Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

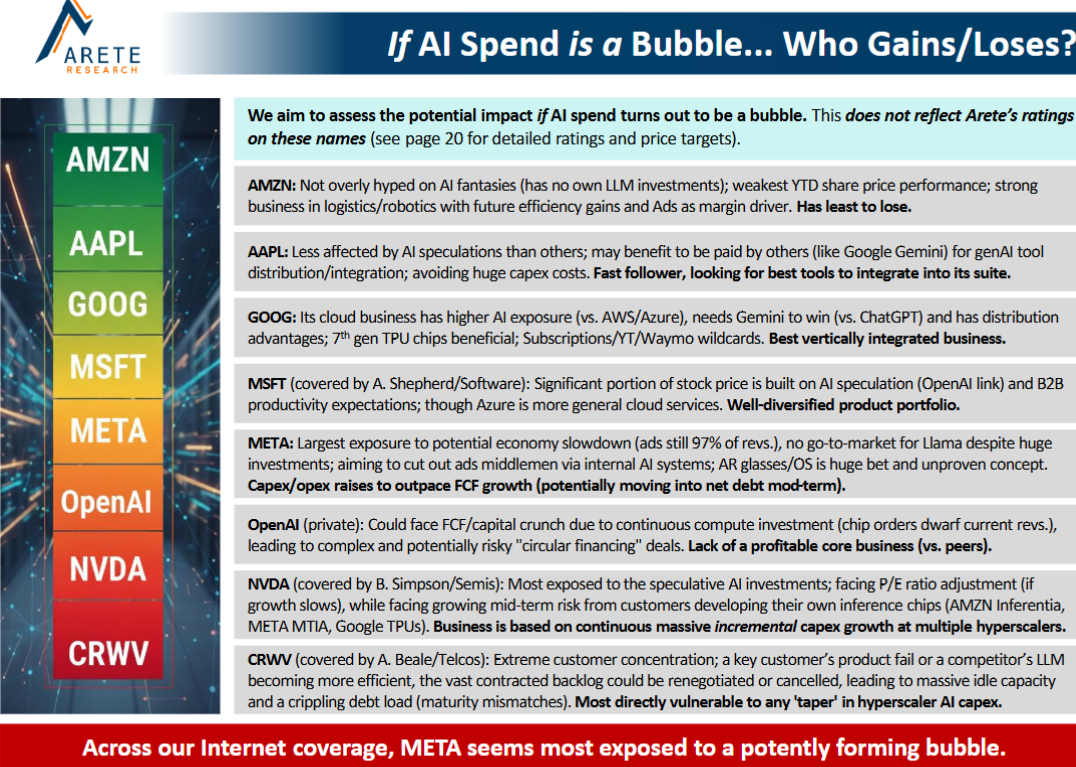

AI & Big Tech: Hunger Games, coming soon

Technology

Arete reviews the surge in Big Tech capex, with their forecasts 20-40% above consensus. They note the mismatch of long-term deals and shortening tech life cycles and accelerated depreciation, believing it will require Big Tech to address new TAMs or target each other’s businesses. Their report weighs whether this spending boom will prove to be a “bubble” and identifies who is most exposed. Arete sees Alphabet, Meta, Apple and Amazon all seeking to “own” a customer interface layer as GenAI products move into mainstream adoption.

Edition: 223

- 31 October, 2025

India trumps China

When Team Trump’s “Tariff Liberation Day” exploded across Asia ex-Japan, the impact varied widely from country to country. The worst hit markets were China, Taiwan, Singapore and Vietnam (-20%). But the following markets were relatively unscathed: India (-4%), Indonesia, Thailand and the Philippines. The reason is straightforward: the latter countries have relatively modest exports to the US. Furthermore, some of these countries could stand to benefit from the US-China trade war with a number of companies - like Apple - choosing to relocate their manufacturing away from China. Crystal Shore currently ranks India No.1 in Asia-ex-Japan. A list of their top-ranked stocks (large / mid-cap) is available on request.

