Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

The energy transition just switched time zones

When it comes to the energy transition, developed markets dominate portfolios, yet the real growth and valuation upside lie in EM clean-tech leaders. It appears that the investment map is upside down. The scale of acceleration in EM is staggering, with 80% of new solar and wind capacity in 2025 being built outside of the US and Europe, and solar imports in Africa jumping 60% year-on-year. The original script for the energy transition was that developed markets would lead the way, with their wealth, policies and moral resolve. 2025 has torn up that playbook. The West has been tripping over its own ambition by erroneously investing in premature or uneconomic tech. Portfolios anchored to Western policy cycles remain exposed to subsidy rollbacks, voter mood swings, and bureaucratic inertia — while emerging-market clean-tech firms are growing revenues at roughly twice the global sector average.

Edition: 223

- 31 October, 2025

Why the gold price is falling back (for now)

In this presentation, Jeffrey Christian of CPM Group discusses the recent volatility across the precious metals markets, particularly gold’s sharp retreat from nearly $4,400 to just above $3,900. He explains the role of momentum traders who entered the market aggressively as buyers in October and have since begun unwinding positions, creating the sharp short-term pull back in the markets. Jeff looks at these price movements in the broader context of ongoing political and economic uncertainty; including the continued US government shutdown, expectations for Federal Reserve rate cuts, and shifting investor sentiment. He also discusses similar volatility in silver, platinum, and palladium, noting how speculative and technical factors have overshadowed fundamentals.

Click here to watch.

Edition: 223

- 31 October, 2025

Will China continue to export inflation to the rest of the world?

Andrew Hunt points out that China’s domestic economy remains soft. Domestic policy conditions look to have tightened: fiscal policy is notably less expansionary and liquidity growth has cooled slightly. The corporate sector’s weak financial situation has led to another bout of export price deflation / rising export shipments to the rest of the world, potentially deflationary for the global economy. Markets in general appear complacent on this issue. However, the crucial question is whether the PRC will continue to recycle the proceeds of its current account surplus into outward investment. China ceasing to export inflation via its capital account would represent a major deflationary shock to the world. Andrew is concerned that intensifying domestic credit constraints may force a reduction in capital outflows as companies are obliged to use funds at home. If CNY shows signs of appreciating further, he would view this as a potential warning sign for global markets.

Edition: 223

- 31 October, 2025

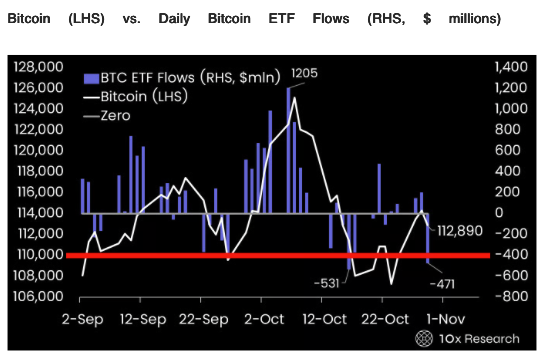

Bitcoin at a line in the sand

Bitcoin trades on shifting sentiment and positioning. The past five months haven’t been because demand disappeared, but rather because a massive transfer has been taking place beneath the surface, with early-cycle OG holders selling and new institutional capital steadily absorbing supply, keeping Bitcoin range-bound. If ETF buyers return following the China-US meeting and the latest FOMC decision, Bitcoin can resume its rally. However, Powell’s slightly hawkish tone and decision to delay QT’s end could keep ETF demand sidelined at a moment when it matters most. As long as Bitcoin holds the $110,000–$112,000 support zone, the 10X Research team are prepared to stay aligned with upside momentum, but a break below $110,000 would trigger a reduction in long exposure – that level remains their hard stop.

Edition: 223

- 31 October, 2025

Venezuela: US intervention

The Don-roe Doctrine is taking shape as the Trump administration intensifies its war against cartels in the Western Hemisphere. The recent deployment of significant military assets to the Caribbean, the authorization of a covert action program in Venezuela, and a rhetorical escalation against cartels are putting intense pressure on Venezuelan President Nicolás Maduro. Now, a constellation of forces—principally driven by US Secretary of State Marco Rubio—is even pushing for direct intervention in Venezuela, up to and including regime change. Niall Ferguson sees a heightened probability of US strikes between now and February. While “regime change” is not his base case, there are meaningful pathways to escalating intervention. Once strikes start, they become very hard to stop. Although Niall expects volatility ahead, bonds have continued to rally, likely due to market sentiment that whatever happens in Venezuela is better than the status quo. Despite the uncertainty, the bond rally looks likely to continue.

Edition: 223

- 31 October, 2025

Full of (soy) beans

Spot soybean meal (USD293.90) has been ranging for many years, finding support at 251.00–290.00 and resistance at USD471.00–554.00. The support area has been intact for 16.5 years and in recent months it has been tested again. With spot soybean meal emerging from the support area, Chris Roberts wants to put on an initial long position. Go 50% long at market. The initial stop loss is a daily close below USD256.00. At the same time, he will exit his long spot soybean oil long position.

Edition: 223

- 31 October, 2025

China: Households ready to invest

The PBC conducts quarterly surveys of firms, banks and households. Paul Cavey says these are useful, because they have long time series – and because for households, there is otherwise a dearth of detailed survey data. The bank and business surveys suggest that sentiment in both sectors is weak compared with ten years ago, but not looking particularly bad relative to the experience of more recent years. In the household survey, price expectations remain very weak. For overall inflation, that is probably in part because actual inflation, particularly for food, has been low. Households are pessimistic about income and employment, although the picture isn't consistent. For consumption, the shift away from spending on goods to consuming services is intact. The one big change in the household survey was the jump in the proportion inclined to make "financial investments". Paul notes that this could be another sign that China's economy is reaching some kind of structural turning point.

