Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Technology

BTN continues to see several areas where OSIS's results may be unsustainable. The company has reduced its bad debt reserve to just 2% of receivables (vs. a 5-7% historical range), adding ~11 cents to Q4 EPS (OSIS only beat Street estimates by 5 cents). The current reserve for bad debts is at least 200 bps too low; if OSIS had to raise it by 100 bps, it would be a 39-cent headwind for EPS. DSOs have surged to 151 days (historically ~90), making Q4's revenue increase more suspect and the $372m forecast for 1Q26 tougher to reach. Warranty expense was cut again (added 3.7 cents to EPS), while OSIS continues to let its PP&E age and is using fully depreciated equipment - saving 29 cents in EPS last year. Finally, FCF remains weak (negative in 5 of the last 8 quarters).

Edition: 222

- 17 October, 2025

Technology

While CDNS appears to be handily beating both sales and earnings estimates, BTN’s analysis shows it is being driven by increasingly aggressive revenue recognition. Recurring revenue growth slowed to 6.5% Y/Y in 2Q25 (vs. mid-teens previously), while upfront revenue has surged >100% Y/Y in the last 3 quarters. BTN cautions comps will toughen significantly in Q4 and even modest declines in upfront revenue would see CDNS lose its EPS beats. Unbilled receivables have doubled in the last 8 quarters and long-term receivables doubled in Q2. Deferred revenue days of sales has also dropped Y/Y for 4 consecutive quarters. Additional red flags include lower bad-debt reserves and an EPS boost from higher stock comp. At >50x forward adjusted EPS, there is little margin for error before the stock price could face pressure.

Edition: 218

- 22 August, 2025

Healthcare

BTN flags deteriorating financial quality despite headline beats. Receivables have surged, with DSOs breaking past 100 days (106.4 in Q2) - up 5 days sequentially and 20 days Y/Y. Sales growth previously stalled when DSOs hit 92. 1 DSO equals ~$12.7m in revenue and every 2-day increase adds ~1¢ in adjusted EPS. Despite a $51m YTD revenue beat, DXCM only raised FY25 guidance by $25m and cut its gross margin outlook from 64-65% to 62%. Operating margin guidance of 21% also looks aggressive (Q1: 13.8%, Q2: 19.2%). Finished goods inventory remains low at 25.8 days and DPOs have been stretched by 30 days over 2 years. While EPS is benefitting from buybacks, BTN questions if cash flow can sustain them.

Edition: 217

- 08 August, 2025

Technology

IOT trades at 100x forward EPS despite being a mature company with limited history of profitability. The firm continues to rely on low-quality sources of EPS growth to drive earnings beats. In Q1, cash R&D and S&M cuts alone added 6.1 cents to EPS, while stock compensation still exceeds 100% of adjusted EPS and cash flow. Deferred Revenue and Remaining Performance Obligations are growing more slowly than sales and both DSOs are dropping (drawing down DSOs by only 1 day is worth $4m in sales and 0.5 cents in adjusted EPS). With fundamentals increasingly out of sync with valuation, BTN believes even modest signs of slowing growth could trigger significant multiple compression.

Edition: 214

- 27 June, 2025

Healthcare

BTN raises concerns about DGX's reliance on acquisitions for growth, questioning its sustainability given rising debt (3.0x EBITDA) and acquisition spending that regularly exceeds FCF post-dividends and buybacks. They also highlight earnings quality issues: over half of Q1’s EPS beat came from an unexpectedly low tax rate; receivables are rising without a corresponding increase in bad debt allowance; and more than $2.00 per share in acquisition-related expenses are not being recognised, which is over 20% of the company’s expected 2025 non-GAAP EPS forecast.

Edition: 212

- 30 May, 2025

Healthcare

BTN’s analysis of DOCS’s earnings quality identified several accounting-related factors that have recently boosted growth but appear to be temporary: 1) The boost to sales growth from falling Deferred Revenue may be difficult to maintain. 2) Rising Receivables are helping sales too. With DSOs at historic highs, this growth may be tough to continue. 3) Even with rising revenue, DOCS is still boosting stock compensation as a % of sales which it adds back to non-GAAP EPS. 4) Cash R&D and selling expenses are down as a % of sales and largely flat in dollar terms. 5) Passive interest income added 2 cents last quarter to Y/Y EPS growth. 6) Hefty share repurchases have lapped and taken away this source of 1-2 cents of EPS growth.

Edition: 209

- 18 April, 2025

Technology

In addition to the last two quarters benefitting from a lower tax rate, BTN’s earnings quality review identifies several other factors worth noting: 1) Concerning movements in receivables and contract assets. 2) Non-GAAP income far exceeds FCF. 3) Allowance for bad debts has fallen to under 3% of receivables from as high as 8% despite higher international sales (this added 12 cps to 2Q25 earnings that beat by only 8 cps). 4) Warranty accruals have fallen from 6.6 days of sale to 2.5 days since 2021. Returning the accrual to 5 days would be a 52-cps headwind over several quarters. 5) Unsustainably low depreciation from using older equipment. 6) An unusual auditor change.