Edition: 209

- 18 April, 2025

Technology

The Apple Killer - Xiaomi is eating up global market share in smart phones, tablets, home electronics and now cars. Erik@YWR feels like many investors are living in a bubble. They don’t spend time outside the US and Western Europe. They don’t go to Africa, the Middle East, or South Asia and see how brands like Xiaomi are gobbling up the world markets. Brands like AAPL and Western car companies are getting boxed into a smaller and smaller market. If the dam breaks and Xiaomi gets momentum in Europe it will do serious damage to AAPL. You can see the network effects it is creating. Make the phone, the tablet, the home appliances and the car, and have it all interconnected with its AI system.

Edition: 208

- 04 April, 2025

Big Tech: Asia vs. US - Samsung spoils the chase

Technology

2024 was a banner year for mega-cap US Tech companies, with Apple, Nvidia, Microsoft, Amazon and Meta rising a collective +64%. Were it not for Samsung Electronics crashing -41%, Asia’s mega-cap Tech companies (TSMC, Tencent, Samsung, Alibaba and Meituan) would have almost matched their US peers: +61% collective return (USD) without Samsung but +40% with Samsung. The good news: rolling into 2025, Crystal Shore has a positive risk rating on all 5 Asian Tech companies. Even Samsung.

Edition: 202

- 10 January, 2025

China: iPhone sales revival comes at a cost

Consumer Discretionary

86Research’s latest MNC* report highlights a revival of iPhone sales in China following the new series release, but driven by an unsually large discount. They suggest that this may be signalling a concession Apple must make in the high-end phone market which has been increasingly competitive. Investing in further offline store expansion does not fully address the challenges and they continue to see persistent pressure on the company's market share and profit margin trends.

*86Research's weekly Multinationals in China publication provides dynamic, accurate and reliable economic, competitive and regulatory, on-the-ground, insight from Multinational companies operating in the country. Investors can subscribe separately to MNC.

Edition: 198

- 01 November, 2024

Apple Silicon in the Cloud

Technology

KC Rajkumar thinks through the implications of Apple potentially adapting its client-focused Apple Silicon for AI applications in its data centres. He reasons Apple Silicon in the cloud has several interesting advantages over incumbent Nvidia’s GPU solution. KC thinks the company is taking a major step to diversify away from its dependence on unit volume of Apple products and instead leverage its power-efficient Apple Silicon for delivery of lucrative Gen AI services. Servers based on Apple Silicon in the cloud could quarterback the delivery of Gen AI services to Apple’s c.2.2bn client devices. KC expects a gradual run-up in the stock into the WWDC event next month. TP $220.

Edition: 186

- 17 May, 2024

The Metaverse: A year to forget

A rotten year for The Metaverse which has one more gift to give with the cancellation of ByteDance’s Pico 5 headset, one of the most popular devices for developers. Cancellations like this and a market that halves will only serve to delay the take-off of The Metaverse as well as slow the development of the ecosystem around it. While the release of the Apple Vision Pro in 2024 could trigger renewed interest, Richard Windsor believes the segment remains uninvestable at the moment. He is keeping tabs on Roblox and Unity, but both companies are too expensive and their shares look set to stagnate / decline for a while yet.

Edition: 176

- 22 December, 2023

Semis & Hardware: Real-Time Views

Technology

Arete’s monthly newsletter covers the latest updates in the global tech hardware and semis markets, with a particular emphasis on foundry, memory, compute, semi-cap, wireless semis, and EV/autos. Highlights from their Nov edition include: 1) Dramatic shift in memory - Q4 price surge signals shift from a buyers’ to a sellers’ market. 2) HBM market dynamics - is AMD diversifying its HBM supplier base with new SK Hynix deal? 3) Why Huawei looks set for a bumper 2024 and US sanctions backfire. 4) Why Apple’s spend at TSMC might be flat in 2024, curbing TSMC recovery. 5) Auto semis - content is king in 2024. 6) Lithium-ion battery outlook - all-time-high earnings amid all-time-low valuations. 7) To infinity and beyond - satellite semis growth in the 2020s.