Edition: 223

- 31 October, 2025

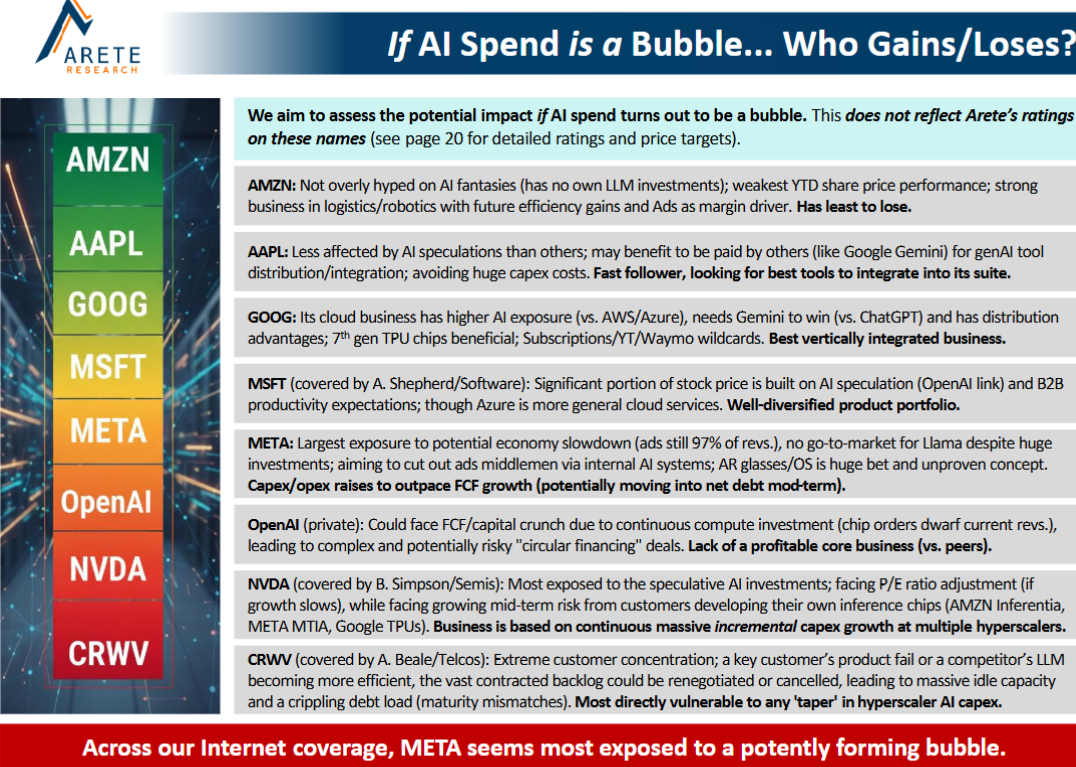

AI & Big Tech: Hunger Games, coming soon

Technology

Arete reviews the surge in Big Tech capex, with their forecasts 20-40% above consensus. They note the mismatch of long-term deals and shortening tech life cycles and accelerated depreciation, believing it will require Big Tech to address new TAMs or target each other’s businesses. Their report weighs whether this spending boom will prove to be a “bubble” and identifies who is most exposed. Arete sees Alphabet, Meta, Apple and Amazon all seeking to “own” a customer interface layer as GenAI products move into mainstream adoption.

Edition: 223

- 31 October, 2025

Fortum (FORTUM FH) Finland

Utilities

Pitched as a long idea at Revelare’s latest investor event, FORTUM operates in Europe’s most attractive market for AI datacentre development. Finland’s grid is mostly hydro and nuclear, with no marginal cost and power prices 60% below mainland Europe, while the cold climate further lowers datacentre cooling needs. All that is required for prices to rise back towards €100/MWh parity is new demand - and that is coming fast. Over 3GW of AI datacentre projects have already been approved, while Google has also bought a huge piece of land in the middle of the country and other hyperscalers are expected to follow. As Finnish power prices increase the company’s earnings should rise from €1 to €3 per share, implying the stock could reach €60 vs. <€20 today.

Edition: 223

- 31 October, 2025

Argentina: Milei’s landslide

Javier Milei won the Argentine midterms decisively with his candidates winning in 16 of 24 provinces, with ~40.8% of the total vote. Most surprisingly, Milei’s La Libertad Avanza (LLA) even won the Buenos Aires province—home to 37% of the country—after losing a local election by 13 points in September. Niall Ferguson sees the victory as firmly consolidating the government’s programme and renews the value of its alliance with former President Mauricio Macri’s PRO in key districts. Milei’s victory speech was conciliatory and clearly opened the door to new alliances with regional governors, which the US has been insisting on. Niall also expects further changes to the FX regime, which still needs reform. The other key winners are President Trump and Treasury Secretary Scott Bessent, who will see this result as vindicating their support for a Latin American government aligned with the United States. Expect strong rallies in Argentine assets.

Edition: 223

- 31 October, 2025

US: How come treasuries are so bid?

This is the question James Aitken was asked repeatedly at Citi’s Australia Conference. Treasuries continue to defy the sticky inflation, debasement, fiscal crisis, Trump risk premium narrative. Swaption skews, however, continue to suggest treasuries will remain bid. Some kind of ‘AI productivity’ angle also helps treasuries or at least ensures inflation expectations remain well anchored. James suggests to shave it down with Occam’s Razor. The US budget deficit/GDP is going to end 2025 with a low 5% handle. Pending financial regulatory relief (leverage ratio) means the big US banks have the capacity to add treasury duration. And James thinks several of them will, in scale. An end to QT means the Fed will reinvest to keep treasury holdings constant, and to maintain the WAM of SOMA holdings which is currently ~8.3 years. That, too, probably ensures the ~10-year part of the curve remains well behaved. All in, James bets the ten-year note will remain supported.

Edition: 223

- 31 October, 2025

Japan: A pause, not a reversal

Japan was another victim of Friday’s Trump tantrum. Since Japanese markets have recently been on a tear, but that trade was crowded. The recent setback wasn’t only about positioning, there was a dent in the confidence in the idea that a new phase of reflationary policies was evolving. Investors had piled into Japan expecting a smooth handover and a return to Abenomics 2.0. We are in the first inning and the market had run ahead of itself. Paul Krake views the situation as a pause, not a reversal. The underlying thesis remains compelling, an AI-driven productivity revival in a country where demographic decline once guaranteed stagnation. Japan may well prove to be the largest economic beneficiary of AI, precisely because of the constraints that have long held it back. A brief shakeout in positioning, combined with a short-term political wobble, does not change that story.

Edition: 223

- 31 October, 2025

US equities: The case for value

Tian Yang is changing his long-held bias against value stocks and recommending a shift to overweight value vs growth. He points out that he is finally seeing alignment across A) market behaviour, B) the macro-outlook, and C) bottom-up fundamentals. On his indicators, today's set up is as good as it has been since the GFC for value to outperform. US earnings estimate revisions have broadened since Liberation Day, which has historically been indicative of value vs growth outperformance over the next 12 months (first chart below). At the same time, he notes a sharp fall in the correlation of the Russell 1000 market cap weighted index vs the equal weighted index. As the second chart shows, this correlation collapse has often marked a low in the value-to-growth ratio historically. Tian is also seeing evidence of a rotation into value stocks over the past couple of months.

Edition: 223

- 31 October, 2025

EM Telcos: When does digital drive a re-rating?