Edition: 206

- 07 March, 2025

Fully depreciated equipment in the Building Products industry

Industrials

Among the 19 companies analysed by BTN, those with the biggest risk of overstated earnings from using fully depreciated equipment or unusually long depreciation lives compared to the industry include Allegion, A.O. Smith, Insteel Industries, Trane Technologies and Masco. Meanwhile, they see Simpson Manufacturing, Advanced Drainage Systems, AAON, Trex and Builders FirstSource as being positioned to start seeing lower depreciation expense and capital spending. These companies are already years into modernisation and expanding their equipment bases. Their depreciation has risen and been a headwind to earnings of late, but they may be about to see this level off and put them in a position of rising margins and FCF.

Edition: 202

- 10 January, 2025

Consumer Staples

KO’s guidance looks like a stealth cut - coming into the year, the group guided to $2.80-$2.82 EPS for 2024, up 4%-5% from $2.69 in 2023. So far, KO has beaten forecasts by 2 cents, 3 cents and 2 cents YTD, but guidance is only up to $2.82-$2.85. BTN believes investors should be concerned about the following items: 1) A wide spread in pricing between what KO is taking in Latin America and North America vs. PepsiCo, who has seen pricing growth become much more muted. 2) The tax issues on transfer pricing are getting worse. 3) At the same time KO just paid $6.0bn to the IRS, payables and accrued expenses keep rising and BTN cannot find much explanation for it.

Edition: 199

- 15 November, 2024

Healthcare

Following DXCM’s 3Q24 results, BTN flags several areas of concern: 1) Receivables remain very high - it looks like channel stuffing could have pulled some Q4 sales into Q3. DXCM’s revenue forecast will be tough to achieve if receivable growth does not continue in Q4. 2) Deferred revenues are unlikely to help this quarter - having already dropped significantly, if anything, it is likely be a headwind. 3) Rebates remain elevated. 4) Inventory looks too high. 5) Cutting warranties as a source of EPS appears played out - the company’s warranty reserve has been more than cut in half on a days of sales basis in the last few quarters.

Edition: 198

- 01 November, 2024

Technology

The stock features in BTN’s 3Q24 Focus Risk List which contains companies they believe have a higher risk of reporting an earnings disappointment based on earnings quality. ARW is guiding to its lowest quarter in years on adj. EPS of $2.10-$2.30 along with flat sales. BTN sees considerable risks for sales, earnings and cash flow. ARW’s adj. EPS beat of 62 cents last quarter had considerable help from one-time items. It picked up 29 cents by reversing bad debt reserves, another 2 cents from bad debt issues, 7 cents from falling depreciation, 12 cents from interest expense coming in below forecasts and 8 cents from interest rate swaps. This looks like a simple story of some unsustainable earnings drivers.

Edition: 196

- 04 October, 2024

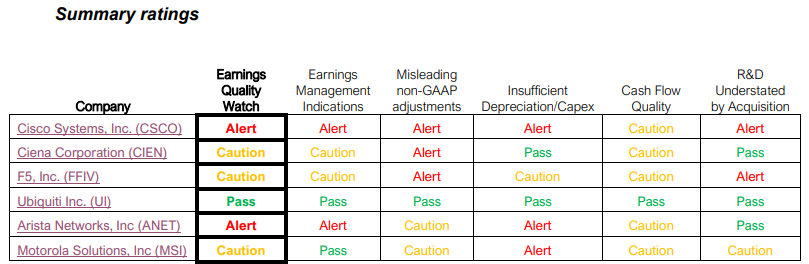

Communications Equipment: Earnings quality review

Communications

BTN’s Earnings Quality Watch industry reports provide readers with a quick way to identify the companies that are the most and least exposed to the risk of reporting disappointing results or guidance due to recent results being distorted by unrealistic, accounting-related benefits. Looking at the table above, only Ubiquiti received a ‘Pass’ rating in the Communications Equipment industry, while BTN sees meaningful risk that Arista Networks and Cisco Systems will disappoint on earnings in the next 2 quarters.

Edition: 190

- 12 July, 2024

Consumer Discretionary

MHK reported non-GAAP EPS of $1.86 in 1Q24 which was 18 cps ahead of the consensus estimate. Revenue was a slight beat. However, as is often the case with this company, there were two one-time accounting-related benefits that BTN believes accounted for almost all the earnings beat - lower allowance for bad debt could have added as much as 12 cps and a decline in warranty accrual relative to sales could have added as much as 5 cps. Both items have been benefitting results for multiple quarters and BTN expects them to shift to becoming earnings headwinds.

