No matches for this search

Try adjusting your filters or search criteria

Technology

JNK’s analysis suggests LSCC is tracking ahead of guidance, with Q1 supported by strong bookings extending into 1H27 and a book-to-bill above 1.2. However, this strength is partly driven by Greater China customers pulling forward demand ahead of a ~15% price increase implemented in March 2026, with regional shipments running ~25% above Q4 levels. Lead times remain elevated at over 26 weeks, constrained by substrate and packaging rather than wafer capacity. With servers accounting for ~60% of revenue and exposure to Intel and AMD platforms, the company also benefits indirectly from AI-related demand. JNK's analysis suggests pricing can support growth even if volumes soften.

Cisco's 800G just hit the same wall GPUs did

Technology

JNK Research indicates CSCO's Silicon One networking roadmap faces the same thermal management bottleneck that constrained Nvidia and AMD GPU production. CSCO is ramping wafer starts 8x - from 1k to 8k annually - at TSMC in 1H26. However, heat spreader suppliers already operate at 85%+ utilisation with capacity concentrated among few Taiwan suppliers. The company is proactively qualifying secondary thermal suppliers and paying for tooling upfront to secure allocation. This mirrors the CoWoS packaging constraints that limited GPU shipments in 2024. Networking ASIC thermal requirements are approaching GPU-level complexity as data centre switches migrate from 400G to 1.6T.

Technology

Richard Windsor argues SoftBank’s $2bn investment in INTC, alongside a potential 10% US government stake, may keep the company alive but does little to resolve its strategic paralysis. INTC faces a stark choice: either invest heavily to catch up with TSMC or break up the business - yet under new CEO Mr. Tan, neither path is clear. The board abandoned Pat Gelsinger’s catch-up strategy due to mounting costs, leaving INTC exposed to further share losses in PCs (to AMD and Qualcomm) and in data centres (to Nvidia and AMD). Richard warns that without decisive strategy, customer confidence will erode, competitors will gain share with ease and capital injections alone cannot avert decline. He sees no attractive entry point in INTC shares.

AI driven 10Q / 10K filings analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) Advanced Micro Devices - struck previous wording around the need to discount products, suggesting more confidence in pricing power. 2) Bright Horizons Family Solutions - no longer anticipating expanding operating cash flows. 3) GoDaddy - takeover target? Plus, further colour on international expansion plans. 4) Gilead Sciences - more competitive market for Bulevirtide. 5) Installed Building Products - new change in control agreement prompted by external takeover interest? 6) New York Times - increasing concerns re. competitors gaining market share at its expense.

Technology

Richard Windsor says MediaTek’s Kompanio Ultra chip sets a new standard for the high end of the Chromebook market and looks to be merely a stone’s throw from Intel and Advanced Micro Devices facing another newcomer in the PC Market. The biggest winner will be Arm, which will see its penetration of PCs accelerate and it will earn higher royalties from MediaTek which buys the processor design and licences the IP. This is neutral for Qualcomm because competition in this space is healthy and will keep the firm on its toes and push it to continue to lead when it comes to performance. INTC and AMD are the real losers here as the x86 architecture looks increasingly obsolete.

Technology

The “ouster” of Pat Gelsinger will almost certainly result in INTC being split up, meaning the once all-powerful brand may soon be just a memory. With the company’s future very uncertain and its once great engineering culture in poor shape, INTC is easy pickings for its resurgent competition. Richard Windsor expects to see Qualcomm, AMD and MediaTek redouble their efforts in PCs and the data centre. He has often said that at 10x earnings, one should shut one’s eyes and buy the stock, but because of the falling EPS estimate the valuation has never gotten there. With the company in this much trouble, there is no price at which he would want to buy it.

