Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Technology

Richard Windsor says MediaTek’s Kompanio Ultra chip sets a new standard for the high end of the Chromebook market and looks to be merely a stone’s throw from Intel and Advanced Micro Devices facing another newcomer in the PC Market. The biggest winner will be Arm, which will see its penetration of PCs accelerate and it will earn higher royalties from MediaTek which buys the processor design and licences the IP. This is neutral for Qualcomm because competition in this space is healthy and will keep the firm on its toes and push it to continue to lead when it comes to performance. INTC and AMD are the real losers here as the x86 architecture looks increasingly obsolete.

Edition: 209

- 18 April, 2025

Communications

SoftBank to invest up to $40bn in OpenAI starting with a $10bn tranche this month of which it will fund 75% itself. It will source the funds from Mizuho Bank although the group has sufficient cash on hand already. SoftBank's LTV ratio increases from 12.9% at Q3 end to c.17%. It should be able to raise up to $46bn in funding through asset-backed finance and borrowing up to the 25% LTV level relative to commitments of c.$47bn (OpenAI, Ampere, Aug payment to SVF for ARM and the initial Stargate push). SoftBank will probably lose money this quarter but not so much it doesn’t end the year in the black. Vision Fund was down $1.1bn, largely on India weakness (-$1.2bn across its four public investments) with the rest of the portfolio moving sideways. The discount to NAV has widened slightly to 55% but remains well within the recent trading range. TP ¥11,000 (65% upside).

Edition: 208

- 04 April, 2025

NBK (NBK KK) KK

Financials

The Kuwaiti lender's lower profitability and dividend yield compared to peers undermines its premium valuation. NBK's 9M 2024 results showed a 6% y/y growth in attributable net profit underpinned by a 7% increase in operating revenues and controlled impairment loss. The decline in non-interest income is quite concerning especially as the monetary policy cycle begins to ease which should put pressure on NIMs. The credit demand in Kuwait is affected by the economic recession and the political crisis in early 2024. Improving NBK’s fundamentals is going to take time. Recall that its Islamic arm, Boubyan Bank and Gulf Bank have decided not to go ahead with a merger, which could have created a single Shariah-compliant bank with US$50bn+ in assets.

Edition: 203

- 24 January, 2025

Communications

Galliano's Financials Research

The current share price discount to the stated NAV of 53% may seem optically attractive, but Victor Galliano believes this figure will be subject to valuation headwinds going forward. Arm (45% of SoftBank Group’s equity value) is starting to experience limits to its “growth at any price” stock status. It trades at super-premium valuations which are unsustainable, not least as Nvidia trades on less than half the prospective earnings multiple for just slightly lower forward consensus EPS growth. Furthermore, while the JPY’s depreciation is supportive of the group NAV, with the Fed’s hawkish stance well known and BoJ expected to raise interest rates, JPY weakness may be largely done.

Edition: 184

- 19 April, 2024

Communications

A surge in the value of Arm Holdings has provided some support for SoftBank shares since an early Dec swoon although the discount has also widened as markets have been hesitant to allocate full value to short-term changes in NAV and (probably) an uncertain yen. Kirk Boodry expects the long-term story for SoftBank will be aligned more with Vision Fund activity, both monetisation and a step up in investment pace, but the discount here provides an attractive entry point (discount to NAV currently stands at 50% - the largest it has been since the Covid sell-off in Mar 20). In Kirk’s latest report he updates his model for Q3 (Dec) including forecasts for the quarter.

