Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

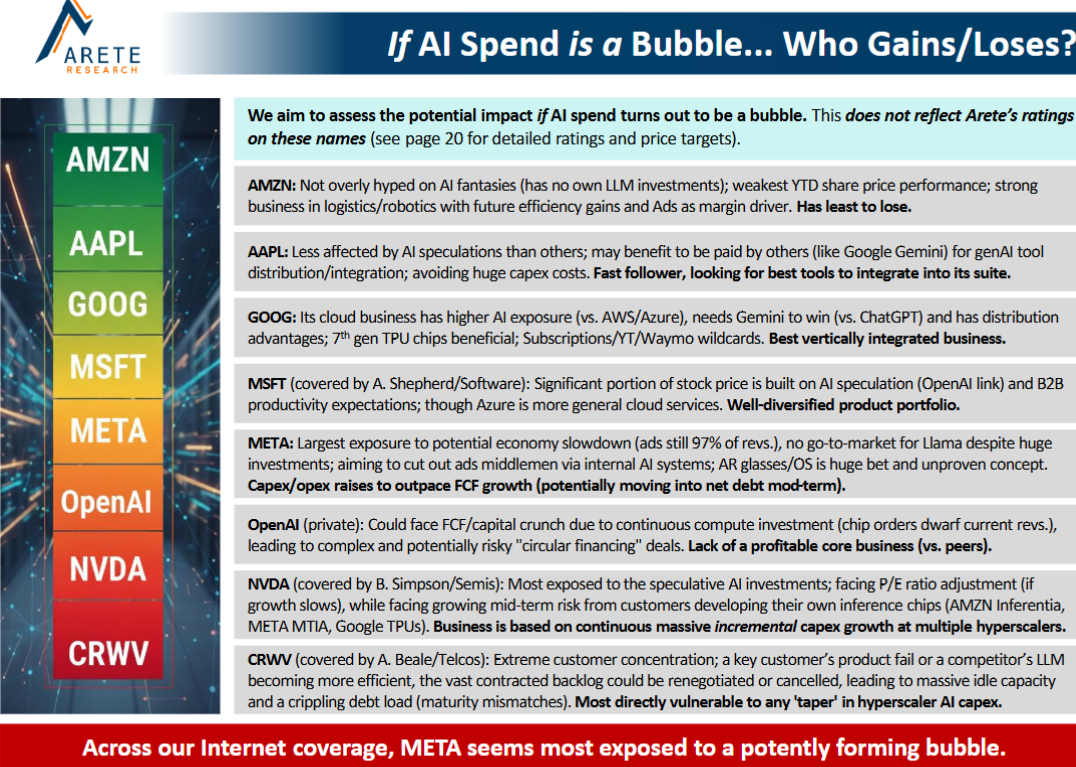

AI & Big Tech: Hunger Games, coming soon

Technology

Arete reviews the surge in Big Tech capex, with their forecasts 20-40% above consensus. They note the mismatch of long-term deals and shortening tech life cycles and accelerated depreciation, believing it will require Big Tech to address new TAMs or target each other’s businesses. Their report weighs whether this spending boom will prove to be a “bubble” and identifies who is most exposed. Arete sees Alphabet, Meta, Apple and Amazon all seeking to “own” a customer interface layer as GenAI products move into mainstream adoption.

Edition: 223

- 31 October, 2025

Something to Snack On: Amazon (AMZN) Drills Lowe's (LOW)

Consumer Discretionary

Amazon ran steep tool discounts over the holiday, highlighting Lowe’s pricing disadvantage. Across 25 items from brands like Bosch and Dewalt, Lowe’s averaged 27.5% higher prices; 15 items were cheaper on Amazon with average discounts of 34.6%, while only one was cheaper at Lowe’s. This follows R5's year-long observation that Lowe’s prices exceed Walmart’s on common goods. The wide gap raises concerns about Lowe’s gross margins and potential sales/earnings headwinds, even if housing improves. Meanwhile, Amazon’s aggressive pricing supports volume growth and advertising profits—a positive for AMZN but a structural challenge for broader retail.