Communications

New Street examines when EM Telcos transition from being “Telcos with digital assets” to “Digital-first” companies and when the market begins to re-rate them accordingly. Their analysis of Safaricom and SoftBank Corp suggests that valuation multiples expand once digital revenues reach 15-20% of total sales. New St flags VEON, MTN, Airtel Africa, Vodacom, Kyivstar and Telefonica Brasil as EM operators now approaching this threshold. Digital businesses typically command higher growth, superior ROIC and lower regulatory risk, supporting a valuation premium. Reflecting this view, New Street upgrades their price targets for VEON ($100), Kyivstar ($16.4), Vivo (R$43), AAF (GBP 380), Vodacom (ZAR 200), Safaricom (KES 32) and MTN (ZAR 245).

Edition: 223

- 31 October, 2025

Ready for the contrarian gold trade?

Cam Hui has been bullish on gold, but point-and-figure charts of gold and gold miners now show that they are either very near or have outrun their measured price objectives. Tactically, the contrarian trade would be to sell gold and buy bonds. However, a cycle analysis leads Cam to conclude that the market is undergoing a shift to a hard asset price leadership cycle. Cam’s base case calls for a multi-month correction and consolidation in the manner of the 2004–2006 experience, followed by a second rally to an ultimate top at much higher gold prices. It is within this context that a long-term point and figure objective of 9,800 is achievable in the next 3–5 years.

Edition: 223

- 31 October, 2025

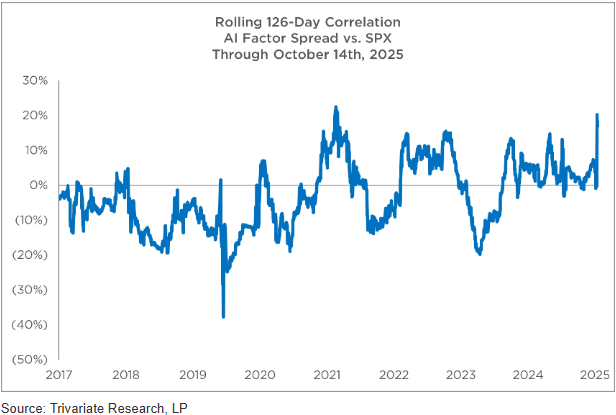

Blow-up avoidance guide - how are you dealing with the S&P500 being an AI factor bet?

While there are plenty of high-quality AI-exposed stocks to own, the challenge is that many non-Tech names have also become correlated to the AI trade. Trivariate screened for stocks with low correlation (<0.2) to their AI Semiconductors basket, that are up >10% in the past 6 months, top-half quality and beta <1 - identifying 28 stocks with a m/cap >$50bn. Given the recent huge moves in speculative names, Trivariate also advises preparing a sell/short list for a potential market rollover. They highlight 24 stocks ($1bn+ m/cap) that are up >100% in 6 months, in the most expensive EV/sales decile and the bottom half of their quality model, companies with high short interest and lower 2026 EPS estimates than at the start of the year, meaning the recent big moves in stock prices are despite a deteriorating nearer-term fundamental outlook.

Edition: 223

- 31 October, 2025

Financials

OWS’s short thesis continues to play out as growth slows and profitability erodes. Total Written Premium (TWP) growth is decelerating, converging toward a long-term low double-digit rate, while management’s talk of 40% growth within five years appears unrealistic. Agent growth has stalled (+3.8% Y/Y vs. +11.1% last quarter) and productivity per agent has essentially been flat for 3 straight quarters. Meanwhile, operating costs per agent continue to rise, leading to margin compression that management expects to persist into 2026. OWS argues that GSHD’s franchise-heavy model is becoming less attractive to experienced agents and increasingly reliant on costly recruitment of new ones, leaving valuation vulnerable to further downside. TP $52 (25% downside).

Edition: 223

- 31 October, 2025

Lifco (LIFCOB SS) Sweden

Industrials

Karl Redin (Subsidiary CEO) purchased 26,350 shares at SEK 381, spending €920k. This is his eighth purchase and over 10x what he has spent on prior buys; the most recent was in Jul at SEK 367. The purchase occurred on the same day as the stock rose sharply after reporting Q3 earnings. This is an unusual buy, into unusual strength. Martin Linder (Subsidiary Head) also recently purchased shares spending €190k - a large purchase for him. Smart Insider has had a positive rank on this stock since early last year, based on buying from Per Waldemarson (CEO), Anna Hallberg (Director) and Martin Linder (Senior Officer). The stock has moved higher and insider buying has continued. Waldemarson made his most significant purchase in Jul, spending €1.3m and then spent an additional €300k in Sep. This is now the fourth time Smart Insider has renewed their +1 rank since Apr 24.

Edition: 223

- 31 October, 2025

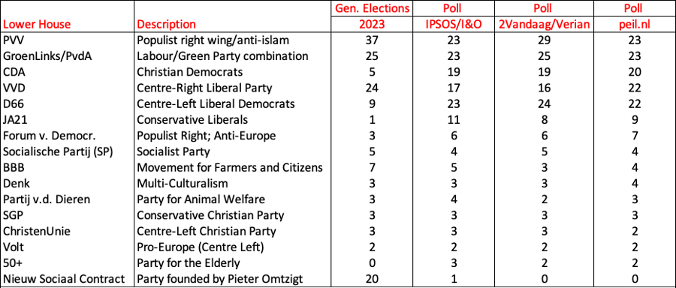

Holland: A close fight

Based on the latest three polls, the Dutch General Elections could end up in a close finish between the five largest political parties (see table). Although the TweeVandaag poll still puts PVV clearly in the lead, the other two polls show an accelerating loss of Geert Wilders’ Freedom Party, which has been banned as a potential coalition partner by most other parties. Maarten Verbeek notes that VVD appears to be the main beneficiary of the Freedom Party losing support, whereas the progress in the polls of D66 continues. Maarten reiterates his view that – based on the polls – the most logical new coalition would be one between GroenLinks/PvdA, D66, CDA and VVD. With the first three parties being left of the centre, this could mark a clear break with the policies of the outgoing cabinet. In view of the meaningful differences in the election programs of these four parties, a new coalition by Christmas would be quite the surprise.

Edition: 223

- 31 October, 2025

UK: Anatomy of a rolling fiscal crisis

Helen Thomas says that the totemic Caerphilly Senedd by-election loss for Labour coupled with the inevitable cost-free, protest-vote election of Lucy Powell for Deputy Leader could not have come at a worse moment for budget preparations and for PM Starmer. After the OBR delivers its final pre-measures forecast, Reeves will know what number is required to meet the fiscal rules. By Nov 10th, the OBR will deliver its initial post-measures forecast - essentially a judgement on whether Reeves's shopping list of measures will pass muster. If not, there will be more HMT/OBR back and forth until it does. Except the shifting political landscape means that this is no longer just an optimisation problem between two economic institutions. Helen says that for the embattled prime minister the situation looks terminal, and Starmer will be gone within months, as a result of challenge to his leadership by those in the Labour Party who now oppose him.

