Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Consumer Discretionary

A story riddled with risk - Brian McGough argues DKS is priced for perfection despite mounting structural and cyclical headwinds. Core growth is tapped out and the House of Sport concept – its only unit growth driver - is not working; comping down 20% in year 2 and down again in year 3. Inventory issues, including a Critical Audit Matter on carrying value, and gross margin risks from tariffs on private-label apparel add further pressure. Apparel (40% of sales) has turned deflationary and the Foot Locker merger is seen as immediately margin-destructive, with no strategic merits and likely to strengthen competitors such as Academy and JD Sports. Brian is incrementally of the view that the 5-year CAGR for athletic footwear in the US is -300bp below pandemic-era trends and warns that at 10x EBITDA, a historical peak, DKS is over-owned, over-earning and due for a correction.

Edition: 223

- 31 October, 2025

Consumer Discretionary

The Retail Tracker notes continued improvement in URBN’s product assortments, describing the current offering as focused, confident and well-positioned for the holidays with stronger gifting and better alignment to its customer. New leadership is credited with sharper merchandising and more responsive assortments visible across stores, online and social media. Anthropologie and Free People remain strong, attracting younger shoppers while maintaining core customers, with standout accessories, home and active lines. Nuuly, the rental platform, continues to expand rapidly, offering tariff resilience and appealing to younger, price-sensitive consumers. The Retail Tracker has been positive on the name since early in the year and remains so.

Edition: 223

- 31 October, 2025

Eurozone: Consensus too optimistic on disinflation

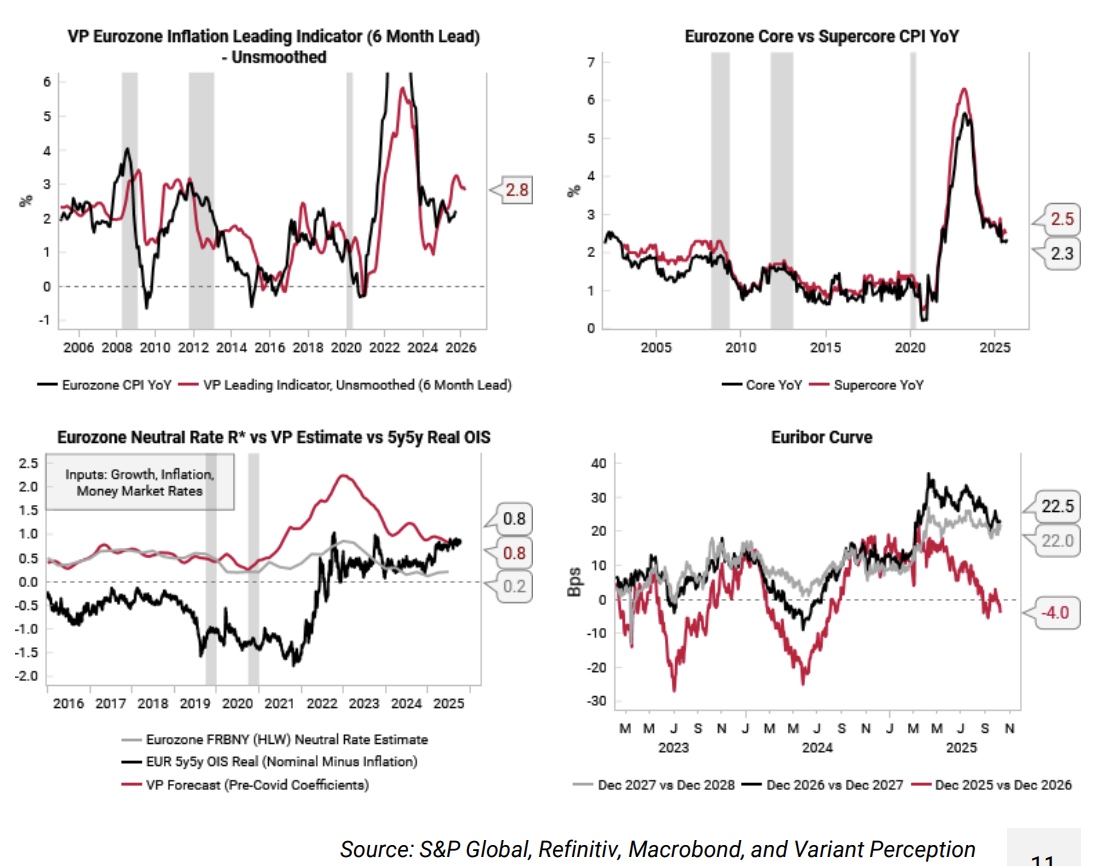

Consensus expectations see 2026 eurozone headline CPI at 1.8% and core CPI at 2%. The Variant Perception team suspects that inflation risks are tilted to the upside from here given the recovery in their eurozone growth leading indicators and the ECB rate cuts so far this year. Their main inflation leading indicator is rolling over from a high level, but the point estimate remains elevated at 2.8% (top left chart). Core and supercore CPI have also been slower to fall, still at 2.3 to 2.5% YoY (top right). The team put the real neutral rate (R*) for the eurozone at 0.8%, which is also where the 5y5y EUR real OIS is trading (bottom left). With headline CPI at 2%, there is good chance that ECB policy is already stimulatory, potentially creating inflation upside in 2026. The team take profits on their SOFR vs Euribor Dec 25/26 convergence trade established last month.

Edition: 222

- 17 October, 2025

Deutsche Boerse integrates social media intelligence in market surveillance software

While Deutsche Boerse has been an early adopter of social media monitoring for years, they have now taken the critical step of integrating Stockpulse's social analytics directly into their core Scila surveillance system. This integration provides comprehensive monitoring of 70,000+ global equities and cryptocurrencies with real-time social sentiment analysis, buzz metrics and seamless workflow integration within their mission-critical market oversight platform. This signals a broader trend toward holistic market surveillance encompassing trading data, news feeds and social sentiment. As social media increasingly shapes market dynamics, similar integrations are likely to follow globally. For investors, Stockpulse's insights into social sentiment, help spot emerging risks and opportunities before they hit the market. Contact us for a free trial / demo.

Edition: 221

- 03 October, 2025

China: The illusion of growth in China’s trust sector

Given the extreme financial stress in China, some may be surprised by the near record y/y growth in trust AUM to RMB29.6trn in 2024. However, Jonathan Anderson points out that nearly all of the growth came from passive products; true investment and financing trust AUM were essentially flat. Over a third of trust companies are technically insolvent or on the brink, and Jonathan doubts their long-term viability. Looking at the core active trust products, one will see them weighed down by unresolved defaults in the real estate and local government financial vehicle sectors, with freeze clauses on repayments placing a lot of active AUM into limbo. The impending collapse of many companies in the sector is unlikely to be a catalyst for broader financial contagion, but Jonathan mentions that its loss as a credit channel will still have wide implications.

