Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

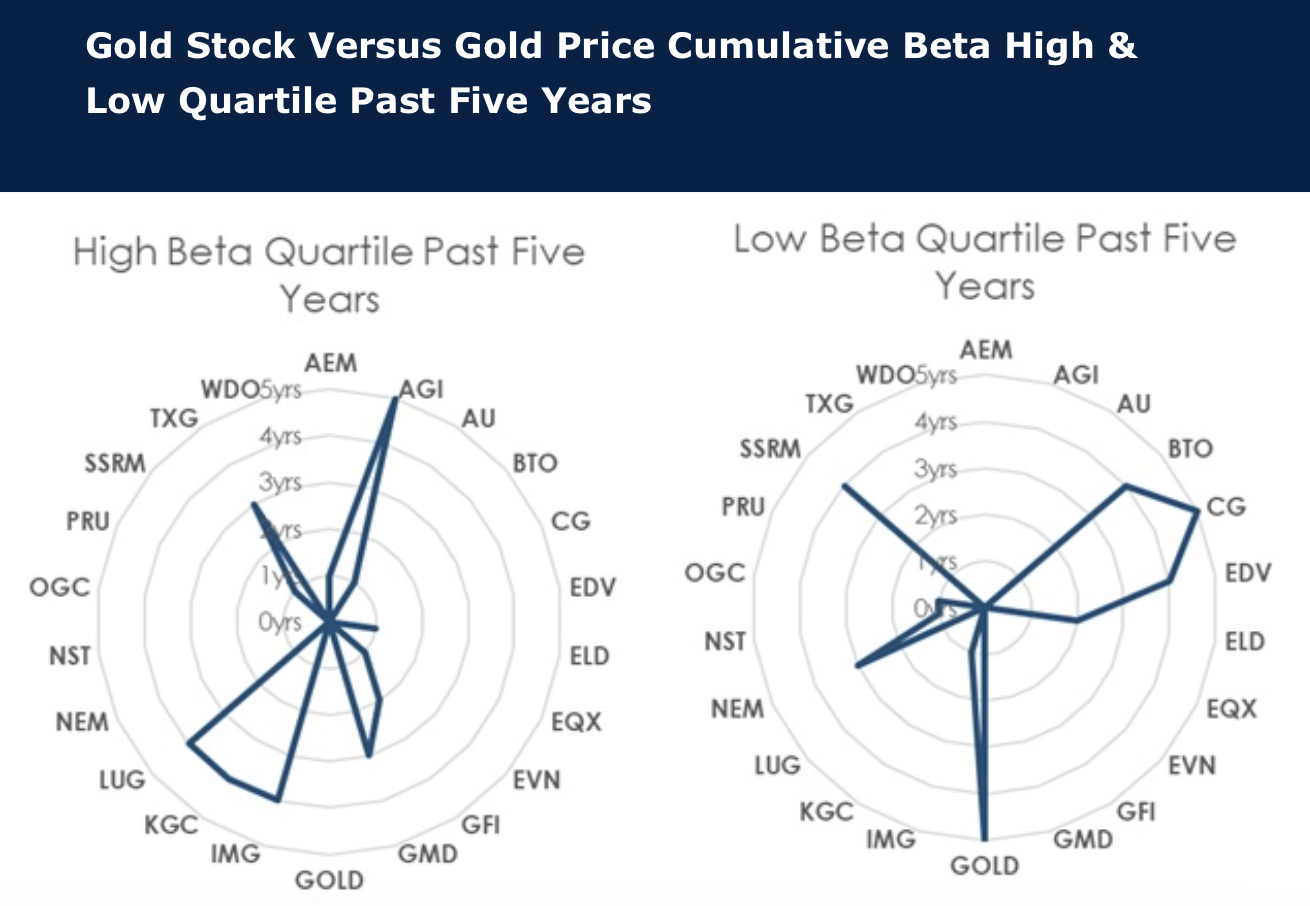

High beta gold stocks outperforming peers

The Global Mining Research team research the correlation of stocks to the gold price and the beta of those stocks. The stocks with consistently high beta to the gold price over the past five years are Alamos Gold, Genesis Minerals, IAMGOLD, Kinross Gold, Lundin Gold and Torex Gold Resources. Stocks with a weak beta to gold price over the past five years are B2Gold, Centerra Gold, Endeavour Mining, Barrick Gold, Newmont and SSR Mining (except 2025), each with mine or management issues, heightened risk or M&A troubles. Market preference for gold stocks appears to be more driven by investor perception rather than quantifiable valuation or sensitivity measures, and investors are preferring stocks with “issues” and aren’t seeking deeply discounted cheap stocks. Preferred gold stocks are BUY-rated Agnico (delivery and lower-risk portfolio), Kinross (risk reduction and execution), Equinox (transitions from project development to cash generation), IAMGOLD (Côté ramp up and derisking) and Lundin Gold (FDN continues to outperform).

Edition: 209

- 18 April, 2025

Gold: Can higher prices translate into cash?

All too often in the last decade for the gold sector, fully loaded costs have come close to equalling the received price. Therefore, one reason gold equities have likely recently lagged spot prices reflects a degree of market scepticism of the sector's ability to translate higher prices into “cash”. Unfortunately, the senior producers have often been key protagonists, but this isn’t the case for all gold stocks. Herein, David Radclyffe updates the sector cost analysis including highlighting Free Cash Flow (FCF) costs and FCF costs plus dividends, seeking to identify those stocks that could bank the proceeds of higher spot prices in 2024. The notional spot margin after base case dividends in 2024E for Agnico Eagle Mines / Barrick Gold Corp / Newmont is ~US$395/GEO, up from US$200/GEO in 2023. However, the best cash notional margins in 2024E could be delivered by Evolution Mining, Lundin Gold, Centerra Gold, and Barrick Gold Corp.

Edition: 186

- 17 May, 2024