Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Technology

Could the stock soar over 100%? KCR argues that CSCO isn’t just cheap vs. AI peers - it is cheap relative to the broader market, trading at roughly the same multiple as Kimberly-Clark despite far stronger growth. Networking product orders have risen 10% Y/Y for 4 consecutive quarters, suggesting investor concerns about a slowdown are unwarranted. Meanwhile, the company’s rapidly growing exposure to AI infrastructure products and shift towards subscription-based revenue both support multiple expansion. CSCO trades at one-third of Arista Networks’ P/E multiple and one-quarter of its EV-to-revenue ratio - even a modest narrowing of the valuation gap would translate into substantial gains for CSCO shares. Finally, a ~5% FCF yield is far too high for a company of CSCO’s quality.

Edition: 222

- 17 October, 2025

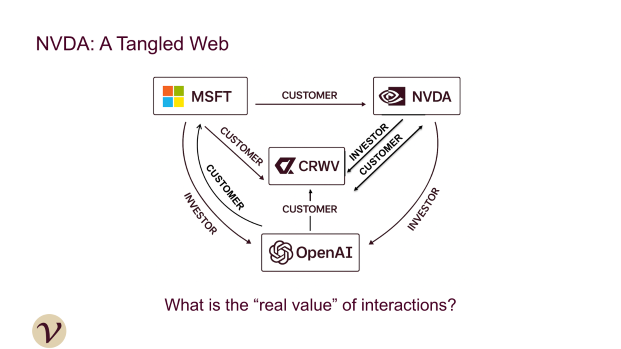

Nvidia's circular financing

Technology

Veritas has been flagging NVDA’s customer financing activities well before they hit the headlines: in 2023, they first highlighted the issue in “Nvidia & The Tech Sector's Circular Cash Flows” and reiterated their concerns earlier this year in “Nvidia’s CoreWeave - A Familiar Story”. Following the Oracle/OpenAI deal, the sell side is now echoing Veritas’ warnings, drawing parallels to the dotcom bubble, when Nortel, Lucent and Cisco extended credit to customers to enable their internet infrastructure buildout. Veritas does not expect this risk to be priced into NVDA's stock until revenue growth slows. If investors doubt customers can generate returns on their chip investments, these large negative cash flow purchases will not be well received.

Edition: 221

- 03 October, 2025

Outside of AI, why invest in the US?

US equities remain the world’s most important market, but passive benchmarks are distorted by AI concentration risk. Durable alpha lies in structural themes beyond AI. Power infrastructure (Constellation, Duke, NextEra) will benefit from grid bottlenecks as data centres drive demand. Re-industrialisation (Caterpillar, Honeywell, Rockwell) reflects reshoring and automation. The energy transition (Dominion, Enphase, ExxonMobil) requires trillions in capex. Housing scarcity (D.R. Horton, Home Depot, Lennar) is a structural imbalance. Healthcare innovation (Abbott, Eli Lilly, UnitedHealth) rides longevity and med-tech advances. Cybersecurity (Cisco, CrowdStrike, Palo Alto) is non-discretionary. Generational wealth transfer (BlackRock, Morgan Stanley, Schwab) reshapes capital flows. The AI productivity super-cycle is real, but thematic allocations across these shifts offer broader, smarter US exposure.

Edition: 220

- 19 September, 2025

Channel Chatter: Regional Security VAR, ESX Conference, BEAD

Technology

SPR’s recent channel conversations highlight growing traction for emerging vendors like Onum and Cribl, which optimise SIEM data flow and reduce Splunk renewal costs. CrowdStrike remains a standout with strong SIEM growth and aggressive sales execution, though channel favouritism limits broader access. Cloudflare, despite a strong product, struggles with channel inefficiencies, while Fortinet is gaining share in select regions but not winning new logos with Lacework. Cisco’s security momentum may be challenged by the departure of Gary Steele. Meanwhile, BEAD funding delays and policy shifts are hurting traditional fibre and “turf” vendors, as fixed wireless and satellite gain favour. At ESX, Napco remains a solid player, but growth has normalised post-3G sunset.

