Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

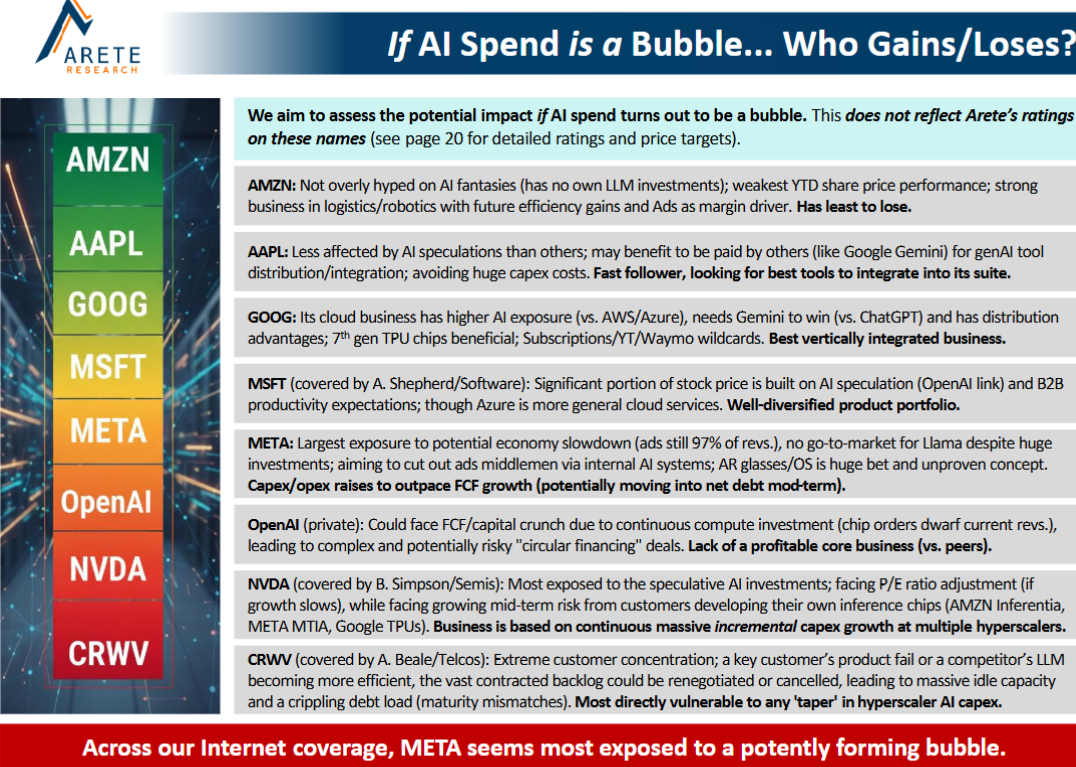

AI & Big Tech: Hunger Games, coming soon

Technology

Arete reviews the surge in Big Tech capex, with their forecasts 20-40% above consensus. They note the mismatch of long-term deals and shortening tech life cycles and accelerated depreciation, believing it will require Big Tech to address new TAMs or target each other’s businesses. Their report weighs whether this spending boom will prove to be a “bubble” and identifies who is most exposed. Arete sees Alphabet, Meta, Apple and Amazon all seeking to “own” a customer interface layer as GenAI products move into mainstream adoption.

Edition: 223

- 31 October, 2025

Fortum (FORTUM FH) Finland

Utilities

Pitched as a long idea at Revelare’s latest investor event, FORTUM operates in Europe’s most attractive market for AI datacentre development. Finland’s grid is mostly hydro and nuclear, with no marginal cost and power prices 60% below mainland Europe, while the cold climate further lowers datacentre cooling needs. All that is required for prices to rise back towards €100/MWh parity is new demand - and that is coming fast. Over 3GW of AI datacentre projects have already been approved, while Google has also bought a huge piece of land in the middle of the country and other hyperscalers are expected to follow. As Finnish power prices increase the company’s earnings should rise from €1 to €3 per share, implying the stock could reach €60 vs. <€20 today.

Edition: 223

- 31 October, 2025

Communications

Paragon Intel takes a negative view on CEO Sundar Pichai, arguing that his slow, consensus-driven leadership style has left the company “fast following” in an AI race it should be leading. While Pichai’s long-term vision and product instincts built successes like Chrome and Android, and his tenure has delivered impressive financial results, his risk aversion, conflict aversion, reluctance to refresh senior leadership and indecisive response to competitive threats like ChatGPT have led to internal stagnation. Paragon’s analysis includes interviews with 6 former Alphabet executives, who portray him as a thoughtful strategist and capable steward, but ill-suited to the fast, “wartime” pace the AI era demands.

