Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Can copper volumes meet big expectations?

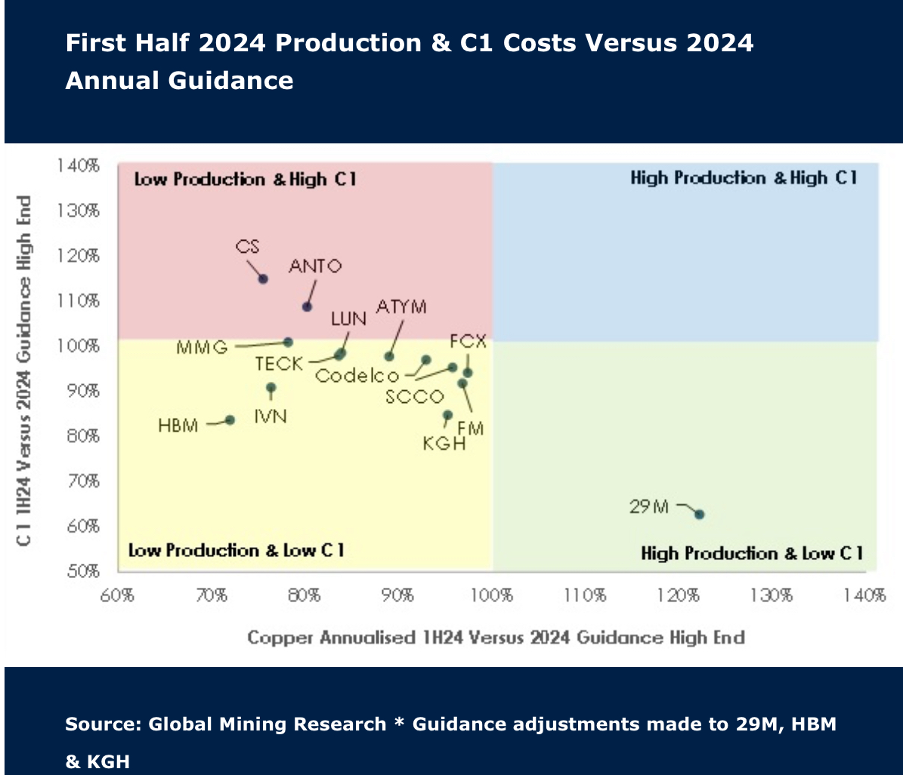

As expected, the first half of the year was met with weaker production, with companies in Global Mining Research’s coverage reporting flat figures of +1.5% and low capex. Costs increased some 4.8%, but this was offset by a ~US$0.60/lb increase in copper prices in the latest quarter. 60% of producers are expecting stronger H2 volumes, but Antofagasta, Ero Copper, Ivanhoe Mines and Capstone Copper are most at risk of missing 2024 guidance. Following the recent pullback and ahead of seasonally stronger Q4 prices, GMR continues to see the sector as attractive. Ratings have been raised for leveraged plays KGHM (to buy) and MMG (to hold).

Edition: 193

- 23 August, 2024

Copper: Risk to the downside

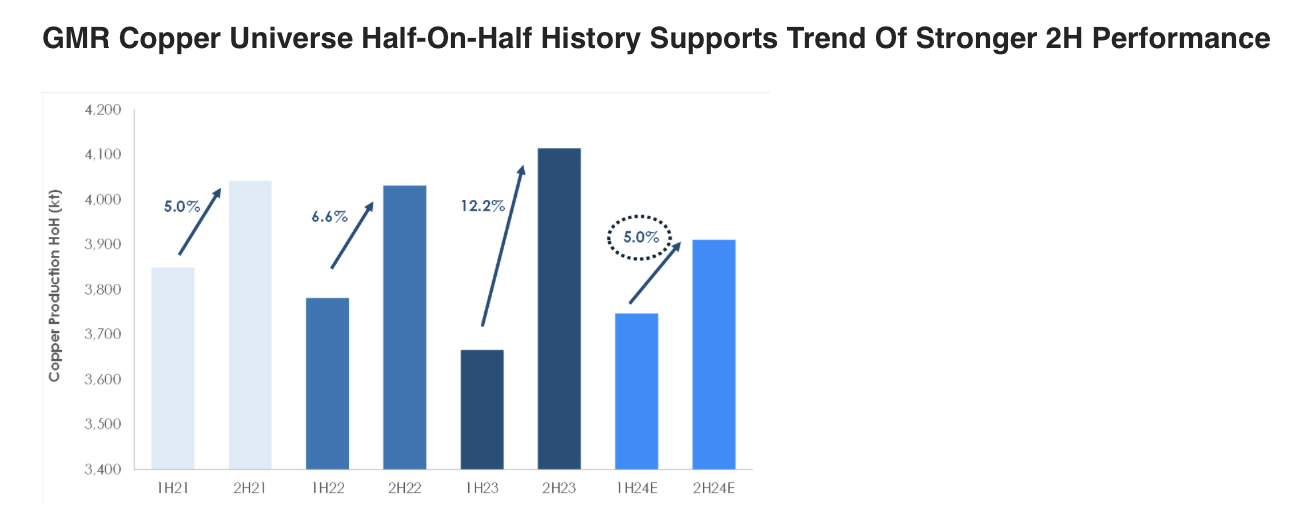

Copper prices had a strong start to the year. David Radclyffe’s review of the Q1/2024 performance versus 2024 guidance for the December year-end stocks helps put the market tightness into perspective. The key takeaway is that, as with gold companies, copper miners are banking on a strong H2/2024 to meet annual guidance figures. The risk is therefore to the downside, with once again copper producers struggling to either meet guidance or increase production appreciably. Only Hudbay Minerals, KGHM, Southern Copper, Freeport-McMoRan and First Quantum Minerals are tracking to 2024 production expectations. David’s preferred copper miners are in the small/mid-cap space on valuation grounds, including Atalaya Mining, Capstone Copper, Sandfire and Hudbay Minerals.

Edition: 187

- 31 May, 2024

Capstone Copper (CS CN) Canada

Materials

A copper growth story with significant optionality within the portfolio to >300kt/yr (vs. 164kt in 2023). After a period of heavy investment, FCF is set to turn positive in 2H24 with production from the Mantoverde sulphides project. The balance sheet is much stronger following the recent equity raising, with Net Debt/EBITDA forecast to fall from 3.8x in 2023 to 1.3x this year. However, near term cash flow is expected to be directed to mines, not the shareholders. CS offers an attractive risk / reward with its exposure to copper, scale, growth upside and a balance sheet expected to rapidly de-lever in the midterm. Growth studies in 2024 are likely to be near-term news catalysts.

Edition: 181

- 08 March, 2024

Sandfire Resources (SFR AU), Capstone Copper (CS CN) Canada

Materials

GMR’s two preferred junior copper names - in addition to offering growth at attractive valuations, their scale, longer mine lives and exploration upside also highlight potential corporate upside as industry peers seek to increase their exposure to copper and the EV materials thematic. The two miners are rapidly evolving businesses; a year ago they each had half the number of producing assets as they do in 2022. SFR is GMR’s cheapest copper stock. It trades at a P/NPV multiple of 0.5x and prospective FY24 FCF yield of 11%. At +200kt/yr from 2023 CS offers scale / leveraged exposure to copper.

Edition: 149

- 25 November, 2022