Edition: 177

- 12 January, 2024

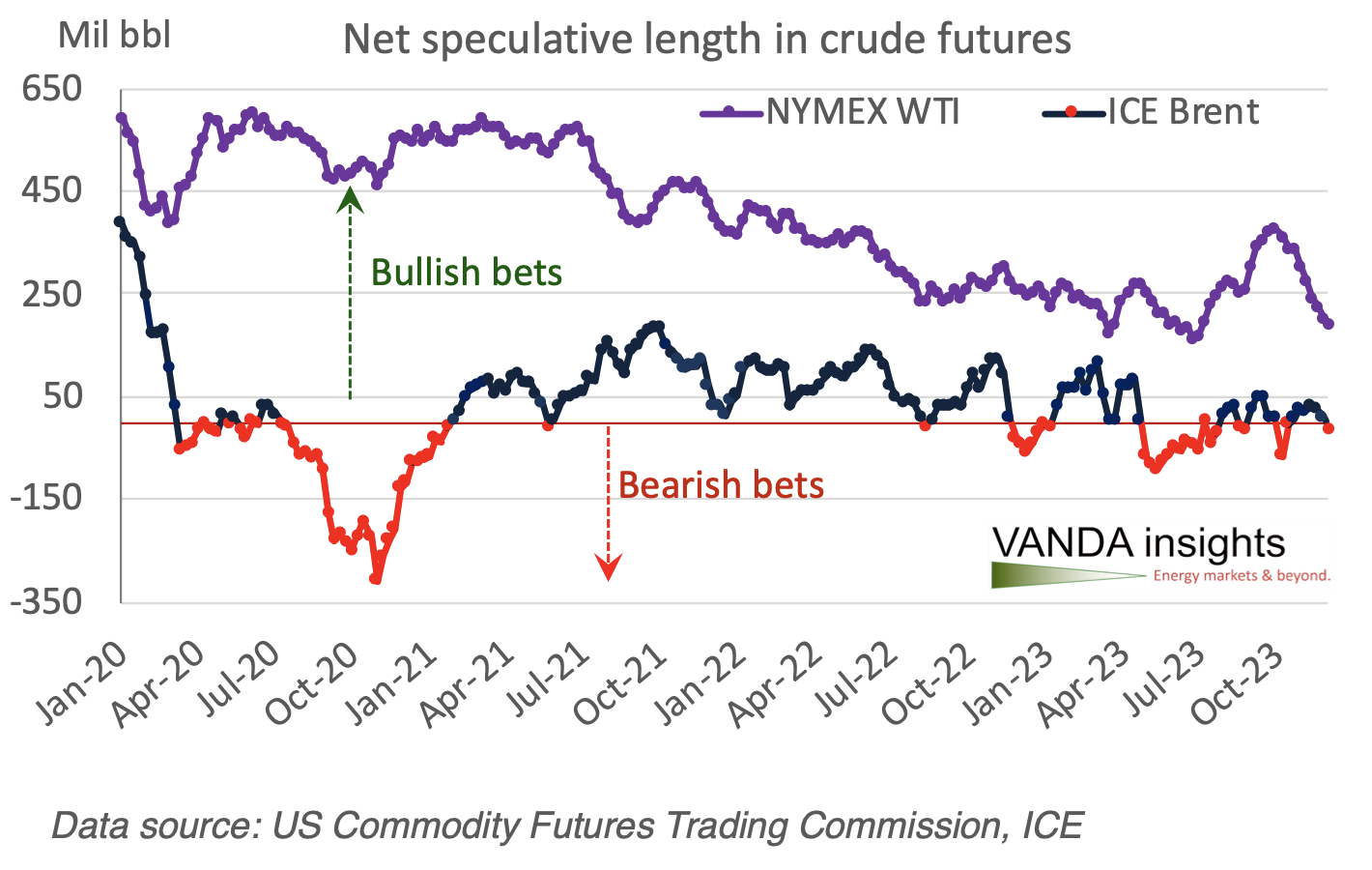

Crude escapes the blues, but don’t bet on a rebound

After the US Fed unexpectedly changed its tune, pencilling in 75 basis points of rate cuts next year, bets on a US economic soft landing came back in full force and overjoyed investors piled into risk assets. Even crude got a shot in the arm from Powell’s remarks, but Vandana Hari remarks that this may not be the early Christmas present from the Fed to the OPEC+ alliance that it may seem. She sees limited runway for crude purely from the latest upturn in risk appetite in the broader financial markets, and remarks that even the most bullish have tempered their views. A bearish view of supply-demand fundamentals going into 2024 has a strong grip on oil sentiment and is unlikely to be pushed aside easily.

Edition: 176

- 22 December, 2023

Healthcare

There has been much excitement around Merck and MRNA's latest cancer vaccine after ASCO, with data appearing impressive. However, Foveal Research’s latest report suggests otherwise, with the vaccine Keytruda combo performing similar to historic Keytruda alone, along with an unusual underperformance of the control arm that flatters results. Secondary endpoint at ASCO reveal the real concerns over the true treatment effect of MRNA's addon. Dr Amit Roy pitched this idea at our recent Equity Shorting Conference. Click here to listen.

Edition: 170

- 29 September, 2023

Communications

Galliano's Financials Research

Victor Galliano continues to be cautious on SoftBank due to its 1) WeWork exposure (estimated at USD 1.8bn and looks increasingly to be at risk of being written off), 2) the risk of over-valuation of private companies in the Vision Funds (private companies accounted for 64% of SVF1’s fair value with SVF2’s private companies accounting for 84% of the fund’s total equity value) and 3) Masa’s debts to SoftBank (USD 5.1bn). In the near term, the upside potential to equity value rests largely with the Arm IPO, but Victor is concerned that its AI credentials may well be being overstated by SoftBank's management.