Edition: 223

- 31 October, 2025

IT Survey: Robust spend, GenAI boom, staffing cuts

Technology

Rosenblatt’s July survey of 100+ senior IT managers reveals a surprisingly robust IT spending outlook, with two-thirds of budgets being revised higher since the start of 2025, despite macro concerns. GenAI is the top investment priority, with 60% increasing spend and nearly 70% expecting a material organisational impact. Over 75% expect developer staffing cuts of 10%+. Cybersecurity remains a defensive spending priority with investment flowing towards securing modern, distributed environments (Cloud, SASE/SSE) and data itself - benefitting CrowdStrike, CyberArk, Palo Alto, Zscaler and Fortinet. AWS fared much better, ranking first in "cloud service provider best positioned in AI", with 28% (vs. 16% in Dec 24), surpassing Google and Microsoft. Infrastructure names like Snowflake, Rubrik and MongoDB are also well-positioned amid data estate modernisation.

Edition: 216

- 25 July, 2025

Brookfield Renewable Partners (BEP CN) Canada

Utilities

BEP signs a landmark Hydro Framework Agreement with Google, representing the largest-ever corporate hydroelectric power deal. However, Veritas estimates the deal’s initial pricing of $56-76/MWh is below BEP’s current US hydro average of $83/MWh in 2024, contrasting with management’s expectation of ~2-4% annual FFO growth from hydro recontracting. Furthermore, BEP faces significant barriers to scaling beyond the initial 670 MW, including long-term contractual commitments and geographic mismatch between available hydro capacity and Google’s priority markets (PJM & MISO). Despite the market’s positive reaction to the news, Veritas maintains their Sell rating and TP of US$20 (30% downside).

Edition: 216

- 25 July, 2025

Communications

META is doubling down on AI infrastructure, raising its 2025 capex forecast to $64–72bn as it accelerates data centre construction amid rising costs. CEO Mark Zuckerberg is committed to making META a leading AI platform and insists on building in-house capacity to avoid reliance on others. While the AI strategy (centred on open source) is progressing well, it comes with a steep price tag, notably the ongoing $4bn+ quarterly burn at Reality Labs. Richard Windsor sees a growing risk of AI infrastructure overbuild, with META, Google, Microsoft and Amazon all ramping up spend - setting the stage for a painful correction. Despite this, META’s core business remains solid, with strong Q1 performance and improved operational efficiency via AI. At 23.5x FY25 PER, META is reasonably valued, but Richard prefers Google, where AI disruption risks from players like OpenAI are, in his view, overstated.

Edition: 210

- 02 May, 2025

Technology

Cyber diamond in the rough - unloved and out-of-favour, VRNS has underperformed its peers by a wide margin over the last 12 months. However, Felix Wang thinks its fortunes may start to change this year. His bullish thesis revolves around overplayed concerns re. the company’s ongoing SaaS transition and with continued product leadership, alongside a better sales team, VRNS's 2025 ARR and earnings guidance are beatable. Investors are highly sceptical of the company’s ability to reach $1bn ARR by 2027. This is why it is trading at only 6.6x 2026 EV/ARR. With a multiple re-rating and M&A optionality (Google's historic acquisition of Wiz for $32bn could open the floodgates to more M&A in cybersecurity), Felix sees 30%+ upside.

Edition: 208

- 04 April, 2025

Technology Spending Intentions Survey: Tracking tech budget trends & vendor demand

Technology

ETR’s Jan TSIS, based on responses from 1,835 tech leaders, projects 5.3% Y/Y IT spending growth in 2025, the highest since Jul 22. 73% of organisations plan budget increases, driven by cloud expansion and project acceleration. Notably, only 6% cited new vendor adoption, while 12% focused on enhancing capabilities with existing vendors - reinforcing debates around platformisation vs. vendor sprawl. TSIS tracks hundreds of companies and each quarter ETR publishes 200+ vendor specific reports. In their most recent webinar, they highlighted 20 vendors including AWS, Google, Salesforce, Snowflake, Workday and Zscaler - 13 had positive outlooks, 2 were downgraded and 3 maintained their outlook.

Edition: 205

- 21 February, 2025

AI: The disconnect

Richard Windsor suspects that genAI services make up only a tiny percentage of the revenue in companies like Alphabet, despite massive investments. This is a more serious problem than the overinvestment in internet capacity in 1999-2000 because the dark fibre sat there until it was needed. In contrast, AI technology evolves so rapidly that it could become obsolete by the time it's needed. 2020 was supposed to be the year of realised AI revenue, yet there is little sign of this—Richard’s research concludes an absurd going rate of 142x revenue to sales. He remains content with his AI adjacencies of interference at the edge, where he owns Qualcomm, nuclear power, and a basket of physical uranium funds, ETFs, and uranium miners.