Edition: 174

- 24 November, 2023

Technology

Preliminary results from Samsung combined with TSMC’s monthly revenue disclosure gives Richard Windsor increased confidence that the inventory correction has come to an end. Of all the component suppliers, QCOM is now trading at the bottom of its peer group in terms of PER ratio which demonstrates just how short-term the market thinks. There is no end in sight to its sales of 5G modems to Apple, it is winning enough deals in automotive to seriously disturb Mobileye and it is very well positioned for the Metaverse when or if it takes off. From a long-term valuation perspective, the shares are on sale.

Edition: 171

- 13 October, 2023

Technology

Buy the dip even as AI momentum shows cracks - as the semis complex comes under pressure for all the right reasons (disappointments at Apple, loss of momentum in AI, analog inventory, China trade worries), KC Rajkumar believes (near-term) long ideas in semis have become harder to come by. However, he argues the Street has become too negative re. traditional servers and expects investors to gravitate towards AMD despite ongoing worries regarding share gain of its MI300. Over time, KC would not be surprised if up to a third of Microsoft’s AI servers come to be based on an AMD solution vs. the dominant share Nvidia currently enjoys.

Edition: 167

- 18 August, 2023

Novatek Microelectronics (3034 TT)

Technology

3Q23 guidance misses expectations due to intensified pricing competition in smartphone OLED driver IC and AceCamp’s industry surveys reveal Chinese peers could gain additional market share as a result of accelerated localisation of smartphone components. Compounding matters, Samsung will also soon begin selling its OLED driver IC to Chinese smartphone makers. AceCamp believes Novatek could have only 15-20% unit market share in Apple’s OLED driver IC orders in 2024 (vs. consensus estimates of 30-40%). Their 2024/25 EPS forecasts are 30-40% below consensus; valuing the stock at 10-13x 2024/25 PE, implies 40%+ downside.

Edition: 167

- 18 August, 2023

Connectivity, speed & scale combine to blow up IT as we know it

Technology

In John Harrington’s latest Tech Trends report, he looks at several factors that have combined to change IT development and sales dynamics. These include how the accelerating deployment of speedier wired and wireless connectivity to the cloud, very fast computing platforms being built at scale within the clouds, the accelerating development of quantum computing as a viable commercial business, and the development of serious AI capabilities are affecting the global digital landscape. As IT increasingly transitions from in-house networking to the cloud, some new areas of IT will benefit, while others face an uncertain future.

Positive: Advanced Micro Devices, Alphabet, Apple, Amazon, Broadcom, Ciena, Dycom, Intel, IonQ, Microsoft, Nvidia, Rigetti.

Negative: C3.ai, Cisco, Dell, Qualcomm, Salesforce.

Edition: 162

- 09 June, 2023

Technology

Inflection Point Research, LLC

China contagion has spread to the US as IPR’s carrier, retail, and supplier checks indicate iPhone 14 sell-through continues to soften, coming in below expected demand for Apr. IPR believes AAPL’s planned test equipment purchases from Keysight, LitePoint and Anritsu were cancelled or delayed, suggesting slower production looking into 2H23. RF component purchases from Qualcomm, Cirrus, Broadcom, Skyworks and Qorvo have been trimmed, reflecting weakening demand. AAPL's Q3 hardware sales typically drop about -9% Q/Q, but IPR believes iPhone 14 could see declines closer to -20%. The iPhone 15 could also prove disappointing.

Edition: 161

- 26 May, 2023

Technology

KC Rajkumar continues to see substantial downside to the stock from current levels as and when investors come to appreciate the secular decline in Product revenue and stagnant Services revenue. He forecasts iPhone revenue down 10% this year and down 5% in FY24. KC expects (overall) FY23 revenue to be down 6.5% vs. consensus down 2% and FY24 revenue to be down 3% vs. consensus up 7%. He models FY23 at $369bn/$5.6 vs. consensus at $386bn/$5.9 and FY24 at $358bn/$5.4, significantly below consensus at $414bn/$6.6. TP $110 (35% downside).

