Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Technology

Could the stock soar over 100%? KCR argues that CSCO isn’t just cheap vs. AI peers - it is cheap relative to the broader market, trading at roughly the same multiple as Kimberly-Clark despite far stronger growth. Networking product orders have risen 10% Y/Y for 4 consecutive quarters, suggesting investor concerns about a slowdown are unwarranted. Meanwhile, the company’s rapidly growing exposure to AI infrastructure products and shift towards subscription-based revenue both support multiple expansion. CSCO trades at one-third of Arista Networks’ P/E multiple and one-quarter of its EV-to-revenue ratio - even a modest narrowing of the valuation gap would translate into substantial gains for CSCO shares. Finally, a ~5% FCF yield is far too high for a company of CSCO’s quality.

Edition: 222

- 17 October, 2025

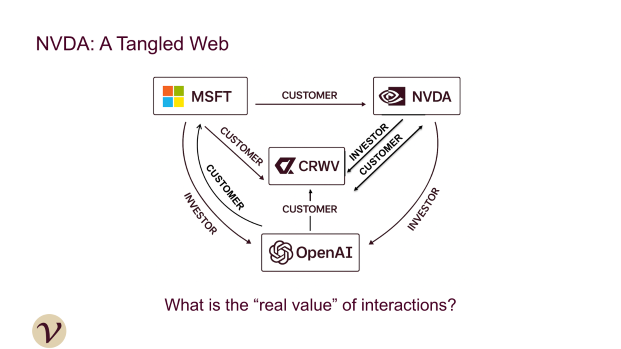

Nvidia's circular financing

Technology

Veritas has been flagging NVDA’s customer financing activities well before they hit the headlines: in 2023, they first highlighted the issue in “Nvidia & The Tech Sector's Circular Cash Flows” and reiterated their concerns earlier this year in “Nvidia’s CoreWeave - A Familiar Story”. Following the Oracle/OpenAI deal, the sell side is now echoing Veritas’ warnings, drawing parallels to the dotcom bubble, when Nortel, Lucent and Cisco extended credit to customers to enable their internet infrastructure buildout. Veritas does not expect this risk to be priced into NVDA's stock until revenue growth slows. If investors doubt customers can generate returns on their chip investments, these large negative cash flow purchases will not be well received.

Edition: 221

- 03 October, 2025

Outside of AI, why invest in the US?

US equities remain the world’s most important market, but passive benchmarks are distorted by AI concentration risk. Durable alpha lies in structural themes beyond AI. Power infrastructure (Constellation, Duke, NextEra) will benefit from grid bottlenecks as data centres drive demand. Re-industrialisation (Caterpillar, Honeywell, Rockwell) reflects reshoring and automation. The energy transition (Dominion, Enphase, ExxonMobil) requires trillions in capex. Housing scarcity (D.R. Horton, Home Depot, Lennar) is a structural imbalance. Healthcare innovation (Abbott, Eli Lilly, UnitedHealth) rides longevity and med-tech advances. Cybersecurity (Cisco, CrowdStrike, Palo Alto) is non-discretionary. Generational wealth transfer (BlackRock, Morgan Stanley, Schwab) reshapes capital flows. The AI productivity super-cycle is real, but thematic allocations across these shifts offer broader, smarter US exposure.

Edition: 220

- 19 September, 2025

Channel Chatter: Regional Security VAR, ESX Conference, BEAD

Technology

SPR’s recent channel conversations highlight growing traction for emerging vendors like Onum and Cribl, which optimise SIEM data flow and reduce Splunk renewal costs. CrowdStrike remains a standout with strong SIEM growth and aggressive sales execution, though channel favouritism limits broader access. Cloudflare, despite a strong product, struggles with channel inefficiencies, while Fortinet is gaining share in select regions but not winning new logos with Lacework. Cisco’s security momentum may be challenged by the departure of Gary Steele. Meanwhile, BEAD funding delays and policy shifts are hurting traditional fibre and “turf” vendors, as fixed wireless and satellite gain favour. At ESX, Napco remains a solid player, but growth has normalised post-3G sunset.

Edition: 215

- 11 July, 2025

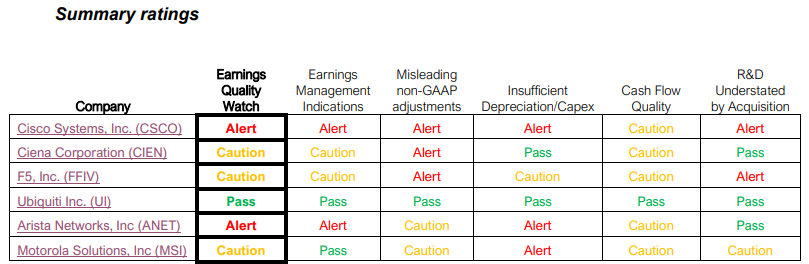

Communications Equipment: Earnings quality review

Communications

BTN’s Earnings Quality Watch industry reports provide readers with a quick way to identify the companies that are the most and least exposed to the risk of reporting disappointing results or guidance due to recent results being distorted by unrealistic, accounting-related benefits. Looking at the table above, only Ubiquiti received a ‘Pass’ rating in the Communications Equipment industry, while BTN sees meaningful risk that Arista Networks and Cisco Systems will disappoint on earnings in the next 2 quarters.

Edition: 190

- 12 July, 2024