Edition: 219

- 05 September, 2025

Consumer Staples

Scott Mushkin downgrades DG to Sell, citing widening price gaps with competitors, which threaten margins and volume share gains over the next 12-18 months. R5’s latest fieldwork shows a total basket premium of 9% vs. Walmart - well above the typical 3-7% range. Scott now sees pressure from WMT starting to impact the back half of 2025; while Amazon’s push to speed up delivery times in rural areas, coupled with its low pricing for everyday essentials also appears be gaining momentum. At the same time, Dollar Tree is making inroads into DG’s core markets. Finally, regulatory risks from SNAP eligibility changes and the MAHA movement targeting sugary foods are expected to negatively impact sales.

Edition: 217

- 08 August, 2025

IT Survey: Robust spend, GenAI boom, staffing cuts

Technology

Rosenblatt’s July survey of 100+ senior IT managers reveals a surprisingly robust IT spending outlook, with two-thirds of budgets being revised higher since the start of 2025, despite macro concerns. GenAI is the top investment priority, with 60% increasing spend and nearly 70% expecting a material organisational impact. Over 75% expect developer staffing cuts of 10%+. Cybersecurity remains a defensive spending priority with investment flowing towards securing modern, distributed environments (Cloud, SASE/SSE) and data itself - benefitting CrowdStrike, CyberArk, Palo Alto, Zscaler and Fortinet. AWS fared much better, ranking first in "cloud service provider best positioned in AI", with 28% (vs. 16% in Dec 24), surpassing Google and Microsoft. Infrastructure names like Snowflake, Rubrik and MongoDB are also well-positioned amid data estate modernisation.

Edition: 216

- 25 July, 2025

Nokia (NOKIA FH) Finland

Technology

NOKIA is undergoing a major transformation under new CEO Justin Hotard, who brings a Silicon Valley mindset to this legacy European company. The recent Infinera acquisition signals a strategic pivot from legacy RAN to high-growth hyperscale data centre infrastructure. The RAN business appears to have bottomed after a multi-year downturn, with pricing power set to improve amid the first hardware upcycle in a decade and increasing replacement of Huawei equipment in Western markets. NOKIA also benefits from stable IP licensing cash flows, expansion into new areas (Amazon streaming) and renewed momentum in networking. Despite a strong balance sheet, ~3.5% dividend yield and a clear path to margin expansion, the shares trade at just ~12x FY26 EPS. With potential EPS power of $0.70, the stock could “easily” double with minimal downside.

Edition: 216

- 25 July, 2025

Consumer Staples

Scott Muskin sees WMT as the “Nvidia of Retail” and explains why its equity could be worth a remarkable $250 per share. The upside is grounded in a powerful multi-year strategy driving accelerating earnings growth, supported by automation, expanding e-commerce profitability, surging advertising income, Walmart+ and improving sales mix. Scott draws bullish parallels to his experience in covering Amazon and its journey around enhancing profitability over the last 12+ months, as well as developing a WMT 2034 financial model similar to what he did to appraise AMZN's potential in its North American business. Fixing the “fresh” food offering through improved quality, delivery and in-store experience is also flagged as a critical catalyst for driving frequency, market share gains and a broader halo effect across the entire business.

Edition: 214

- 27 June, 2025

What is Amazon doing in its grocery store business?!

Consumer Discretionary

Amazon Fresh stores are an embarrassment, according to Scott Mushkin - just when he thought things couldn’t get any worse, his latest store visit reveals rampant out-of-stocks, incorrect electronic tags, as well as bizarrely low prices on certain items. Indeed, there were times when the AMZN price was nearly half of what Walmart was charging. While Scott currently does not see the lack of progress in the grocery business as a problem for the equity given how well the retail business is operated overall, getting fresh foods right will make a difference regarding the ultimate TAM of the business. He has advocated the need for a different approach, including floating the idea of spinning Whole Foods back out and keeping a minority stake.

Edition: 211

- 16 May, 2025

Communications

META is doubling down on AI infrastructure, raising its 2025 capex forecast to $64–72bn as it accelerates data centre construction amid rising costs. CEO Mark Zuckerberg is committed to making META a leading AI platform and insists on building in-house capacity to avoid reliance on others. While the AI strategy (centred on open source) is progressing well, it comes with a steep price tag, notably the ongoing $4bn+ quarterly burn at Reality Labs. Richard Windsor sees a growing risk of AI infrastructure overbuild, with META, Google, Microsoft and Amazon all ramping up spend - setting the stage for a painful correction. Despite this, META’s core business remains solid, with strong Q1 performance and improved operational efficiency via AI. At 23.5x FY25 PER, META is reasonably valued, but Richard prefers Google, where AI disruption risks from players like OpenAI are, in his view, overstated.

