Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

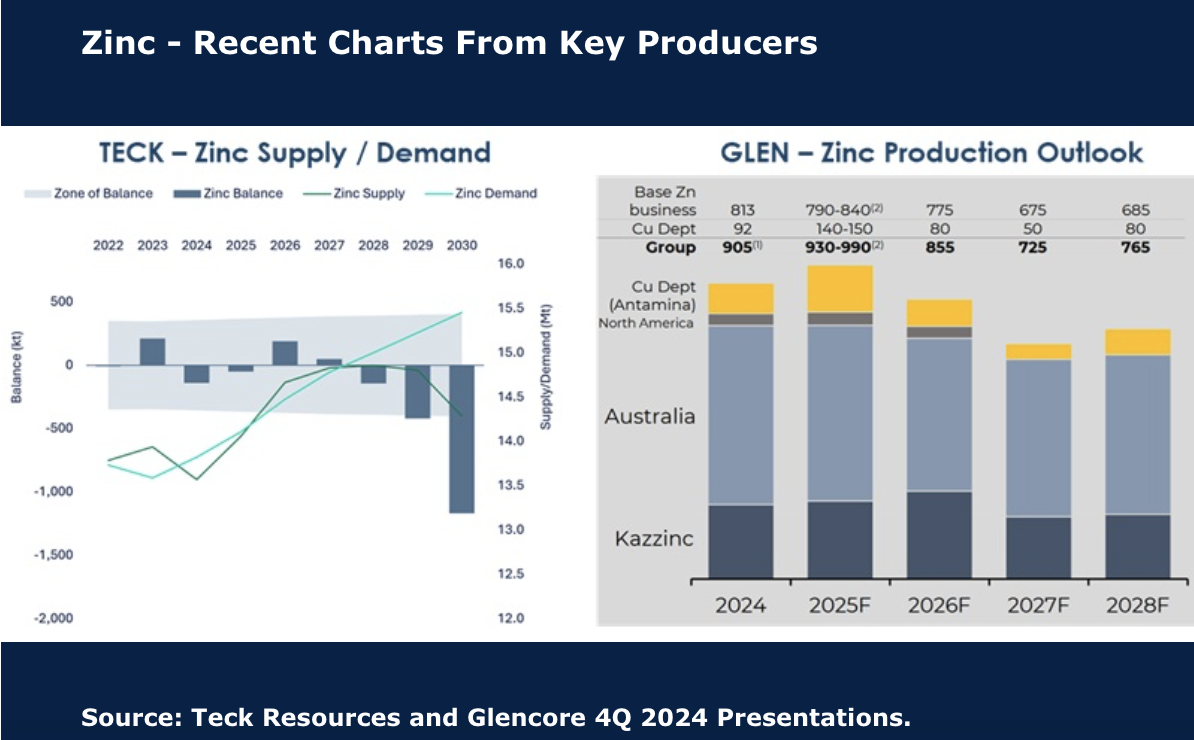

Zinc: Lagging in 2025

As Zinc production falls 2.8% YoY, the modest deficit appears to be accelerating towards the end of the year, as indicated by two of the largest players in the industry (see chart). Ailing production is in part due to the maturing of existing operations, although headwinds are expected to be offset in part by full year of production restarts, with Ozernoye the key one to watch. Whilst the zinc price is lacklustre, the fundamentals look ok. Inventories are moving in the right direction and are already less than 1 week of global supply, which to the team appears tight. Another positive is also expected to come from lower benchmark Treatment Charges (TCs) given a shortage of concentrate in the market. 2025 and 2026 will really be about the tussle of additional supply offset by closing supply.

Edition: 206

- 07 March, 2025

Healthcare

JEH's high brand value stems from a unique business model that integrates everything from product planning and design to manufacturing, processing and sales. This approach not only differentiates it from other brands but also ensures product quality and craftsmanship, earning the trust of its customers. Yuka Marosek believes JEH’s 19x PE is not only justifiable but expandable with an OP margin of 27%, expected OP growth for 2025 of 35% y/y and ROE at 23%. She considers LVMH to be the closest benchmark due to its focus on high-end concepts and explains why JEH is a beneficiary of inbound tourism with foreign buyers attracted to the company’s glasses produced in Sabae.

Edition: 203

- 24 January, 2025

2024 was ugly for turnarounds, 2025 should be awesome!

An uptick in TOBs, MBOs and merger talks is suddenly making it unsafe to short low-PBR companies indiscriminately. Dozens of previously complacent companies are acting to up their profitability and the market is taking notice. More than two-dozen large- and medium-cap stocks with deep discounts to the benchmark began to bounce off well-defined support levels in late Dec. The turnaround strategy was tough in 2024 because most of the stocks that fell out of bed in 2023 were not turnarounds. They were grossly over-valued theme stocks that suffered massive changes in sentiment. This year is starting out completely different. Mike Allen introduces 20+ turnaround ideas that have more potential than anything he saw at this time a year ago.