Edition: 223

- 31 October, 2025

Consumer Discretionary

A story riddled with risk - Brian McGough argues DKS is priced for perfection despite mounting structural and cyclical headwinds. Core growth is tapped out and the House of Sport concept – its only unit growth driver - is not working; comping down 20% in year 2 and down again in year 3. Inventory issues, including a Critical Audit Matter on carrying value, and gross margin risks from tariffs on private-label apparel add further pressure. Apparel (40% of sales) has turned deflationary and the Foot Locker merger is seen as immediately margin-destructive, with no strategic merits and likely to strengthen competitors such as Academy and JD Sports. Brian is incrementally of the view that the 5-year CAGR for athletic footwear in the US is -300bp below pandemic-era trends and warns that at 10x EBITDA, a historical peak, DKS is over-owned, over-earning and due for a correction.

Edition: 223

- 31 October, 2025

Saint-Gobain (SGO FP) France

Industrials

Following publication of its FY24 registration document, Iron Blue increases their SGO score to 27/60 (newly top quartile). This principally reflects FY24’s P&L benefit from compression in the expense for inventory and bad debtor impairment provisions, which could provide a tough comp effect in FY25. They also note two new contingent liabilities related to a new Grenfell Tower claim brought against SGO subsidiaries as well as assumed Australia asbestos liabilities with FY24’s CSR acquisition. For the first time the FY24 annual report quantified SGO’s reverse factoring activities (€106m). Iron Blue continues to flag sustained stripped out costs and an elevated gap between PPE capex and the P&L depreciation charge.

Edition: 223

- 31 October, 2025

BLS International (BLSIN IN) India

Industrials

While growth and margins appear strong, Iii’s forensic review of BLS International highlights concerns across the company’s financial reporting with alarm bells ringing especially when it comes to consolidation of accounts, unaudited subsidiaries and the tax stance of the Dubai subsidiary. They also flag an impairment in DSS Gulf Realtors that has surfaced on the balance sheet, in addition to irregularities in cash-flow statements and governance practices. Iii argues these findings highlight gaps in transparency and accounting discipline that investors should monitor closely when assessing the company’s reported results.

Edition: 223

- 31 October, 2025

Adyen (ADYEN NA) Netherlands

Technology

Strong net revenue growth and take rate, were both ahead of expectations for Q3. At constant currencies, net revenue growth amounted to 23%. This is the highest quarterly growth rate this year whilst expectations were that revenue growth would remain flattish in the remainder of the year. Its take rate showed a strong improvement as well, driven by the above average growth of Platforms (up 50.2% and increased take rate to 13.2 from 10.8). Another positive element of Adyen’s quarterly update is that FTE growth (9.0%) lagged net revenue growth again. This will result in a further improvement of its EBITDA margin. Investors can expect more clarity on growth targets at the company's upcoming Capital Markets Day, but based on current momentum and fundamentals, the IDEA! maintains that Adyen remains an attractive investment opportunity.

Edition: 223

- 31 October, 2025

Beneficiaries of US-Japan rare earths deal

Asymmetric Advisors highlights Furukawa and Tadano as potential beneficiaries of the US-Japan initiative to revive American mines, aimed at countering China’s resource dominance. Furukawa’s Rock Drill segment (17% of sales, ~30% of OP), derives over half its overseas sales from North America. The recent acquisition of EarthTechnica should more than double this segment’s sales from FY3/27. The Industrial Machinery division (11% of sales but >20% of OP), which includes belt conveyors used to transport mined materials, provides further exposure. Tadano with ~40% global share in Rough Terrain cranes and ~70% of its US demand tied to resources, also stands to gain. Europe remains its main drag and turning this around is a key factor in any share recovery. The stock trades at 0.78x PBR.

Edition: 223

- 31 October, 2025

Navitas stock surge masks growing execution crisis in AI power market

Technology

JNK Supply Chain Research reveals serious problems hiding beneath the surface as NVTS transitions chip production from TSMC to PSMC. The new factory has lower quality standards and worse yields. Critical 650V GaN devices won't reach mass production until late 2026 or early 2027. Competitor Infineon already ships 800V power solutions to AI data centres. NVTS remains in development while the market moves forward. Big customers like NVIDIA are diversifying suppliers instead of depending on NVTS. The company has few shipping products in hyperscale AI infrastructure. NVTS pioneered GaN technology with 250 million units shipped. But execution matters more than innovation when competitors deliver working products first. NVTS is one of 23 companies JNK tracks in the analog space. Click here for recent results.

Edition: 223

- 31 October, 2025

Materials

EM Spreads initiates coverage on Braskem with an Overweight recommendation. They believe the company’s large domestic footprint, political relevance and partial government ownership make a default event less likely near term, but the credit now hinges less on fundamentals and more on political and strategic decisions involving Petrobras, the federal government and Braskem’s ability to strengthen liquidity. They see asymmetric risk-reward at distressed prices, with outcomes contingent on a secured-liquidity bridge, PRESIQ approval, direct support measures and broader policy backing for Brazil’s petrochemical sector. They favour exposure to the lower-priced bonds within the curve for better downside protection and see greater value in the 2030s at $38.3, 32.1% YTM, 3.1-yr duration.

Edition: 223

- 31 October, 2025

Industrials

Sidoti lifts their target price by 45% following another record-breaking quarter for FIX. 3Q25 EPS and sales beat forecasts by 32% and 16%, respectively, as the company continues to steer its project mix towards the technology sector (mostly data centres). FCF hit $516m (177% of net income) while the order backlog rose 15% sequentially (all organic) and 65% Y/Y (62% organic) to $9.4bn. Expanding modular capacity remains a potential near-term catalyst, while beyond 2026, Sidoti views no shortage of end markets experiencing secular growth (e.g. reshoring, advanced manufacturing, chip plants), or other hyperscalers for that matter, that would like a greater chance to compete for FIX’s services, were current customers to decrease their expenditures. Sidoti now models 2025 EPS of $25.60 (from $22.91), 2026 EPS of $30.34 (from $26.50) and introduces 2027 EPS of $38.50.

Edition: 223

- 31 October, 2025

Consumer Discretionary

PLNT is well positioned in the growing high‑value‑low‑price gym segment with scale and ample runway for growth. New CEO Colleen Keating brings relevant hospitality franchise experience to drive the next phase of growth in the US and internationally. Gen Z is the fastest‑growing membership cohort for the company, supported by initiatives like the “High School Summer Pass”. PLNT continues to refine club formats and contractual terms to improve efficiency and unit economics. 2Xideas expects 2024-31E system‑wide sales CAGR of 11.7%, driven by 6.6% annual net unit growth and 5.0% same‑club sales growth. They forecast an 11.1% EBITDA CAGR and a 44.6% margin in 2031E. European expansion remains an upside not reflected in their forecasts. They see 17.2% annualised total returns based on an exit NTM P/E of 28.0x (17.7x EV/EBITDA).