Edition: 210

- 02 May, 2025

Consumer Staples

Scott Mushkin upgrades UNFI to Buy with a $38 target (40% upside), citing its strong position in the healthy eating trend. He expects revenue to outperform management’s conservative guidance, fuelled by robust store growth at Amazon’s Whole Foods banner, UNFI’s largest customer. Margin expansion should come from the group's adoption of Lean Operation Management - boosting FCF, reducing debt and enabling future buybacks. Assuming a 55% natural/organic sales mix by FY28, EBITDA margins could surpass 2.3%, with earnings exceeding $4 per share. The stock currently trades at a ~12x PE, 5.5x EV/EBITDA on FY26 estimates. If Scott’s projections around growth and margins verify, not only will the company see better than estimated earnings growth, but valuation multiples will increase.

Edition: 210

- 02 May, 2025

Technology

ADEA has been swept up in the latest market selling as fears related to tariffs have taken hold even though the company generates its revenue from long-term licensing agreements. ~85% of revenue stems from pay TV and streaming video operators. The remaining portion is from semiconductor companies where tariffs remain an unknown. Q1 was filled with renewals as ADEA tries to leverage last year’s video streaming license with Amazon into new license agreements. Investors are overlooking the resilience of the business and the cash flow ADEA is able to generate this year to further reduce its debt. Hamed Khorsand expects the share price to bounce back when the company reports Q1 results in May. TP $18 (50% upside).

Edition: 209

- 18 April, 2025

Consumer Discretionary

An off-the-radar winner of the evolution of Amazon’s ambitions and role in the auto ecosystem - AMZN is not looking to own, prep and ultimately sell cars, but is instead looking to provide more content on its marketplace and to help dealers reach consumers. It was likely to have been a very competitive environment for a back-end auction platform to get status with AMZN and the fact that ACV has been chosen as its partner, signifies something special about the approach it is bringing to the market from a technology and go-to-market standpoint. Northcoast is increasingly confident in the company's growth trajectory and considers the pullback in the shares YTD as a buying opportunity. TP $28 (100% upside).

Edition: 208

- 04 April, 2025

Consumer Discretionary

The world’s largest e-commerce company is considering spinning off its India business and listing it on the domestic stock market. Data localisation requirements and the ability to maintain direct inventory are among the key factors driving this consideration. In recent years, AMZN has also faced certain challenges in India, losing market share to Flipkart and encountering increasing competition from Meesho, which recently raised over $500m in new funding. The Indian e-commerce market is projected to grow from $123bn in 2024 to $292.3bn in 2028, reflecting a CAGR of 18.7%. This rapid growth presents a compelling opportunity. Click here to access Joe Cornell’s Forbes article.

Edition: 208

- 04 April, 2025

Technology Spending Intentions Survey: Tracking tech budget trends & vendor demand

Technology

ETR’s Jan TSIS, based on responses from 1,835 tech leaders, projects 5.3% Y/Y IT spending growth in 2025, the highest since Jul 22. 73% of organisations plan budget increases, driven by cloud expansion and project acceleration. Notably, only 6% cited new vendor adoption, while 12% focused on enhancing capabilities with existing vendors - reinforcing debates around platformisation vs. vendor sprawl. TSIS tracks hundreds of companies and each quarter ETR publishes 200+ vendor specific reports. In their most recent webinar, they highlighted 20 vendors including AWS, Google, Salesforce, Snowflake, Workday and Zscaler - 13 had positive outlooks, 2 were downgraded and 3 maintained their outlook.

Edition: 205

- 21 February, 2025

Technology

Emerging competitive pressures from Amazon's in-house DSP create a very real and underappreciated bear case. Furthermore, TTD has likely been overearning the last several years as the majority of CTV spending occurred in the open internet, yet much of these ad dollars are now shifting back toward the walled gardens (AMZN / Netflix). TTD’s mature client base is no longer growing, rendering it increasingly reliant on customer spend growth. Amid lofty expectations and an elevated ~45x FY25 EBITDA multiple (>2x PEG vs. ~0.9x average for AdTech peers), the share price could fall as much as ~50% over the next 12-24 months.

