Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Lumber: Falling down

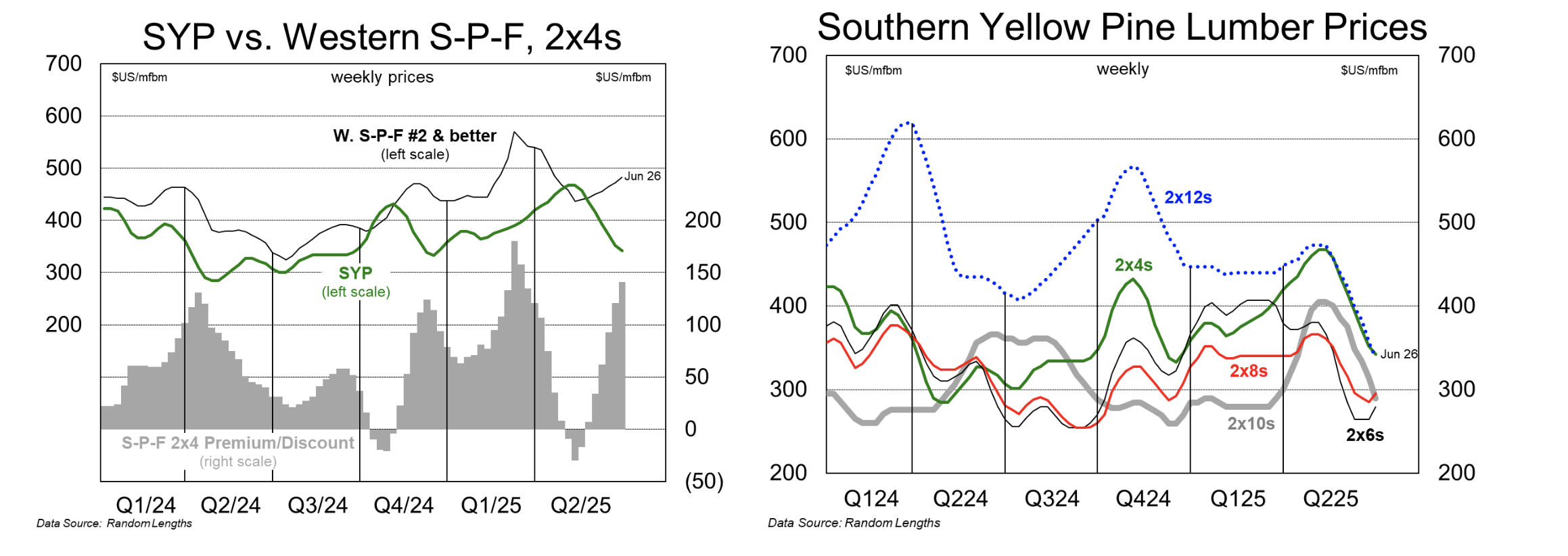

SYP lumber prices have been extremely weak in H1/2025, with 2x4 averaging $402 compared to S-P-F 2x4s averaging $479 (chart, left). Given these challenges, Canfor announced it will permanently close two mills. This may come as a surprise to some given the focus on trade woes and Canadian duties/tariffs, but the ERA team believe the move was sorely needed and sees future closures potentially following. SYP producers, as a whole, will benefit from marginally improved supply and demand balance over the near- to medium-term. However, with lumber demand expected to remain subdued through year-end and likely into 2026, further SYP mill capacity closures/downtime will be required before there is a sustained lift in SYP prices. The team continues to urge caution on Canadian lumber names given expectations for volatility related to the implementation of higher AR6 softwood lumber duties and a potential incremental tariff resulting from the ongoing Section 232 investigation.