Edition: 187

- 31 May, 2024

Healthcare

BTN lowers their earnings quality rating for TEVA to 1- (Strong Concern) - the company gave its lowest FCF guidance in years as it had already stretched payables by 29 days last year ($630m), pulled in more from sold A/R ($378m) and will need to start paying its opioid settlements. TEVA posts small EPS beats. It cut sales allowances to add 18-40c the last 3-years. EBITDA of $4.5-$4.9bn looks overstated as TEVA adds back recurring cash costs for litigation, some R&D, regulatory compliance… BTN sees EBITDA at $3.1-$3.3bn. TEVA’s debt to EBITDA is 3.45x. At $3.2bn and adding the opioid settlements to debt, the ratio is almost 7x.

Edition: 181

- 08 March, 2024

How accounting for contract costs is impacting the earnings of 70 big software names

Technology

BTN continues their review of the software industry with a look at accounting for costs to obtain contracts. In this report they examine 70 software companies with M/Caps of $5bn+ and highlights four different groups: 1) Companies where the earnings benefit of deferring commissions represents a material amount of reported earnings. 2) Ones that may be about to face earnings headwinds from a decline in benefit from deferring commissions. 3) Ones that may be about to enjoy a positive inflection point where falling accruals are leading to lower amortisation relative to the new commissions being deferred. 4) Ones where amortisation is falling relative to deferred commissions which may indicate that new contracts are rising in the mix of new business.

Edition: 177

- 12 January, 2024

Communications

DASH reported 3Q23 results that beat consensus but much of this outperformance can be attributed to low-balling forecasts. Furthermore, BTN questions how much of the gain can be sustained given the size of the cuts to key expenses. Adjusted EBITDA was $74m ahead of the high end of guidance, but to get there the company added back an additional $30m in litigation costs, had a sudden $50m drop in G&A costs, a large decrease in advertising, and it appears that employee pay increases have stalled and R&D is flat-to-down. These boosts to EBITDA filter down to earnings. In addition, earnings benefitted from interest income rising by $31m.

Edition: 173

- 10 November, 2023

Hot pricing down south

BTN has come across several companies whose organic revenue growth and profits have been receiving material boosts from increasing prices in their Latin American operations at a far faster pace than foreign currency depreciation would seem to justify. When they look at the amount of pricing net of FX that many companies are getting of late, it’s greater than 10 percentage points. The problem BTN sees is the longer historical spread is closer to 2-3 percentage points. Many companies could soon see a sizeable part of their growth vanish.

Edition: 166

- 04 August, 2023

Technology

One cannot begin a discussion of OKTA without bringing up the ever-changing definitions of non-GAAP results. The items that are being added back continue to grow and are helping to boost earnings. Despite reporting beats in each of the last three quarters, BTN argues that without some short-lived cuts in expenses OKTA would have missed each one. The company is still unprofitable and FCF negative if it cannot pay employees with stock compensation at >30% of sales. The retention rate is falling due to decreasing upsell rates and a lack of expanding the number of seats, macro headwinds are getting worse and deals are taking longer to close.

Edition: 163

- 23 June, 2023

Consumer Staples

POST’s last Qtr saw pricing up $231m vs inflation costs up $157m adding 86-cents to EPS of $1.08. Much is egg-related. After Easter, eggs have fallen to $1.62/dozen from $5.33 in late Dec. BTN expects pricing to drop. Earnings are also helped by cutting marketing as competitors are spending more. POST is a roll-up story but its borrowing costs on new money is 8-9% and even with pricing ROI is ~6%. BTN estimates a 5% ROI on the latest pet food deal. Net debt is 5.1x forecast EBITDA and that assumes all this pricing holds. Losing $100m of pricing that exceeds inflation would push debt close to 6x EBITDA.

Edition: 159

- 28 April, 2023

Healthcare

Restatements don’t erase its problems - in early 2022 BTN warned clients that XRAY’s 2021 EPS had benefitted from unusual one-time items including some sleight of hand with R&D expense. Soon thereafter, key management departed after announcing results would fall well short of its previous forecasts. To make matters worse, the company later announced that it had detected problems with its accounting and it would be unable to file audited financial statements for 1Q22. While the accounting problems may appear to be behind the company, BTN sees several barriers to XRAY’s return to consistent, meaningful growth.

Edition: 152

- 20 January, 2023

Consumer Staples

MO's appeal is its 8.2% yield. However, smoking income is essentially equal to the dividend. The company is already missing forecasts, and smoking income tailwinds are about to become headwinds as volume decay is already accelerating. BTN does not see much cushion for the dividend going forward. Not for the first time the tobacco giant finds itself on BTN's Quarterly Focus List - companies they believe have a higher risk of reporting an earnings disappointment based on their analysis of earnings quality. MO's EQ score is 2- (Weak).

