Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

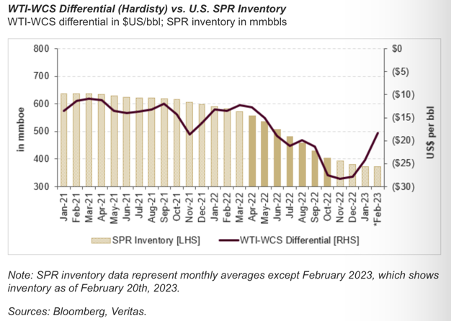

The narrowing of the WTI-WCS differential

Dan Fong highlights a recent and rapid narrowing of the WTI-WCS differential, which has generally positive implications for Canadian oil sands producers. Since bottoming out at ~USD$33/bbl last October, heavy differentials have narrowed to ~USD$18/bbl. This coincides with a pause in US Strategic Petroleum Reserve releases and the prospect of replenishment. In addition, with support from L3R and TMX, Canadian heavy has a line of sight into additional takeaway capacity and new markets. Price and spread volatility notwithstanding, these factors should be a net positive for WCS. Canadian Natural Resources and Imperial Oil have some of the highest cash flow sensitivity to differential changes.

Edition: 155

- 03 March, 2023

Canadian Oil Sands: Crack spread comedown

Energy

North American refiners had a banner year as demand for refined petroleum products surged and crack spreads hovered at record highs for most of 2022. However, we are starting to see signs of weakening demand and US crack spreads are already coming off their highs. In light of recent macro data points, Dan Fong lowers his crack spread assumption (to US$20/bbl from US$29/bbl) and updates his recommendations and valuations for Canadian Natural Resources (rated Buy), Suncor (Buy), Cenovus (Sell) and Imperial Oil (Reduce).

Edition: 152

- 20 January, 2023

Canadian Energy Stocks: Gushing Cash Flows

Energy

Canada's 'Final Four' large-cap integrated oil sands producers are set to generate significant cash flow - Canadian Natural Resources (Veritas' top pick), Suncor, Cenovus and Imperial Oil trade at a 20% 2022 FCF yield (assuming US$65 WTI). Even if management teams spend half of free cash on debt reduction, it will still leave plenty of room for some eye-popping shareholder yields (dividends + buybacks) ranging from 8.7% to 13.5%. Veritas’ report also outlines potential M&A that could result from recent climate policy initiatives.

Edition: 119

- 17 September, 2021

Canadian Oil & Gas

Even with recent OPEC+ news, Veritas Research expects the global oil market to remain undersupplied until 2021’s end, with a floor of $60 per barrel through 2022. With this low case, the setup for Buy Rated Oil Sands Producers is attractive, with Canadian Natural Resources, Cenovus and Suncor all attractive options (FCF Yields of >15% and Net Debt/FFO <1.0x).

Edition: 115

- 23 July, 2021