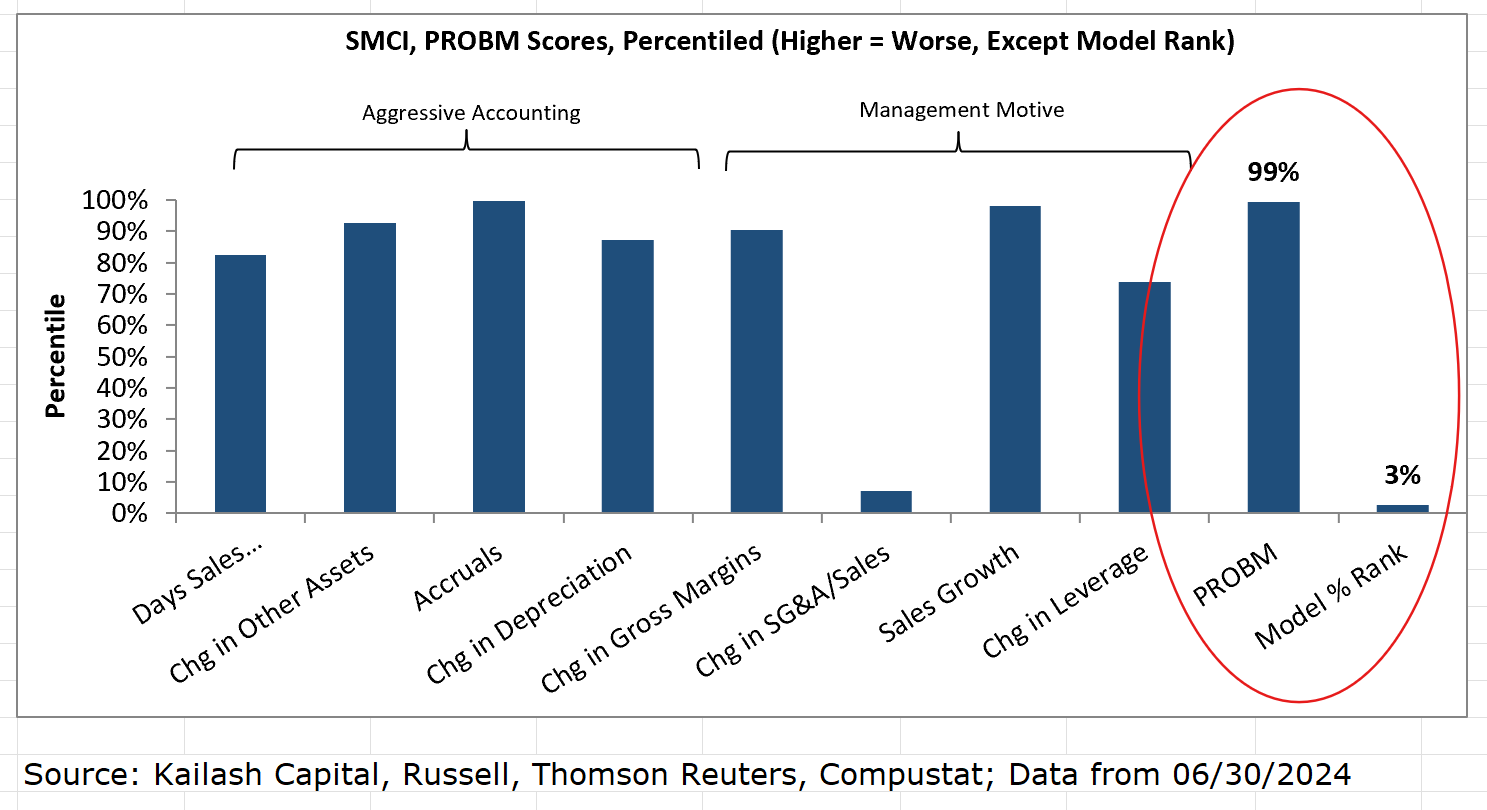

A systematic approach to identifying potential earnings manipulators like SMCI

SMCI shares fell nearly 20% after the company delayed the filing of its annual report and Hindenburg Research alleged “fresh evidence of accounting manipulation”. Interestingly, SMCI features in KCR’s S&P 500 Earnings Manipulator list, which includes stocks in 1) the worst quintile based on academia’s PROBM formula and 2) the bottom 20% of KCR’s ranking methodology. Other companies flagged include Advanced Micro Devices, Tesla, and Xylem, with Block and Emerson Electric added last month. Over the past 14 years, KCR’s Research Short Portfolios have been valuable for spotting potential risk flags and generating short ideas. To access the return summary for these portfolios click here.

Technology

Bad news comes in threes. First, there is a new-found realisation that AI returns are not keeping up with massive AI investments. Second, there are macro-related worries. And now third, a report emerged that NVDA’s Blackwell roll-out is being delayed due to “design flaws”. KC Rajkumar is not surprised. In a recent Micron note, he pointed to the potential for heating-related failures of the NVDA GPU-HBM module. His most recent checks now show that NVDA is likely to pause GPU wafer starts at TSMC until yield-issues are resolved. KC expects a hole appearing in NVDA’s 2FH25 product roll-out and revenue ramp. Estimate cuts are on the way. He is looking for the stock to head to the $80 level into the upcoming earnings call. Advanced Micro Devices, on the other hand, could end up being an accidental winner.

Technology

The must-have name in the AI space - KC Rajkumar sees MU rivalling AMD’s market cap in the next 12-18 months. As KC predicted, MU blew away investor expectations, not merely by beating and raising quarterly numbers, but by providing a qualitative outlook for revenue / margins into Cy24 and Cy25 - unimaginably impressive for what is supposed to be a cyclical business. Not even Nvidia has been able provide a two-year outlook. Agnostic to AI chip suppliers, and increasingly a pure-play in AI, renders MU more attractive, at this stage in the investment cycle, to the likes of NVDA, AMD, Broadcom and Marvell.