Edition: 150

- 09 December, 2022

Higher rates and the FASB may be about to break up the supply chain finance party

BTN have been warning investors about companies enjoying an unsustainable tailwind to cash flow growth by accelerating their use of short-term financing vehicles. However, rising rates are about to end the SCF party. They highlight Keurig Dr Pepper, JM Smucker and Procter & Gamble who have utilised SCF arrangements to a material degree and offer a simple framework for assessing the impact on their earnings and cash flows. They also discuss the implications of the FASB announcement this summer that it will be requiring enhanced disclosure regarding these programs (new rules go into effect in 2023).

Edition: 146

- 14 October, 2022

Real Estate

AFFO = Absurd Funds from Operations. Many investors do not realise that the company’s definition of AFFO features adjustments that are completely unrealistic and that without these adjustments, AFFO does not cover the dividend. BTN’s note examines this as well as multiple one-time benefits that made the latest quarter’s figure even less reliable. Click here to read more.

Edition: 143

- 02 September, 2022

Security software earnings quality comparison

Technology

BTN’s earnings quality comparison on six of the major security software players (Cloudflare, Palo Alto Networks, Okta, Fortinet, Zscaler and CrowdStrike) examines factors such as relative dependence on stock options and policies regarding capitalised software, sales commissions, network depreciation, and aggressiveness of non-GAAP adjustments. The report ranks the company from most to least aggressive.

Edition: 137

- 10 June, 2022

Six companies at risk of inventory-related 1Q'22 misses

The current macro environment is bringing to the forefront the importance of the different impacts that the various inventory accounting methods have on company results during times of inflation. BTN have noticed several companies whose inventory levels have declined which may have shielded them from the full impact of rising costs. Meanwhile, their revenues have benefitted from aggressive price hikes. They believe this may be setting the stage for earnings disappointments in 1Q and 2Q 2022. Companies highlighted General Mills, The Coca-Cola Co, The Hershey Co, Post Holdings, Ball Corp, and Mondelez International.

Edition: 131

- 18 March, 2022

Bank BTN (BBTN IJ) Indonesia

Financials

Value pick underpinned by fundamental momentum and lower risk - while GEM investors tend to prefer expensive bank franchises within Indonesia’s innovative financial ecosystem, Paul Hollingworth thinks they should instead be looking at much improved BBTN - FV of 6%, PBV 0.88x and Earnings Yield of 13.5%; the bank commands a sky-high PH Score™ of 10. A well-managed state-controlled bank dedicated to mainly collateralised mortgages (77% of portfolio), BBTN continues to benefit from the government’s Housing Loan Liquidity Facility. FY21 results showed positive momentum in Profitability, Efficiency, Liquidity, Asset Quality, Provisioning, Capital Adequacy and NIM.

Edition: 131

- 18 March, 2022

Consumer Staples

Raised prices to grow sales and margins amid cost inflation against easy comps. However, KO has NOT fully replaced inventory at higher costs as DSIs are down 10 days (with units likely down more than dollar terms). The repurchasing delays should pressure margins more quickly as KO will be buying at even higher costs than last fall. 1Q21 and 2Q21 bring tougher comps on pricing and volume and BTN expects margin pressure to build.

Edition: 129

- 18 February, 2022

Materials

Investor enthusiasm unwarranted, price rises will be unable to offset cost pressure - the price hike will only help 15 days in 3Q and BTN believes commodity inflation has worsened since the price increase was announced. SEE’s easy comps are over and the company will miss guidance this quarter. The stock remains a high conviction Short idea with an EQ (Earnings Quality) rating of 2 (Weak) - indicating that results have benefitted materially from aggressive accounting.

Edition: 118

- 03 September, 2021

Sysco (SYY)

Consumer Staples

Behind the Numbers added SYY to its Top Sell list (11th June) arguing the recovery seemed more than priced in, Covid-related market share gains would quickly be lost and there was little room left to grow by acquisition. In addition, SYY has a history of reporting results with unusual items that allow it to top estimates. The last quarter was no exception. BTN identified over 7 cps in unusual benefits without which the company would have reported a miss. The stock is down 9% since addition but they see a strong possibility for disappointment in upcoming quarters.

Edition: 115

- 23 July, 2021

Equinix (EQIX)

Real Estate

When the market digests the fact that the company is not self-funding, the degree of dilution it is incurring to fund growth, and that the dividend is far outgrowing the organic growth rate, the stock price could be more than cut in half. While data centres might be a hot investment right now, BTN’s analysis underlines the importance of paying close attention to a company’s underlying performance in addition to highlighting several earnings quality concerns.

Edition: 110

- 14 May, 2021