Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Fully depreciated equipment in the Building Products industry

Industrials

Among the 19 companies analysed by BTN, those with the biggest risk of overstated earnings from using fully depreciated equipment or unusually long depreciation lives compared to the industry include Allegion, A.O. Smith, Insteel Industries, Trane Technologies and Masco. Meanwhile, they see Simpson Manufacturing, Advanced Drainage Systems, AAON, Trex and Builders FirstSource as being positioned to start seeing lower depreciation expense and capital spending. These companies are already years into modernisation and expanding their equipment bases. Their depreciation has risen and been a headwind to earnings of late, but they may be about to see this level off and put them in a position of rising margins and FCF.

Edition: 202

- 10 January, 2025

Building Product Distributors still offer plenty of upside

Industrials

Many market participants are looking for a way to play housing and it would be easy to look at building product distributors and write them off as being overvalued and that you’ve missed out. However, TRG believes this is faulty logic. Builders FirstSource, Beacon Roofing and GMS (as well as others) have margin profiles that have risen to comparable or superior levels in relation to the “premium-valued group” (SiteOne, Pool, Leslie's, Core & Main and Ferguson), but have EV/EBITDA multiples (avg. 10.6x) well below these stocks (avg. >20x). If they gain a more appropriate multiple (for strong SF starts and better margins) on higher EBITDA, then all three companies still offer significant (~70%) upside.

Edition: 183

- 05 April, 2024

Consumer Staples

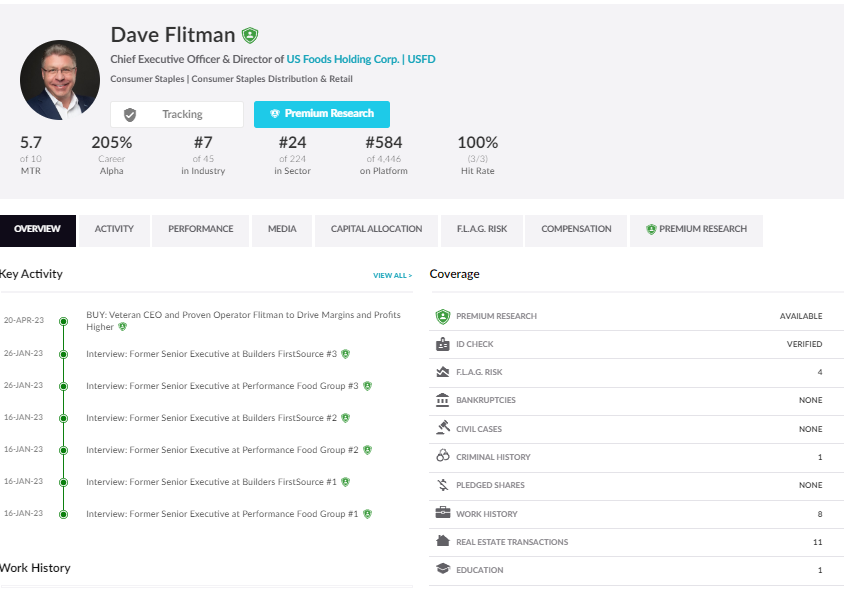

New CEO David Flitman to drive margins and profits higher - former colleagues interviewed by Paragon described Flitman as a strong operator who excels at driving costs out of businesses. He is a rigorous, data-driven, and profit-focused executive who quickly understands the largest levers to pull to improve performance at distribution businesses. He drove significant shareholder value at BMC and its merger partner Builders FirstSource where the combined stock performance of the two companies outperformed the S&P 500 more than two-fold.

Edition: 159

- 28 April, 2023