Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

US: The Fed is far behind the 8 ball

Higher unemployment expectations have flared to extremes. In five of the six previous instances when UMich Higher Unemployment Expectations first crossed the 60% threshold, real GDP contracted four quarters out by an average of -0.8% YoY; despite this, the Fed’s median projection for 2025 GDP growth sits at 1.7% YoY. Regardless of the evolving core inflation narrative, the Fed has responded to economic hardship on par with the current episode in previous cycles with aggressive easing actions. With just two rate cuts expected and priced by year-end, investors are not prepared for a repricing that would validate the historical context. Every single cycle following a crescendo in UMich Higher Unemployment Expectations saw the Fed funds rate cut by more than a full point 4 quarters out; clearly, the Fed, rates traders and sell-side alike are all out of step with history.

Edition: 207

- 21 March, 2025

The state of video gaming in 2025

Communications

Matthew Ball* joined Revelare for a discussion on the outlook for video gaming. He shared his in-depth analysis of waning growth trends for gaming spend and engagement, pricing power for video games, title development issues, Nintendo and the outlook for the Switch 2, as well as the potential impact of GenAI among other topics.

*Matthew is the CEO of Epyllion, which provides investment and strategic advisory services, produces television, films, and video games, and co-operates/owns the Roundhill Ball Metaverse ETF, which was the single largest sector ETF launch of 2021, among various other operating subsidiaries.

Edition: 205

- 21 February, 2025

South Africa: Ground to a halt

The economy continues to flatline in real terms, with nominal growth is at an all-time low as well. SARB has begun a cautious easing cycle, but real rates are stuck at record highs. Nominal rates are coming down gradually, but real rates and rates/growth gaps are still at record highs. As a result, South Africa's public debt ratio continues to rise rapidly. Unlike Brazil, where the policy onus falls both on the central bank and the treasury, Jonathan Anderson points out that in South Africa the ball is almost completely in SARB's court, waiting for further easing and any measures to help rein in long yields. Until that happens, the main silver lining of the current painful combination of high rates/no growth is that the external balance is back in surplus, the rand is relatively stable, and fixed income and carry returns are very attractive. Jonathan stays all-in on fixed income.

Edition: 204

- 07 February, 2025

Euro: Running behind

For the fourth time in 2024, the ECB cut rates by 25bps. At 3.0%, the deposit facility rate is down 100bps from its peak and approximately half-way down to what many believe to be the neutral rate of ±2.0%. PMIs now suggest that the Eurozone economy may barely grow, so concerns over undershooting inflation have risen. They should, according to Niall Ferguson. However, calls for accelerating the pace of rate cuts are unlikely to gain traction until there is a clearer signal of inflation undershooting and hard data on growth stagnating or even being negative. The ECB could also be prompted to consider a larger than 25bps move if Trump’s trade threats materialise. Nevertheless, Niall’s baseline is that the ECB will cut by 25bps in January and March. In short, they will remain behind the ball. He remains short EURUSD.

Edition: 201

- 13 December, 2024

South Africa: The endless wait for SARB

The economy continues to flatline in real terms, with nominal growth at an all-time low. Rates are stuck at record highs, with long yields at record levels and SARB keeping short rates at a 15-year high as well. As a result, South Africa’s public debt ratio continues to rise at a rapid pace despite a very conservative fiscal stance. Unlike Brazil, where the policy onus now falls equally on the central bank and the treasury, in South Africa the ball is almost completely in SARB’s court, waiting for a combination of rate cuts and QE measures to rein in long yields. Until that happens, Jonathan Anderson sees the main silver lining of the current high rates/no growth combination is that the external balance is back in surplus, the rand is stable, and fixed income and carry returns are very attractive.

Edition: 191

- 26 July, 2024

The warning sign in US labour

The latest Non-Farm Payroll report showed the US keeps adding jobs at a sustained pace, but Alfonso Peccatiello says this feels weird. It’s hard to square how the US job market can remain so resilient even as rates remain high for long. One of the most reliable long-term indicators of job market weakness is the Sahm Rule: when the 3-month moving average of the unemployment rate exceeds its 12-month low by 0.5%, the recession is here. The latest reading says 0.37%, often cited by bears as a warning sign. If the underlying labour market weakness gets more evident, the Fed needs to react fast. From a long-term asset allocation perspective, one can still remain invested in risk assets here but must be vigilant of surfacing labour market weakness and the Fed reaction function. If they play ball, buying bonds when 10-year Treasuries approach 4.6-4.7% offers great risk/reward.