Edition: 223

- 31 October, 2025

Consumer Discretionary

The Retail Tracker notes continued improvement in URBN’s product assortments, describing the current offering as focused, confident and well-positioned for the holidays with stronger gifting and better alignment to its customer. New leadership is credited with sharper merchandising and more responsive assortments visible across stores, online and social media. Anthropologie and Free People remain strong, attracting younger shoppers while maintaining core customers, with standout accessories, home and active lines. Nuuly, the rental platform, continues to expand rapidly, offering tariff resilience and appealing to younger, price-sensitive consumers. The Retail Tracker has been positive on the name since early in the year and remains so.

Edition: 223

- 31 October, 2025

Debt Risk Monitor

TT has launched their first Debt Risk Monitor, highlighting 53 companies across Europe and the Americas, that have been flagged by their proprietary tool as potential debt risks. Previously integrated within TT’s accounting risk framework, the new monitor flags firms where debt concerns exist regardless of whether they see any other accounting issues (i.e. earnings manipulation). The tool detects signs of hidden on- and off-balance-sheet debt, an approach that previously identified Steinhoff and NMC Health ahead of their collapses. Similar to the accounting risk score, the higher TT’s debt risk score, the more indication they have that companies have hidden debts. Clients can access the full monitor, covering 7,500+ listed companies, via TT’s website, alongside historical data, background reports and ongoing monthly updates.

Edition: 223

- 31 October, 2025

Communications

Paragon Intel takes a negative view on CEO Sundar Pichai, arguing that his slow, consensus-driven leadership style has left the company “fast following” in an AI race it should be leading. While Pichai’s long-term vision and product instincts built successes like Chrome and Android, and his tenure has delivered impressive financial results, his risk aversion, conflict aversion, reluctance to refresh senior leadership and indecisive response to competitive threats like ChatGPT have led to internal stagnation. Paragon’s analysis includes interviews with 6 former Alphabet executives, who portray him as a thoughtful strategist and capable steward, but ill-suited to the fast, “wartime” pace the AI era demands.

Edition: 223

- 31 October, 2025

Peru perks up

Exports and markets have really rallied on the back of rising volumes and buoyant prices. And now, Jonathan Anderson points out that the domestic economy is starting to perk up. By contrast, the weight of political turmoil and uncertainty had been killing activity at home - but the recent data now suggest a renewed pickup. “What to do?” asks Jonathan. On equities there's no doubt that external volume gains are coming through with the new port, and with some signs of life at home we see no reason to exit the market now despite strong gains this year. And as before, the combination of a strong external balance and positive real rates make local carry and yield attractive.

Edition: 223

- 31 October, 2025

AI: Solving a solved, unsolved problem

Richard Windsor has long held the view that existing AI models are incapable of reasoning and can only regurgitate. Recent news that OpenAI’s ChatGPT5 managed to find solutions to 10 Erdös problems and was making progress on 11 others immediately triggered great interest, suggesting a profound leap. The announcement was made, only for OpenAI to find out that all of the problems had in fact been solved, with GPT pulling from existing sources to “solve” the problems. It’s a gag that will soon be forgotten but is another example that reiterates Richard’s view that AGI is not on the cards any time soon. Humans have created a new tech whose usefulness may rival that of the internet in time, offering a lot of opportunity for value creation, but there will still be a correction ahead as many valuations remain far higher than fundamentals support.

Edition: 223

- 31 October, 2025

Germany: IFO Business Climate Index reflects optimistic tone

Germany’s IFO Business Climate Index rose to 88.4 in October, up from 87.7 in September and beating the consensus forecast of 87.8, reflecting a cautiously optimistic tone. John Fagan notes that the gain was primarily driven by the Expectations Index, which climbed to 91.6—its highest reading since February 2022. In contrast, the Current Economic Assessment Index edged down to 85.3, below both the prior month and the market forecast, underscoring the fragility of current conditions despite improving sentiment. Across sectors, the picture was mixed. Manufacturing optimism strengthened on expectations that the worst of the order-book contraction may be over. Services rebounded, buoyed by IT and tourism. Wholesale trade sentiment improved on less negative expectations, while the construction sector saw diverging signals: a modest uptick in current conditions offset by deepening pessimism over the forward outlook amid persistent order shortages.

Edition: 223

- 31 October, 2025

Healthcare

Leveraging purchase order data from 450 US facilities, MedMine is closely tracking the rollout of Pulse Field Ablation (PFA), the key driver of BSX’s Electrophysiology growth. The US ablation catheter market for AFib is estimated to be growing about 12% Y/Y. BSX has been growing faster in part due to mix shifting from lower-priced Cryo and RF products to its premium FARAPULSE PFA system. However, BSX is facing increasing competition with its PFA market share now at 80%, 10 percentage points lower than its peak. This raises a key question: will BSX’s next growth phase come from converting the larger RF market or expanding the total patient base estimated at 60m globally? MedMine’s near real-time data helps investors track these shifts in market share, pricing and technology adoption as they unfold.

Edition: 223

- 31 October, 2025

Beyond training LLMs

Technology

In the second report of their Data Centre / AI series, Kolytics examines how LLM scaling is shifting. Early AI gains came from brute-force scaling - models grew 2,000x since 2015 - but that trajectory now faces diminishing returns. They question whether bigger still means better, as performance gains from increased data, model size and compute begin to slow. A key focus is the changing split between training and inference and how this shift will reshape data centre demand. Kolytics sees this transition as a critical inflection point for both AI model development and infrastructure investment.

Edition: 223

- 31 October, 2025

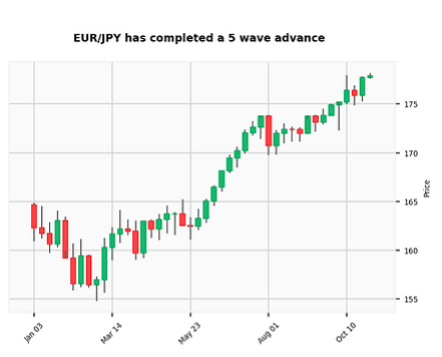

Sell EUR/JPY

David Woo points out that EUR/JPY is trading at its high as a result of domestic politics, with Takaichi being confirmed as PM in Japan, while Lecornu has managed to build a coalition with the socialists for now in France. It seems that EUR/JPY is pricing all this good news, and will struggle to go higher. EUR/JPY has completed a 5-wave advance over the past 9 months. David’s models suggest that this trend is now looking exhausted as JPY shorts are crowded. On the EUR side, Lecornu is coming under renewed pressure over the budget. The government may not collapse this week, but the market might start to price it. EUR may also come under pressure if the rare earth issue isn’t solved by Trump in a way that is friendly to German automakers. David sold the December EUR/JPY (RY) future at 177.56. He'll take profit on a move to 173, and stop out at 179.50.