Edition: 220

- 19 September, 2025

Galderma (GALD SW) Switzerland

Healthcare

While GALD shares have performed well since the company’s IPO, the stock remains in a "discovery phase", in which its valuation appears expensive amid consensus estimates that do not fully appreciate the underlying fundamental opportunity. Over 50% of cash flows are derived from Botox and dermal fillers, positioning GALD in a duopoly market with a wider moat and longer growth runway than traditional beauty peers. GALD's core skincare business is growing ~10% annually (relative to L’Oreal’s sub-5% revenue growth), driven by exposure to higher value, nascent life cycle segments. The investment case is further supported by the company’s new eczema treatment, Nemluvio, which could generate $5bn+ in sales vs. management’s $2bn guidance. TP CHF230 (60% upside).

Edition: 220

- 19 September, 2025

Industrials

FAN stands out as a high quality (29% FY24 FCF RoE) mid-cap building products and business services company that has bucked the trend of sluggishness across its core markets. The business has had a very successful buy-and-build strategy, using excess FCF and modest leverage to undertake earnings accretive M&A. The recent acquisition of Fantech exemplifies this and Fighting Financials thinks consensus estimates underestimate the full benefits of this deal. Beyond fundamentals, FAN also fits the profile of UK SMID-caps attracting takeover interest with 1) geographically diversified revenues; 2) high returns on capital; 3) modest leverage; and 4) suffering a discount due to trading on the troubled UK market.

Edition: 220

- 19 September, 2025

Technology

86Research attended Kuaishou’s Investor Day in Chengdu, where management highlighted how AI is boosting engagement and monetisation across its core community while scaling Kling AI. OneRec has already lifted time spent and GMV, with full rollout and ecommerce upgrades ahead. Management frames Kling as a sustainable long-term business in a US$140bn video market, though further proof points are still needed.

Edition: 219

- 05 September, 2025

Consumer stocks poised for a recovery

Consumer Discretionary

AIR expects a wave of upward revisions from European corporations in the coming months as tariff clouds thin, China stabilises, infrastructure spend ramps up and European rates remain low. The missing piece is consumer confidence, which should rebound quickly if geopolitical tensions ease. Consumer names like Inditex, Stellantis, LVMH, Diageo, Kering, Adidas, Nestle and Unilever look compelling after steep share price declines, with valuations back to decade-lows. Many of these firms are pursuing clear turnaround strategies focused on FCF generation, deep efficiency gains (utilising AI) and renewed focus on core businesses - supported by a trend toward insider CEO appointments, after a decade of appointing outsiders.

Edition: 218

- 22 August, 2025

Consumer Staples

Scott Mushkin downgrades DG to Sell, citing widening price gaps with competitors, which threaten margins and volume share gains over the next 12-18 months. R5’s latest fieldwork shows a total basket premium of 9% vs. Walmart - well above the typical 3-7% range. Scott now sees pressure from WMT starting to impact the back half of 2025; while Amazon’s push to speed up delivery times in rural areas, coupled with its low pricing for everyday essentials also appears be gaining momentum. At the same time, Dollar Tree is making inroads into DG’s core markets. Finally, regulatory risks from SNAP eligibility changes and the MAHA movement targeting sugary foods are expected to negatively impact sales.

Edition: 217

- 08 August, 2025

Quantum computing primer unveils two new Buy ideas

Technology

Rosenblatt initiates coverage on D-Wave (Buy, $30 TP) and IonQ (Buy, $70 TP), identifying them as differentiated, high-conviction ideas in the rapidly expanding quantum computing market. QBTS offers unique exposure to quantum annealing - particularly suited for optimisation workloads - and is expected to grow revenues at a +66% CAGR from 2025-2030. IONQ, a leader in trapped-ion architectures, is positioned to exceed $1bn in revenue within the next few years, with significant upside from its product roadmap and ecosystem development. These initiations are framed by Rosenblatt’s comprehensive quantum computing primer, which outlines the core principles, architectures and commercialisation pathways shaping the industry’s next era and underpins the firm’s bullish stance on both names.

Edition: 217

- 08 August, 2025

Data centre market outlook

Real Estate

Kolytics’ report, the first in a series on the data centre sector, examines how the landscape is evolving amid surging AI-driven demand, mounting infrastructure pressures and a shift in focus from compute capacity to power availability. As the AI revolution transitions from hype to application, investor attention is shifting from core performance to grid access as the primary constraint. While current market conditions remain favourable and landlords benefit from pricing power amid grid bottlenecks, elevated valuations leave limited room for execution missteps. Risk-adjusted opportunities remain attractive; however, the materialisation of substantial downside risks could swiftly reshape the outlook. REITs covered include Digital Realty, Equinix and Iron Mountain.

Edition: 217

- 08 August, 2025

Consumer Discretionary

John Zolidis reiterates his bearish view on CAKE, warning that the multi-year tailwind from aggressive menu price hikes is ending. From 2023-2025, the company raised prices by over 20%, boosting restaurant-level margins to an 8-year high despite a ~5% decline in traffic. However, pricing is set to decelerate to 3.5% in 2H25 (vs. 4.0% in H1) and that slowdown doesn’t account for the rollout of new, lower-priced menu items. Meanwhile, non-core concepts continue to dilute margins. After reviewing Q2 results, which featured a 1.2% comp and 7% EPS growth (the slowest in 3 years), John sees little justification for the stock’s 30% rally over the past 3 months.

Edition: 217

- 08 August, 2025

Materials

WCC has issued a positive profit alert, forecasting 1H25 net profit to rise 80-100% Y/Y. Lucror reiterates a Buy on the WESCHI 4.95% 2026s at 90.5 / 16% YTW / 0.9Y, noting the attractive yield for a short holding period. The bonds have rallied ~10 points since mid-Jun, supported by Xinjiang asset sales, which enable WCC to repay over one-third of the USD 600m notes. A tender offer and new issuance could follow. Further non-core disposals in Guizhou and growth in African operations may improve refinancing flexibility and recovery value. Despite expected negative FCF in H1 due to capex and acquisitions, fundamentals are improving.

Edition: 216

- 25 July, 2025

Consumer Discretionary

Once a top post-Covid long idea, EXPE has ceded leadership to peers and the broader travel industry. Hedgeye believes the bull thesis - centred on margin expansion, mix shift and market share stability - has grown stale and is now reversing. Investors are 1) underestimating the magnitude of near term deceleration in the core B2C platform, 2) underestimating EXPE’s exposure to regional demand issues and incremental competition, 3) overestimating EXPE’s ability to leverage marketing and drive higher margins, and 4) significantly overestimating EXPE’s ability to maintain (or even grow) share of the total accommodation market in the coming years. While the stock screens as cheap, the risk/reward still skews negative, especially compared to Booking, their preferred long in Online Travel. Hedgeye's EXPE target price offers ~30% downside.

