Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

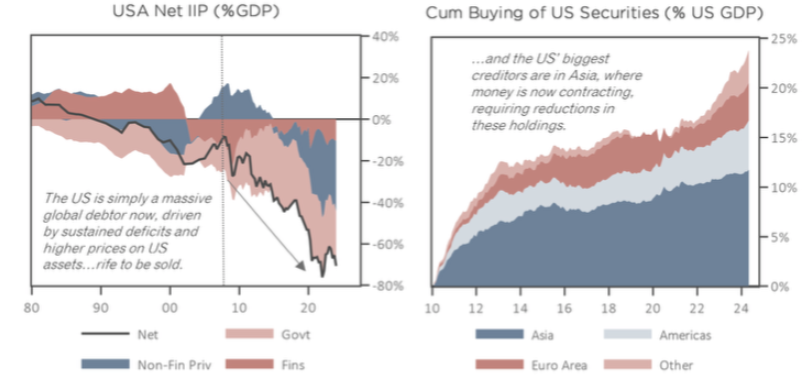

Asian Financial Crises v.2.0

Whitney Baker believes North Asian financials will buckle under the one-sided mismatches they’ve built up in US assets, with losses buried under the veneer of tech-geared equity gains. Liabilities are being contracted by policymakers’ own misguided attempts to defend currencies. Shrinking monetary bases force bond sales, crowding out stocks. Asian sales of US bonds add duration back to the US, aligning with a shallow American recession. Despite ongoing investment in infrastructure, the Fed will overreact with rapid rate cuts, causing a rotation out of US stocks into bonds. As Asians repatriate funds, the dollar weakens, triggering asset declines. Eventually, renewed Fed printing sets the stage for a stagflationary recession. Bottom line: in AFC v.2.0, the Asians are the creditors with too many foreign assets, while the US is the EM with too many foreign liabilities.

Edition: 190

- 12 July, 2024

Suspicious Overearners: Buckle (BKE), HCA Healthcare (HCA) & Owens & Minor (OMI)

Two Rivers’ model seeks companies that are potentially “over-earning” - defined as companies with unusually high margins relative to their own history or relative to the industry. Provides fertile hunting ground for shorts if the reasons for the margin increase are either unsustainable or fraudulent. The best short candidates include:

BKE - No sales growth pre-Covid. Gross margins have since risen from 40% to 48% and EBITDA margins from 14% to 25%.

HCA - Incremental gross margins have reached 40% vs. sub-20% GAAP. Trades at record high EV/S and EBITDA multiples.

OMI - Stock trades based on the continuation of very high margins. Insiders are suddenly and sharply selling off shares.

Edition: 116

- 06 August, 2021