Edition: 216

- 25 July, 2025

BC lumber producers facing it tough

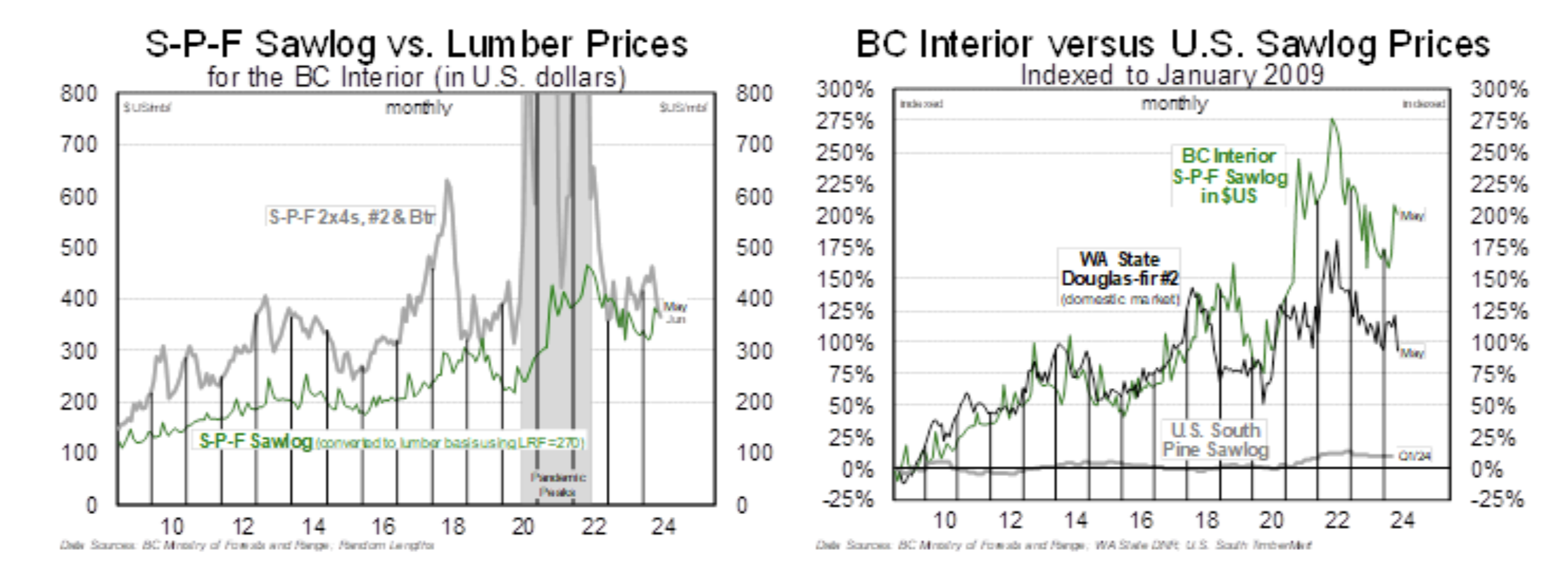

BC log costs are moving higher again (chart 1), and with S-P-F lumber prices rolling over—2x4 prices recently declined to $332—the ERA Forest Products team believe that the majority of BC sawmills are losing money today. Lumber prices are slumping across all species and dimensions, but log costs in BC are significantly higher (chart 2). More downtime is needed in all regions to remedy the issue. How to trade it? Most names will see limited further downside from current levels and upside catalysts remain elusive for now. The team do see long-term value in Canfor ($18 target price), Interfor ($22) and West Fraser ($116) but recommends that investors wait until at least Q4/2024 before building long positions.

