Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

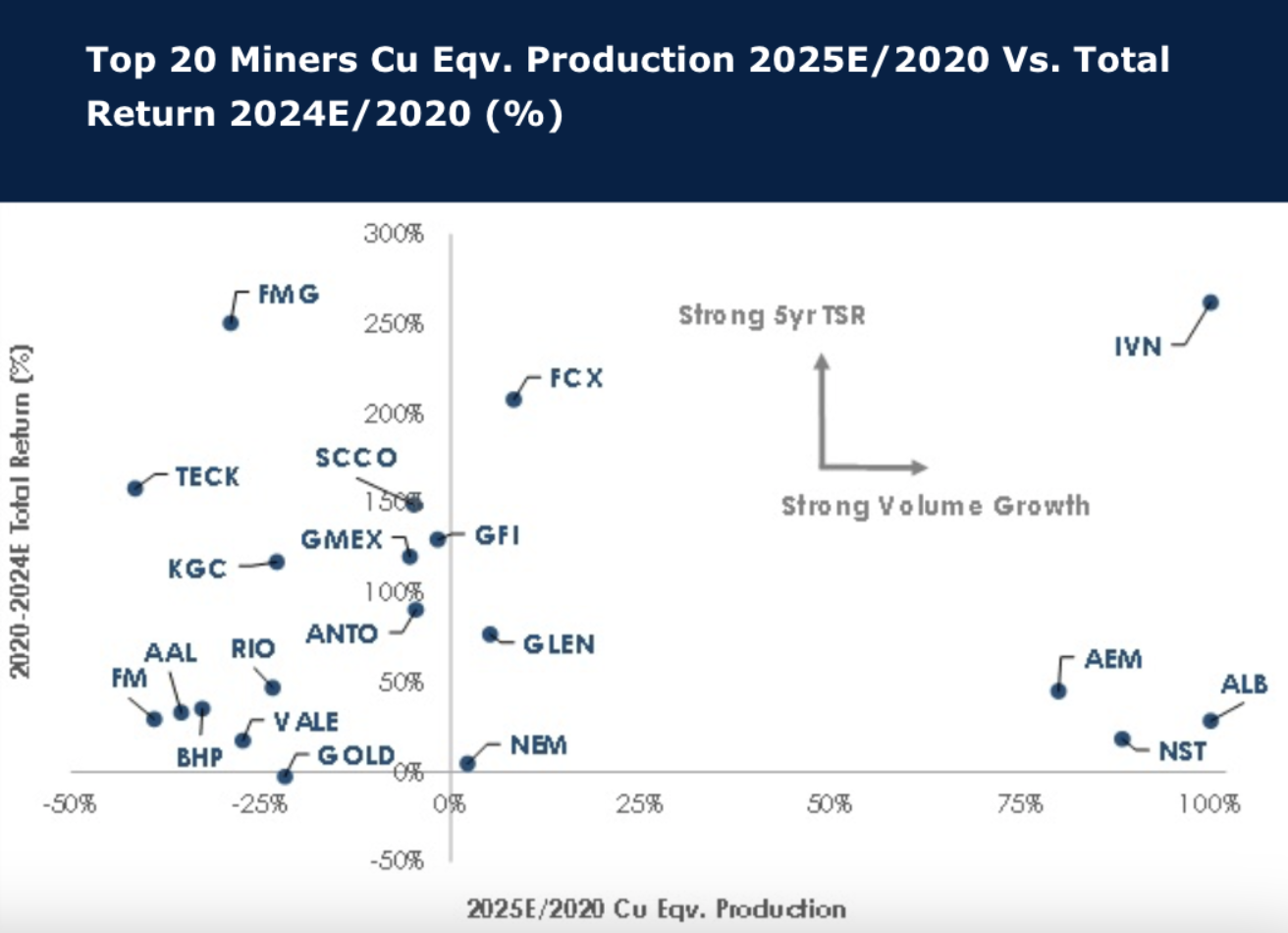

Large cap miners: Performance and growth are not related

As Sellside and Buyside set expectations for 2025, Global Mining Research examines the recent history of the leading miners. Interestingly, only Agnico Eagle Mines Limited, Albemarle Corporation, Ivanhoe Mines Ltd, and Northern Star Resources Limited are estimated to have materially grown through investment and M&A over 2020-2025E. In fact, most miners have shrunk in terms of Cu Eqv. Production, and exiting coal was a clear trend. The copper miners have outperformed, despite iron ore miners clearly returning the most cash to shareholders in dividends. Buybacks should have helped the share price return but there is little evidence this works. For over half the group, a ‘buy and hold’ strategy has not generated a robust return over the period. This reinforces the view that miners are to be traded.

Edition: 202

- 10 January, 2025

Materials

ALB sweetens its offer for Liontown to A$3.00/share, a significant premium to its initial reported offer of A$2.20/share in Oct 22. ALB’s persistent interest in LTR points to a long-term plan that would secure stakes in 3 of the top 5 Australian spodumene mines, while it also reduces Chilean exposure and increases US FTA compliant production. However, the downside is that it is a full price being paid, leveraging the balance sheet and likely locking ALB out of other moves, at least for a few years. GMR maintains their Sell rating on the stock.

Edition: 169

- 15 September, 2023