Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Shell: To Be(P) or not to Be(P); that’s the question

Energy

Analysts at the IDEA! weigh in on media speculation about a potential Shell acquisition of BP. While Shell has the financial strength to pursue a deal, acquiring BP would involve taking on its $77bn of debt and other long-term liabilities, including those from the Deepwater Horizon spill. Although synergies are possible, integration would be costly and could disrupt Shell’s shareholder returns, which is key to closing its valuation gap with US peers. The deal would also bring in non-core assets and regions Shell has been moving away from, along with notable cultural differences. the IDEA! suggests caution and favours Shell sticking to its current strategy or exploring other deals instead.

Edition: 211

- 16 May, 2025

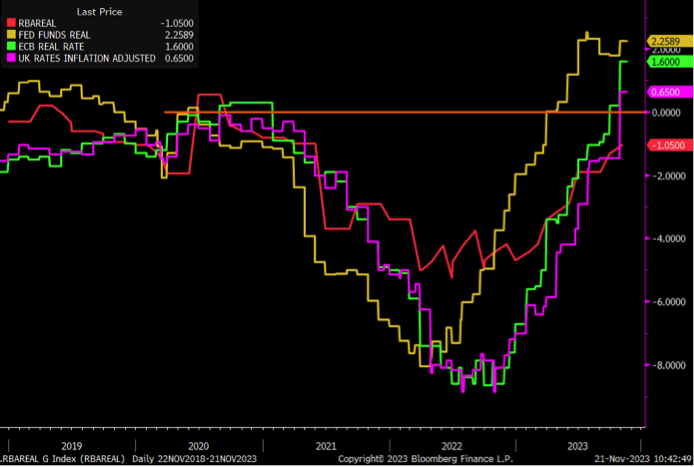

Australia: Why isn’t the cash rate moving?

One of these lines is not like the others, says James Aitken. Whereas Fed funds rate is at ~2.25%, ECB depo rate at ~1.6% and BoE bank rate at 65 bp, the real RBA cash rate is still around minus 1. This is amidst a high-pressure economy that is facing a surge in migration, an undersupplied housing market, rising input costs and record super benefits being paid out. Monetary policy is way too loose. The good news is the fairly new RBA Governor Michelle Bullock isn’t mucking around, making her hawkish stance clear. Yet peak RBA cash rates have not moved. It’s quite odd. James has said again and again the RBA cash rate is closer to or even above 5%, and now he says it again but with more conviction than ever.

Edition: 174

- 24 November, 2023

China: Balance sheet impairments plague property

The current official and market consensus view on China is that macro weakness is a function of inadequate demand. William Hess disagrees, believing that this mistakes outcomes for underlying causes. The latter are a function of ongoing balance sheet repair in large segments of the economy. He continues to expect Beijing to introduce more easing measures in Q2, including steps to lower debt burdens for households and local governments in the form of 15 bp cuts to 5-year LPR in both May and August. However, this alone will not resolve systemic balance sheet problems, and until policymakers address them, the effectiveness of conventional demand side policy measures will remain subdued.

Edition: 161

- 26 May, 2023

A core portfolio holding

James Aitken continues to believe that oil and gas should be a core portfolio holding. He remains LONG Hess and BP, and recommends that investors remain long, too. The recent (past three months) inelasticity of major oil and gas stocks to declining oil prices may be a hint that new (fed up with ESG) buyers are coming into these well-run, cash-flow vomiting businesses.

Edition: 152

- 20 January, 2023

This isn’t demand destruction, it’s demand construction!

The transitory inflation crew want you to believe demand destruction will soon restore commodity prices to normal levels, yet every so-called government solution involves subsidising demand! James Aitken reiterates how the largest commodities demand construction event is the climate transition currently underway. In fact, as important as the recent repricing of bonds has been, commodities are the world’s new risk-free curve, and everything is priced off them. Recommended related trades include LONG AUD, which will benefit as the world turns to Australia as a trusted commodity supplier, and staying LONG BP and Hess Corporation.

Edition: 132

- 01 April, 2022