Edition: 203

- 24 January, 2025

Big Tech: Asia vs. US - Samsung spoils the chase

Technology

2024 was a banner year for mega-cap US Tech companies, with Apple, Nvidia, Microsoft, Amazon and Meta rising a collective +64%. Were it not for Samsung Electronics crashing -41%, Asia’s mega-cap Tech companies (TSMC, Tencent, Samsung, Alibaba and Meituan) would have almost matched their US peers: +61% collective return (USD) without Samsung but +40% with Samsung. The good news: rolling into 2025, Crystal Shore has a positive risk rating on all 5 Asian Tech companies. Even Samsung.

Edition: 202

- 10 January, 2025

Do consumers need anyone else besides Walmart & Amazon?

Following WMT’s latest results, Scott Mushkin doesn’t think so. With market share flowing to WMT and AMZN at a quickening pace, which he sees being aided over the next few years by efficiency gains in distribution and logistics, as well as a growing high margin advertising business, other retailers will be pressured. At the same time, the increasing buying power of both companies could weigh on the margins of suppliers. Considering this backdrop, Scott sees slim pickings for investors owning other retailers, however, he does highlight the natural and organic grocery sector, as one that can grow quickly; he currently has a Buy on Natural Grocers, whose share price has risen 170% YTD.

Edition: 201

- 13 December, 2024

Consumer Discretionary

There is no bone for this dog - Scott Mushkin initiates coverage with a Sell rating and TP of $0! He forecasts EBITDA to decline to $217m in 2026 (vs. $401m in 2023) with margins expected to come under pressure in large part due to R5’s research that competition in the industry has increased meaningfully over the last few months. Indeed, their pricing surveys show that both Amazon and PetSmart are aggressively reducing prices. At the same time, macroeconomic headwinds will also hinder sales growth. All told, and considering the company’s substantial debt load (total debt/LTM EBITDA at ~4.7x at the end of 2Q), Scott sees no equity value.

Edition: 197

- 18 October, 2024

Amazon's aggressive pricing will likely have implications across retail

Consumer Discretionary / Staples

R5’s online pricing survey between AMZN and Walmart reveals shocking results - its one time purchase price basket was lower than WMT by 9%, which ballooned to 22% when they included all the discounting. With WMT generally considered to be the price leader, when R5 surveys retail stores, the incredibly sharp pricing by AMZN online could easily turn the holidays into a discounting jungle. Their research also reveals continued pressure on consumers and they believe the holiday selling period could be difficult for many retailers both from a revenues and profits perspective. They would exercise caution adding to positions, with the exception of AMZN, as it will likely gain share and it is the aggressor with the price cuts, suggesting that it is accounted for in its guidance.

Edition: 196

- 04 October, 2024

Beauty retail disruption

Consumer Discretionary

Ulta share losses accelerate as Sephora, TJX and Amazon are set up to win in US Beauty this fall / holiday. Q2 was a bloodbath at Ulta with historical promotional levels and muted traffic vs. Sephora. Amazon Prime Day highlighted new, exclusive product and the migration of prestige & luxury brands. TJX's core beauty presence continues to ramp up as holiday approaches. At the current level of execution, H2 appears bleaker than guidance.

Edition: 192

- 09 August, 2024

Technology

Vision sees risks for Allegro.eu (ALE.WA) shares due to rising competition. Despite slightly better-than-expected GMV and take rate growth, management's comments confirmed intensified competition, particularly from Temu, which is rapidly expanding in Poland. Allegro increased marketing spend to counter this, impacting future margins. 1Q24 revenue increased 6.6% YoY and adjusted EBITDA beat expectations at PLN 706mn, but net income missed at PLN 242mn. Vision believes increased competition from Temu, Amazon, and AliExpress, alongside rising delivery expenses, will pressure Allegro's profitability.

Edition: 188

- 14 June, 2024

Technology

A lot of IT Services companies that are employee-heavy and not prepared for the AI revolution, will get displaced by hardware- and software-based solutions. ACN has ~750k employees. Revenue per employee is lower than a restaurant group like Darden. The entire share price move during 2023-24 was ACN pitching themselves as an AI solution company; they have been trying to buy the expertise by doing small acquisitions but why would anyone hire them vs. using Microsoft or Amazon? ACN has negative organic growth in a massive AI tech spending boom and trades at a bigger multiple than MSFT! TP $200 (30% downside).