Edition: 215

- 11 July, 2025

Colombia: A shock to the downside

The Pacifico Research team interpret June’s inflation reading with caution. The monthly variation was at the lower end of Bloomberg’s survey forecasts for the second consecutive month. However, the most significant monthly declines were concentrated in volatile components such as perishable food and energy. As a result, the normalization of core inflation is proceeding more slowly than that of headline CPI. While the slowdown in monthly inflation aligns with seasonal patterns, this was the lowest June figure since 2021. Of the volatile downward contributions, the most significant was electricity, but this should see a less pronounced decrease in July. Food was also a contributor, as expected, but rent saw a downside surprise. Looking ahead, this result introduces a downward bias for July inflation due to the high weight of effective and imputed rent, which together account for 25% of the CPI basket, while also increasing the degree of uncertainty.

Edition: 215

- 11 July, 2025

Argentina: Three scenarios for FX and inflation

Inflation in May was below expectations again and core price inflation decelerated. Inflation was 1.5% MoM. Inflation in June will be in the vicinity of 2% MoM, according to Marcos Buscaglia’s estimates. As a result, national inflation may drop below 40% YoY for the first time since March 2021. The government is prioritising the reduction of inflation over other objectives such as the purchase of reserves. With this in mind, Marcos lays out three scenarios for the FX and inflation until yearend. In the baseline scenario (50% probability), the peso weakens but remains inside the target band, in the risk scenario (20% with upside risks) it jumps to the top of the band, and in the government-preferred one (30% with downside risks) it weakens very mildly. In the baseline scenario, inflation remains contained at or below 2.5% MoM, but it stops declining, ending 2025 near 32%.

Edition: 214

- 27 June, 2025

What’s trending in Retail

Consumer Discretionary

Each week, The Retail Tracker offers an insightful perspective on retail, fashion and consumer trends and what it means for the stocks. So far this year, Garage is a standout, nailing the “sexy x comfy” aesthetic for teens and taking share from Aerie and Pink. Gap and Old Navy are “crushing it” with consistently strong assortments, offsetting tariff challenges through fewer markdowns. Meanwhile, Urban Outfitters and Nuuly are gaining traction, with Nuuly emerging as a promising rental and tech-driven play. Aritzia is showing good momentum with its best assortment in some time. Department stores may be in free fall, but the best Macy’s stores have never looked better. In contrast, Lululemon is losing its way, expanding beyond its core and diluting its brand identity, while Bath & Body Works' range of new items is exhausting.

Edition: 214

- 27 June, 2025

Consumer Discretionary

Gordon Haskett Research Advisors

Chuck Grom maintains a Buy rating on FIVE following a strong 1Q25, with 7.1% SSS growth and $0.86 EPS, both ahead of guidance. The company's swift turnaround, driven by leadership changes and a return to core strengths in merchandising, marketing, value and customer experience, has exceeded expectations. Traffic growth (6.2%) and broad-based sales gains support Q2 SSS guidance of 7-9%, which Chuck sees as potentially conservative by ~300bps. He believes FY25 EPS could plausibly exceed $5.50. FIVE stands out as one of the few names he covers that can strongly argue the case for both EPS upside and a higher multiple.