Edition: 215

- 11 July, 2025

Tech: AI innovations, market disruptions and emerging opportunities

Technology

The themes SPR will be focusing on in 2025 include 1) AI related: (a) AI applications move to the edge - benefitting the likes of Ciena, Arista and Crown Castle. (b) AI networking transition to ethernet vs. InfiniBand, benefitting Arista, Cisco, Juniper and Extreme. (c) AI use cases that are delivering strong ROI vs. others that are not, despite strong sales efforts by vendors - impacting renewals for Salesforce, ServiceNow, and others. 2) In cyber security, areas of growing priority include SOC automation and Next Generation SIEM. 3) More vendors bypass distribution and sell via the CSP marketplace or direct, negatively impacting large distributors. 4) BEAD - despite delays, this program will drive meaningful revenue. 5) Vendors benefitting from the rapid growth in DevOps / DevSecOp.

Edition: 202

- 10 January, 2025

Technology

Overall trends for 1Q25 are weaker Y/Y, according to Verbatim’s latest channel survey. The majority of respondents reported that they are not meeting their internal goals, while their sales activity for PANW is also below their expectations. Price sensitivity, delayed projects, negative market environment, and competition from Fortinet and Cisco are the major headwinds for the current period. The average sales cycle is either the same or slightly longer (ranges between 4-18 months). Deal sizes are mostly either flat or up Y/Y. A North American system integrator also mentions that new product launches are having no impact on overall sales.

Edition: 199

- 15 November, 2024

IT Spending: Sentiment weaker than last quarter

Technology

SPR’s latest channel checks reveal disappointment that the second half pick up that many expected has not materialised. Stock specific feedback includes: ServiceNow - all very positive - probably the strongest indications for any vendor. Crowdstrike channels and end users see the vendor moving quickly past its recent crash. SPR has picked up mixed feedback re. Fortinet’s recent security breach and whether it negatively impacted Sept Qtr end deal flow. Outside of security, the vendors seeing an increase in positive comments include IBM, Oracle, Microsoft, Arista and Juniper/Mist. It has been easy to pick up comments on share loss by Cisco.

Edition: 197

- 18 October, 2024

Technology

While it is not unusual to hear of CSCO reorganising at the end of its FY, channel chatter is that the upcoming changes are fairly major. CSCO has been one of the companies that SPR hears of replacing senior employees with younger, lower paid staff. Indications are that the only teams that are preforming well are those selling to the public sector. Expectations are low so much of this weakness is baked in, but if investors are expecting signs of improvement, that is not what channels are reporting.

Edition: 192

- 09 August, 2024

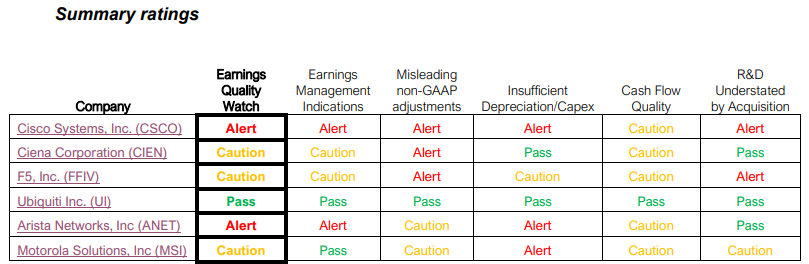

Communications Equipment: Earnings quality review

Communications

BTN’s Earnings Quality Watch industry reports provide readers with a quick way to identify the companies that are the most and least exposed to the risk of reporting disappointing results or guidance due to recent results being distorted by unrealistic, accounting-related benefits. Looking at the table above, only Ubiquiti received a ‘Pass’ rating in the Communications Equipment industry, while BTN sees meaningful risk that Arista Networks and Cisco Systems will disappoint on earnings in the next 2 quarters.

Edition: 190

- 12 July, 2024

Technology

Sales Pulse continue to pick up more positive views of the tailwinds for Nutanix and examples of deals that are driven by Broadcom’s acquisition of VMware however, channels are quick to state that the move from VMware is challenging, at least for large users. In Nutanix upcoming report we expect to see more evidence of growth from the Broadcom/VMware acquisition as well as the other catalyst that we have discussed in recent notes (increase in partnerships including Cisco, Dell and additional VARs), but rapid acceleration seems unlikely. Many speakers at Nutanix’ Next Conference in Barcelona discussed their move from VMware to Nutanix.