Edition: 185

- 03 May, 2024

Utilities

TLNE announces the sale of its zero-carbon data centre campus in Pennsylvania to Amazon Web Services for $650m. The transaction value is more than Hamed Khorsand was expecting and includes a power purchase agreement that would create a minimum of $300m of adjusted EBITDA over the next seven years for TLNE. Moreover, the group has additional assets for sale that could further showcase the underlying value of TLNE's current stock price. Further liquidation of assets could lead to the company being sold in pieces as it would have a small operating footprint to remain public. The share price is up more than 30% since Hamed turned bullish earlier this year.

Edition: 181

- 08 March, 2024

Key stories from Japan's retail and consumer markets

The latest edition of JapanConsuming includes commentary on 1) the proposal to bring Welcia and Tsuruha together to form a new FMCG mega-retailer. Although both are designated drugstores, their expansion into food and general FMCG means the creation of what will be Japan’s single largest retail chain by sales, sending shockwaves across the entire industry. 2) KDDI acquiring 50% of Lawson, making it a partner to Mitsubishi Shoji in running the third largest convenience store chain. It’s a big deal, but no one really knows what KDDI’s aims are. Some more imaginative analysts suggest this could be just the first step towards KDDI merging with Rakuten in order to beat Amazon.

Edition: 181

- 08 March, 2024

Technology

TSMC is enjoying renewed investor interest after its surprisingly strong Oct monthly sales. In KC Rajkumar’s view, the consensus bull thesis for 2024 - ASP increase as the 3nm node ramps, cyclical upturn in PC / smartphone - is inadequate. KC expects upside theme to TSMC’s consensus expectations next year includes significant 5nm demand from major cloud service providers - Microsoft’s newly unveiled AI accelerator chip and Amazon’s newly unveiled Graviton-4 CPU. Relative to Nvidia, KC believes TSMC is an inexpensive vehicle to invest in the AI theme as MSFT's internal AI program makes a major effort to find an alternative to NVDA’s GPU. TP NT$750 (30% upside).

Edition: 175

- 08 December, 2023

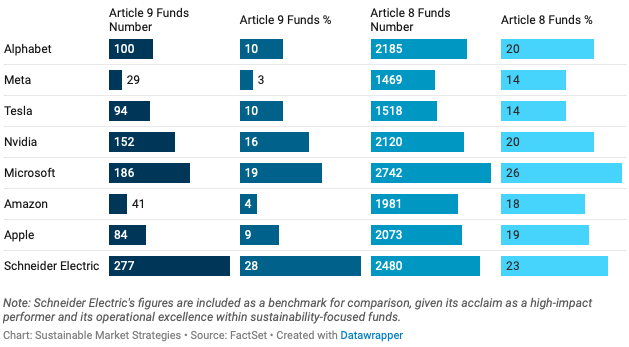

The Magnificent Seven

The impressive growth trajectory of the Mag 7 has been fuelled by AI and cloud computing, as money continues to chase their share prices higher despite pressure from rising bond yields on tech stocks’ long duration and their steep valuations compared to equity benchmarks. As pioneers in innovation, they are increasingly encountering legal challenges, but this has been intensifying as of late. The giants have a noteworthy presence in sustainable investment funds (see chart). However, the Sustainable Market Strategies team see the broad inclusion of these stocks as somewhat dubious. They tout Nvidia and Microsoft as the leaders, although the former is trading on a lot of AI hype and will fall short of growth expectations. Meanwhile, Amazon and Meta should be avoided as long positions in a sustainable strategy.

Edition: 173

- 10 November, 2023

Don’t miss out on Crypto

The chart of Crypto Total Market Cap Exclude BTH and ETH is one of the most bullish charts Raoul Pal has ever seen, which may well give us a repeat of 2015-17; this has been Raoul’s base case for a while. This would ignite Solana, which will break the inverse head-and-shoulders. There’s also some big news brewing in the crypto space, with the Bitcoin spot ETF about to get passed. Interestingly, when the SEC asked all of the ETF providers to say which exchange they will use, they all said Coinbase, which Raoul sees as a repeat of Amazon in the early 2000s. BUY Coinbase, Ethereum, Solana and double KR1 LONG position.

Edition: 165

- 21 July, 2023

Connectivity, speed & scale combine to blow up IT as we know it

Technology

In John Harrington’s latest Tech Trends report, he looks at several factors that have combined to change IT development and sales dynamics. These include how the accelerating deployment of speedier wired and wireless connectivity to the cloud, very fast computing platforms being built at scale within the clouds, the accelerating development of quantum computing as a viable commercial business, and the development of serious AI capabilities are affecting the global digital landscape. As IT increasingly transitions from in-house networking to the cloud, some new areas of IT will benefit, while others face an uncertain future.

