remains only around 50%, the market brought its expectation forward from October to June (compared with last week). Igal continues to maintain his view that the policy rate is close to neutral and should stabilise around 4.5%.

Edition: 222

- 17 October, 2025

Capital Markets at Risk: Jefferies echoing Bear Stearns

Financials

Charles Peabody believes we are in the mature phase of the capital markets cycle, with revenues likely topping out in 2026, while stocks are expected to turn lower well before then. He recommends selling Morgan Stanley and Goldman Sachs on near-term strength. Credit and liquidity stresses are emerging following the automotive credit, Tricolor and First Brands developments, while syndicated loan offerings are being pulled. He sees echoes of Bear Stearns at JEF, noting that MS and BlackRock have ended relations with Bonita Point, the JEF subsidiary housing First Brands receivables, just as this rapidly growing broker reached top-tier status. Sell Capital Markets, Buy NII - he favours Citi, M&T, Citizens Financial and UBS.

Edition: 222

- 17 October, 2025

Drug pricing demos as Pharma scrambles

Healthcare

President Trump's drug pricing plans are progressing from the conceptual to a more serious phase. As CMS prepares to issue its most favored nation (MFN) demonstrations and pharma companies attempt to cut pricing and manufacturing deals with the administration, Capital Alpha Partners' Rob Smith and Kim Monk caught up with a former director of the Center for Medicare and Medicaid Innovation (CMMI) on the administration’s advancing Medicare drug pricing agenda. The team sees at least one demo being proposed by the end of the year and implemented by late 2026, though legal challenges remain significant. Physician-administered Part B drugs are the most likely target for a drug model.

Edition: 222

- 17 October, 2025

Technology

TD trades at levels implying investors value its operating business at near zero, reflecting deep scepticism about growth and profitability amid dependence on Samsung and exposure to memory price volatility. While these risks are real, Yuka Marosek argues they are already priced in and TD’s close ties to Samsung Japan and Toyota Tsusho provide stability and long-term relevance. Expansion into automotive and server / storage markets, supported by rising AI-driven demand for memory, offers potential for improved margins and diversification. Toyota Tsusho owns 50.1% of TD and Yuka wonders if Tsusho might eventually absorb the entire company - if Samsung allows it.

Edition: 222

- 17 October, 2025

Technology

Could the stock soar over 100%? KCR argues that CSCO isn’t just cheap vs. AI peers - it is cheap relative to the broader market, trading at roughly the same multiple as Kimberly-Clark despite far stronger growth. Networking product orders have risen 10% Y/Y for 4 consecutive quarters, suggesting investor concerns about a slowdown are unwarranted. Meanwhile, the company’s rapidly growing exposure to AI infrastructure products and shift towards subscription-based revenue both support multiple expansion. CSCO trades at one-third of Arista Networks’ P/E multiple and one-quarter of its EV-to-revenue ratio - even a modest narrowing of the valuation gap would translate into substantial gains for CSCO shares. Finally, a ~5% FCF yield is far too high for a company of CSCO’s quality.