Edition: 167

- 18 August, 2023

Healthcare

In newly published data from MRK / MRNA’s PD1 + mRNA cancer vaccine trial at AACR last week, headline efficacy may be flattered by Keytruda alone control arm underperformance by c.11% compared its historic phase III performance, with the vaccine combination arm performing similar to previous monotherapy Keytruda alone trials, suggesting the phase III confirmatory trial may have a higher than expected hurdle to beat.

Edition: 159

- 28 April, 2023

Merck (MRK) & Gilead (GILD) / Arcus Biosciences (RCUS)

Healthcare

Dr Amit Roy remains concerned over the added benefit of TIGIT to established PD1 therapy for MRK and GILD / RCUS. As expected, the street’s expectations over MRK’s TIGIT in cancer was misplaced again, as it failed to beat chemo in later line lung cancer. GILD / RCUS 1st line TIGIT data also appears equivocal with large imbalances in baseline characteristic and an underperforming PD1 arm in high PDL1 expressers. Moreover, the TIGIT + PD1 response of 41% still falls short of response rate seen with Keytruda alone. Amit also remains concerned about MRK’s prospects in first line lung, with, again disappointing response rate of just ~33% in patients naïve to PD1 therapy.

Edition: 157

- 31 March, 2023

Technology

Sumeet Singh runs the rule over SK Telecom’s cybersecurity arm as it looks to raise US$860m in its upcoming Korea IPO - a key issue for Sumeet relates to the proportion of revenue that SKS derives from related parties. It has increased from 15.7% of revenue in 2019 to 25.5% by 2021 and accounted for 43.4% of growth in FY20 and 65.6% in FY21. In addition, he has previously flagged how SKS’s physical security and cybersecurity segments have been suffering from margin pressure for several years and the fact that the company is now heavily in debt. The stock is being offered at an expensive looking 8.2-9.3x FY23 EV/EBITDA, 2.4-2.7x FY22 EV/Sales and 44-55x FY22 P/E.

Edition: 134

- 29 April, 2022

Communications

Transfer of Arm China shares does nothing but raise red flags - Arm moves its shares in China JV to a special purpose vehicle which it owns together with SoftBank. While this could technically eliminate the obstacles to an audit for an IPO, Mio Kato believes regulators would be remiss in allowing such a flimsy change to pass muster. In addition, the move reeks of desperation for cash and SoftBank’s typical disregard for prudence and the importance of due diligence to investors. Stay short.

Edition: 133

- 14 April, 2022

Technology

The FTC drops the hammer as it announces that it will be suing NVDA (and SoftBank) to block the acquisition of Arm - this is a significantly stronger move than any other regulator has made so far and the scale of the remedies required could end up destroying the value of the deal for NVDA. The simplest solution to SoftBank’s ownership of Arm is to put it back where it found it on the LSE. The problem here is that this deal is now worth $80bn to SoftBank thanks to the blistering rally in NVDA’s share price. If Arm relists on the LSE (or even the Nasdaq), achieving a valuation of this magnitude will be almost impossible.

Edition: 125

- 10 December, 2021

UK: New government interventionism?

New government scrutiny of individual takeovers (incl. ARM and Newport Water Fab) has raised concerns over the UK entering a more interventionist paradigm. These forces shouldn’t be overstated according to Charles d’Arcy-Irvine: the UK is still an outlier among the G7 in its reluctance to intervene. That said, the cat is now out of the bag and politicians will continue to dance to the tune of interventionism.

Edition: 116

- 06 August, 2021

MediaTek (2454 TT)

Technology

High-quality 5G beneficiary that also offers a very attractive dividend - earnings upgrade cycle set to continue. MediaTek will experience an outsized benefit from the replacement trend brought by technology upgrades to 5G and Wi-Fi 6, Bluetooth, and ARM-based SoCs that integrate wireless communication. It also boasts net cash of $5.9bn (nearly doubled over the past 2 years); management have raised the dividend payout ratio to 80-85% and budgeted NT$100bn for special cash dividends over the next 4 years. The stock currently trades on a forward dividend yield of 5.2%. TP NT$1292 (40% upside).

Edition: 113

- 25 June, 2021

Nvidia (NVDA)

Technology

Blueshift Research examine whether dramatic developmental changes in chip technology are putting increased pressure on NVDA to close its deal to buy Arm - smart everything means that the standard edge-to-the-data center model is going to break; a new kind of edge-based compute fabric centred around Arm’s tiny chip designs will rapidly emerge - an area that NVDA does not have a strong foothold. They also consider opposition to the deal to be short-sighted especially since Softbank cannot fund the innovation necessary for Arm to continue to evolve chip architecture.

Edition: 109

- 30 April, 2021