Positive: Advanced Micro Devices, Alphabet, Apple, Amazon, Broadcom, Ciena, Dycom, Intel, IonQ, Microsoft, Nvidia, Rigetti.

Negative: C3.ai, Cisco, Dell, Qualcomm, Salesforce.

Edition: 162

- 09 June, 2023

Advanced AI: Sink or swim time for cybersecurity vendors

Technology

How are AI advancements and hype affecting the cybersecurity industry? What are data security vendors doing with AI/ML and cybersecurity automation, and can they protect their market from the major cloud operators with their investments in AI-driven security for their own platforms? During the interviews conducted by Blueshift, industry sources were also asked how they would play the sector near to mid-term and out over time. Companies discussed include Amazon, CrowdStrike, Cisco, CyberArk, Fortinet, Google, IBM, Microsoft, Okta, Palo Alto and Zscaler.

Edition: 158

- 14 April, 2023

Rapidly detecting meaningful language changes in 10Qs / 10Ks. Recent alerts include...

Acuity Brands (AYI) - Working on a large acquisition(s) that could endanger dividends / share repurchases?

Amazon (AMZN) - No more reduced prices for AWS customers?

Kilroy Realty (KRC) - Under pressure to lower rents and increase expenditures for re-leasing?

Microsoft (MSFT) - Growing concerns that government contracts are at risk of being cancelled?

Edition: 148

- 11 November, 2022

Financials

Andrew Hollingworth provides an update to his bull thesis having previously described the company as the “Amazon of finance” - it offers customers "no-trade-off" between good service and super low pricing. His early analysis revealed how SCHW would become extremely cash generative whilst continuing to grow. That day has now come - its arrival being delayed by its merger with TD Ameritrade. This piece focuses on what Andrew believes investors are missing and why Mr Market’s forecasts remain much lower than his own - 2023E EPS is $5.62 (vs. consensus at $4.80) and 2025E is $8.69 (vs. $6.30). TP $155 (100% upside).

Edition: 148

- 11 November, 2022

Consumer Discretionary

Delivering an inflection point - after two quarters of slogging through tough comps, incremental costs, and the rest...it is clear that AMZN is strengthening while other companies are weakening. Noteworthy highlights from 2Q22 include revenues accelerating and cost growth decelerating. No sign of discounting (stark contrast to others) and the competitive advantage of the fulfilment network is starting to shine through again. Advertising strength stood out (had the strongest quarter of all the large digital advertisers). AWS’ backlog is $100bn! It grew 65% this quarter (second highest rate in 3 years). AWS and Advertising are the entire valuation of AMZN right now.

Edition: 141

- 05 August, 2022

bpost (BPOST BB) Belgium

Industrials

Amazon’s insourcing of (part of) the last mile delivery is already having a negative impact on bpost’s parcels volume (-17% in 1Q22). However, the main threat of a local AMZN website will come from AMZN targeting small and mid-sized web shops to use its platform and its FBA services. By doing so, it would directly compete against bpost which is trying to compensate for the loss of its AMZN volume share by chasing new clients in this segment. Now is not the time for investors to go bottom fishing.

Edition: 139

- 08 July, 2022

Companies with dangerous inventory levels

"FISH" - First In, Still Here. Two Rivers deconstruct their Earnings Quality model to focus solely on one aspect of poor earnings quality: significant inventory slowdowns. This looks at 1) The materiality of inventory levels to the business. 2) The trend in turnover. 3) The magnitude of the slowdown. As the odds of recession rise, companies caught with excess inventory will find themselves forced to offer price concessions, leading to sales and margin declines, and to earnings disappointments. Highlighted names include Alcoa, Amazon, Arista Networks, Beacon Roofing, Beyond Meat, First Solar, LGI Homes and Walmart.

Edition: 139

- 08 July, 2022

Things are ugly in the crypto world, but that’s to be expected

Recent events in the crypto world haven’t dissuaded Raoul Pal, who explains that his crypto investments are a long-term secular trend that will play out over the rest of the decade. Right now, we’re experiencing inevitable volatility. He compares Bitcoin to Amazon, with the former providing a superior risk-reward for investors who suffered through the volatility. The same goes for Ethereum with a higher Sharpe Ratio of 1.6 to Bitcoin’s 1.31 since 2015. Don’t let the short-term pain dissuade you and stay LONG.