$400bn spent on datacentre AI chips in 2027? Is it possible?!

Technology

The mother-of-all sanity checks - Lisa Su (CEO of Advanced Micro Devices) pitched late last year a total addressable market for datacentre AI chips of $400bn, New Street looks to make sense of this number. In the first of what will be a number of pieces on this theme, they estimate the total datacentre capex, the opex required to run such an AI infrastructure, the revenues required to justify the investment, and, last but not least, what industry revenues and capex would need to look like to support all this.

Semis & Hardware: Real-Time Views

Technology

Arete’s monthly newsletter covers the latest updates in the global tech hardware and semis markets, with a particular emphasis on foundry, memory, compute, semi-cap, wireless semis, and EV/autos. Highlights from their Nov edition include: 1) Dramatic shift in memory - Q4 price surge signals shift from a buyers’ to a sellers’ market. 2) HBM market dynamics - is AMD diversifying its HBM supplier base with new SK Hynix deal? 3) Why Huawei looks set for a bumper 2024 and US sanctions backfire. 4) Why Apple’s spend at TSMC might be flat in 2024, curbing TSMC recovery. 5) Auto semis - content is king in 2024. 6) Lithium-ion battery outlook - all-time-high earnings amid all-time-low valuations. 7) To infinity and beyond - satellite semis growth in the 2020s.

Technology

Buy the dip even as AI momentum shows cracks - as the semis complex comes under pressure for all the right reasons (disappointments at Apple, loss of momentum in AI, analog inventory, China trade worries), KC Rajkumar believes (near-term) long ideas in semis have become harder to come by. However, he argues the Street has become too negative re. traditional servers and expects investors to gravitate towards AMD despite ongoing worries regarding share gain of its MI300. Over time, KC would not be surprised if up to a third of Microsoft’s AI servers come to be based on an AMD solution vs. the dominant share Nvidia currently enjoys.

Connectivity, speed & scale combine to blow up IT as we know it

Technology

Report by

Blueshift Research

BL

In John Harrington’s latest Tech Trends report, he looks at several factors that have combined to change IT development and sales dynamics. These include how the accelerating deployment of speedier wired and wireless connectivity to the cloud, very fast computing platforms being built at scale within the clouds, the accelerating development of quantum computing as a viable commercial business, and the development of serious AI capabilities are affecting the global digital landscape. As IT increasingly transitions from in-house networking to the cloud, some new areas of IT will benefit, while others face an uncertain future.

Positive: Advanced Micro Devices, Alphabet, Apple, Amazon, Broadcom, Ciena, Dycom, Intel, IonQ, Microsoft, Nvidia, Rigetti.

Negative: C3.ai, Cisco, Dell, Qualcomm, Salesforce.

Artificial Intelligence: Look for the picks and shovels of this latest bubble

Technology

The popularity of ChatGPT and the technology press’ willingness to ignore the reality of what it is, has kickstarted an arms race where a series of huge but very dumb machines will be created to meet demand. Richard Windsor predicts crashing valuations, huge write-offs and another period of navel-gazing while the AI industry ponders what went wrong. This will be the 4th AI Winter. This does not mean that there is not money to be made but it will not be in the companies that are building these behemoths but in the companies that supply them (e.g. Nvidia and Advanced Micro Devices) who may well see a sudden surge in demand as this bubble gets underway.

Technology

Report by

Inflection Point Research, LLC

IN

NVDA's dominance in AI workloads, both in cloud computing infrastructure and other implementations, remains very much intact - Michael Fox believes the bevy of current start-ups will have a steep uphill climb to get any traction in high volume AI deployments (i.e. cloud), and while Advanced Micro Devices and Intel have competing solutions that look good on paper, both fall short in ecosystem and support. Ultimately, Michael expects the real competition for NVDA’s dominance will come from internal chip developments at the hyperscalers. Fortunately for NVDA, any true competition is years down the road.

Rapidly detecting meaningful language changes in 10Qs / 10Ks

Analysis of the data and subsequent insights are driven by AI, NLP, data analytics and qualitative analyst oversight. Recent examples:

New Relic (NEWR) - Added the following wording to its 1Q23 10Q, “Businesses may look to rationalise their spending in response to such factors, which may impact our sales and renewal rates and negatively impact our business”.

Broadridge Financial Solutions (BR) - Added to its 2022 10K, “And the loss of any of such clients could have a material impact on our revenues and also result in an asset write-down of our client onboarding costs”.

Avnet (AVT) - Clear concerns re. cancellations, inventory and pricing.

Advanced Micro Devices (AMD) - Minor amendment to its 2Q 2022 10Q suggests they are more positive on cash flows.