No matches for this search

Try adjusting your filters or search criteria

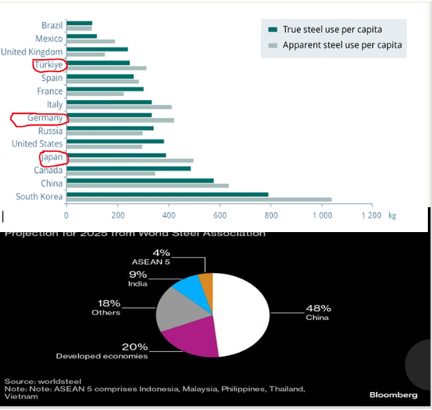

Iron ore: China’s urbanisation supercycle is over

James Burdass notes that China’s National Bureau of Statistics has reported a production of 960.81 million tonnes of steel last year, 4.4% less than in 2024. This may not appear significant, but is in fact an important data point that every commodities investor needs to be aware of. In his presentation a year ago "The New World Order and Commodities", James showed just how far China's apparent steel use per capita could fall. He suggested at the time a fall of at least 200 million tonnes from the peak – the trend is definitely on the way towards that. Falling materially below 1 billion tonnes for the first time since 2018 is the official obituary for the "Urbanisation Supercycle." It signals to every Iron Ore investor (Rio Tinto, BHP, Vale) that the volume cap is in place. This has the potential to be a headwind for the global steel sector for years to come.

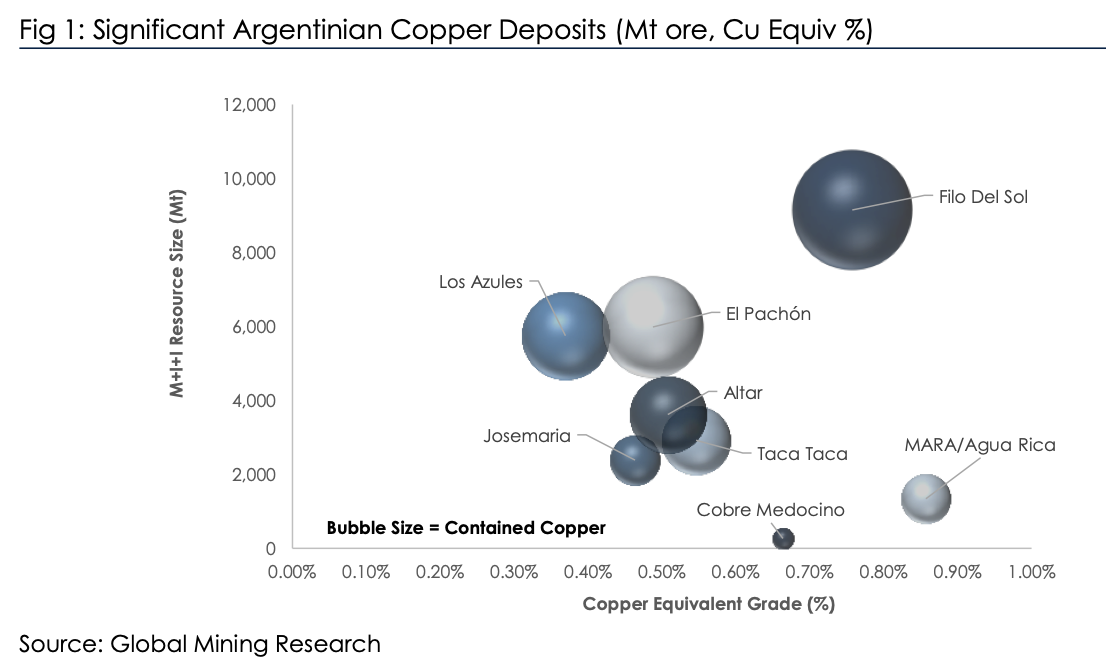

Is Argentina the next big thing?

Argentina has significant copper reserves yet produces no material copper (see chart). The new investment climate (RIGI) in Argentina, spearheaded by libertarian President Milei, is hoping to reverse this. Other volatile countries including DRC have achieved significant growth, so it’s possible. In his latest report, David Radclyffe examines the potential of Argentina copper. He sees potential for the nation to become a 1.0–1.5 Mt per year copper producer (top 10 globally), but comments on the aspirational timelines, with first copper unlikely on this side of 2029. Issues also cannot be discounted, with ESG concerns bubbling alongside a lack of infrastructure and skilled workers. David estimates the total capex at USD $40–50 billion.