Edition: 222

- 17 October, 2025

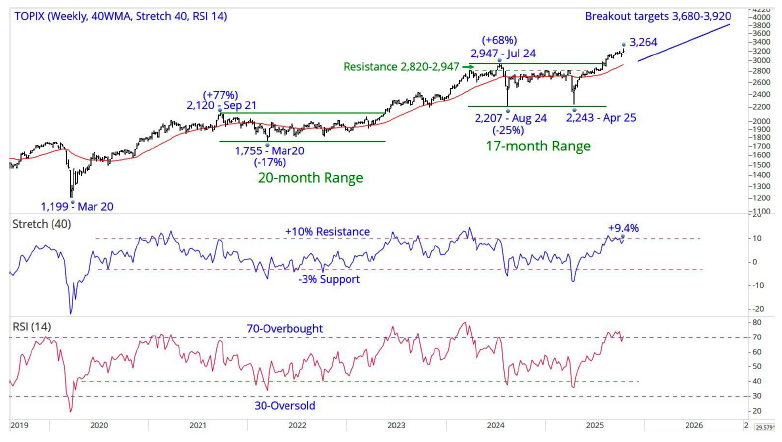

Japan: Hot Topix

The Topix’s (3,198) breakout from the 2,207–2,947, 17-month range targets an advance to 3,680–3,920. The break above the 1,700–1,825, 28-year ceiling in 2021 targets a minimum of 3,400–3,650+. Weekly indicators are either overbought, or close to overbought, but have been higher during this bull market. Chris Roberts remains 50% long from 2,857, with the stop for all longs moving up to a daily close below 2,780 from 2,475. His preferred target is now 3,680+, and he is looking to add to longs. He will add 5% long at 3,178, 5% at 3,168 and 5% at 3,158. If fully executed, he will move to 65% long.