Edition: 188

- 14 June, 2024

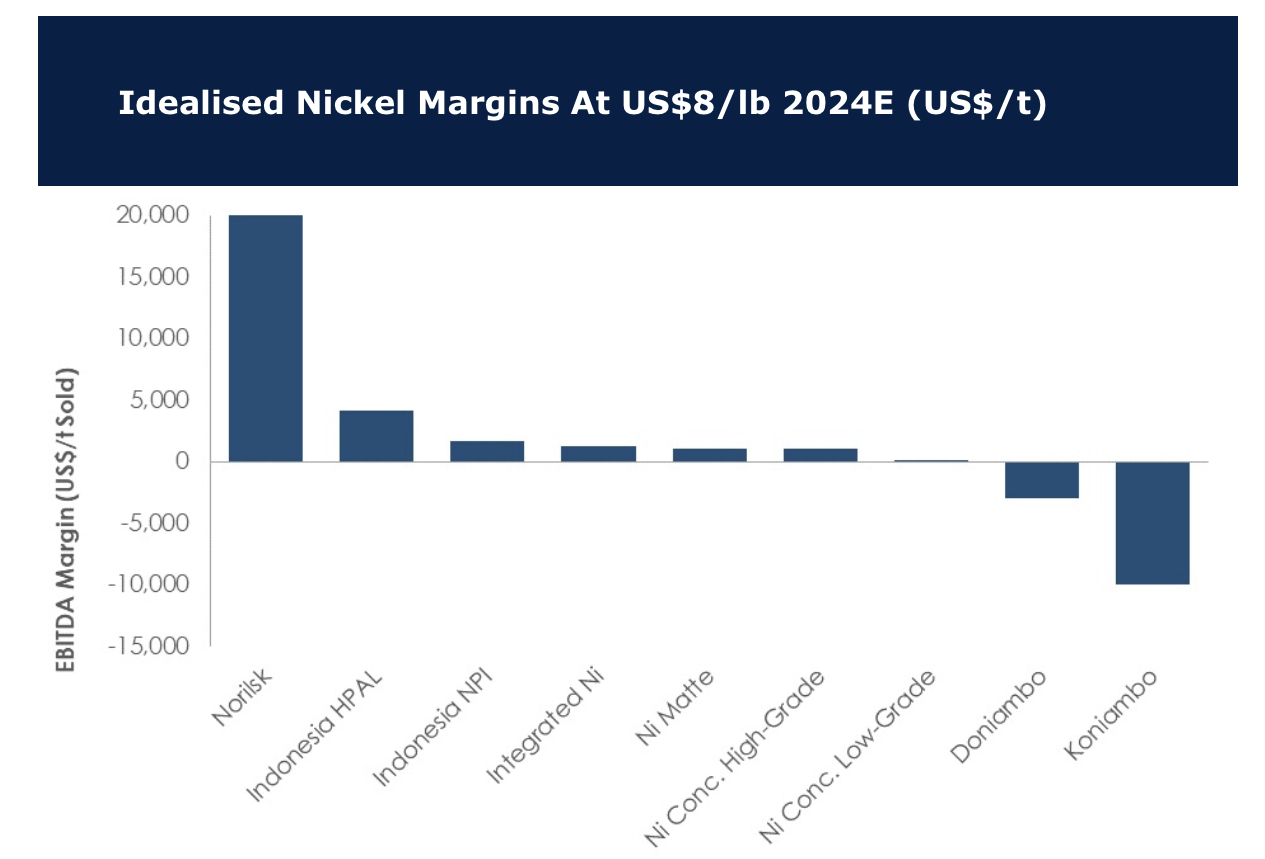

Wrecking ball demolishing the house of nickel

A year ago, nickel stood at US$13.00/lb, now it stands at ~US$7.30/lb. David Radclyffe turned bearish in July 2023 – since then producers have been hit hard, with projects across the board facing closure or review. The chart shows some idealised EBITDA margins for 2024; even at US$8.00/lb, some operations are already under water. With lower prices of US$7.50/lb or US$7.00/lb, only a few would not be in the red, including Norilsk, the Indonesian HPAL plants and some other Indonesian plants with cheap power. With so much pain in the industry, investors will no doubt be asking whether it’s a good time to start buying at the bottom? Before rushing in, remember Indonesia production is still ramping up and not enough production is being taken off-line. The wrecking ball will continue to swing for some time more and do further damage to the house of nickel.