Edition: 160

- 12 May, 2023

Technology

Inflection Point Research, LLC

Could report an in-line Mar quarter, but IPR expects AAPL to guide down as it faces headwinds on softening demand across multiple product lines - IPR’s US carrier store checks suggest iPhone 14 inventories increased in Feb / Mar. While China iPhone sell-through checks suggest ~10% growth for the quarter, the tech giant could find recent improvement difficult to sustain on normalising demand post-reopening. Checks on Macs are consistent with last quarter, showing continued weakness with no end in sight. Checks with Apple watches, Air Pods, and other accessories paint a grimmer picture of forecasts down up to 50% Y/Y, indicating significant inventory build due to very weak end markets.

Edition: 158

- 14 April, 2023

Novatek Microelectronics (3034 TT)

Technology

The Street is overly optimistic about the firm’s outlook in 2023/24 due to 1) gross margin and ASP contraction and 2) lower-than-expected gross margin and uncertainty for Apple’s OLED driver IC orders. AceCamp expects structural negatives for the display driver IC sector including 1) intensified pricing competition in large / small-sized display driver IC and 2) 20-30% dollar content decline for ram-less OLED driver IC despite a rising penetration. Their 2023/24 EPS forecasts for Novatek are 25-30% below consensus estimates and they expect 30-40% derating for the stock over the next 12 months.

Edition: 155

- 03 March, 2023

Technology

Inflection Point Research, LLC

IPR’s industry checks indicate a recent significant change in AAPL procurement - order cuts have been made across the board, including iPhones, Macs, iPads, Watches, and accessories. It is likely to take some time for supply and demand to normalise causing problems for suppliers in the near term. In a separate note, IPR also discusses the recent Bloomberg report re. AAPL's plans to replace Qualcomm and Broadcom iPhone chips with in-house solutions. IPR believes this is just the first round of a negotiation dance between Tim Cook and Hock Tan, that will ultimately lead to another LTSA.

Edition: 152

- 20 January, 2023

Communications

During each of the first two weeks of the NFL season, DirecTV’s NFL Sunday Ticket streaming service went dark at numerous times. On top of this, some customers were unable to log in and numerous users complained that the Sunday Ticket app blacked out certain games even though they were available locally. After this football season, NFL Sunday Ticket will likely have a new home because DirecTV’s rights are set to expire this year. Google (GOOG) and Apple (AAPL) are reportedly in the running to secure the rights.

Edition: 145

- 30 September, 2022

Technology

Form over substance - unimpressed with AAPL’s latest launch event, Richard Windsor believes the tech giant is now going to feel the full sting of the weak macro environment. Against this backdrop, the shares are not particularly cheap and there are plenty of other options to look at that offer far higher growth at a lower multiple. In a separate note, Richard also discusses the difficulties AAPL faces to keep both the CCP and the US Congress happy and is likely to be forced to drop its budding relationship with YMTC, meaning the Chinese memory chip maker will disappear once again into industry obscurity.

Edition: 144

- 16 September, 2022

Communications

Using Craig Huber’s 2024 EBITDA estimates and segment multiples in his SOTP analysis suggests that the current price is implying an overly punitive 42% conglomerate discount to NWSA’s valuation. If management won't break up the company, then they should at least sell / spinoff Subscription Video Services and break out Professional Information into its own segment. Craig notes that there are signs that NWSA’s portfolio is moving in the right direction including some shrewd acquisitions as well as content licensing deals with Google, Facebook and Apple, but the stock has been trapped in underperformance (7 of last 9 years) and something big needs to change here.

Edition: 142

- 19 August, 2022

In-house modem development is tougher than it looks

Inflection Point Research, LLC

The blogosphere continues to buzz that Apple's in-house modem will not ship in 2023 and the iPhone 15 will ship with 100% Qualcomm silicon - while Michael Fox does not believe AAPL has “failed”, it is proving to be more difficult than Johny Srouji and his team anticipated. AAPL highly unlikely to risk all-important iPhone franchise on first-generation internal silicon; will begin the switch with iPads / Macbooks which have simpler use models. As with AAPL, Samsung continues to struggle with its LSI modem. Despite years of experience with developing / shipping in-house modems, design flaws could push the company to ship all 2023 Galaxy S models with QCOM modems.