Edition: 222

- 17 October, 2025

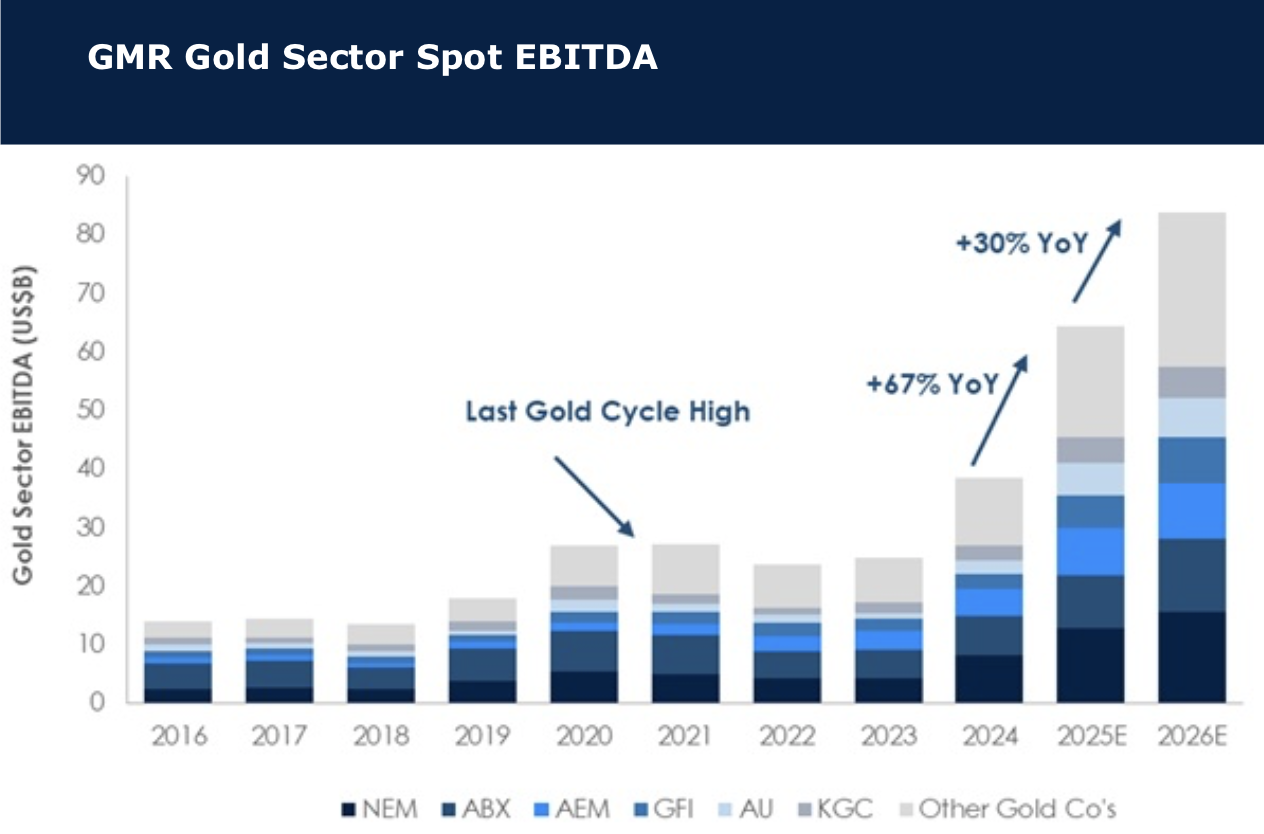

All that glitters is gold

Gold has been setting new highs through 2025 as the best performing major commodity. The music will come to an end, but David Radcliffe says that until that happens, a spot gold price over US$3,800/oz will generate some extraordinary returns. He examines the impact that spot prices could make to a sector that has already benefited from a robust 18 months. The 2026 consensus gold price is ~US$470/oz below spot, implying further upside if prices are maintained. On David’s expectations, spot prices into 2026 could lift sector EBITDA another 30% after an expected 67% lift in 2025. His covered gold stocks trade at a discount with spot P/NPV5 of 0.87x, or an implied gold price of ~US$3,330/oz, a 13% discount. There remains a value argument for gold miners, plus earnings momentum. David’s preferred exposures remain Agnico Eagle, Kinross and Northern Star of the seniors, and IAMGOLD, Equinox and Alamos of the more leveraged intermediates.

Edition: 221

- 03 October, 2025

Should investors re-enter India?

Jonathan Anderson’s growth proxy index has rebounded to around 5% y/y in the past few months, with a renewed pickup in credit activity and earnings. It may be below the official 8% real GDP growth rate, but is a very respectable pace nonetheless. The external balance is back in surplus on the back of weak imports and low oil prices, inflation continues to fall, the fiscal balance is "just enough" to avoid serious trouble, and the RBI still has room to cut rates at the margin. Jonathan sold his Indian equity position a year ago, and the index has underperformed since then. This is still an expensive market on any valuation metric - but if he really sees the cycle stabilizing and growth maintaining at 5% or more, he is certainly considering a re-entry. Stay tuned.

Edition: 221

- 03 October, 2025

Special Sits Idea Forum

The majority of ideas presented at MYST's latest buyside event were industrial-related, with themes including potential takeouts, SOTP simplification stories and power-related names. Stocks highlighted include:

Aptiv (APTV) - “GoodCo vs. BadCo” split to unlock hidden value of Connection Systems business. TP $125 (45% upside).

Bed Bath & Beyond (BBBY) - unappreciated assets create “zero enterprise value” amid positive FCF inflection. TP $28 (180% upside).

DuPont de Nemours (DD) - re-rating tailwinds fuelled by fundamental and technical catalysts. TP $115 (45% upside).

Idaho Strategic Resources (IDR) - enormous upside from potential US government partnership / investment.

Peloton (PTON) - new product launches + subscription price increase to accelerate turnaround.

Ralliant (RAL) - ignored "broken spin” poised for positive revision cycle. TP $60 (35% upside).