Edition: 137

- 10 June, 2022

Consumer Idea Forum

MYST’s group of Consumer specialists offered a diverse set of ideas ranging from M&A beneficiaries, capital return stories, “Value” bellwethers and potential overearners. Three of the most compelling ideas presented included…

Amazon (AMZN) - Self-help story with renewed focus on costs. AWS growth slowdown is temporary. Trades below tough valuation. TP $4970 (100%+ upside).

Jack in the Box (JACK) - Capital light with high margins and minimal cyclicality. Mispriced at 12x P/E (vs. peers at 20x+). TP $250 (200%+ upside).

MGM Resorts (MGM) - GGR growth to stall and margins contract even without a recession. With no fat left to cut, a 1% decline in GGR could wipe out FCF entirely. Selling real estate portfolio was “insane” given the permanently escalating rent MGM must now pay. TP $20 (40% downside).

Edition: 135

- 13 May, 2022

Technology

Mike Churchill sets a 12-month TP of R$8.46 (70% upside) for this consumer electronics distributor - based on 9x 2024 earnings (10.5% FCF yield) which seems fair given its growth rate, net income margins of ~10% and solid balance sheet. It appears Multilaser's IPO last year was time to capitalise on the lockdown boom. The share price has followed a similar pattern to former Brazilian glamour stock Magazine Luiza, which was all the rage a year ago (billed as the Brazilian Amazon), but has since fallen by 80%. However, the big difference between the two stocks, is that Magazine Luiza still trades at 100x earnings and 2.7x book vs. Multilaser at 6.8x earnings and 1.1x book.

Edition: 135

- 13 May, 2022

$5bn reasons why we’re watching Amazon's Project Kuiper

AMZN just made history with the largest commercial launch contract ever, cementing Project Kuiper as Starlink’s most formidable competitor - in their new 9-page brief, space sector analysts at Quilty Analytics break it down, focusing on implications to the sector at large, including the three big contract winners (Arianespace, Blue Origin, ULA), the GEO market (Inmarsat, Intelsat, SES, Eutelsat) and other heavy-lift launch operators (Firefly Aerospace, Relativity Space, Rocket Lab).

Edition: 133

- 14 April, 2022

Technology

Has an appealing proposition for consumers in the emerging BNPL industry, but sellers are not seeing much differentiation among the leading competitors, according to Blueshift’s interviews with merchants, payment industry specialists and payment technology developers. Sources also revealed how the industry is ripe for consolidation (Amazon to acquire AFRM?); how BNPL will continue to grow in the US but won’t match the adoption rate internationally; as well as voicing concerns around credit risk and increased regulation.

Edition: 130

- 04 March, 2022

Breaking M&A news

Betaville published two proprietary intelligence alerts in Dec 21 and Jan 22 highlighting how Audioboom, the Aim-listed, podcasting business was at the centre of takeover speculation, including the possibility of interest from a US-based technology giant. At the time of the first alert, BOOM’s shares were trading at £14.20. On Sunday, Sky News reported that both Amazon and Spotify are looking at purchasing the company. The shares are now trading above £20.00.

Edition: 129

- 18 February, 2022

Boon For Commercial Satellite Industry From US Military’s “Pivot to LEO”

Communications

The US Space Development Agency (SDA) is launching satellite services that will stimulate the commercial industry, according to leading Space sector analysts, Quilty Analytics. The 60-page briefing summarises the SDA’s plan, highlights sector developments and constellation updates for Amazon, OneWeb, SES, SpaceX and Telesat, and offers in-depth analysis on topics including space sustainability, Viasat/Inmarsat acquisition, and GEO satellite launches.

Edition: 124

- 26 November, 2021

Allegro (ALE PW) Poland

Technology

At the IRF Short Ideas conference in June, Vision explained its thesis, including increased competition (Amazon and others), high household penetration, and rising cost pressures. Amazon recently announced the rollout of Prime in Poland and Shopee has announced its entrance. Since the conference shares are down ~14% while the Stoxx600 is up ~1%.