Edition: 188

- 14 June, 2024

Connectivity, speed & scale combine to blow up IT as we know it

Technology

In John Harrington’s latest Tech Trends report, he looks at several factors that have combined to change IT development and sales dynamics. These include how the accelerating deployment of speedier wired and wireless connectivity to the cloud, very fast computing platforms being built at scale within the clouds, the accelerating development of quantum computing as a viable commercial business, and the development of serious AI capabilities are affecting the global digital landscape. As IT increasingly transitions from in-house networking to the cloud, some new areas of IT will benefit, while others face an uncertain future.

Positive: Advanced Micro Devices, Alphabet, Apple, Amazon, Broadcom, Ciena, Dycom, Intel, IonQ, Microsoft, Nvidia, Rigetti.

Negative: C3.ai, Cisco, Dell, Qualcomm, Salesforce.

Edition: 162

- 09 June, 2023

Advanced AI: Sink or swim time for cybersecurity vendors

Technology

How are AI advancements and hype affecting the cybersecurity industry? What are data security vendors doing with AI/ML and cybersecurity automation, and can they protect their market from the major cloud operators with their investments in AI-driven security for their own platforms? During the interviews conducted by Blueshift, industry sources were also asked how they would play the sector near to mid-term and out over time. Companies discussed include Amazon, CrowdStrike, Cisco, CyberArk, Fortinet, Google, IBM, Microsoft, Okta, Palo Alto and Zscaler.

Edition: 158

- 14 April, 2023

Technology

Earnings beat expectations and Next-Gen security ARR surpasses $2bn for the first time, in what Srini Nandury describes as a “stunning achievement” - PANW continues to see strong demand as security remains the most resilient of IT budget priorities within the enterprise and the group now possesses arguably the broadest offering in the industry. Srini expects Cisco will continue to cede share to PANW (as it has been doing for the last several quarters). The stock trades at 5.3x EV/C2024 sales vs. peer avg. of 5.0x, but a premium multiple is warranted. Srini's $200 TP translates to 6.7x EV/C2024 sales of ~$9bn.

Edition: 149

- 25 November, 2022

Giant layoffs loom as Tech firms face customer budget freezes

Blueshift’s IT sector sources are pointing at Oracle’s plan to cut c.30k jobs as the crack in the dam that is going to trigger a resizing of workforces across all of tech - as one recruitment executive said, “They have literally been making up jobs for the past several years to beat each other to talent. It had nothing to do with rightsizing. It was a competition to impress investors.” Sources were unanimous that earnings forecasts for the rest of the year across most vendors in all verticals of DIY enterprise networking are going to be poor. Companies covered include Arista Networks, Cisco, CrowdStrike, Dell, Fortinet, IBM, Palo Alto and Zscaler.

Edition: 140

- 22 July, 2022

Technology

New CEO Rick McConnell will profitably scale DT to a multi-billion dollar company - former colleagues describe McConnell as the perfect fit for the job because of his industry expertise and track record scaling businesses (Akamai and Cisco). Well versed in finance, product and go-to-market strategy, he will grow DT's business from $1bn to $5bn+. Unlike many of its high-valuation software peers, DT’s valuation reflects sustainable 30% revenue growth, 25% EBIT margins and strong >30% FCF margins. Forecasts EPS to increase 44%-65% from FY22-FY24, materially ahead of current estimates.

Edition: 133

- 14 April, 2022

Arista (ANET), Juniper (JNPR) & Cisco (CSCO)

Technology

While checks on product and sales execution have been steadily improving for JNPR and ANET, they are declining for CSCO. Sales Pulse believe that investors who are looking for any improvement for CSCO are going to be disappointed. While ANET's stronger performance may be expected, JNPR's appears less well known.

Edition: 115

- 23 July, 2021

Lack of customer expertise hurts Enterprise IT sales

Technology

Blueshift primary research finds the effectiveness of cloud-based applications is swiftly diminishing the need to retain in-house IT staff, leaving a dwindling pool of experienced workers clinging to familiar last-generation technologies, instead of staying current on newer IT capabilities. Hence, enterprise technology sales are likely to miss a hoped for rebound in H2 to the direct benefit of the public cloud operators. Positive: Amazon, Datadog, Microsoft. Negative: Cisco, IBM, Snowflake.

Edition: 111

- 28 May, 2021