Edition: 213

- 13 June, 2025

Japan: Inflationary habits

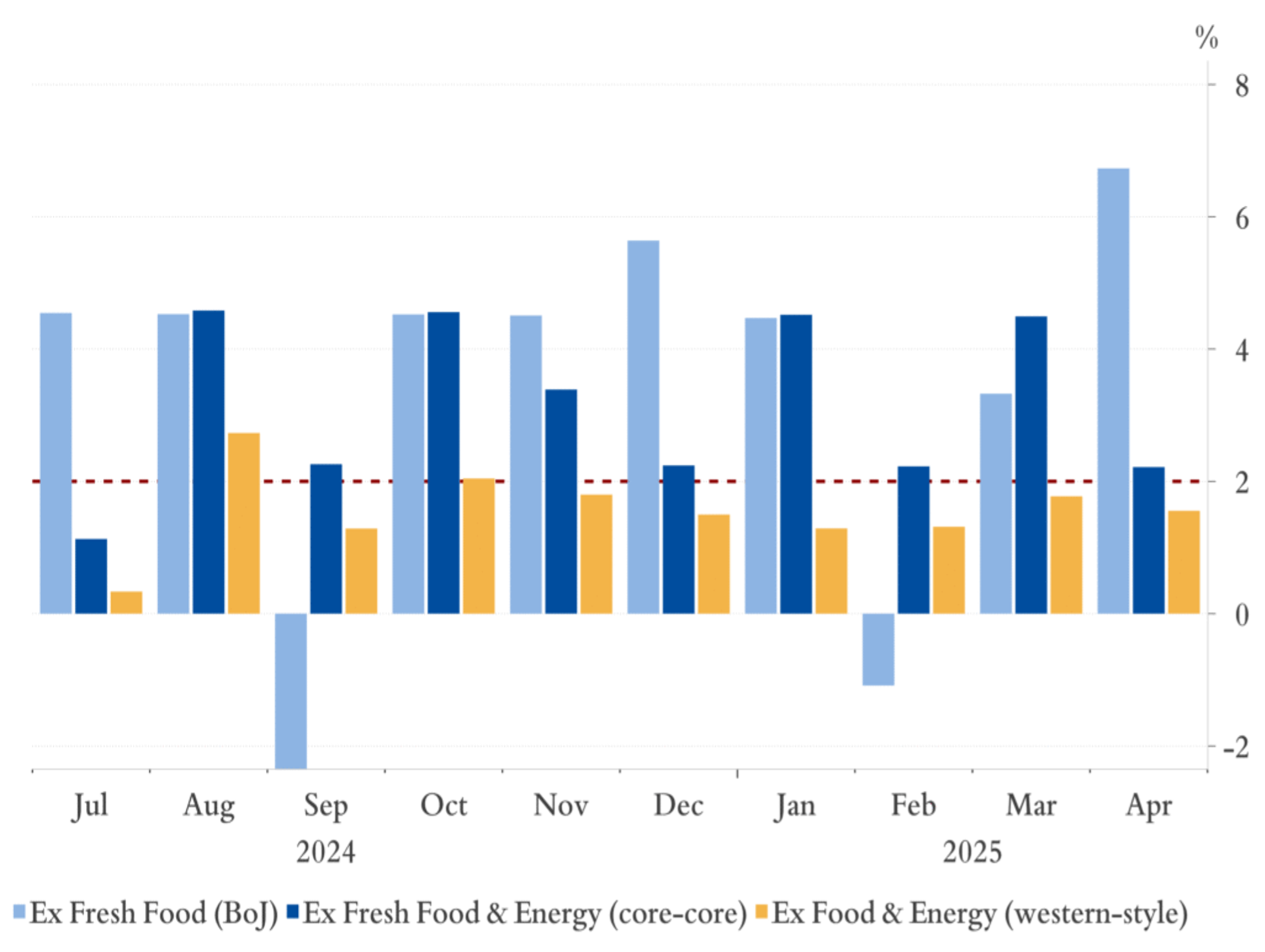

Riccardo Trezzi’s models suggest that Japan is experiencing a persistent inflationary trend, around the BoJ’s 2% target. Riccardo estimates that in April, the BoJ’s core index (excluding fresh food) rose 6.7% MoM SAAR (see chart). As for the other two core inflation measures, the index excluding fresh food and energy (core-core) increased 2.2% MoM SAAR, while the index excluding both food and energy (US-style core) rose 1.6% MoM SAAR. Given potential seasonal adjustment distortions, Riccardo continues to emphasize looking at NSA levels, which suggest that price pressures remain persistent and even higher than last year. His models remain well above the BoJ’s forecasts for core-core in FY2025 and FY2026, with the central bank’s current forecast implying an unrealistic average MoM of less than 10bps sa for core-core this year.

Edition: 212

- 30 May, 2025

Crypto: Soaring higher

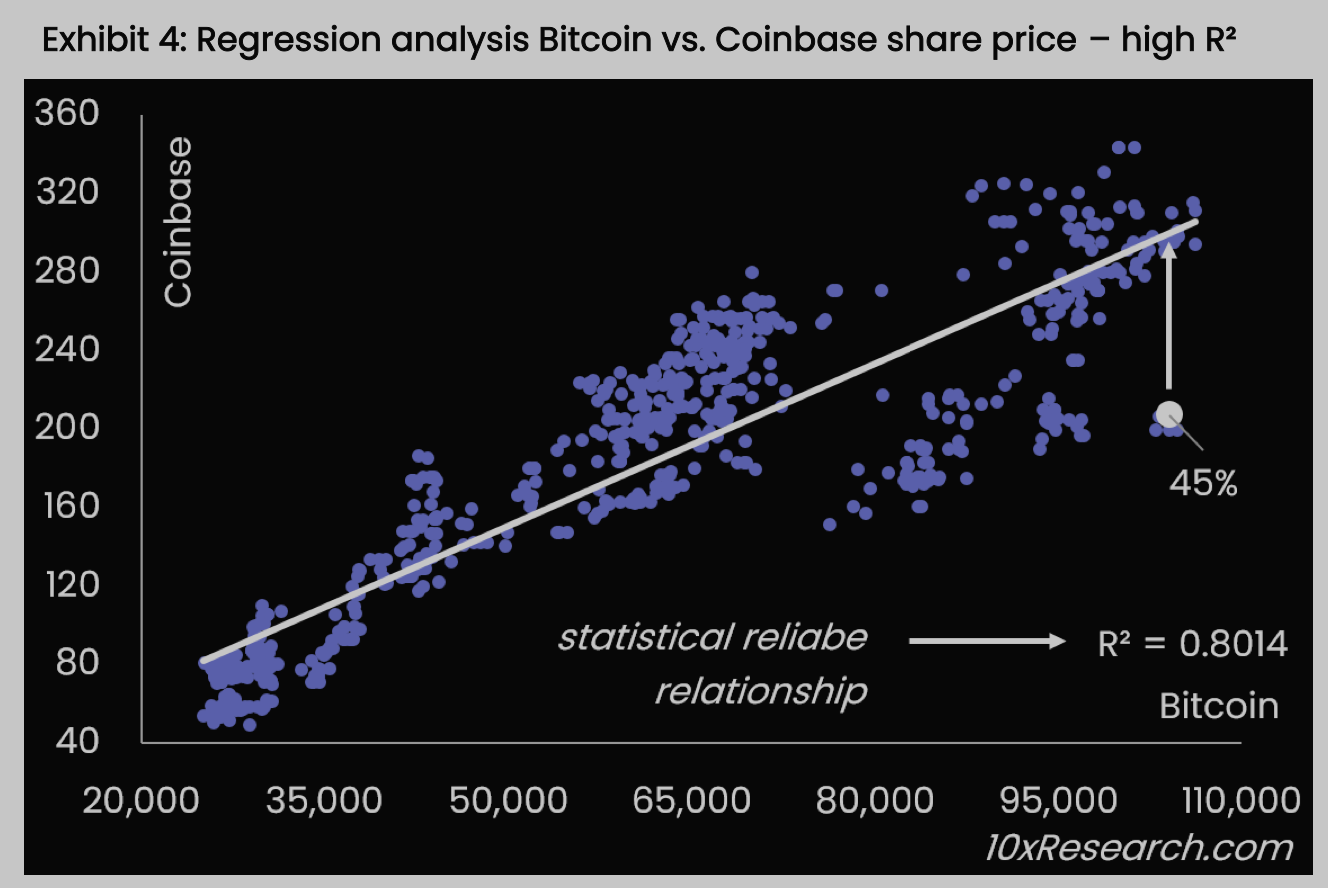

Bitcoin's explosive +160% rally since January 2024 has exposed the fragile economics of Bitcoin miners, with most struggling to keep pace. 10x Research reveals that only a few miners, such as Core Scientific, which achieved +187% gains, have outperformed Bitcoin, while others face rising costs and declining profitability. In contrast, Coinbase offers a more compelling opportunity, with a clear correlation between its stock price and Bitcoin, making it a better play in the current market; their regression with Bitcoin analysis reveals a potential upside of +45%. The team also recommend a spread trade: long Bitdeer vs short Marathon Digital. As Wall Street eyes crypto IPOs worth $100 billion, the stakes have never been higher for the crypto industry.

Edition: 211

- 16 May, 2025

Feeling Chile

Chile is entering electoral mode, with candidates competing for support, but over half of voters remain undecided. While voters may punish the outgoing leftwing administration, the moment is ripe for an anti-elite candidate with a law-and-order, pro-growth message. Marcos Buscaglia has revised his 2025 GDP growth forecast to 2.1% from 1.9%, despite expecting a slowdown in the second half. Inflation surprised to the downside at 0.2% month-on-month (vs. 0.3% expected), but core prices rose, and the fiscal anchor remains under pressure, suggesting inflation is likely to exceed consensus. Although some expect rate cuts, Marcos believes the central bank should maintain or raise rates to restore its lost inflation anchor, as his Taylor Rule model does not support cuts. However, with the central bank considering a 25bp cut at its last meeting, a reduction remains plausible.