Edition: 223

- 31 October, 2025

Financials

Abacus sees FIGR as a highly disruptive leader in real-world asset tokenisation - a theme they expect to define the next decade. The company has found a real-world use for blockchain, proving it can reduce the cost and time in HELOC origination by 90% (current 3% market share), with an average production cost per loan of just $730 vs. an industry average of $11,000. Beyond its low-cost origination engine, FIGR operates a marketplace for pooled credit, creating liquidity and transparency in traditionally illiquid markets. Abacus expects this model to scale into other asset classes, underpinned by ~30% operating margins and 80%+ incremental margins, with potential upside of 150% to $115.

Edition: 223

- 31 October, 2025

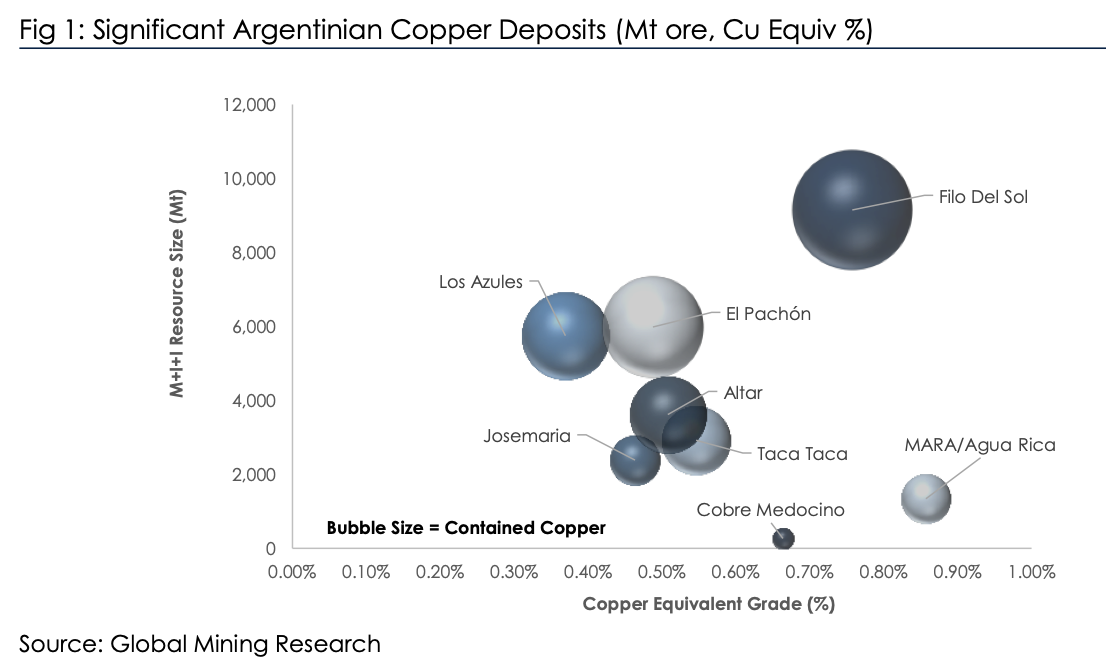

Is Argentina the next big thing?

Argentina has significant copper reserves yet produces no material copper (see chart). The new investment climate (RIGI) in Argentina, spearheaded by libertarian President Milei, is hoping to reverse this. Other volatile countries including DRC have achieved significant growth, so it’s possible. In his latest report, David Radclyffe examines the potential of Argentina copper. He sees potential for the nation to become a 1.0–1.5 Mt per year copper producer (top 10 globally), but comments on the aspirational timelines, with first copper unlikely on this side of 2029. Issues also cannot be discounted, with ESG concerns bubbling alongside a lack of infrastructure and skilled workers. David estimates the total capex at USD $40–50 billion. Lundin Mining has the most leveraged exposure to Argentina in partnership with BHP and is the preferred exposure. There are a few exploration plays, of which NGEx Minerals (non-rated) and its Lunahuasi discovery is the largest.

Edition: 222

- 17 October, 2025

US: A bubble in bubble fears

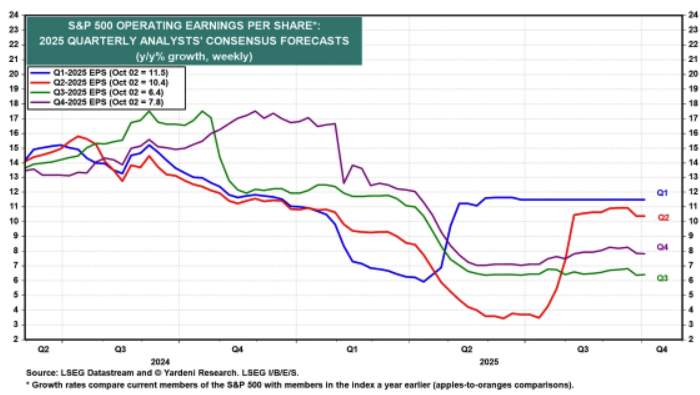

Ed Yardeni is raising his S&P500 year-end back to 7,000. He reckons that the V-shaped stock market rebound since April is discounting the economy’s resilience, which reduces the odds of a recession. Right now, we’re experiencing a slow-motion melt up, a result of the Fed rate cut in September and expectations of an additional one or two cuts before 2026 arrives. Ed sees the odds for a melt up at 30% and reduces the base-case for a sustainable bull market (without correction) at 50%. When the tech bubble emerged in the 90s there wasn’t as much chatter about the bubble, unlike this time; from a contrarian perspective, Ed sees this as comforting. He is counting on another better-than-expected quarter earnings season for Q3 to support the stock market’s rally to record highs. He expects a 10.7% increase compared to the 6.4% consensus (see chart).

Edition: 222

- 17 October, 2025

US: It’s not time to be bearish

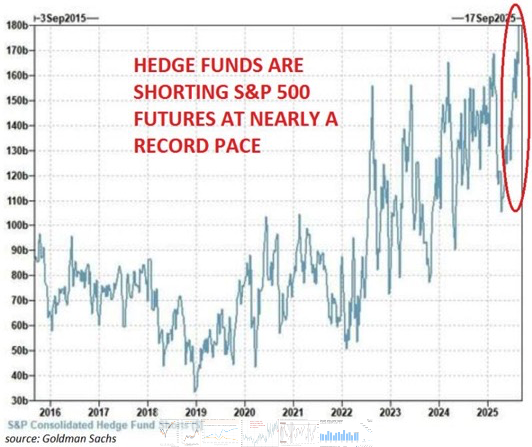

Forget the argument that this is a new dot.com bubble, argues Gaius King. The top 10 countries in the S&P500 are the ones delivering real growth whilst the remaining 490 and the broader economy are remarkably weak. Ironically, fund managers shorting this market is actually a contrarian indicator. There is little or no seasonality this year, and recall that asset and fund managers remain seriously under invested since the Tariff Tantrum. Actively shorting this market (see chart) in such a low volatility environment is hopium that they will match the index if the market falls. Gaius expects an additional year of market craziness ahead of us, peaking in Q3/2026, and draws remarkable parallels to the 1970s. Investors should buy momentum stocks. If you want a market canary, look at AI’s forward order book.

