Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

MSCI emerging markets pullback in process

The EEM-US broke below its 20-day MA for the first time in over three months. Any potential pullback to major base support ($46) should be considered a buying opportunity. As discussed in Vermilion’s weekly Int’l Compass reports, EM countries that they are overweight include South Korea and Greece. Additionally, there continues to be several other countries that are bullish and/or worthy of overweights, including South Africa, Taiwan, Hungary, Czech Republic, Poland, Vietnam, UAE and Pakistan. Turning to China, the Shanghai Composite displays a significant base breakout, and China has been a favourite country to add exposure to over the past month (July 3 Int’l Compass titled “China and Japan Breaking Out” and also July 22 Int’l Macro Vision). As long as base support holds on this pullback, David Nicoski remains bullish and he is monitoring China for a potential upgrade to overweight.

Edition: 217

- 08 August, 2025

The warning sign in US labour

The latest Non-Farm Payroll report showed the US keeps adding jobs at a sustained pace, but Alfonso Peccatiello says this feels weird. It’s hard to square how the US job market can remain so resilient even as rates remain high for long. One of the most reliable long-term indicators of job market weakness is the Sahm Rule: when the 3-month moving average of the unemployment rate exceeds its 12-month low by 0.5%, the recession is here. The latest reading says 0.37%, often cited by bears as a warning sign. If the underlying labour market weakness gets more evident, the Fed needs to react fast. From a long-term asset allocation perspective, one can still remain invested in risk assets here but must be vigilant of surfacing labour market weakness and the Fed reaction function. If they play ball, buying bonds when 10-year Treasuries approach 4.6-4.7% offers great risk/reward.

Edition: 188

- 14 June, 2024

Compass (CPG LN) & BAE Systems (BA/ LN)

Consumer Discretionary / Industrials

Willis Welby looks at UK growth names (>$2.5bn M/Cap) that have not shared in the share price rises since Oct 26th. CPG has seen analyst downgrades despite a robust update during Nov, but looks like a very strong compounding story that is not expensive and makes great sense at current prices. However, it is BAE that really stands out. The defence contractor has seen upgrades to consensus Y2 EBIT over the last three months and more recently has announced more good news on orders. Relative to US peers that implied to Y3 EBITM ratio of <60 looks way too low. Other stocks discussed in their report include AstraZeneca and Games Workshop.

Edition: 176

- 22 December, 2023

Residential Real Estate: A deep dive into various cases plaguing the industry, buyside exposure and much more

Real Estate

Gordon Haskett Research Advisors

GHRA 1) Examines the two most pressing class action lawsuits facing the industry (Sitzer/Burnett & Moehrl), which will likely determine the fate of secondary cases. 2) Explores the dynamics of eight other class action lawsuits across the US. 3) Compiles buyside exposure across a half dozen companies. 4) Runs sensitivity analyses to illustrate how topline challenges could impact EBITDA for Compass, Redfin and Zillow. 5) Analyses commentary from more than a dozen management teams to provide investors an in-depth view into how the US residential real estate industry is grappling with what could be the biggest regulatory-induced business model change GHRA has come across.

Edition: 175

- 08 December, 2023

Three emerging markets to own

Alfonso Peccatiello claims the EM complex is under-owned and is overall a cheap and sensible exposure to have. Looking through a long list of countries, he has created a shortlist of three darling EMs to own. First comes Malaysia, a net commodity exporter with a new government keen on structural reforms, and an equity market that trades at an acceptable 15.0 forward P/E. It will benefit from global supply chains shifting away from China, as will Indonesia, Alsonso’s next choice. The recent banning of unprocessed export nickel shows how Indonesia could attract investments going forward, and the market trades at a 13.5 forward P/E. Last but definitely not least is Poland, which is a productive economy that has beaten most of its European peers in per capita GDP growth, has a new government headed by ex-European Council President Donald Tusk, and has an equity market trading at a meagre 8.0 forward P/E!

Edition: 175

- 08 December, 2023

How do you make money in markets with a directional view?