Edition: 211

- 16 May, 2025

Shell: To Be(P) or not to Be(P); that’s the question

Energy

Analysts at the IDEA! weigh in on media speculation about a potential Shell acquisition of BP. While Shell has the financial strength to pursue a deal, acquiring BP would involve taking on its $77bn of debt and other long-term liabilities, including those from the Deepwater Horizon spill. Although synergies are possible, integration would be costly and could disrupt Shell’s shareholder returns, which is key to closing its valuation gap with US peers. The deal would also bring in non-core assets and regions Shell has been moving away from, along with notable cultural differences. the IDEA! suggests caution and favours Shell sticking to its current strategy or exploring other deals instead.

Edition: 211

- 16 May, 2025

Consumer Discretionary

Another miss, another excuse - this is now the 4th consecutive quarter that DKNG has missed on revenue. This is also the 7th consecutive quarter where Sports Outcomes were a y/y headwind to revenue growth. As a bookmaker, DKNG’s core job is to set odds and it is become increasingly worse at doing so. Hesham Shaaban remains bearish, expecting management will have to cut 2025 guidance (again); noting it relies on the same flawed assumptions as 2024, which was revised down twice. Management also assumes 2024’s negative comps will become 2025 tailwinds, despite two consecutive quarters of poor results. Structural issues will become more evident now that DKNG is working with a slowing inorganic tailwind from new state launches.

Edition: 211

- 16 May, 2025

Communications

META is doubling down on AI infrastructure, raising its 2025 capex forecast to $64–72bn as it accelerates data centre construction amid rising costs. CEO Mark Zuckerberg is committed to making META a leading AI platform and insists on building in-house capacity to avoid reliance on others. While the AI strategy (centred on open source) is progressing well, it comes with a steep price tag, notably the ongoing $4bn+ quarterly burn at Reality Labs. Richard Windsor sees a growing risk of AI infrastructure overbuild, with META, Google, Microsoft and Amazon all ramping up spend - setting the stage for a painful correction. Despite this, META’s core business remains solid, with strong Q1 performance and improved operational efficiency via AI. At 23.5x FY25 PER, META is reasonably valued, but Richard prefers Google, where AI disruption risks from players like OpenAI are, in his view, overstated.

Edition: 210

- 02 May, 2025

Consumer Discretionary

Looking out over the NTM, whether trade deals are made or not, Brian McGough thinks LULU's earnings power lands closer to $10 than the Street's $17+ and that the current narrative around high growth in China / RoW offsetting North American weakness dissipates, as a +30% revenue growth number gets more than cut in half and the continued weakness in the core US model rears its ugly head. In that context, a peak margin gets slashed, McDonald gets fired and the company sees a major restructuring / cost cutting programme to prop margins and save face… but, not before the stock is trading at 15x a $10 earnings number. Brian still sees 50% downside from current levels.

Edition: 209

- 18 April, 2025

US: The Fed is far behind the 8 ball

Higher unemployment expectations have flared to extremes. In five of the six previous instances when UMich Higher Unemployment Expectations first crossed the 60% threshold, real GDP contracted four quarters out by an average of -0.8% YoY; despite this, the Fed’s median projection for 2025 GDP growth sits at 1.7% YoY. Regardless of the evolving core inflation narrative, the Fed has responded to economic hardship on par with the current episode in previous cycles with aggressive easing actions. With just two rate cuts expected and priced by year-end, investors are not prepared for a repricing that would validate the historical context. Every single cycle following a crescendo in UMich Higher Unemployment Expectations saw the Fed funds rate cut by more than a full point 4 quarters out; clearly, the Fed, rates traders and sell-side alike are all out of step with history.

Edition: 207

- 21 March, 2025

A strong core Europe equals a higher centrifugal force

Europe’s cyclical outlook has improved with its adoption of an expansionary fiscal posture. Stephen Jan and Fatih Yilmaz say that investors should be favourably inclined towards EUR assets, including the currency. They think EUR/USD could test 1.20 this year. However, investors should also be mindful of all the structural flaws that will one day return to haunt these same assets if they are not fixed. Stephen and Fatih are cyclically positive but remain structurally cautious on Europe. They suspect the intra-European divergences may widen in the coming years as core economies like Germany outrun the peripherals. The bullish European market narrative is a nuanced one.

Edition: 207

- 21 March, 2025

Technology

YOU's KPIs are continuing to deteriorate, its ancillary businesses are not demonstrating meaningful revenue generation and its 1Q25 bookings guidance was notably weak. Relationships with key partners are fraying and YOU's CFO abruptly announced his departure. OWS maintains their view that YOU is a company whose core business is facing an existential structural challenge from TSA PreCheck’s new Touchless ID verification system and has limited optionality with which to respond. They believe this view has yet to be fully recognised by the group's growth-technology oriented investor base and therefore continue to encourage clients to short the stock. TP $16 (40% downside).

Edition: 207

- 21 March, 2025

The Power of Perspective: The Intelligent Investor’s Framework

Omaha Insights employs a systematic and rigorous approach to restating reported financial data, examining shifts in accounting standards and incorporating economic adjustments, thereby providing clients with an accurate view of a firm's underlying economic performance. At the core of this methodology lies their unique Competitive Lifecycle framework, which underpins their ability to generate powerful, actionable insights into equity risk and anticipated returns. Beyond precise financial restatement, Omaha’s platform equips clients with a customisable “lens” through which they can tailor financial analysis to align with their specific investment philosophy and strategic objectives. This approach allows for a uniquely personal perspective on data, empowering clients to uncover information in ways that traditional analysis might miss. Click here for further details.

Edition: 206

- 07 March, 2025

Navigating a multi-polar fragmented world

Craig Ferguson’s core macro/AA view says a 40yr disinflation cycle ended in 2020 and that a new multi-decade inflationary cycle began. This has seen cash rates rise, global growth slow, rates get cut and inflation fall. At the start of 2025 Craig points out that we are now near the end of the first up (2020/22) and down (2023-24) cycle, so a new cycle may be starting. Craig’s takeaway from his detailed analysis of US/Trump geopolitical & economic policy is to expect stagflation forces to unfold and impact AA portfolios during 2025-28… For now, Craig says we need to face up to the notion that markets are priced for perfection in an uncertain and fragile geopolitical, economic and military world. The new order may last decades, and investors need to position their asset allocations for this important change.

Edition: 206

- 07 March, 2025

Consumer Discretionary

Corto anticipates further declines as FTDR’s share price crashes post earnings - despite a Q4 revenue beat, most upside came from the 2-10 Home Buyers Warranty acquisition, with organic growth at just 3% (management guided for long-term organic growth in the HSD range, which seems like a stretch absent a sharp improvement in the housing market). Excluding A/C replacement revenue, core revenue declined in Q4, casting doubt on the company’s 2025 organic growth target. FTDR added 170k service plans, but without 2-10 HBW, service plans declined by 3%, continuing a downward trend since 2021. Membership trends also remain weak given the company's increased spending on sales and marketing.