Lundin Mining has the most leveraged exposure to Argentina in partnership with BHP and is the preferred exposure. There are a few exploration plays, of which NGEx Minerals (non-rated) and its Lunahuasi discovery is the largest.

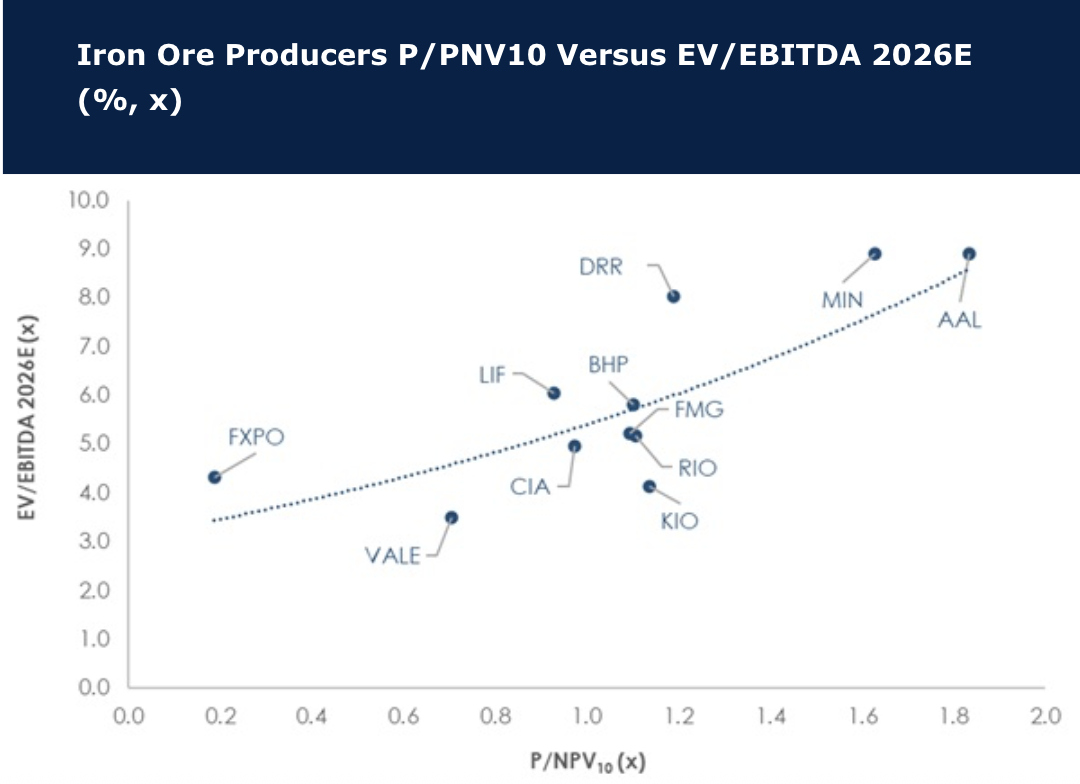

Iron ore is too big to ignore, but headwinds prevail

Iron ore seaborne supply is increasing at a time when steel demand is ailing, and David Radclyffe points out that this rightly makes investors nervous. However, the spot iron ore price has proven to be quite resilient this year at ~US$100/t. The headwinds may have dissuaded some investors, but at $378bn the iron ore market is simply too big to ignore in mining. As demand rolls the cost curve is key to sustaining volumes, and David assesses the LT price at US$95/t (US$101/t). Iron ore pure plays and diversified miners trade at 1.1x P/NPV10, and a prospective next two years average EV/EBITDA of ~5.8x and dividend yield of ~4.4%. Relative to other sectors this is reasonable, but high compared to historic levels. In the diversified iron ore-rich miners David prefers buy-rated BHP, then Vale, while in the pure plays it is Labrador Iron Ore Royalty. Overall, he remains underweight iron ore, with sells on key pure plays. Herein, Champion Iron is upgraded from sell to hold.

Super Copper

Craig Ferguson points out that US tariffs uncertainty remains with 50% tariffs on copper imports spiking the metal to new all-time highs. He expects a supply deficit from next year, one that will last for years as electrification and the transition to renewables unfolds. Countries like the US will now build copper strategic reserves, so Craig would not fade this price spike. This may be the start of a major run higher in the commodity and inflation cycle with copper (and gold, uranium and platinum) already leading the way. This may suggest a new super cycle in commodities has begun. This would suggest a super cycle in big ASX miners and the AUD also has begun (be OW both). However, it also is inflationary and would complicate things for global central banks, bond yields and stock markets. Craig is surprised that both BHP and the AUD are not higher as both should be on this news.