Alfonso Peccatiellio is of the view there are two main ways to achieve this sought-after outcome: 1) Your view is NOT consensus, and you express it through the right asset (no proxy trading); 2) Your view IS consensus, but you still pick an undervalued asset to squeeze the remaining juice left. Soft landing is now consensus. If you want to bet against it there are plenty of cheap ways to do that: equity put options are not particularly expensive, and if you think inflation accelerates you can sell bonds pricing in 100+ bps of cuts for next year or buy crude oil which has been slaughtered. If you want a really contrarian way to express the soft landing idea, look at Chinese tech stocks.

Edition: 174

- 24 November, 2023

The Psychedelic Revolution

Healthcare

The potential of using psychedelics for therapeutic benefit has taken several steps forward recently. The FDA is getting closer to issuing specific guidance and guidelines for the use of psychedelic drugs to treat mental illnesses - notably for depression and PTSD - as well as for addictions and for use in clinical trials. Psychedelics are gaining cultural awareness and acceptance, with two US states (Oregon and Colorado) legalising controlled uses. Investors are taking notice. By last year, more than 50 psychedelics companies, including Compass Pathways and ATAI Life Sciences, had gone public at a combined valuation of over $2bn.

Edition: 167

- 18 August, 2023

Short Shots

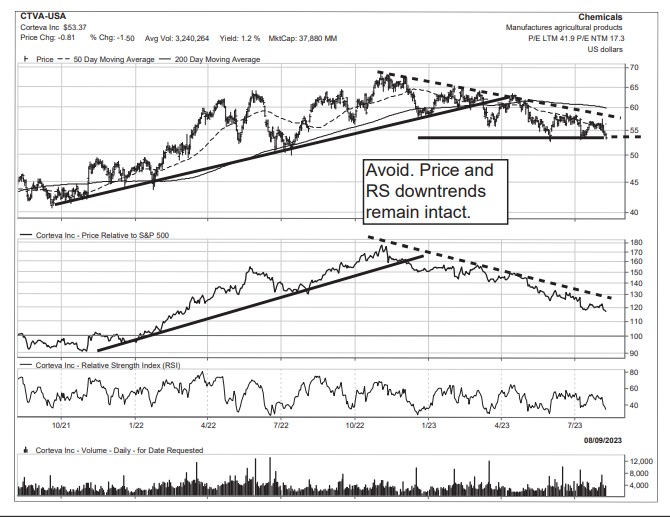

Is a collection of technically vulnerable charts culled from the “Negatively Inflecting” and “Toppy” columns within Vermilion’s Weekly Compass report or from various technical screening processes. The charts contained in this report have developed concerning technical patterns that suggest further price deterioration is likely. For these reasons Short Shots can also be a great source of ideas for investors interested in short-selling candidates.

Charts highlighted include Corteva (see above), Enphase Energy, General Mills, Kraft Heinz, Hershey, MarketAxess, Moderna, Newmont, Penumbra, Roblox, SolarEdge and Valmont Industries.