Edition: 206

- 07 March, 2025

A search for big returns in small packages

Last Apr, KCR highlighted the remarkable opportunities in micro cap stocks. Their portfolio was a group of ignored and overlooked companies that typically had prodigious cash-flows and healthy growth runways, and despite delivering an impressive 21% return, KCR continues to source wildly mispriced (too cheap) stocks. Their Micro Cap Model Portfolio has a FCF Yield of 10% vs. the Russell 1000 Core ETFs’ holdings FCF Yield of <3%; suggesting powerful upside returns with a much higher margin of safety than the expensive and concentrated large cap index funds. A recent addition is ScanSource, which has transformed itself into a leading hybrid solutions provider by combining traditional technology hardware with cloud-based solutions. While headwinds have hampered sales recently, SCSC is generating solid cash flow and KCR thinks the stock can potentially double.

Edition: 205

- 21 February, 2025

Euro Area Inflation – Core HCIP at 2.5% in January

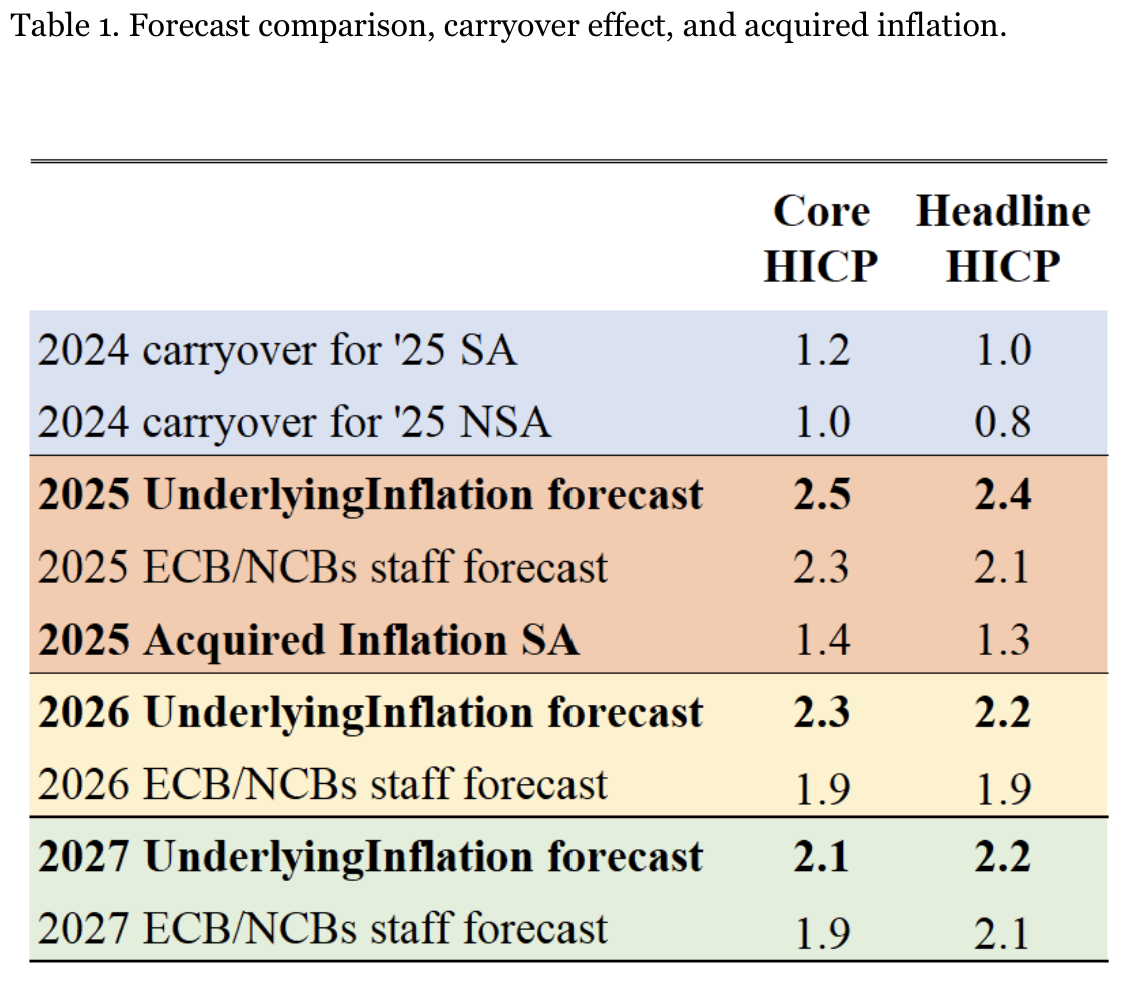

As expected, Euro Area services inflation remains a concern. The flash release for the HICP (Harmonized Index of Consumer Prices) in January came in as Riccardo Trezzi expected. Riccardo points out that the broader issue remains unchanged: there’s still no sign that services inflation is slowing, having followed its 2023 trajectory throughout 2024 with no signs of the pattern ending yet. Riccardo remains skeptical that a significant slowdown is imminent and he expects inflation to remain sticky in the near term. His models continue to project inflation above the ECB/NCBs staff forecasts. The big picture hasn’t shifted. On one hand, there’s no certainty that it will return to target. On the other, concerns about growth and trade tensions persist—yet the ECB remains focused solely on the latter.

Edition: 204

- 07 February, 2025

Abu Dhabi Commercial Bank (ADCB UH) United Arab Emirates

Financials

ADCB’s share price has already risen ~40% since Fighting Financials turned bullish in Jul 24, yet they continue to anticipate further upside. The company last week announced its intention to double profits in the next five years. This doesn't seem unreasonable given it doubled profits in the last five years and has good momentum today, having grown PBT at +26% in FY24 y/y. However, consensus is still modelling only mid-single digit annual EPS growth across FY25e and FY26e. ADCB also benefits from the UAE's dollar peg, low tax, geopolitical neutrality and a higher oil price. Fighting Financials core portfolio was up 15% in 4Q24 and is currently +6% YTD with ADCB a key contributor.

Edition: 204

- 07 February, 2025

EM Exchanges: Brazilian exchange B3 stands out

Financials

Galliano's Financials Research

Victor Galliano sticks with B3 as his core value pick; it has a growing share of data revenues, its post-trade revenues are understated and equity fee pressure is easing. He keeps Hong Kong Exchange as a buy, with its high share of post-trade revenues; its shares have been highly volatile, but represent relative value combined with growth potential. Philippine Stock Exchange and BSE are new additions to Victor’s coverage of EM exchanges with PSE being one to watch; MexBolsa is deep value but lacking a re-rating catalyst.