Edition: 202

- 10 January, 2025

Active GEM Funds: Positioning insights

Steven Holden highlights 3 key investment themes across his Global Emerging Market fund universe: 1) Average exposure to South Korea has plummeted to 15-year lows of 9.25%. Net outflows of $2bn and a significant reduction in exposure to Samsung Electronics have collectively driven South Korean exposure down by -1.75% over the past six months. 2) Real Estate exposure is rebounding. The percentage of funds invested has risen to 76.7%, nearing a 5-year high, with average weights and benchmark metrics at their highest levels in 10 years. 3) South African Financials are experiencing a resurgence with 69.54% of funds now holding exposure - the highest percentage in 4.5 years.

Edition: 202

- 10 January, 2025

High conviction financials for 2025

Financials

Galliano's Financials Research

Bradesco, Hana Financial and Bank of Baroda are Victor Galliano’s top picks amongst the GEM banks due to deep value with positive returns catalysts, while his sell on premium-valued Nubank is due to fundamental return headwinds emerging. In the Japanese banks, Victor identifies Mizuho and Resona as key beneficiaries of higher benchmark rates going forward, alongside very attractive valuations and supported by strategic share portfolios. CME Group is his 2025 pick in global exchanges, as a "flow monster" with a very strong competitive position. PagSeguro is his deep value, contrarian pick in payments.

Edition: 201

- 13 December, 2024

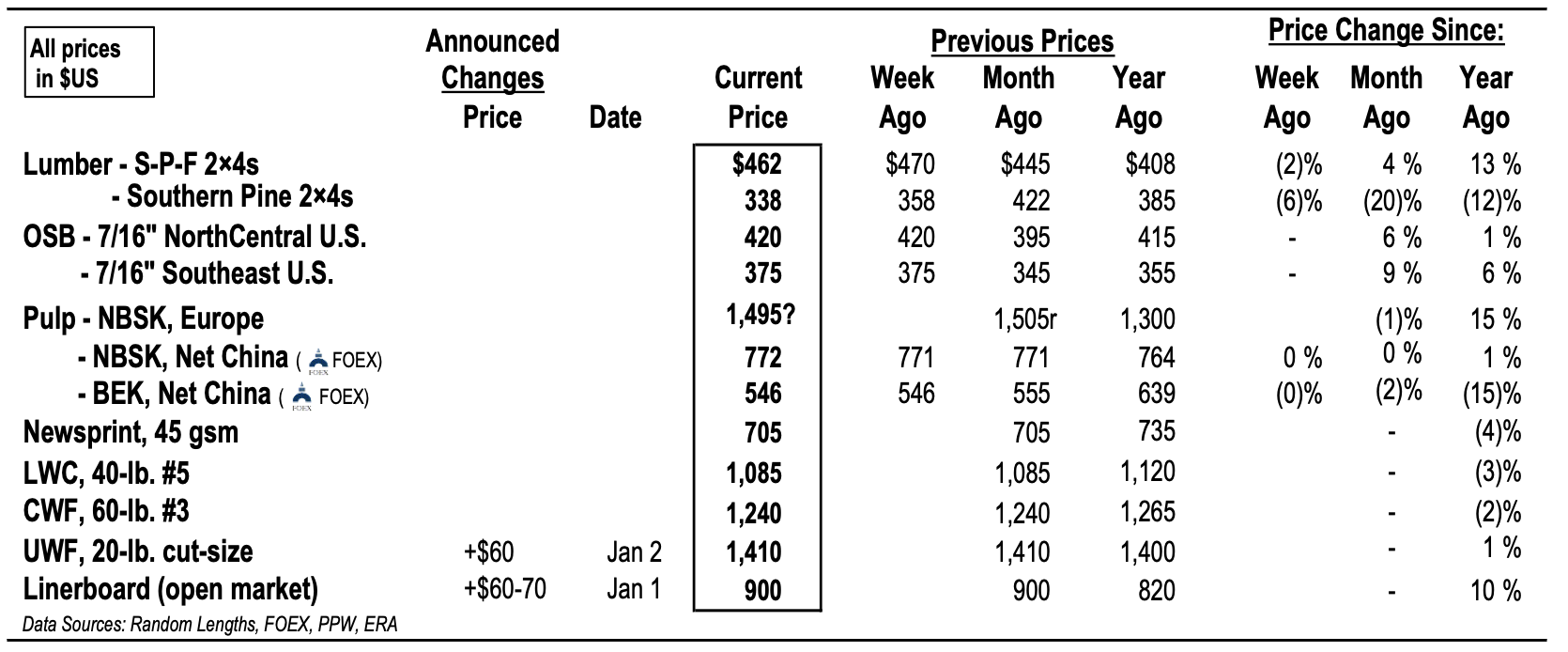

Lumber: Cracks in the market

The North American lumber market continued to weaken last week as price declines, initially concentrated in Southern Yellow Pine (SYP), extended to Spruce-Pine-Fir (S-P-F) and other species. Benchmark S-P-F 2x4 prices dropped by $8 to $462, while SYP 2x4 prices fell an additional $20 week-over-week to $338. With wintry weather affecting Canada and the northern US demand is slowing, and buyers are expected to manage inventories cautiously, particularly in states with year-end inventory taxes. The ERA team anticipates further near-term price declines across all species. However, with SYP prices now at or below cash cost levels for many southern mills, additional market-related sawmill downtime, potentially aligned with the holiday season, is likely.