Edition: 221

- 03 October, 2025

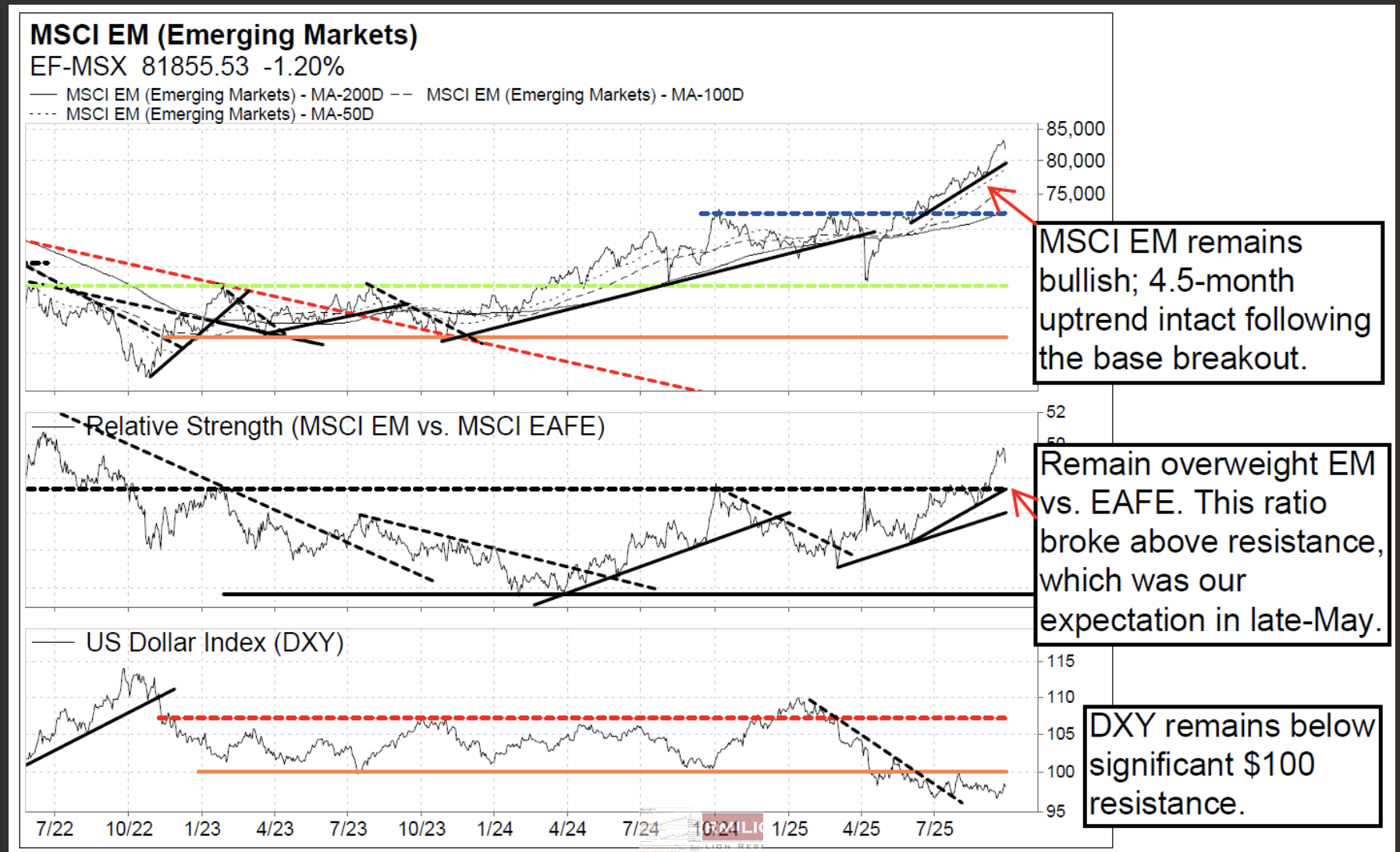

Remain overweight Taiwan, China and Korea

According to David Nicoski, the MSCI Emerging Markets index (local currency) and EEM-US (USD) are both trading within 4.5-month uptrends, and he remains bullish. David expects support at the uptrend, which also coincides with the 50-day MA and $50.65 horizontal support on EEM-US. He would view any pullback to $48 support on EEM-US as a buying opportunity. For EM countries, while price remains attractive, he is downgrading Greece to market weight due to RS deterioration. EM countries where he remains overweight include Taiwan, China, and South Korea. Additional leadership countries include Vietnam, Romania, and Pakistan. For EM sectors, defensive EM sectors (staples and utilities) continue to underperform and are at YTD RS lows; underperformance has continued, as expected -- avoid. Meanwhile, attractive EM sectors where David expects outperformance include: MSCI EM technology, consumer discretionary, materials, and communications. He is also monitoring for a RS bottom on EM health care.