Edition: 140

- 22 July, 2022

Carmageddon

Apple declares war on OEMs - expansion of CarPlay into the instrument cluster pushes OEMs further away from the Digital Life of the vehicle and brings them closer to being handsets on wheels. RFM’s research has found that electrification and autonomy could reduce vehicle transport spending by up to 65% which no OEM is likely to survive in its current form. Hence, it is crucial that OEMs have a seat at the table when it comes to delivering digital services in the vehicle. So far OEMs have kept Google out of the heart of their vehicles, they now need to treat AAPL in the same way.

Edition: 138

- 24 June, 2022

ESG in gold mining

Metals Focus’ new annual report, The Gold ESG Focus, is due for release in July. The extensive report compares a wide range of senior gold producers, including the likes of Barrick Gold, Endeavour, IAMGOLD and others. Looking at topics such as emissions, water, waste, biodiversity and health & safety, the report features “apple versus apple” ESG comparisons for the included companies. Please contact us to find out more.

Edition: 136

- 27 May, 2022

Technology

Smartphone sector China demand risks are still not fully appreciated - consensus believes the premium end of smartphones will outperform the overall smartphone market, as they did in 2021. However, Lynx believes that this year, it will be the low-end of the price spectrum that outperforms. Ultra-low-priced 5G models will flood the developed markets (especially the US). A shift away from high ASP models is not good news for QCOM. The degree of weakness at China brands is also being underestimated (QCOM is heavily exposed). Even in the iOS domain, QCOM’s downside has not been fully priced in; expects Apple iPhone shipment in FY22 to underwhelm investors.

Edition: 133

- 14 April, 2022

Communications

Have Apple’s new privacy restrictions permanently damaged Snapchat’s ad business? AAPL’s new anti-tracking restrictions represent more of a short-term headache than any permanent degradation of SNAP's ad value, according to Blueshift’s interviews with advertisers, agencies and other industry specialists. However, perception of SNAP as an ad vehicle skewed negative, with sources citing a lack of innovation, slow movement on e-commerce tools and a continued perception of Snapchat as a messaging app.

Edition: 127

- 21 January, 2022

Something to Snack On: Three that Should Thrive

Consumer Staples

Walmart, Target, and Albertsons, roughed up by last month’s choppy market, are now building momentum and recent pullbacks present buying opportunities. WMT-Home Depot partnership shows a positive business trajectory. TGT is creating an unrivalled total experience allying with Levi's, Apple and Disney. ACI's company specific initiatives, including streamlining purchasing and growing its private brands, show the business is strong.

Edition: 121

- 15 October, 2021

Sector rotation just hit a major inflection point

Energy, Financials and Value are IN, Tech and Growth are OUT - that's according to market timing and sector rotation specialist Michael Belkin. Having previously had an underperform forecast for both energy (S&P Energy -26% alpha from early Mar to end Aug) and financials (S&P Financials -10% alpha from its Jun peak to its recent relative low), his model forecast has just turned bullish for both these sectors on a 3-6 month view. This rotation also feeds into a reversal for value vs. growth - Michael has a fresh sell signal and underperform forecast for the likes of Alphabet, Amazon, Apple, Facebook and Microsoft.

Edition: 120

- 01 October, 2021

Ceridian (CDAY)

Technology

Underappreciated opportunity - CDAY’s Dayforce Wallet is the company’s first foray into a very different segment of the fintech ecosystem: digital wallets and earned wage access solutions. In this industry primer, Veritas assess the competitive landscape and compare CDAY's offering to products launched by Apple, Alphabet, PayPal, Square, Mastercard, Visa, Tencent and Alibaba. Veritas think the long-term gains of developing a fintech ecosystem are incredibly attractive and CDAY’s unique distribution advantage will help carve itself a piece of the market. Estimates that the module can generate ~US$220m of annual net earnings and be worth US$19 per share.

Edition: 114

- 09 July, 2021