Edition: 201

- 13 December, 2024

Chile: Slow and steady

Igal Magendzo has modified his base scenario for the path of the monetary policy rate (MPR). While Igal still believes the Central Bank will continue lowering the benchmark rate, he now projects that this will be preceded by a ‘front load’ approach. Nonetheless, he continues to think that from January 2025, the Central Bank will resume a ‘slow and steady’ approach, with pauses, until reaching a neutral rate of 4.25% in June of that year. The Pacifico team has decided to close the monitoring of the tactical paid position in 3m6m CLP/Cámara, as despite having a fair value approximately 15 bps above the market, the current level is almost identical to the entry point, meaning the upside potential is zero.

Edition: 196

- 04 October, 2024

Motor Oil (MOH GA) Greece

Energy

MOH’s Q2 results were much stronger than what benchmark refining margins implied for the quarter. This is thanks to stronger gasoline vol & cracks and the higher naphtha-gasoline spread compared to Q1. ResearchGreece upgrades their rating on the stock to OWN IT with a TP of €28.5. The share price is down -15% since the government imposed another windfall tax on refineries in Jun. At 3.3x clean EBITDA 2024-2025E, there is enough valuation upside (+30%) to compensate for the low refining visibility and enough cash flow to support a solid dividend yield out of 2024 earnings (min. 5%) without raising net debt.

Edition: 194

- 06 September, 2024

Financials

Galliano's Financials Research

Kyoto Financial’s stakes in 3 key listed Japanese corporates are valued at over 85% of its market cap with its total equity holdings accounting for 130%+ of its market cap. However, management intends to retain the bulk of these positions, opposing the growing trend for Japanese listed companies to unwind crossholdings. Given this decision, combined with underwhelming fundamentals (e.g. not as well geared into rising domestic interest rates as peers; neither is it well exposed to potentially rising benchmark rates through BoJ deposits; and unattractive valuation), Victor Galliano is negative on the stock, preferring the likes of Resona, Mizuho and SMFG instead.