Edition: 221

- 03 October, 2025

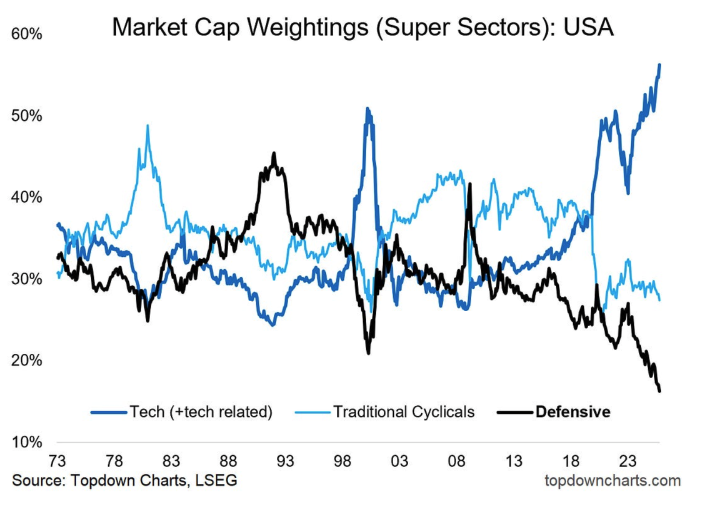

US: Drift risk rising

The good thing about cap-weighted index investing is that over time it automatically allocates more money to the best stocks and takes from the bad ones. The bad thing about it is that… over time it automatically allocates more money to the best stocks and takes from the bad ones. Callum Thomas’ chart shows both of these aspects in action, with tech dominating the scene and record lows for defensives. In times like these where there is a very sector driven bull/boom/bubble underway, such strategies can become very undiversified and lop-sided very quickly. Options for investors include switching to equal-weighted indexes, active allocation, tactically making sector tilts when major extremes are reached, or correct it at the portfolio level by including uncorrelated/defensive assets.

Edition: 221

- 03 October, 2025

Ginlong Technologies (300763 CH)

Industrials

It has been three years since the last insider activity in this stock occurred. In Jun 22, the selling was from Finance Director Junqiang Guo and Deputy GM Chan Zhang around CNY 200 per share. The stock rose for a few months but then fell sharply in 2023. Recently, Guo, Zhang and Deputy GM Hefeng Lu made large sales at less than half that price: Guo sold US$862k at CNY 85, Zhang US$515k at CNY 85.06 and Lu US$350k at CNY 87, reducing their holdings by 30%, 30% and 23%, respectively. The stock has nearly doubled from its Apr 25 low but remains flat over the past 12 months and below 2023 levels. Smart Insider are ranking the stock -1 (lowest rating).

Edition: 221

- 03 October, 2025

Technology

AI is fuelling accelerating demand for high-performance compute (HPC) and Bitcoin miners-turned HPC hosting providers have been huge beneficiaries. While the stocks have rallied significantly as multi-billion-dollar contracts become more frequent, Rosenblatt sees a valuation disconnect at WULF due to its perceived smaller power pipeline. They view this as more of a disclosure issue than anything fundamental and expect the power experts at WULF to proactively add new capacity ahead of current market expectations. As such, Rosenblatt reiterates their Buy rating and raises their TP to $14.50, based on 16x their 2027 Adjusted EBITDA estimate.