Edition: 222

- 17 October, 2025

Make European Equities Great Again

Earlier in the year, Callum Thomas told investors that he saw several factors lining up for MEEGA (Make European Equities Great Again); still cheap valuations, lingering excess pessimism, monetary tailwinds, political drift to the business-friendly governments, fiscal stimulus, and the prospect of global growth reacceleration into 2026. Callum’s chart this week shows a breakout to new all-time highs, which he remarks only took 25 years! Callum has recently documented several other big breakouts currently underway, including DM ex-US equities, EM equal-weighted index and China tech stocks, and he says the European one has good company. When there’s a clean, clear breakout like this after such a prolonged period of base-building, you better pay attention.

Edition: 222

- 17 October, 2025

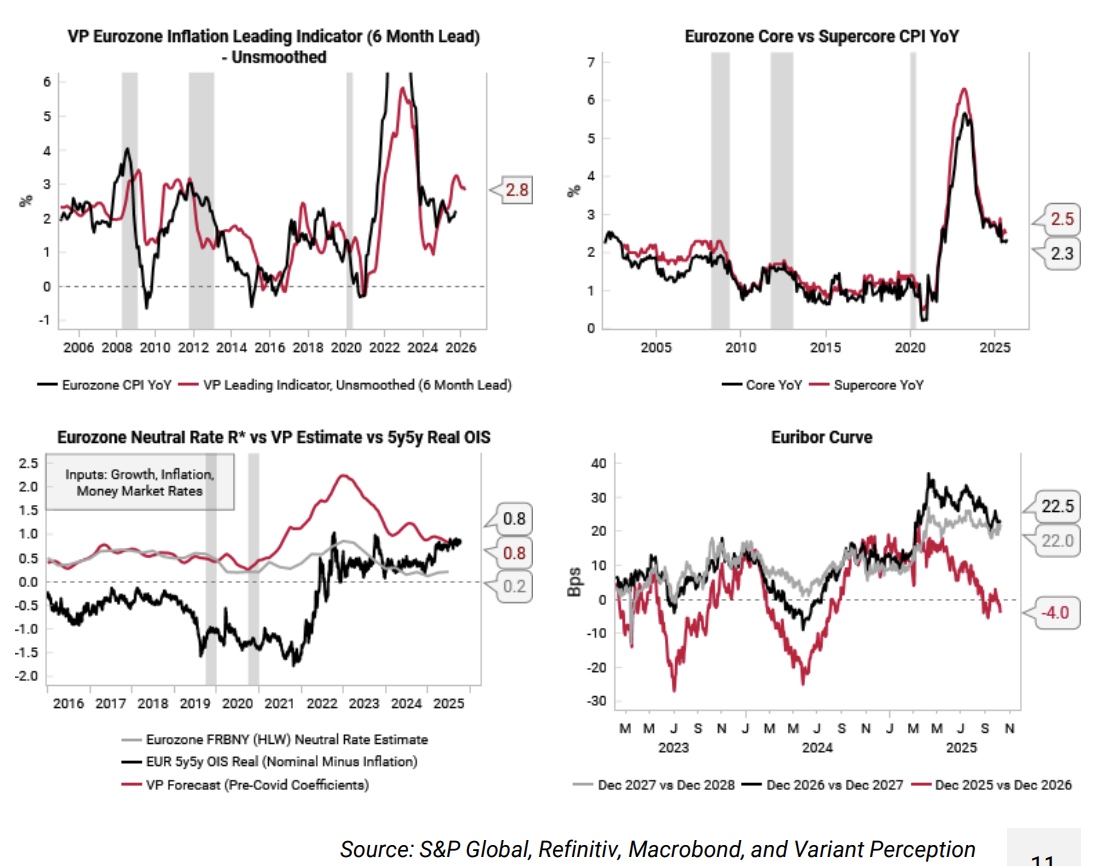

Eurozone: Consensus too optimistic on disinflation

Consensus expectations see 2026 eurozone headline CPI at 1.8% and core CPI at 2%. The Variant Perception team suspects that inflation risks are tilted to the upside from here given the recovery in their eurozone growth leading indicators and the ECB rate cuts so far this year. Their main inflation leading indicator is rolling over from a high level, but the point estimate remains elevated at 2.8% (top left chart). Core and supercore CPI have also been slower to fall, still at 2.3 to 2.5% YoY (top right). The team put the real neutral rate (R*) for the eurozone at 0.8%, which is also where the 5y5y EUR real OIS is trading (bottom left). With headline CPI at 2%, there is good chance that ECB policy is already stimulatory, potentially creating inflation upside in 2026. The team take profits on their SOFR vs Euribor Dec 25/26 convergence trade established last month.

Edition: 222

- 17 October, 2025

France: Survival

French Prime Minister Sébastien Lecornu survived two motions of censure on Thursday in the French National Assembly. The oppositional far-right Rassemblement National (RN) and the far-left France Insoumise (FI) were 18 votes short of toppling Lecornu. Parliament will now negotiate the 2026 budget, which it will vote on in December, and Macron can sigh a breath of relief. These negotiations could still fall apart, with the centre-left Parti Socialiste (PS) likely to threaten that it will walk away from a budget deal. That said, Niall Ferguson’s base case is that the various centrist parties that backed Lecornu today will reach a budgetary compromise resulting in a deficit of around 5% of GDP. The rise of French sovereign bond yields is over… for now.