Edition: 191

- 26 July, 2024

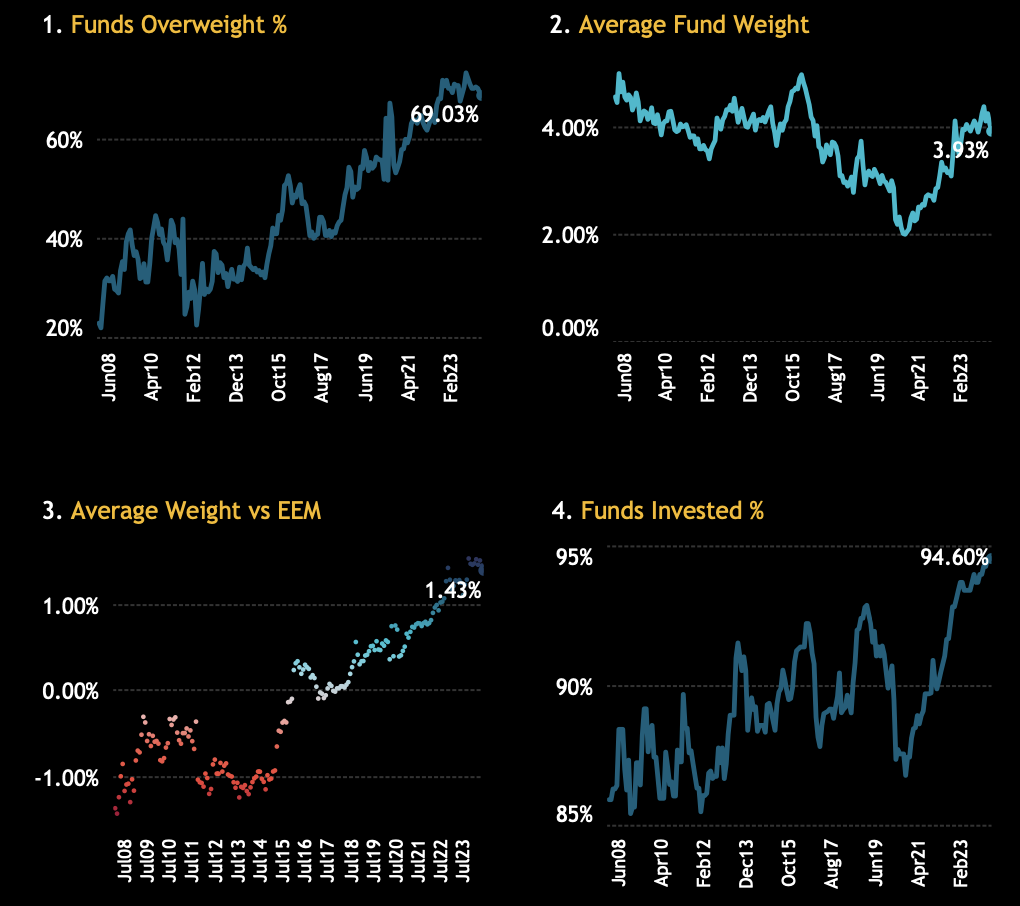

Mexico: GEM funds wrong footed after election results

Active GEM fund managers were caught off guard with their exposure to Mexico heading into the election. The nation had benefited from increased inflows and exposure over the past 3-4 years, with the percentage of funds invested reaching an all-time high of 94.6%. However, the country’s positioning against the benchmark is where it truly stands out, with the percentage of EM funds overweight the benchmark now at 69% compared to just 20% in 2011. This proved costly in the wake of the elections, with crowded stocks like Banorte experiencing big price declines. As it stands in the EM space, Mexico is the largest overweight by average fund weight and the second most common overweight after Indonesia.

Edition: 190

- 12 July, 2024

Crude may stay rangebound this summer

More than three weeks of rangebound movements in benchmark crude prices, which have seen Brent broadly locked in a $82-84/barrel range, has stirred up some unease in the market as to whether there might be factors gathering in the background that could prompt a bull run or a bear slump. With the geopolitical risk premium firmly out of the way for the time being – both on account of the Gaza war and the Ukraine war – Vandana Hari thinks the conditions remain conducive for the current equilibrium to hold for a bit longer. Economic outlook is in the driver’s seat for the oil complex and there is plenty of uncertainty and skittishness in the broader financial markets. However, the mood shifts are a few degrees removed from implications for oil demand, so they do not produce big price swings in crude.

Edition: 187

- 31 May, 2024

Watch the dollar

Michael Howell's Global Liquidity Index inched lower in March 2024 to a reading of 27.5, ('normal' range 0-100). This is the weakest index since last November and continues the recent sideways pattern. It's not a surprise, as it aligns with his recent warnings of a coming dip in Global Liquidity. The significant decrease can largely be attributed to Asian economies, notably China, the dominant regional player. With geopolitical tensions and rising gold bullion prices, Howell's main focus this month shifts towards the US dollar. Like in the mid-1980s, the USD's relative strength is defying consensus. Michael predicts US economic acceleration, higher policy rates, and term premia being pushed into positive territory, which will force the 10-year benchmark bond to test yields of 5-5.5%. He continues to favour equities and recommends buying into any setbacks.

Edition: 184

- 19 April, 2024

Bank of Africa (BOA MC) Monaco

Financials

Following the stock’s 40% jump over the last three years, BOA has exhausted its upside, according to AlphaMena, whose valuation methods now flash red. The fruitful African expansion seems to be fully priced in and investors are looking for a new catalyst. Why not a new bold move by targeting the attractive and large Egyptian market? While BOA trades at a discount to the sector on both P/E (18%) and P/B (12%), this is warranted because of its low ROE and dividend yield (at 10% and 2.4% vs. 12.5% and 3.4% for its benchmark, respectively). BOA is fundamentally expensive amid an anticipated near-term reversal in monetary policy.

Edition: 182

- 22 March, 2024

Indonesian equities are too cheap to ignore

The Indonesian stock market is priced for bad times, but CPI has fallen sharply and the central bank should start cutting benchmark rates soon. While some companies are suffering cost creep and margin contraction, Mike Churchill continues to find plenty of stocks that are posting good earnings and decent top-line growth. Stocks recently added to his Classical Insights portfolio include: Bank Danamon, Bumi Serpong, Delta Dunia Makmur, Indofood, Jaya Konstruksi, Kobexindo Tractors, Mulia Industrindo, Surya Semesta and United Tractors.

Edition: 175

- 08 December, 2023

Artificial Intelligence: Lifecycle of a bubble

Technology

As more and more models are released by companies, start-ups and open source, the harder they will have to work to attract users, resulting in falling prices. The current mantra (and what companies seem to be raising money on) is that $20 per user/month is the benchmark and at this price, a lot of money will be made. However, Richard Windsor suspects the real price will be no more than $20 per user/year. This means that in 12 months when these new companies need to raise more money, they will have badly missed their targets and the long-term outlook will be lower. This is what pricks the valuation bubble and causes expectations and valuations to reset to reality.

Edition: 173

- 10 November, 2023

Japan: Big changes ahead

As Niall Ferguson expected, the BoJ held policy steady with Governor Ueda’s comments indicating no change in approach. Niall’s base case remains that disinflation’s presence will remain in Japan for several more months, with core inflation stabilising at ~2% next year. Sometime soon, YCC will need to be scrapped, the benchmark rate increased to 0%, and a path fleshed out for the BoJ's massive asset purchase program. More forward guidance is almost certainly on the way in Q4 as Ueda eases the market into pricing in the momentous policy adjustment to come. Niall anticipates a yen rally and the continued steepening of the yield curve in Q4, He also recommends being LONG Japanese banks.