Edition: 190

- 12 July, 2024

Softwood lumber duties set to move higher this summer

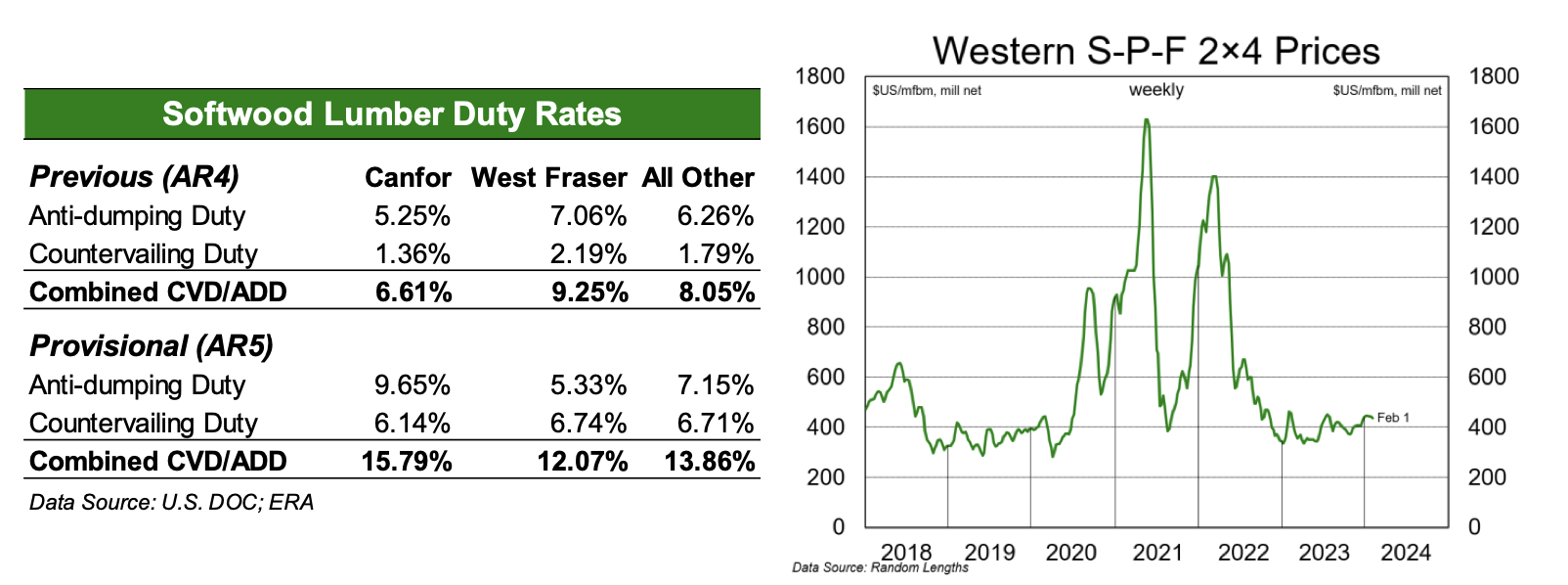

Preliminary results of the US Department of Commerce’s fifth administrative review into the 2022 North American lumber market sees an increase in combined duty rates, pointing to the potential for significant rate increases for next year’s review. Looking to 2023, S-P-F 2x4 prices averaged just $391 and spent most of the year near, or below, cash-cost levels; the ERA team expect that overall duties could increase sharply for the next review. So, who wins? US-based lumber mills (and perhaps Europeans exporting to the US) are the only winners as onerous softwood lumber duties increase Canadian producers’ costs. The release of the preliminary duties does not change ERA’s view on lumber equities, who sees upside from current levels for all lumber names given expectations for a sustained recovery in US housing. Interfor remains their top pick (target price $28), with West Fraser (TP: $116) and Canfor (TP $25) also seeing upside.

Edition: 179

- 09 February, 2024

Forest Products: Tough year ahead

Materials

The outlook for lumber / panel producers (Canfor, West Fraser, Boise Cascade, Louisiana-Pacific) is difficult, with no obvious upside catalyst before a recovery in US housing (unlikely before late 2023). ERA expects pulp prices to move lower through 1H23. Anticipated price declines are now almost fully priced into pulp names (Mercer, International Paper). In packaging, more pain lies in store for containerboard (Westrock) and a raft downtime will be needed to combat weaker demand and offset new capacity. Boxboard will outperform (Graphic Packaging, Clearwater Paper), with both demand and prices expected to remain robust.

Edition: 151

- 06 January, 2023