Edition: 121

- 15 October, 2021

Clean Energy Fuels Corp (CLNE)

Energy

Actively integrating its business into the rapidly growing RNG supply chain. Recent deal with Amazon provides significant business model validation. CLNE is set to benefit from a more robust sales network, added scale, and a larger balance sheet. Expect RNG production, distribution, and consumption to continue growing significantly. TP $13 (~45% upside)

Edition: 121

- 15 October, 2021

Sector rotation just hit a major inflection point

Energy, Financials and Value are IN, Tech and Growth are OUT - that's according to market timing and sector rotation specialist Michael Belkin. Having previously had an underperform forecast for both energy (S&P Energy -26% alpha from early Mar to end Aug) and financials (S&P Financials -10% alpha from its Jun peak to its recent relative low), his model forecast has just turned bullish for both these sectors on a 3-6 month view. This rotation also feeds into a reversal for value vs. growth - Michael has a fresh sell signal and underperform forecast for the likes of Alphabet, Amazon, Apple, Facebook and Microsoft.

Edition: 120

- 01 October, 2021

Technology

Has ESTC found the right formula to stand out from the competition in search, security, and observability? Source feedback was far more negative than in Blueshift’s previous report, especially around the threat from Amazon. One source even suggested it would be “game over” for ESTC if AMZN offers a fully managed version of its forked Elasticsearch service. ESTC’s recent license model change (aimed at preventing AMZN from reselling its product) is unlikely to have much impact.

Edition: 118

- 03 September, 2021

Consumer Staples

This small cap niche company is quickly becoming a dominant force in the in the healthy-sugar/sugar-substitute market while also targeting the broader and rapidly growing free-from category. Led by CEO Albert Manzone, FREE's highly experienced management team is one of the key reasons why Scott Mushkin believes investors should take a hard look at the company. Management’s integration and streamlining of operations is already paying dividends through shelf gains in stores, as well as better Amazon search placements. TP $24 (>100% upside).

Edition: 117

- 20 August, 2021

Amazon (AMZN)

Consumer Discretionary

AMZN is at an important inflection point as it builds out an enormous distribution and logistics network - once completed no other company will come close to offering the same service. Management envisage that by speeding up delivery the market opportunity will be enlarged significantly. Scott Mushkin’s research strongly supports this notion. Further, as this natural monopoly matures, he sees a strong possibility that the government will step in and separate parts of the enterprise - this is likely to be value enhancing for equity holders.

Edition: 116

- 06 August, 2021

Brazil’s droughts to threaten agricultural output

Climate change and deforestation in the Amazon rainforest are being pointed at as the reasons behind the country’s latest drought, the worst in 91 years. Electricity supply has suffered - no longer being generated from dried up hydropower reservoirs - and is threatening the agricultural powerhouses of the country. With agriculture accounting for more than 25% of GDP, a profound change is needed or else the worst has yet to come.

Edition: 113

- 25 June, 2021

DoorDash (DASH)

Communications

Clear case to be made that DASH can rise from an upstart restaurant ordering/delivery company into an empire spanning Restaurants, Convenience, Grocery and other CPG categories. Hedgeye believe that the company can easily exceed $70bn in Marketplace GOV in FY24, up over 80% from $37bn in FY21. Their bullish thesis also includes DASH’s opportunity to monetise DashPass (compares it to Amazon Prime/Starbucks Rewards) and its potential to capture substantial market share in the digital advertising space.

Edition: 113

- 25 June, 2021

Zooplus (ZO1 GR)

Consumer Staples

An online-only niche business that has outcompeted Amazon and built real scale economics - it has a 40% share of the EU online pet food market and its customers love it, but Mr Market less so. Why? Well, it is a little old-fashioned in its desire to grow slow and steady, generating scale, customer loyalty and cash along the way. Its US peer (Chewy) has grown itself and its end market (US only) far faster and as a result trades on c.5x sales (vs. Zooplus on a lowly 0.88x). One day either Zooplus’ scale economics payoff or Chewy comes calling…

Edition: 113

- 25 June, 2021

Lack of customer expertise hurts Enterprise IT sales

Technology

Blueshift primary research finds the effectiveness of cloud-based applications is swiftly diminishing the need to retain in-house IT staff, leaving a dwindling pool of experienced workers clinging to familiar last-generation technologies, instead of staying current on newer IT capabilities. Hence, enterprise technology sales are likely to miss a hoped for rebound in H2 to the direct benefit of the public cloud operators. Positive: Amazon, Datadog, Microsoft. Negative: Cisco, IBM, Snowflake.

Edition: 111

- 28 May, 2021