Edition: 170

- 29 September, 2023

The decline in Turkish investor positioning

Ownership levels in Turkish equities have fallen to new lows among active EM equity funds. The percentage of funds invested in Turkey stands at an all-time low of 31.45%, pushing average holding weights down to just 0.38%. For the first time since 2008, active managers are now running an underweight in Turkey, with just 18.6% of funds positioned ahead of the iShares MSCI Emerging Markets ETF. With both active weights and benchmark weights so small, the risks of not holding a Turkey position are diminishing for the average active manager. Only 16 of the 373 funds in Copley Fund Research’s analysis hold more than a 2% allocation – to bet big on Turkey here is a significant non-consensus call.

Edition: 168

- 01 September, 2023

China Consumer Staples: Conviction overweight

Consumer Staples

Steven Holden reports how active MSCI China funds are positioned for the outperformance of the Consumer Staples sector - overweights are near record levels at +3.97% above the benchmark. Today’s 7 most widely held stocks in the sector join a prized group of just 15 companies that have ever been owned by more than 20% of funds at any one time. Dubbed the 20% Club, 8 of these stocks have since left, with Luzhou Laojiao the most recent entrant. The remaining 6 stocks are Kweichow Moutai (the highest conviction holding), China Mengniu Dairy, China Resources Beer, Wuliangye Yibin, Inner Mongolia Yibin and Tsingtao Brewery.

Edition: 163

- 23 June, 2023

Japan stocks back in vogue, prefer domestic plays

Tim Morse reiterates his view of why he believes Japan’s inflation rate is likely to surprise the market on the upside, forcing the BOJ's hand into dramatically tweaking its yield curve control which will strengthen the yen this year. This in turn should lead to a major divergence in the relative performance of domestic-related stocks versus multinationals and exporters. In particular, Tim is positive financial names, deep value cyclical and inbound tourism plays. Potential upside in JGB yields will remain fairly limited as domestic institutional investors are waiting in the wings to raise their exposure if the ten-year benchmark rate is allowed to move freely above the bank's current 0.5% ceiling.

Edition: 161

- 26 May, 2023

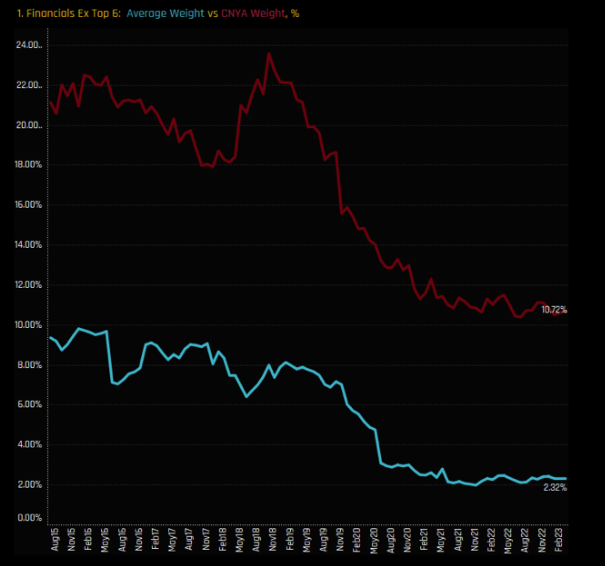

China A-Share Financials: Out of love

Ownership levels in the China A-Share Financials sector are at their lowest ebb, driven by lack of confidence. The top 6 most widely held Financial stocks make up 5.5% of the average active A-share fund and 5.75% in the iShares MSCI China A-Share ETF, but it’s outside of this where the divergence between active and benchmark occurs. Across 83 companies, active A-Share funds have allocated just 2.32% whereas the iShares MSCI China A-Share ETF has allocated 10.72%. The message is clear – stick to the top 6 and avoid the long tail.