Edition: 179

- 09 February, 2024

Jet2 (JET2 LN) & BAE Systems (BA LN) UK

Consumer Discretionary & Industrials

Both these stocks look seriously cheap and both have seen upgrades over recent results. Jet2 comes with very strong finances and a lot of market share growth. Of course, travel can be cyclical and lots of the cash is not really theirs, but Willis Welby’s adjusted implied to Y3 EBITM ratio is just 25, which is really low. BAE’s share price responded well before giving part of the gains up on the announcement of the Ball acquisition. Willis Welby considers BAE to be a first-rate international defence company and the expectations ratio of 57 is at a major discount to its largely US peers.

Edition: 168

- 01 September, 2023

Materials

Reports across-the-board misses and guides for lower-than-expected 2023 earnings - inventory growth continued unabated and Gradient remains concerned that management’s attempts to curtail production to right-size supply and demand may be too late to alleviate near-term gross margin pressure. Receivables continued to increase on an absolute and relative basis, suggesting the company faces an elevated risk of revenue shortfalls. A material relative decline in accrued employee costs, along with lower depreciation expense stemming from a recent accounting exchange, may have temporarily prevented a more material operating margin contraction.

Edition: 155

- 03 March, 2023

Materials

The can-maker’s equity is expected to come under further pressure - the main concerns cited in Gradient’s 13-page report include: 1) Volume and profitability headwinds. 2) Inventory growth higher than targeted and has outpaced forward sales estimates. 3) Growth in receivables suggests a pull-forward of revenue. 4) Accrued compensation fell to a five-year low relative to adjusted operating expenses. 5) Despite the recent share-price correction, BALL still appears expensive. Other active shorts Gradient have initiated coverage on this year include ADT, Cerence, Lamb Weston, Owen’s & Minor and RingCentral.

Edition: 140

- 22 July, 2022

Six companies at risk of inventory-related 1Q'22 misses

The current macro environment is bringing to the forefront the importance of the different impacts that the various inventory accounting methods have on company results during times of inflation. BTN have noticed several companies whose inventory levels have declined which may have shielded them from the full impact of rising costs. Meanwhile, their revenues have benefitted from aggressive price hikes. They believe this may be setting the stage for earnings disappointments in 1Q and 2Q 2022. Companies highlighted General Mills, The Coca-Cola Co, The Hershey Co, Post Holdings, Ball Corp, and Mondelez International.

Edition: 131

- 18 March, 2022

Blue states’ growing crackdown on plastic

Democratic-controlled states have rapidly expanded laws taking aim at reducing consumer dependence on plastic. The surge in recycling laws, particularly extended producer responsibility (EPR) will raise costs for packaging producers, but manufacturers of more easily recyclable materials will benefit relatively. Aluminium is particularly well-positioned due to its properties, and manufacturers such as Crown Holdings, Ball Corp and Ardagh Metal Packaging will benefit from the Dem’s crackdown. Expect other companies leading the change from plastic to paper to also benefit, such as Graphic Packaging.

Edition: 127

- 21 January, 2022

Russia & NATO: State of play

Upcoming meetings between Russia and the US will be key pointers for the possibility of de-escalation. While Russian demands on NATO remain a non-starter, there is agreement among many US policymakers (shared by some EU members) that NATO enlargement can’t continue on autopilot. Instead, a new security arrangement is needed with Russia. This could provide an opportunity for Russia to climb down, if the US is also able to lean on Ukraine to play ball on Minsk implementation. But, if these fail, we can expect the West to increase the pressure by highlighting the cost of a conflict. This would indicate a diplomatic deadlock and so a high risk of conflict.

Edition: 126

- 07 January, 2022