Edition: 167

- 18 August, 2023

The liquidity illusion

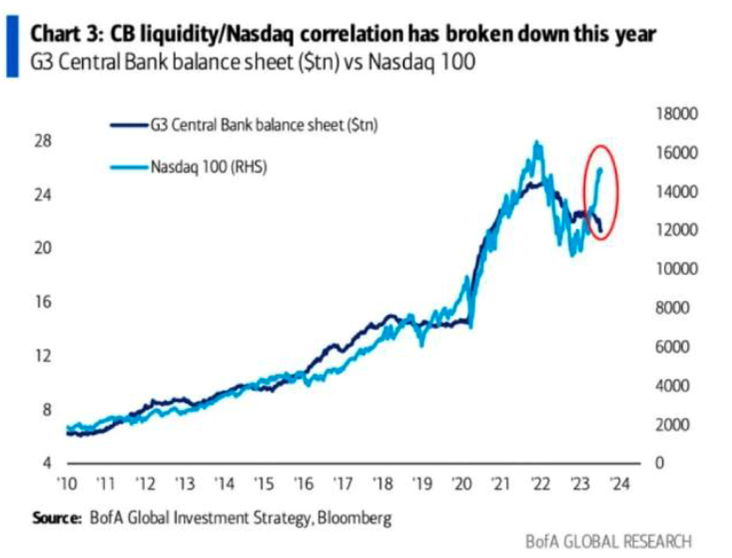

One of the most popular but misleading charts in macro. Many believe the Fed “pumping money” into the system leads to equity markets going up, but that’s not how it works. Bank reserves operate in a closed system that never reaches the private sector. Some people point to the portfolio rebalancing effect to explain the relationship, but even then, we only see second-order effects, reliant on underlying economic fundamentals. A simple linear regression analysis shows that in the last 15 years, US liquidity only explained 3-4% of the variation of SPX returns!

Edition: 166

- 04 August, 2023

Finally emerging?

Selected emerging markets are having a great year, with equity markets like Poland and Mexico already up 25-30% YTD. EM currencies have been broadly appreciating against the USD. The macro context generally required for a sustained EM rally includes disinflationary, below-trend growth in the US with a weak USD benefitting the EM space, and strong global demand and trade growth. We have a lot of the first scenario and a little bit of the second. The team are currently LONG Poland and Latin America, mainly Brazil with its promising growth story.

Edition: 165

- 21 July, 2023

Consumer Discretionary

Compass Restaurant Consulting & Research

One of the standout performers in Steve Crichlow’s latest Restaurant Industry Pulse Report - the burger giant enjoyed a strong performance in the US during Nov which has continued into Dec driven by an exceptionally successful marketing campaign of running multiple promotions simultaneously and all being profitable (something it has been unable to achieve since 2012). 82% of contacts interviewed stated they were pleased with the recent shifts in promotional focus. Steve now expects Dec SSS to be at the top end of his current estimates of 5-7%.

Edition: 150

- 09 December, 2022

UK growth stocks

One easy response for equity investors faced with such a radical change in the backdrop for equity pricing this year is to assume that growth stocks can get further derated. Willis Welby, who use expectations analysis to help decode share prices, differentiates between duration stocks which require a transformation in business models and growth stocks which do not. They draw particular attention to IHG, Burberry, Compass, Sage, Auto Trader and Experian. Notable absentees from their analysis are the industrial fan club stocks of Croda, Halma and Spirax which did not make their consensus Y3 revenue growth criteria.

Edition: 147

- 28 October, 2022

Consumer Discretionary

Compass Restaurant Consulting & Research

Stands out for the wrong reasons in Steve Crichlow’s monthly Restaurant Industry Pulse Report - August sales were negative and momentum decreased due to a failure to offer promotional items that would resonate with consumers (2 for $6.99 promotion is very good but the ads are confusing. The new Oven Baked Pastas, while good in theory, according to customers the taste and presentation made them unappealing). For September, SSS expectations are in the negative 4-2% range based on current momentum and failure of the relaunched Detroit Pizza promotion. Additionally, Pizza Hut gave up its sponsorship to the NFL and will suffer from this all season.

Edition: 144

- 16 September, 2022

Chipotle (CMG), McDonald's (MCD), Domino's (DPZ)

Consumer Discretionary

Compass Restaurant Consulting & Research

CMG - Can sustain current SSS trends (June est. +8-10%); growing positive traffic trends (one of the only concepts doing so) coupled with little to no resistance to price increases. The new Pollo Asado is one of the most successful promotions in a long time.

MCD - Dominating the price / value messaging and taking market share from peers. June SSS expectations are +2-4%. Top sales drivers: 2 for $6, Nugget Bundles, Off Premise sales. On the negative side, most franchisees unhappy with the new PACE Store Visitation Program.

DPZ - Declining momentum. June SSS expectations are in the negative 3-1% range. Driver shortages not only impacting sales and market share, but also brand credibility; not easily fixed.

Edition: 137

- 10 June, 2022