Edition: 159

- 28 April, 2023

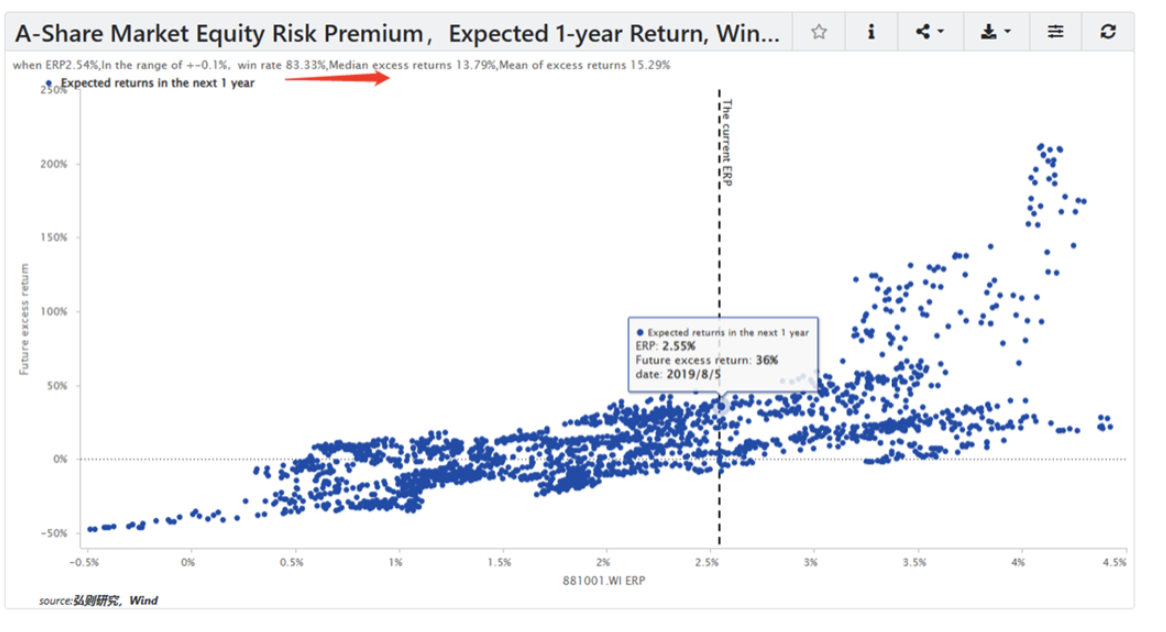

China: The volatile nature of the A-share market

Being volatile in nature, the A-share market displays a robust positive relationship between market valuation change and market investment returns. That is to say that valuations drive the A-share market's investment return in the short run, while in the long run it is company earnings that determine the market performance. With China's economic recovery, company earnings will start to bottom out in Q1 of 2023. With benchmark index valuations hovering around middle-and-low ranges, the A-share market appears an attractive deal with limited downside risks. With the equity risk premium of around 2.5%, there is a fairly high possibility (83.3% probability) that the market will deliver a 13% excess investment return in the next 12 months (against the 10-year treasury yield).

Edition: 157

- 31 March, 2023

Financials

Galliano's Financials Research

4Q22 results confirm that NU is the benchmark among EM neobanks in terms of activity rates, as well as trends in revenues and costs per client and digital efficiencies. Victor Galliano sees further potential for broadening and deepening the product offer to customers, at little incremental cost especially in Brazil, to drive cost effective revenue growth. Victor’s proprietary NU model forecasts are broadly in sync with positive consensus estimates; he forecasts group ROE of close to 30% in FY25, despite high cost of credit assumptions.

Edition: 155

- 03 March, 2023

Canada: Resilient for now

Canada’s inflation remains at a near four-decade high, but households’ exposure to variable-rate mortgages has tied the hands of the Bank of Canada (BoC). In January, the BoC hiked the benchmark overnight rate by 25bps to 4.50%, as anticipated. Niall Ferguson now expects the BoC to pause for the rest of 1Q23 (75% probability). Combined with a tight labor market and a likely oil price rally, he reckons higher inflation expectations will persist in Canada, putting the BoC in an even worse position later in the year. Niall remains bearish Canadian real estate.

Edition: 153

- 03 February, 2023

UK Healthcare: Value funds drive underweight

Healthcare now stands as the third largest underweight risk to UK investors (behind Consumer Staples and Energy) driven by two key factors: 1) AstraZeneca positioning. The net underweight of -2.62% accounts for more than the net underweight of -2.36% for the entire sector. Overweights in Smith & Nephew, ConvaTec and out-of-benchmark Sanofi provide the partial offset. 2) Value Fund positioning. Active UK Value managers are seemingly happy to let underweights increase, with a huge gap of -6.27% vs. the FTSE All Share weight. Value managers are banking on some serious underperformance.

