Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

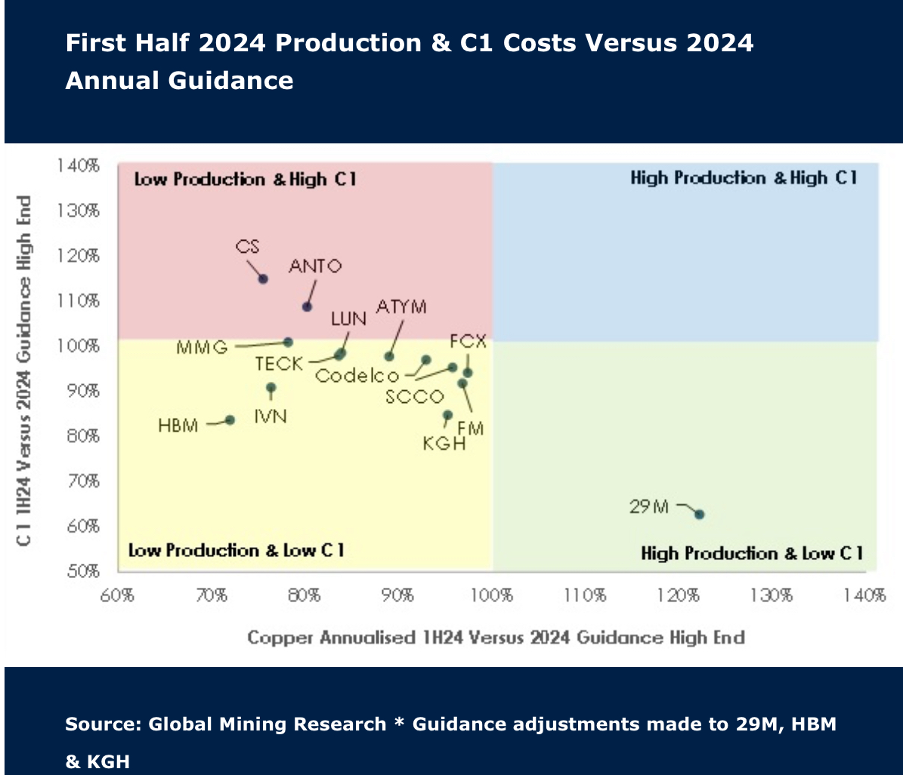

Can copper volumes meet big expectations?

As expected, the first half of the year was met with weaker production, with companies in Global Mining Research’s coverage reporting flat figures of +1.5% and low capex. Costs increased some 4.8%, but this was offset by a ~US$0.60/lb increase in copper prices in the latest quarter. 60% of producers are expecting stronger H2 volumes, but Antofagasta, Ero Copper, Ivanhoe Mines and Capstone Copper are most at risk of missing 2024 guidance. Following the recent pullback and ahead of seasonally stronger Q4 prices, GMR continues to see the sector as attractive. Ratings have been raised for leveraged plays KGHM (to buy) and MMG (to hold).

Edition: 193

- 23 August, 2024

Increasing overweight position in copper

David Radclyffe recently published on the positive supply outlook for copper, setting out the scene for near- and medium-term market deficits and noted the lack of new projects to fill demand. In addition to the near-term price forecast, the long-term copper price forecast has been lifted to $4.00/lb in 2023 dollar terms. As a result, the sector trades on a prospective 2024 EV/EBITDA of 8.2x, and P/NPV10 of 1.3x. For equities, copper exposure remains in demand and is likely to drive more M&A. Investors may move along the equity risk curve to small caps. Capstone and Sandfire Resources are preferred in the small cap copper stocks, and Antofagasta and Grupo México in the mid/large ones.

Edition: 151

- 06 January, 2023