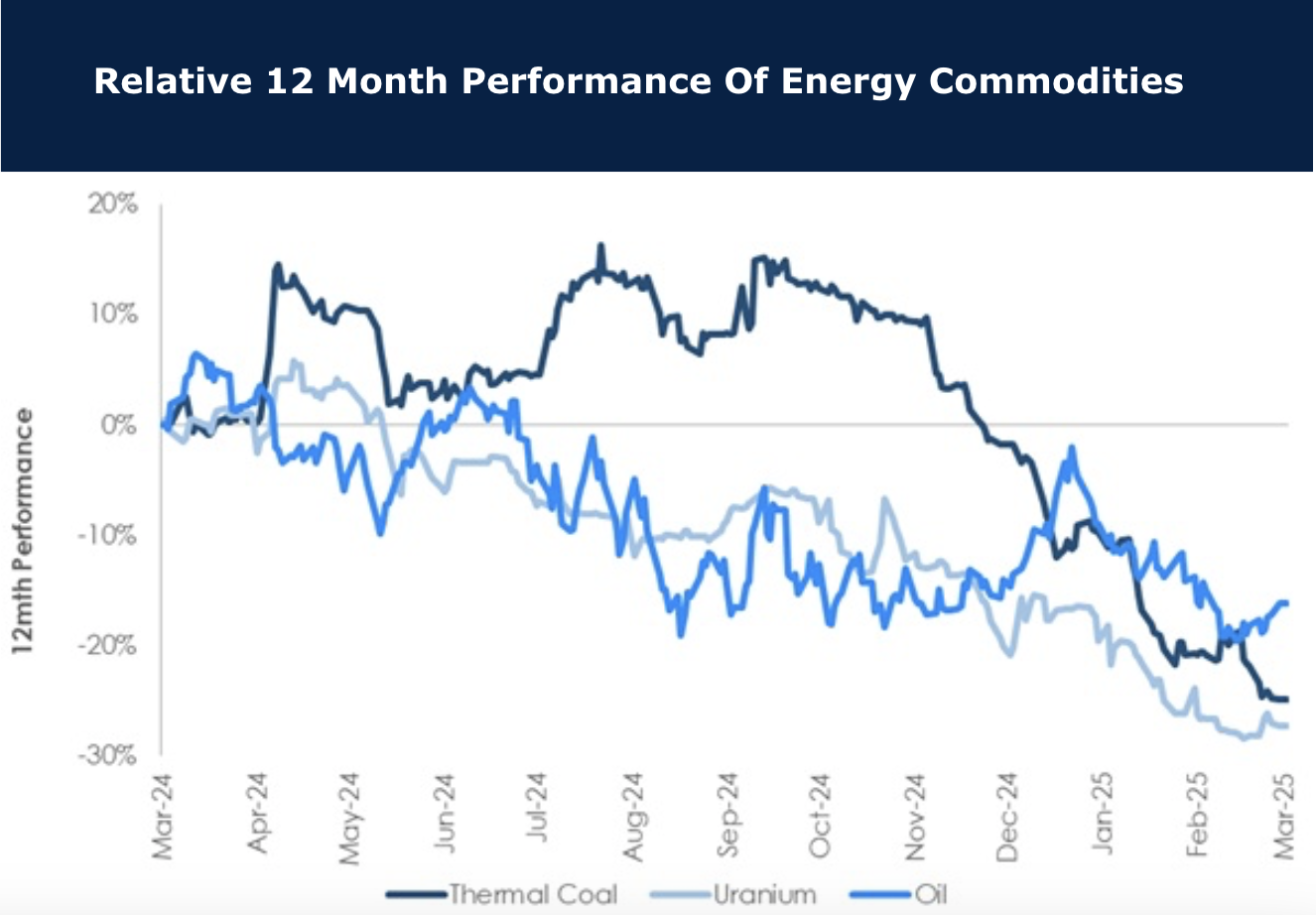

Thermal lost its spark

One of the worst performing commodities of 2025, thermal coal has been a drag on the coal miners. The reason is largely down to China and Australia’s strong production. Of course, there is a wider overlay of tariff concerns, recession fears and Deepseek disrupting the AI market. The chart shows how thermal weakness is not isolated, and has actually lagged the decline in both oil and uranium prices. Some coal producers are feeling the pain, although some producers have seen stronger share prices relative to the underlying thermal and met coal prices--they’ll need this strength going forward. The potential silver lining is that lower energy prices are deflationary, which can support remote miners reliant on diesel power generation. It’s bad news for the diversified miners producing coal such as Anglo American, BHP Group and Glencore, and also the pure play coal miners, but good news for much of the mining sector.