Edition: 151

- 06 January, 2023

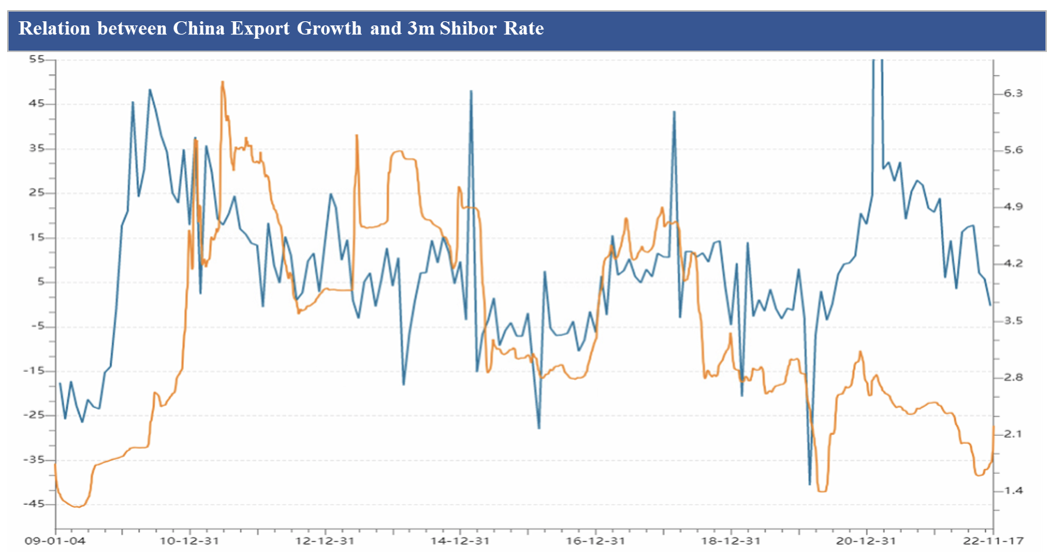

China: Bond market panic & downward risks in Q4

With positive changes in Covid policy and easing property measures, China’s benchmark interest rates have shot considerably higher in November. However, the Horizon Insights team believes that the still-weak fundamentals don’t support such a sharp increase, especially with the simultaneous slowdown in Chinese exports and real estate – expect benchmark rates to stay at relatively low levels in coming months (see chart). As we pass through Q4 the major risks of a US and Chinese tumble are growing, which could bring a huge shock to the global economy.

Edition: 149

- 25 November, 2022

Mexican allocations continue to surge higher

Over the past 6 months there has been some aggressive country repositioning among active EM managers - Mexico is now the largest country overweight position (vs. the benchmark iShares MSCI EM ETF). Despite this sentiment shift, Steven Holden says allocations look far from stretched (avg. weights among active EM funds: 3.4% today vs. nearly 5% in 2015). On a Style basis, Yield managers have increased weights the most. On a stock level, Grupo Financiero Banorte and Wal-Mart de Mexico have been instrumental in Mexico’s rise up the ranks.

Edition: 147

- 28 October, 2022

The ASEAN rotation

In Steven Holden’s latest report, which features a comprehensive analysis of active EM fund positioning in the ASEAN region, he finds that the region has been a key beneficiary from a drop in EM Europe allocations following the Russian exodus. Indonesia and Thailand have captured the lion’s share of the rotation, whilst investors sell down stakes in non-benchmark Singapore exposure. Above all, this rotation comes at a time when allocations are at their lowest levels on record for many countries in the region.

Edition: 142

- 19 August, 2022

France: Europe's high conviction holding

Global equity managers are positioned at their highest ever overweight in French equities - average holding weights have moved towards the top end of the 8-year range at 4.16%, pushing net overweights to a record +1.48% above the iShares ACWI ETF benchmark. Out of the 365 global funds in Copley’s analysis, 64.4% are overweight France compared to the ACWI index. Aggressive Growth and Yield managers have led the charge. On a stock level, LVMH is the most widely held name, while Sanofi and Capgemini have benefited from fund rotation this year.

Edition: 141

- 05 August, 2022

Australia: Down, down, down under

The Reserve Bank of Australia (RBA) has increased its benchmark policy rate by 50bps to 0.85%, with the 2022 sum of increases now at 75bps. Frank Shostak warns that the lagged momentum of the inverted policy rate does not bode well for economic activity in the months ahead (see chart 1). His AMS indices also indicate a subdued annual growth of job ads and a poor PMI services index ahead (see charts 2 & 3), further adding to the worsening outlook.

Edition: 137

- 10 June, 2022

The China Rotation: Allocations hit 4-year lows

Allocations in China & HK equities among active EM investors have plummeted 10%+ in the space of 18-months (India, Taiwan and Mexico have been the biggest beneficiaries) - on a sector level, China Industrials and Consumer Staples are the overweights, with managers rotating into Financials and away from Consumer Discretionary. On a stock level, Alibaba remains a core holding; out-of-benchmark AIA Group and Midea Group are popular, and for Value managers, China Mobile and CNOOC are key overweights. Active managers have stayed away from both NIO and Xiaomi, so pressure to invest on the grounds of benchmark tolerance should be disregarded.

Edition: 136

- 27 May, 2022

Utilities ownership among active Asia Ex-Japan funds hits lowest levels on record

With risk assets taking a turn for the worse it is surprising that a safe haven sector is so far out of favour (average fund weight is just 0.98%) - the record underweight has been driven in large part due to benchmark increases in stocks that active managers have ignored (Adani Green Energy, Adani Transmission and Adani Gas). However, one can’t ignore the record low participation levels, with just 41% of managers exposed to the sector. With Aggressive Growth investors all but abandoning Utilities and only 35% of Growth investors holding a position, if risk assets continue to deteriorate, some of that rotation away from the sector should start to reverse.