Edition: 203

- 24 January, 2025

Consumer Discretionary

The shares are not cheap, trading at a 4% FY25E FCF yield. However, this is for a company with significant long-term pricing power, a track record of double digit revenue growth and no debt. Consensus forecasts imply growth turns negative in H2, but Fighting Financials thinks this is unlikely and anticipates upgrades to FY numbers. Ultimately, they like the opportunity mainly as a hedge to a book of UK shorts. In FY24, only 22% of the group’s core revenues were UK-based, with 44% derived from North America. With the strong USD likely to persist, they see GAW as a rare example of quality and therefore a relative winner in an otherwise troubled and low-growth UK stock market.

Edition: 203

- 24 January, 2025

Consumer Discretionary

EXPE has gone to great lengths to showcase its “industry-leading” B2B business, but this segment is only 30% of revenue and y/y growth just slipped below 20% for the first time since 2021, so it can only obfuscate weakness in the group’s core US lodging business for so long. Hesham Shaaban expects core declines to become more evident if his Revenge Travel Hangover theme manifests. He also plans to be short in force into the next print, especially given EXPE has a history of setting aspirational 4Q targets into year-end. It has missed 4Q revenue estimates twice in the past 3 years and the stock has also traded down on 4Q results each of the past 4 years.

Edition: 200

- 29 November, 2024

China: Easing the surge

Diana Choyleva expects Chinese equities to rise in coming quarters, with Beijing actively managing the pace to ensure sustainable multi-year gains rather than speculative surges. China placed equities support at the core of its unexpected stimulus package with two new tools: a Rmb500bn central bank swap facility and Rmb300bn re-lending facility. If the policies are successful, the authorities pledged to expand these tools, which could bring the overall size of equity market support to Rmb2.4trn, comparing favourably with the Rmb1.6trn of national team buying in 2015. As Diana argued in September, this is as close to the Chinese authorities saying, "whatever it takes" and will help unleash greed. But the authorities want to attract professional investors and institutional capital, not retail-driven speculative volatility. They appear to have learnt from past boom-bust cycles and are prioritising stable wealth creation over short-term excitement.

Edition: 200

- 29 November, 2024

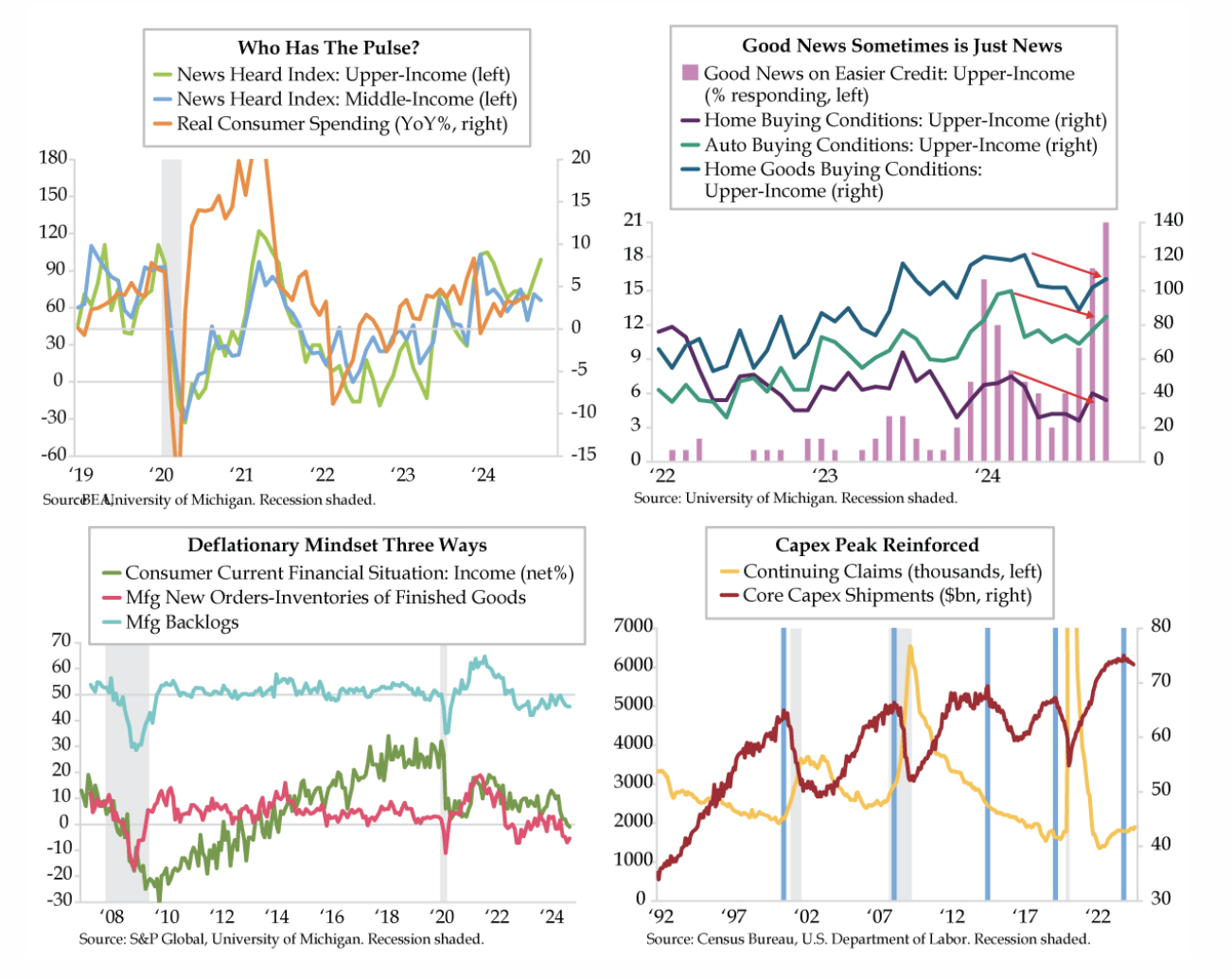

US: Rate optimism collides with capex pessimism

Surging good news about easier credit has improved upper-income households’ collective mood. That optimism has not, however, translated into improved top earners’ big-ticket purchases. Buying conditions for homes, autos, and home goods remain impaired, and households’ current financial situation related to income turned negative for the first time in a decade. A developing deflationary mindset from consumer finances and the factory sector reinforces the peak in capex occurring as the labour market continues to loosen; core capex shipments fell -0.3% MoM in October, below the flat consensus and the sixth loss since January. Investors should be mindful of these fundamental risks for the consumer discretionary cycle.