Is the diversified model dead?

Materials

GMR recently published a review of the leading mining stocks’ performance over the last five years. For the diversified miners this highlighted weak TSR and overall negative returns stripping out cash payouts. A critical issue facing the group, especially the iron ore-dominated miners, is how to restructure their portfolios for the long-term. GMR reviews six key questions: 1) Is the diversified model dead? 2) Can dividends be sustained? 3) Miners exited coal but should it have been iron ore? 4) Shrinking to greatness might have merit? 5) How to increase EV materials exposure & in which commodity? 6) Is M&A the answer? BHP is their preferred pick, with Glencore second. Vale is very cheap, but it is hard to see a catalyst.

Materials

With the Golden Age, when copious amounts of cash was returned to shareholders, now a distant memory, GMR examines where the diversified miners are, in terms of existing and prospective valuations, free cash flows, as well as exposure to preferred commodities. Averages are EV/EBITDA 5.2x, FCF Yield 7.2% and Dividend Yield 4.8% for 2025 on GMR forecasts (iron ore US$115/t, copper US$4.20/lb), with P/NPV10 a reasonable 1.0x. Cash + capex costs range from US$2.49/lb for BHP to US$3.89/lb for South32, on a copper equivalent basis. GLEN is upgraded to Buy, offering reasonable value with good FCF, with AAL reduced to Sell following share price run to £24.

Materials

In this 14-page report, GMR examines the potential BHP takeover of AAL. BHP would need to take a long-term view as AAL comes with ~US$11bn net debt and midterm FCF is very weak, plus uncertainty in several of its businesses including DeBeers. Fundamentally, GMR fails to see the material value opportunity for BHP in what appears to be a dilutionary transaction. How is this different from the large deals of the past which struggled to add value?

Materials

On several metrics Rio Tinto now looks more attractive than BHP, but the difference is not that marked and partly explained by BHP’s large market cap. P/E, P/CF, EV/EBITDA, FCF yields and dividend yields are somewhat similar. For the coming year which one outperforms may be as simple as aluminium vs. met coal price moves, with copper favouring BHP. However, information flow in 2024 possibly favours RIO with good news from Oyu Tolgoi. With a positive outlook for copper and met coal, GMR prefers BHP for 2024 (upgrades to Buy; TP A$52). This is a non-consensus call with most preferring RIO. For best value and yield they prefer Vale.

Materials

OZL rebuffs BHP's A$25/share cash offer - goal is now to try and extract a higher bid, but with limits as it is not a “must have” for BHP (11% more copper, but not worth the effort from an EBITDA perspective; main appeal is safe jurisdiction with assets near one of BHP’s key mines). OZL’s Carajas projects would likely be sold, but West Musgrave is an interesting potential growth asset. The offer price is equivalent of US$0.26/lb of OZL’s contained copper in resources, which is on the lower side to recent deals. For 2023, GMR estimates the combined copper assets would have a sales revenue of ~US$3.6bn, EBITDA ~US$1.4bn, copper production ~340kt and an AISC ~US$2.20/lb.

Diversified miners becoming less diversified

The three leading diversifieds have worked hard in un-diversifying themselves in recent years, becoming more and more iron ore focused, with fewer points of differentiation. David Radclyffe finds that nearly all investment ratios favour Vale

(FCF yield 15%, EV/EBITDA 2.6x), then Rio Tinto

and finally BHP Billiton. For as long as iron ore can hold around US$100/t, expect average cash return yields of 8-12% in 2022E. BUY Vale with a target price of $15.40.

Materials

Pass-the-parcel - you can only give so much away before there’s little left to unwrap. Divesting the Petroleum business leaves BHP with little to differentiate it from Rio Tinto and Vale. BHP should have used its petroleum expertise and customer base to build a hydrogen / ammonia business taking a leaf from Fortescue’s playbook. From a ROCE and CO2-e perspective the met coal business would have a greater overall impact on the business if it were divested. However, the problem appears to be a lack of interested buyers.