Edition: 221

- 03 October, 2025

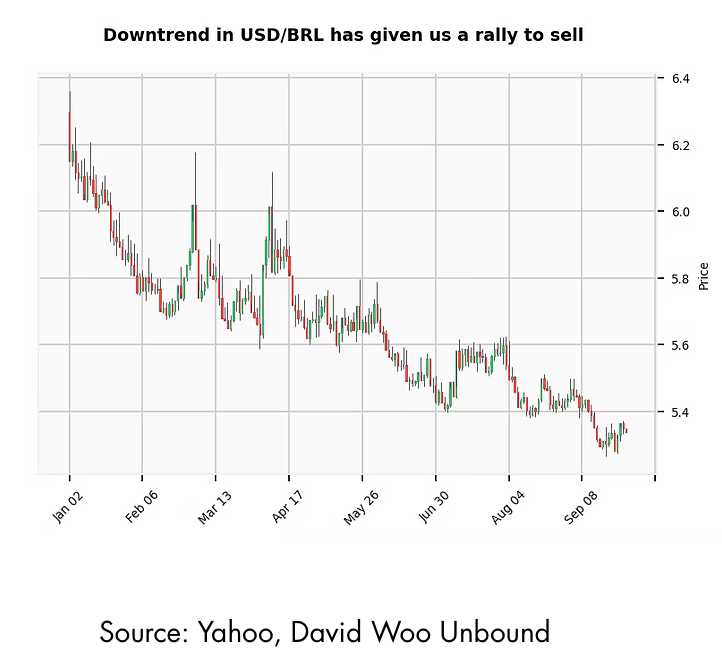

Brazil: Benefitting from uncertainty

The short-term trend in the dollar switched to a bull trend against most currencies as rates reversed higher last week. This wasn't the case for MXN and BRL however, where David Woo points out that the correction to the trend wasn't sufficient to reverse it. BRL in particular failed to get above pivotal resistance at 5.40. Brazil has been a beneficiary of the trade war between US and China, with China choosing to purchase soybeans from Brazil. Uncertainty about the future of the government in Argentina has also been a tailwind for BRL. A shutdown in the US should be beneficial for carry trades as markets will have little guidance from data to change macro views. David bought the November BRL future at 0.18625. He’ll take profit on a move to 0.1930 and stop out at 0.1820.

Edition: 221

- 03 October, 2025

Argentina tries… orthodoxy

From a muddle-through approach fraught with renewed peso and inflation risk, to more classically orthodox measures, Jonathan remarks just how much the policy stance has changed in the past three months. This is the best chance of getting money growth and inflation back down into low double and ideally single digits, at the cost of keeping the economy in recession. In the face of the country’s anaemic export economy, the only hope for external stabilisation is to keep overall demand and import spending weak. Even if Argentina holds course, it doesn’t guarantee a stable peso, and the needs to give up the USDARS 1,500 "ceiling" and let the exchange rate find its level without endless borrowing support. The recent backup in dollar yields has opened tactical value, but not necessarily a structural buying opportunity; there's a big difference between successfully stabilizing the macro position and finding an exit strategy for external indebtedness.

Edition: 221

- 03 October, 2025

China: Holding against resistance

Chris Roberts comments on the Shanghai Composite (3,828), which has been ranging above 10-year resistance at 3,500–3,732 for five weeks. Daily chart indicators have now unwound very overbought readings (14-day RSI reached 88, just below extremely overbought 90), and the area of the rising 40-day WMA has been acting as support since May. The ranging above major resistance is seen as a sign of strength, and there is a low-risk entry here that allows Chris to try an initial long position. Go 50% long at market. His initial stop is a daily close below 3,695.

Edition: 221

- 03 October, 2025

Delhivery (DELHIVER IN) India

Industrials

At first glance, Delhivery’s FY25 results - its first net profit and positive EBITDA margins - suggest the company has finally scaled and matured. However, Iii argues the turnaround is more cosmetic than fundamental. Favourable revenue recognition policies (contract assets equal to ~30 days of sales vs. a 13-day transit cycle), depreciation changes and halved ESOP charges materially flattered reported profits. Capital allocation remains troubling, with Spoton Logistics revenues collapsing >70% since its INR 16bn acquisition, yet losses effectively buried via amalgamation. Rising impairments, questionable subsidiary accounting and elevated executive compensation add to concerns.

Edition: 221

- 03 October, 2025

Industrials

Under new leadership, Kyodo is accelerating its pivot from the declining paper-printing business towards higher-margin niches such as high-performance packaging materials, flexible packaging and tube products. Margin gains in recent years already reflect this shift and the company’s 10-year plan aims to scale these efforts further. The key question for investors: with DNP and Toppan well ahead in diversification, can Kyodo leverage its niche strengths to establish itself as a viable third player in a consolidating industry. Yuka Marosek argues it can. While Kyodo’s OP recovery appears partially priced in (13.9x P/E vs. DNP at 14x and Toppan at 18.4x), a 4.8% dividend yield should appeal to income investors and with FY26 OP projected +20% y/y and ROE rising to 6.1%, further upside remains possible.