Edition: 198

- 01 November, 2024

Healthcare

Paragon’s analysis of CEO Bryan Hanson includes interviews with ten former colleagues who worked with him at Zimmer Biomet, Covidien and Medtronic for 110 years, combined. Sources (6 positive, 2 negative, 2 neutral) focused on his strengths as a builder of culture and teams. He begets loyalty in those who work with him, has a high level of transparency and strong communication skills. In fact, his focus on company culture may overshadow other areas, as he and those around him can become absorbed in the excitement of cultural transformation and big-picture ideation at the expense of more disciplined strategy. All the same, Hanson will take a portfolio management approach to SOLV, honing core areas of the business through both divestments and tuck-in acquisitions.

Edition: 196

- 04 October, 2024

Financials

Galliano's Financials Research

Hana Financial did not make the cut for the Korea Value-up Index announced on 24th Sep as it apparently fell short of the PBV ratio threshold. Despite being excluded from the Index, Hana is Victor Galliano’s core South Korean bank pick for its attractive valuations, low PEG, solid core capital ratio and strong credit quality credentials. He believes it stands out positively on fundamentals and return trends vs. its peers, while there is also potential for its inclusion in a planned rebalancing scheduled in Dec.

Edition: 196

- 04 October, 2024

Healthcare

PODD is on the cusp of a new product cycle for Omnipod 5 for diabetes 2 patients which will drive upside to 2H24 and 2025 consensus estimates. Abacus also argues the market’s GLP-1 fears are overplayed (impact will be negligible over the next decade / have no impact on type 1 diabetes, PODD's core customer). If this is proven, the multiple should expand. Although competitors Medtronic and Tandem will launch new products over next few years, their success is not guaranteed. For now, Omnipod has a first mover advantage. Abacus sees a path to $3.6bn in 2027 revenues (2023-27 CAGR of 21%) and an EPS of $6.50 (25% CAGR).

Edition: 195

- 20 September, 2024

China Banks: Opportunities among the credit quality challenges

Financials

Galliano's Financials Research

Victor Galliano screens 10 China banks, including the “Big Four”, using his proprietary database to build bank metrics up-to the 2Q24 results season. He examines the banks’ core profitability and their credit quality metrics to better identify banks that are attractive value, have good earnings growth prospects and have the potential to deliver healthy returns, even in the face of a potentially tough credit quality cycle in China. China Construction Bank is a core GEM bank Buy for its deeply discounted valuations and strong balance sheet; Ping An Bank is the deep value contrarian pick; China Minsheng Banking is Victor’s fundamental Sell.

Edition: 195

- 20 September, 2024

China’s trust sector problems continue to pile up

Over a third of Chinese trust companies are technically insolvent or are on the brink. Jonathan Anderson points out that although the asset quality situation did not worsen in 2024, the longer-term issues look problematic. The core asset quality issues facing trust companies still revolve around the real estate sector, but at the same time an upswell in local government financing vehicles is also causing pain. The good news is that the impending collapse of many trust companies is unlikely to be a catalyst for broader financial contagion. There may also be some good news around the corner, with government efforts to reduce unsustainable deposit inflows beginning to bear fruit. The beneficiary of this shift so far appears to be credit bonds vis inflows into bank wealth management products, but other investment managers will likely benefit.

Edition: 192

- 09 August, 2024

Beauty retail disruption

Consumer Discretionary

Ulta share losses accelerate as Sephora, TJX and Amazon are set up to win in US Beauty this fall / holiday. Q2 was a bloodbath at Ulta with historical promotional levels and muted traffic vs. Sephora. Amazon Prime Day highlighted new, exclusive product and the migration of prestige & luxury brands. TJX's core beauty presence continues to ramp up as holiday approaches. At the current level of execution, H2 appears bleaker than guidance.

Edition: 192

- 09 August, 2024

Technology Spending Intentions Survey

ETR’s July 24 TSIS saw participation from 1768 IT Decision-Makers, including 293 Fortune 500 and 419 Global 2000 organisations. Highlighted vendors include:

Equinix (EQIX) - rising sector and vendor-level spending intent places EQIX in a dominant position among peers, as the vendor seems well-aligned with broader IT spending and ML/AI trends, warranting ETR’s first-ever positive outlook on the data set.

Salesforce (CRM) - souring spend intent for its core Enterprise Apps business, in tandem with overall Net Score in Cloud Computing registering sharp declines, warrants a negative outlook.

Varonis (VRNS) - Negative outlook. ETR has observed a clear declining trend in spending intentions for two years, with an even lower Net Score among the Global 2000 and a sharp rise in Replacement intentions among existing customers.

Edition: 191

- 26 July, 2024

Industrials

Investors seem to believe the business is more cyclical than it is causing OC to trade at a far steeper discount to the market than it deserves. Management has successfully raised prices and controlled costs meaning its financial results look more like those of a growth company. Yet its shares trade at <14x earnings and an EV/Adjusted EBITDA of just 7.3x. Both figures represent >40% discounts to the S&P 500 Index. KCR also finds it notable that both their Large Cap Value and Large Cap Core models rank OC in the top 100 despite significantly different loadings. When a stock is highly ranked across models with divergent mandates, it signifies greater potential interest across the investor base.

Edition: 191

- 26 July, 2024

Special Situations Idea Forum

The majority of stocks presented at MYST’s latest buy-side event had very near-term (<6 months) catalysts to unlock value either through business transformations, fundamental business inflections, M&A / spin-off activities, or “technical” tailwinds. Ideas included:

Core Scientific (CORZ) - Bitcoin mining conversion provides “shortcut” to new data centre capacity. TP $18 (85% upside).

Golar LNG (GLNG) - “Orphan stock” nearing closure of multiple lucrative long-term FLNG vessel contracts. TP $75 (145% upside).

Jacobs Solutions (J) - Long-awaited exit from “deal purgatory” to finally showcase fundamental strength. TP $180 (30% upside).

Teck Resources (TECK) - Coal divestiture creates significant re-rate potential / M&A optionality. TP $65 (35% upside).

Edition: 189

- 28 June, 2024

Abu Dhabi Commercial Bank (ADCB UH) United Arab Emirates

Financials

The share price has risen more than 150% post Covid, but AlphaMena still sees over 30% upside. Strong 1Q24 results were reassuring and AlphaMena remains confident about ADCB’s business model based on the expansion of its core businesses powered by digitisation, portfolio de-risking and disciplined cost management. The lender also possesses the highest rating on AlphaMena’s Fundamental Strength Indicator, a set of metrics that help gauge stocks on their financial and operating performance. The stock continues to trade at a discount to its 2019 P/B while the organic capital generation has noticeably improved. Finally, ADCB offers a generous payout (7% dividend yield).

Edition: 189

- 28 June, 2024