Edition: 222

- 17 October, 2025

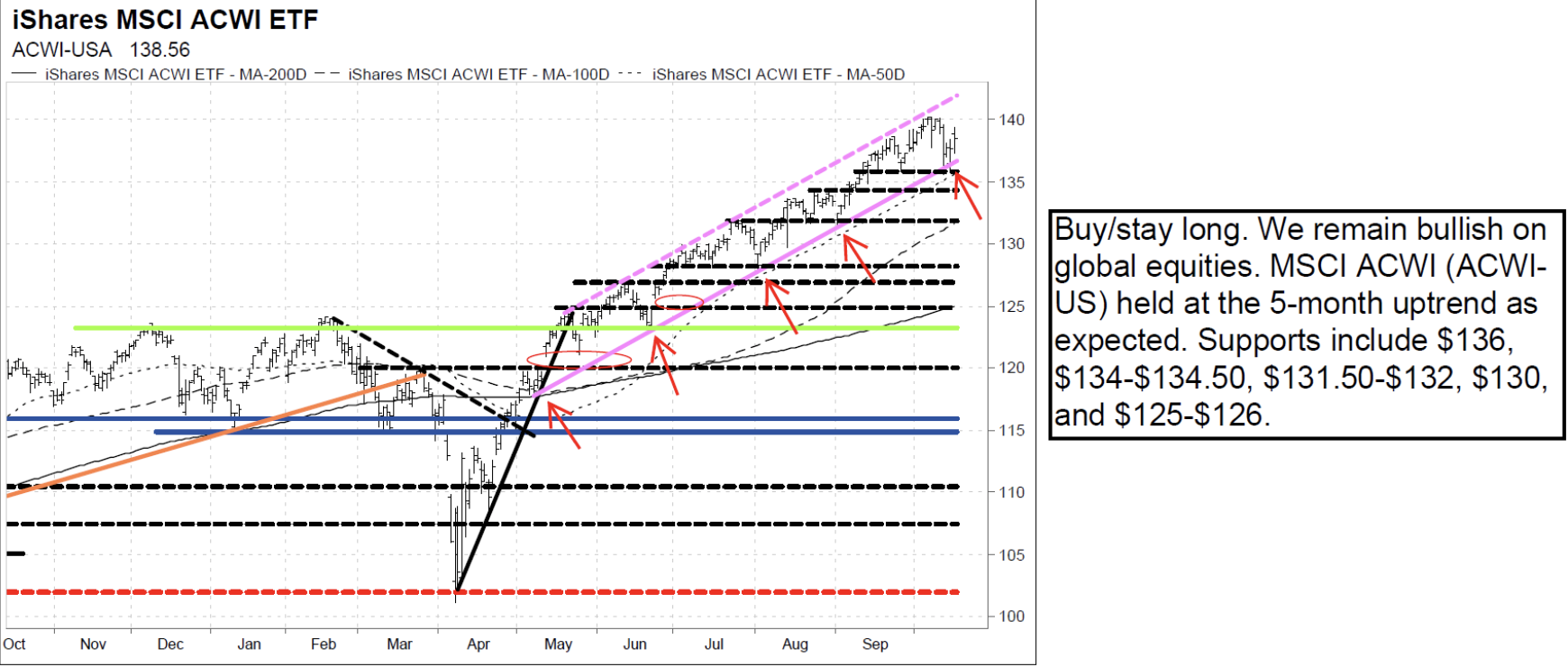

Global bulls

The Vermilion team remain near-term bullish since their April report, with their intermediate-term outlook also remaining bullish. They will maintain this view for as long as market dynamics remain healthy and the SPX and ACWI-US are above 6028-6059 and $125-$126. Their bullish near-term outlook will remain in place as long as the 5+ month uptrend continues on ACWI-US. So far, the latest pullback is testing the uptrend -- buy/stay long. Short-term supports to watch on ACWI-US include the 5+ month uptrend (currently at $136), $134-$134.50, $131.50-$132, $130, $128, and $125-$126. Expect more upside into year-end and early 2026. Remain overweight Taiwan, China, Korea and the US, and bullish on EM particularly MSCI EM Tech and Materials.

Edition: 222

- 17 October, 2025

A compelling growth story

AIR highlights Spain as the Eurozone’s standout growth opportunity, further supported by US immigration tightening redirecting talent and labour. The country is benefitting from its strong position in the EU’s €750bn Next Generation EU program, minimal exposure to US tariffs and insulation from Chinese industrial competition. A rapid transition to renewables has driven a 40% decline in wholesale electricity prices over five years, while lower structural taxes and spending continue to support competitiveness. Preferred sector calls include Infrastructure (Acciona, Ferrovial, Sacyr) with robust project pipelines supported by public and private investment; Banking & Insurance (CaixaBank) benefitting from SME exposure and high household savings rates; Real Estate (Merlin, Metrovacesa) poised for catch-up gains vs. other European countries amid supply constraints; and Defence, where Indra Sistemas is well positioned for M&A.

Edition: 222

- 17 October, 2025

Technology

Asymmetric Advisors has turned bearish on Fujikura, having recently closed their long position after what they call a “crazy rerating”. They were “beating the drum” when the stock traded around 15x earnings, but it now sits near 30x FY27, a level they see as unjustified for what remains a largely commodity cable supplier. While earnings surged in recent years on strong demand for its Spider Web Ribbon fibre cables used in AI data centres, capacity constraints and intensifying competition from Corning to Ciena to Furukawa and Sumitomo Electric are likely to cap further upside. Asymmetric now views Fujikura as a suitable short hedge against more attractive technology names in their portfolio.

Edition: 222

- 17 October, 2025

How the Gulf is saving Pakistan

Foreign remittances from the Gulf are still exploding upwards, as Saudi, UAE and other GCC states continue to borrow and spend at a rapid pace, employing overseas workers in the process. Jonathan Anderson points out that remittances now overwhelm exports and official financing as the single biggest source of dollar income in Pakistan. The inflow has kept the current account in balance and the rupee stable, leading to equity gains too. It’s also pushing dollar sovereign spreads lower still. Jonathan had already exited his dollar bond position last year and had been cautious on further equity upside, but he has to admit that markets look more attractive today. Without remittances, Pakistan has a moribund export economy, much wider fiscal imbalances, an unworkably rising debt load and no exit strategy, but as long as Gulf earnings are flooding in it's difficult to be short this story.

Edition: 222

- 17 October, 2025

China: From trade war to tech war

Don Ma has distilled the latest US-China escalations into actionable insights. The shift from trade to tech war amplifies trends like self-reliance and friend-shoring, reinforcing long-term investment themes rather than disrupting them. In the short term, rising risks in market sentiment, supply chains, countermeasures, and geopolitics could trigger a 10%+ adjustment, eroding momentum strategies. Rare earth disruptions pose real threats to global tech production. Over the medium-term, expect supply chain redundancy builds, accelerated Chinese outbound manufacturing, and stronger domestic substitution. Trump's negotiation leverage may weaken due to legislative roots, prolonging tensions. Over a longer horizon, systemic distrust will entrench friend-shore/near-shore economies, benefiting ASEAN hubs and amplifying US’s structural inflation vs China’s deflation. Hedge with long gold/short crude. Compared to prior rounds, the recent conflicts are more strategic and entrenched, with lower compromise odds mid-term but enhanced supply chain rebuilding long-term.

Edition: 222

- 17 October, 2025