Edition: 191

- 26 July, 2024

10Q / 10K text analysis

By utilising AI, NLP, data analytics and qualitative analyst oversight, 280First can glean material and actionable insights on companies which will be missed by most institutional investors. Recent highlights include: 1) Lockheed Martin - changing expectations for future aircraft delivery; LMT’s 2023 10K no longer references its previously expected 156 per year delivery rate. 2) Adobe - brighter capital resources outlook. Acquisitions planned? 3) Alphabet - higher expectations for operating margin trend. 4) Comcast - concerns on multichannel video provider agreements. 5) Mondelez - losing shelf space due to disputes. Delay / unable to raise prices. 6) Sysco - dialling back growth expectations.

Edition: 179

- 09 February, 2024

Communications

Andrew Freedman describes GOOGL's latest results as a classic case of good, but not good enough with expectations high going into the print. While the stock sold off, he does not see consensus numbers going lower for 4Q23 or 2024 off this report (if anything a touch higher). Assuming the Middle East conflict doesn’t escalate, Andrew’s base case continues to be for the ad business to accelerate to 13-15% growth in Q4 (vs. 10-11% consensus). He still sees $7.00-7.50 in EPS in 2024 * 23x (2018/19 average) = $161-173 stock… while downside is $6.50 * 18x = $117 (and that is pushing it). So, with the stock trading at $125, you have less than $10 downside and $40 upside in the next 6-9 months.

Edition: 172

- 27 October, 2023

Connectivity, speed & scale combine to blow up IT as we know it

Technology

In John Harrington’s latest Tech Trends report, he looks at several factors that have combined to change IT development and sales dynamics. These include how the accelerating deployment of speedier wired and wireless connectivity to the cloud, very fast computing platforms being built at scale within the clouds, the accelerating development of quantum computing as a viable commercial business, and the development of serious AI capabilities are affecting the global digital landscape. As IT increasingly transitions from in-house networking to the cloud, some new areas of IT will benefit, while others face an uncertain future.

Positive: Advanced Micro Devices, Alphabet, Apple, Amazon, Broadcom, Ciena, Dycom, Intel, IonQ, Microsoft, Nvidia, Rigetti.

Negative: C3.ai, Cisco, Dell, Qualcomm, Salesforce.

Edition: 162

- 09 June, 2023

Technology

Inflection Point Research, LLC

A Cloudy future is a good one - ANET is in a great competitive position, with tailwinds across all its end markets and product lines. Michael Fox points to the ongoing and accelerating networking upgrade cycles at Microsoft and Meta Platforms, in addition to greenfield business ramping at Alphabet as reasons to be bullish. Add to that share gains in an increasing TAM for enterprise / campus and you get the best networking growth story for the next two years.

Edition: 131

- 18 March, 2022

Market moving legal disputes…

MDC's “Event-Driven Legal℠" Weekly Report summarises near-term legal events including analysis on their potential as share-price catalysts for the indicated companies. Recent coverage includes:

Arbutus Biopharma and Genevant Sciences recently filed Patent Infringement Lawsuit against Moderna seeking licensing fees for the manufacture and sale of Moderna’s vaccine for COVID-19.

IDT Corporation's Defense of a shareholder lawsuit challenging the repurchase of an Indemnification Claim from Straight Path Communications that spared it from having to pay $614m in FCC fines.

Sonos and Alphabet's continuing battles at the US International Trade Commission and US District Courts.

Edition: 130

- 04 March, 2022

Sector rotation just hit a major inflection point

Energy, Financials and Value are IN, Tech and Growth are OUT - that's according to market timing and sector rotation specialist Michael Belkin. Having previously had an underperform forecast for both energy (S&P Energy -26% alpha from early Mar to end Aug) and financials (S&P Financials -10% alpha from its Jun peak to its recent relative low), his model forecast has just turned bullish for both these sectors on a 3-6 month view. This rotation also feeds into a reversal for value vs. growth - Michael has a fresh sell signal and underperform forecast for the likes of Alphabet, Amazon, Apple, Facebook and Microsoft.

Edition: 120

- 01 October, 2021

Ceridian (CDAY)

Technology

Underappreciated opportunity - CDAY’s Dayforce Wallet is the company’s first foray into a very different segment of the fintech ecosystem: digital wallets and earned wage access solutions. In this industry primer, Veritas assess the competitive landscape and compare CDAY's offering to products launched by Apple, Alphabet, PayPal, Square, Mastercard, Visa, Tencent and Alibaba. Veritas think the long-term gains of developing a fintech ecosystem are incredibly attractive and CDAY’s unique distribution advantage will help carve itself a piece of the market. Estimates that the module can generate ~US$220m of annual net earnings and be worth US$19 per share.

Edition: 114

- 09 July, 2021