Fortnightly Publication Highlighting Latest Insights From IRF Providers

Company Research

Outside of AI, why invest in the US?

US equities remain the world’s most important market, but passive benchmarks are distorted by AI concentration risk. Durable alpha lies in structural themes beyond AI. Power infrastructure (Constellation, Duke, NextEra) will benefit from grid bottlenecks as data centres drive demand. Re-industrialisation (Caterpillar, Honeywell, Rockwell) reflects reshoring and automation. The energy transition (Dominion, Enphase, ExxonMobil) requires trillions in capex. Housing scarcity (D.R. Horton, Home Depot, Lennar) is a structural imbalance. Healthcare innovation (Abbott, Eli Lilly, UnitedHealth) rides longevity and med-tech advances. Cybersecurity (Cisco, CrowdStrike, Palo Alto) is non-discretionary. Generational wealth transfer (BlackRock, Morgan Stanley, Schwab) reshapes capital flows. The AI productivity super-cycle is real, but thematic allocations across these shifts offer broader, smarter US exposure.

Edition: 220

- 19 September, 2025

AI driven 10Q / 10K text analysis

Since there are always reasons when companies change the wording in their financial filings, being alerted to these changes allows investors to realise potential risk factors and opportunities before they are reflected in the market. Recent alerts include: 1) AZZ - extension of credit to larger customers. 2) Constellation Brands - competitive pricing pressure. 3) DR Horton - changing long term expectation on debt to total capital ratio. 4) Moog - changing order demand in simulation and test products. 5) T-Mobile US - acquisitions of business with international exposure. 6) TriNet - change in stock repurchase expectations.

Edition: 210

- 02 May, 2025

Home Construction ETF (ITB)

Consumer Discretionary

Guy Cerundolo ranked and reviewed the constituents of the ITB and found a 10% reduction in the number of stocks with a bullish multi-factor model score from a 1-month look back. At the end of July, he had 79% of the constituents with a positive score compared to 69% now. Some of the stocks had a large negative step size drop in their score and the largest weighted stock in the ETF, DR Horton, is one of them - DHI's share price is beginning to show signs of weakness with both the absolute and relative uptrends being broken.

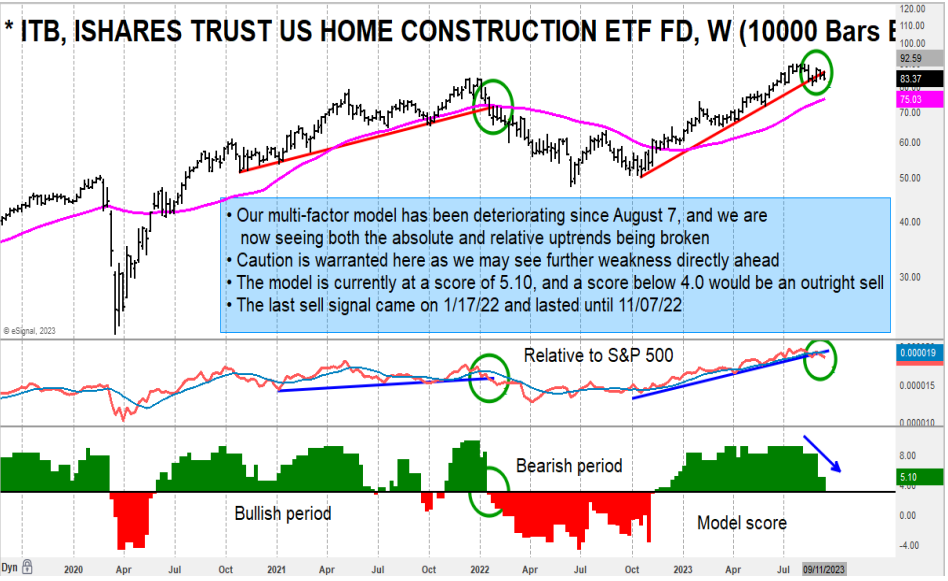

Edition: 169

- 15 September, 2023

Consumer Discretionary

2Q23 results smash expectations - Alex Barron believes FY23 will prove to be the trough in earnings. His EPS estimate for this year is $12.25 and sees it heading towards $18.00 in FY24. Alex considers DHI to be one of the two strongest companies in the industry and therefore deserves to trade at a much larger premium to the group in either P/E (currently at 8.0x based on his 2023 forecast vs. 14.3x for the group) or P/B (1.5x vs. 1.4x for the group) than it is currently trading at. He increases his TP from $117 to $167 (55% upside).

Edition: 159

- 28 April, 2023