Edition: 135

- 13 May, 2022

GEM Funds Investor Positioning Insights: India maximum divergence

Stephen Holden’s data highlights the growing divide between Value and Aggressive Growth managers in India - while Aggressive Growth investors double down, especially in Financials and Tech, Value managers are finding fewer opportunities to invest, and appear comfortable allowing their underweights to increase. That’s not to say there are no Value opportunities in India, just not enough to match either the benchmark weight, or the weight of their Growth peers. As the world focuses on a potential Growth to Value switch, in EM at least, India will be a key driver of relative performance between the two sets of investors.

Stocks highlighted include HDFC Bank, Housing Development Finance, Indian Oil Corp, Infosys and Tata Consultancy.

Edition: 134

- 29 April, 2022

Canadian Banks: Tax grab

Financials

New bank and insurance company surtax unjustified - unfair to use pandemic earnings as a benchmark to support additional taxation. It is not a good look to attract foreign investment to the sector or for the sector's performance over the long term, given its importance to retirement portfolios and Canada's economy. Onerous taxation during 'good times' could hurt banks during 'bad times' and change the calculus on bank expectations for ROE through the full cycle. Bank of Montreal remains Nigel D'Souza's only Buy-rated bank of the Big Six.

Edition: 133

- 14 April, 2022

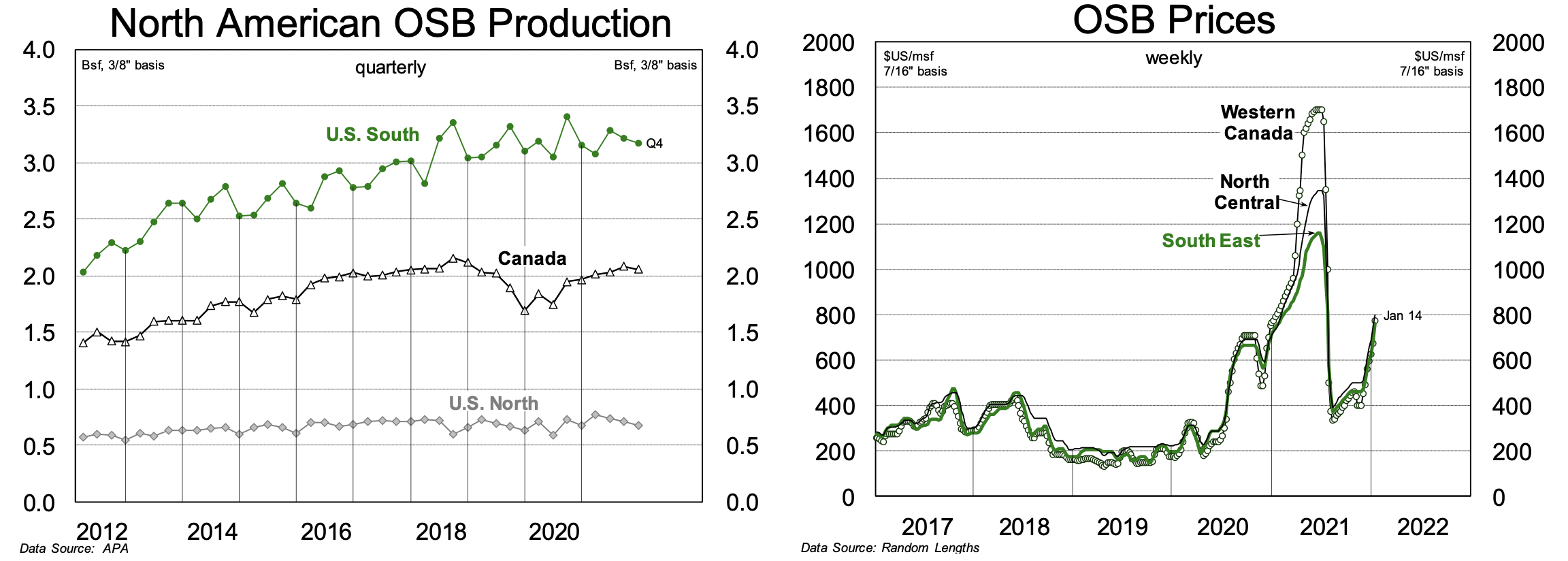

North American OSB production

North American OSB markets have shifted into high gear, with benchmark North Central 7/13” prices up by $145, to $800 over the last three weeks (see chart). While demand has been robust, supply shortages have had greater impact on the market. Despite two OSB mill restarts in 2021, prices have not begun cycling back closer to historical averages and higher prices are here to stay for another couple of years. To play it, go for West Fraser Timber and Louisiana-Pacific Corp.

Edition: 128

- 04 February, 2022

Pharma: Saviours of the world

The global healthcare sector has begun to rally hard after hitting all-time lows in terms of its recommended weight vs benchmark. It had been previously ignored since it doesn’t fit in the current debate about growth vs. value, but Simon Goodfellow thinks it is worth another look. The risk of price controls on US prescription drugs is much lower than feared; Congress has no time for legislation in the run up to elections, and public opinion may have changed after the success of Covid vaccines.

Edition: 115

- 23 July, 2021