Edition: 221

- 03 October, 2025

Materials

Buy the VEDLN 9.85% '33s at 101/9.6%/4.9Y; Hold the rest of the curve - Vedanta priced its USD 500m 144A/RegS 7NC2 notes at 9.125%, down from IPT of 9.5%. The lower-than-expected yield signals strong demand and investors’ growing confidence for the credit. Lucror’s Credit Bias on VRL remains "Stable", as the company's low-cost positions and robust balance sheet should help it weather commodity price volatility amid global trade tensions. The 9.85% '33s have the longest duration and would hence have the most upside if the credit spread tightens, which Lucror expects to occur following the successful issuance of new 7NC2 notes.

Edition: 221

- 03 October, 2025

Bios scores big on 89bio, rotates to new opportunities

Healthcare

Bios Research’s long call on 89bio has paid off handsomely: since turning bullish in Apr 25, the shares have climbed ~120%, culminating in Roche’s announced takeover at $14.50/share plus a $6 CVR. With conviction now removed, Bios suggests rotating into SMID-cap biotech to capture what they see as the early stages of a new bull cycle. On the short side, the team has just launched a new idea with 30-50% expected downside over the next 6 months. Their track record is strong: 15 of 22 shorts over the past 18 months have generated absolute returns (~72% alpha-adjusted hit rate), with notable successful conviction removals including Apellis, Butterfly Network, Geron and Inspire Medical.

Edition: 221

- 03 October, 2025

Don’t miss out on the gold rally

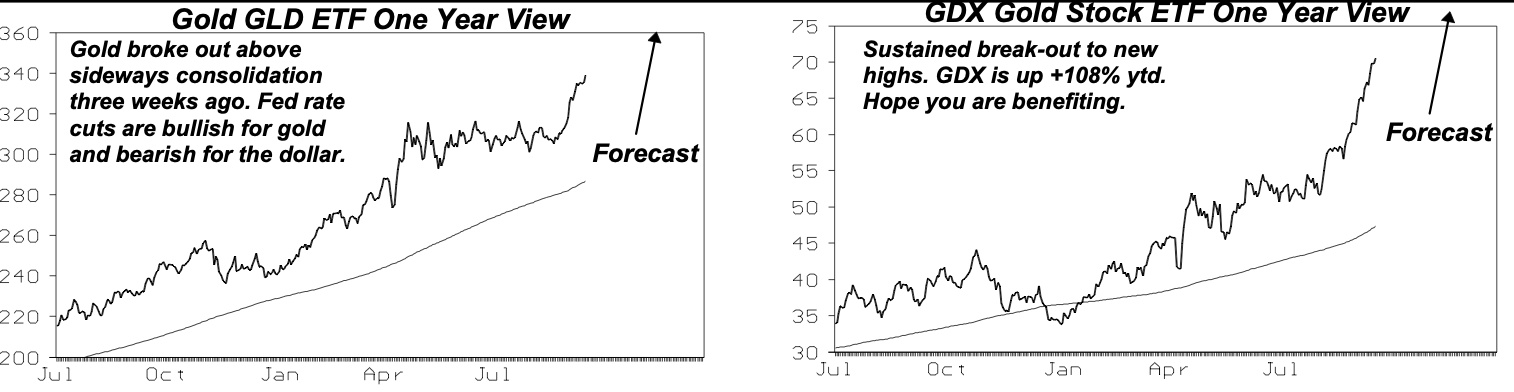

Gold stocks have been the top recommendation on Michael Belkin’s US industry group/stock page all year. The VanEck Gold Miners ETF (GDX) is now up +108% ytd after just 1.5 months of inflows, six times as much as the MAG7 +18% ytd gain. The fundamentals remain positive. The Fed’s policy shift waves a green flag toward gold prices, with central banks continuing to accumulate gold as they shift reserves out of the USD. The fundamental attraction for gold miners is finally being recognised, but we are only 1.5 months into the change in perception. GDX has only US$19bn of assets at this point, and the five largest stocks clock in at US$275bn, indicating that it is large enough to accommodate industrial buying, which could dramatically expand the market cap of related stocks as the rally continues. Michael’s recommendations include small-cap stocks that have lagged the GDX advance, including Galiano Gold, McEwen, Seabridge Gold and Equinox Gold.

Edition: 220

- 19 September, 2025